The Car Loans Economy: Your Ultimate Guide to Navigating Automotive Financing

The Car Loans Economy: Your Ultimate Guide to Navigating Automotive Financing Carloan.Guidemechanic.com

The open road beckons, and for many, a car is not just a mode of transport but a symbol of freedom, independence, and necessity. However, the path to vehicle ownership often runs through the complex landscape of car loans. Understanding this intricate system, which we call the "Car Loans Economy," is crucial for both individual financial well-being and the broader economic health.

This comprehensive guide will demystify the world of automotive financing, offering insights into what drives it, how to make informed decisions, and its wider impact. Whether you’re a first-time buyer or looking to refinance, grasping these concepts will empower you to navigate the market with confidence and secure the best possible deal. Let’s embark on this journey together to unlock the secrets of the car loan market.

The Car Loans Economy: Your Ultimate Guide to Navigating Automotive Financing

The Engine Room: What Drives the Car Loans Economy?

The car loans economy is a dynamic ecosystem influenced by a multitude of factors, much like a finely tuned engine. Key components like interest rates, credit scores, and overarching economic indicators play pivotal roles in determining accessibility and affordability. Grasping these foundational elements is the first step toward smart auto financing.

The Power of Interest Rates

Interest rates are arguably the most influential factor in the car loans economy. They dictate the cost of borrowing money over time. When central banks raise their benchmark rates, it typically leads to higher interest rates across the board, including for auto loans.

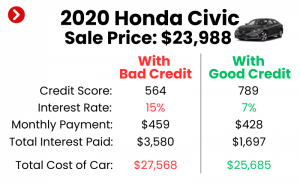

This direct correlation means that a slight increase in rates can significantly impact your monthly payments and the total amount you pay for a car. Conversely, lower rates can make car ownership more accessible and affordable, stimulating demand. Based on my experience, even a half-percent difference in an interest rate on a 60-month loan can save you hundreds, if not thousands, of dollars over the loan’s lifetime.

The Indispensable Role of Credit Scores

Your credit score acts as your financial report card, reflecting your history of borrowing and repayment. Lenders use this three-digit number to assess your creditworthiness and the risk associated with lending you money. A higher credit score generally translates to lower interest rates and more favorable loan terms.

Conversely, a lower credit score can result in higher interest rates, stricter terms, or even loan denial. This is why maintaining a healthy credit profile is paramount when entering the car loan market. Pro tips from us: Regularly check your credit report for errors and strive to make all payments on time to keep your score robust.

Broader Economic Indicators

Beyond individual credit and interest rates, macroeconomic conditions significantly shape the car loans economy. Factors like unemployment rates, consumer confidence, and inflation all play a part. High unemployment, for example, can lead to decreased consumer confidence, reducing demand for new vehicles and thus for car loans.

Inflation, on the other hand, can erode purchasing power, making current car prices feel more expensive. Lenders also adjust their risk models based on these indicators, influencing their willingness to lend and the terms they offer. A robust economy often sees a vibrant car loan market, while downturns can lead to tighter lending standards.

Navigating the Landscape: Types of Car Loans and Where to Find Them

Understanding the various types of car loans available and where to source them is crucial for making an informed decision. The car loans economy offers several pathways to vehicle ownership, each with its own set of advantages and considerations. Exploring these options will help you tailor your financing to your specific needs.

Direct vs. Dealership Financing

When seeking a car loan, you generally have two main avenues: direct lending or dealership financing. Direct lending involves securing a loan directly from a bank, credit union, or online lender before you even step foot in a dealership. This approach provides you with pre-approval, giving you a clear budget and strong negotiation power.

Dealership financing, conversely, is arranged through the car dealership itself, which acts as an intermediary connecting you with various lenders. While convenient, these loans may sometimes carry higher interest rates as the dealer often adds a markup. Common mistakes to avoid are accepting the first offer from a dealership without comparing it to a pre-approved direct loan.

New vs. Used Car Loans

The type of car you purchase—new or used—also influences your loan options. New car loans typically offer lower interest rates and longer terms due to the vehicle’s higher value and perceived reliability. Lenders view new cars as less risky.

Used car loans, while still widely available, often come with slightly higher interest rates and shorter terms. This is because used cars carry more inherent risks, such as unknown maintenance histories and faster depreciation. It’s essential to factor in the total cost of ownership, including potential repairs, when financing a used vehicle.

Leasing vs. Buying: A Brief Comparison

While not strictly a "loan," leasing is a significant part of the car loans economy as an alternative to outright purchase. When you lease, you essentially pay to use a vehicle for a set period, typically 2-4 years, rather than owning it. This often results in lower monthly payments compared to buying.

Buying, however, means you own the asset once the loan is paid off, building equity over time. Leasing might be ideal if you prefer driving a new car every few years and don’t want the hassle of selling a used vehicle. Buying is better if you plan to keep the car for an extended period and want to avoid mileage restrictions.

Refinancing Car Loans

Refinancing involves replacing your existing car loan with a new one, ideally with more favorable terms. This can be a smart move if interest rates have dropped since you initially financed your vehicle or if your credit score has significantly improved. Refinancing can lead to lower monthly payments, reduced total interest paid, or a shorter loan term.

Pro tips from us: Always calculate the total savings before refinancing, considering any potential fees for the new loan. It’s a great way to optimize your financial position within the car loans economy.

The Consumer’s Compass: Making Smart Car Loan Decisions

Navigating the car loans economy successfully requires more than just understanding the mechanics; it demands strategic decision-making. As a consumer, you hold significant power to influence your own financial outcomes. Arming yourself with knowledge and employing smart strategies can save you thousands over the life of your loan.

Understanding the True Cost

When evaluating a car loan, it’s crucial to look beyond the advertised interest rate and focus on the Annual Percentage Rate (APR). The APR includes the interest rate plus any additional fees, giving you a more accurate picture of the total cost of borrowing. A loan with a slightly lower interest rate but higher fees might actually have a higher APR.

Furthermore, remember that the "true cost" of a car extends beyond the loan itself. Factor in depreciation, insurance premiums, maintenance, and fuel costs. A seemingly affordable monthly loan payment might hide a much larger overall financial burden.

Budgeting for a Car Loan

Effective budgeting is the cornerstone of responsible car ownership within the car loans economy. A popular guideline is the "20/4/10 rule": make a 20% down payment, finance the car for no more than four years, and ensure your total monthly vehicle expenses (loan payment, insurance, fuel) don’t exceed 10% of your gross monthly income. While this is a guideline, it serves as a healthy benchmark.

Based on my experience, many people get into trouble by stretching their loan terms too long or putting too little down. A substantial down payment reduces the amount you need to borrow, thereby lowering your monthly payments and total interest paid. It also helps you avoid being "upside down" on your loan, where you owe more than the car is worth.

Negotiation Strategies

Negotiating a car loan isn’t just about getting a lower interest rate; it’s about the entire deal. Start by separating the car price negotiation from the financing negotiation. Secure your best possible car price first, then discuss financing options. Having a pre-approved loan offer in hand gives you leverage.

Common mistakes to avoid are focusing solely on the monthly payment. Dealerships can easily manipulate this by extending the loan term, which ultimately costs you more in interest. Always negotiate on the total price of the car and the APR of the loan. Be prepared to walk away if the terms aren’t favorable.

Reading the Fine Print

Before signing any loan agreement, meticulously read all the fine print. Look for details regarding prepayment penalties, late fees, and any mandatory insurance requirements. Some loans penalize you for paying them off early, which can negate the benefits of refinancing or making extra payments.

Understand what happens if you miss a payment and the specific terms of default. This due diligence ensures there are no unpleasant surprises down the road. Transparency is key in the car loans economy, and it’s your responsibility to seek it out.

The Broader Impact: Car Loans and the Macroeconomy

The car loans economy is far more than just individual transactions; it’s a significant force shaping the broader macroeconomy. Its ebb and flow can signal economic health, influence consumer debt levels, and directly impact one of the world’s largest industries. Understanding this wider context provides a holistic view of its importance.

Stimulus for the Automotive Industry

Car loans are the lifeblood of the automotive industry. They facilitate car sales, driving production, manufacturing, and employment across a vast supply chain. When access to affordable credit is robust, car sales tend to increase, stimulating economic activity from steel production to dealership services. This ripple effect supports millions of jobs globally.

Conversely, a contraction in the car loans economy, often due to tighter lending standards or higher interest rates, can significantly dampen car sales. This can lead to production cuts, layoffs, and a slowdown in the entire automotive sector, demonstrating its profound economic impact.

Consumer Debt Levels

While car loans enable mobility and economic participation, they also contribute significantly to overall consumer debt levels. When managed responsibly, this debt can be a productive tool. However, an over-reliance on car loans, particularly for expensive vehicles or with extended terms, can strain household budgets.

Excessive auto debt can limit consumers’ ability to save, invest, or absorb unexpected financial shocks. Policymakers and financial institutions closely monitor auto loan debt trends as an indicator of consumer financial health. Spikes in delinquencies can signal broader economic distress.

Economic Cycles and Car Loan Trends

Car loan trends often act as a barometer for economic cycles. During periods of economic expansion, consumer confidence is high, leading to increased demand for cars and, consequently, car loans. Lenders are more willing to extend credit, and interest rates might remain stable or even fall to encourage spending.

Conversely, during recessions or economic slowdowns, lending standards tighten, interest rates might rise, and consumer demand for new vehicles typically drops. This makes car loan activity a useful leading or lagging indicator for economists attempting to predict or confirm economic shifts.

The Regulatory Environment

The car loans economy operates within a framework of regulations designed to protect consumers and ensure fair lending practices. Government bodies and consumer protection agencies, like the Consumer Financial Protection Bureau (CFPB) in the United States, oversee auto lenders. They work to prevent predatory lending, ensure transparency in loan terms, and provide avenues for consumers to report issues.

These regulations play a crucial role in maintaining trust and stability within the market. For example, the CFPB offers resources and information on auto loans, helping consumers understand their rights and make informed decisions. External Link: Learn more about your auto loan rights from the CFPB

Future Forward: Trends Shaping the Car Loans Economy

The car loans economy is not static; it’s constantly evolving with technological advancements, shifting consumer preferences, and environmental concerns. Looking ahead, several key trends are poised to reshape how we finance vehicles, offering both new opportunities and challenges.

Digitalization of Lending

The digital revolution has profoundly impacted the car loans economy. Online lenders and digital platforms are making the loan application and approval process faster, more convenient, and often more competitive. Artificial intelligence and machine learning are increasingly used for credit scoring, allowing for more nuanced risk assessments and personalized loan offers.

This shift towards digital solutions is expected to continue, potentially democratizing access to auto financing and streamlining the entire car-buying journey. Consumers can now compare offers from multiple lenders within minutes, empowering them with more choices.

Electric Vehicles (EVs) and Financing

The accelerating transition to Electric Vehicles (EVs) is a significant trend impacting auto financing. EVs often come with a higher upfront cost, which can influence loan amounts and terms. However, various government incentives, tax credits, and specialized "green" loan products are emerging to make EV ownership more accessible.

Lenders are also beginning to factor in the lower running costs and potentially higher resale value of EVs into their loan offerings. For more on EV financing, check out our article on .

Subscription Models and Alternative Ownership

Beyond traditional buying and leasing, innovative ownership models like car subscriptions are gaining traction. These services offer access to a vehicle for a monthly fee that typically includes insurance, maintenance, and roadside assistance, without the long-term commitment of a loan or lease. While not a loan in the traditional sense, these models represent an alternative to financing a car.

This trend could challenge the conventional car loans economy by offering flexibility and convenience, particularly for urban dwellers or those who prefer not to shoulder the full responsibilities of ownership. The future may see a hybrid landscape where traditional loans coexist with these evolving alternatives.

Conclusion: Driving Forward with Financial Intelligence

The car loans economy is an indispensable, complex, and ever-evolving component of our financial world. From the individual decision to finance a vehicle to its macroeconomic implications, understanding its nuances is key to making empowered choices. We’ve explored the foundational drivers like interest rates and credit scores, navigated the various loan types, and discussed strategies for smart consumer decision-making.

Remember, the goal is not just to secure a car, but to do so on terms that support your overall financial health. By staying informed about market trends, diligently researching your options, and always reading the fine print, you can confidently navigate this intricate landscape. Your financial intelligence is your most powerful tool in the car loans economy.

Make informed choices, secure your ride, and enjoy the journey ahead. To dive deeper into personal finance and smart borrowing, explore our blog’s .