The Definitive Guide: Securing a Car Loan with a 550 Credit Score

The Definitive Guide: Securing a Car Loan with a 550 Credit Score Carloan.Guidemechanic.com

Facing the prospect of buying a car with a 550 credit score can feel like navigating a dense fog. Many people assume that such a score immediately slams the door shut on auto financing, leading to frustration and despair. However, based on my extensive experience in the world of personal finance and auto lending, I can confidently tell you that it’s not an impossible feat.

While challenging, securing a car loan with a 550 credit score is absolutely within reach. It requires a strategic approach, a clear understanding of the lending landscape, and a willingness to put in the effort. This comprehensive guide will equip you with the knowledge and actionable steps needed to turn that "impossible" into a "possible." We’ll explore everything from preparing your finances to finding the right lenders and even using this opportunity to rebuild your credit.

The Definitive Guide: Securing a Car Loan with a 550 Credit Score

Understanding Your 550 Credit Score: What It Means to Lenders

Before diving into strategies, it’s crucial to understand what a 550 credit score signifies in the eyes of a lender. A FICO score of 550 falls squarely into the "Very Poor" category, which means it signals a higher risk of default. Lenders use credit scores to assess your creditworthiness and predict how likely you are to repay a loan.

When your score is in the subprime range (typically below 620-660, depending on the lender), it suggests a history of missed payments, high credit utilization, or other financial challenges. This elevated risk translates directly into higher interest rates and more stringent loan terms if you are approved. Traditional banks, with their stricter lending criteria, are often hesitant to approve loans for scores in this range.

However, the good news is that not all lenders operate under the same rules. There are financial institutions and auto finance companies that specialize in working with individuals who have less-than-perfect credit. These lenders understand that life happens, and they are willing to take on more risk, albeit at a higher cost to the borrower.

Is Getting a Car Loan With a 550 Credit Score Possible? The Reality

Let’s address the elephant in the room directly: Yes, getting a car loan with a 550 credit score is indeed possible. It’s not a myth, but it’s also not a walk in the park. The key lies in understanding the specific challenges and knowing how to proactively address them. You won’t walk into just any dealership or bank and get approved for a prime rate, but you can secure financing.

The primary hurdle you’ll face is the higher interest rates, which are a direct reflection of the perceived risk. Your loan terms might also be less flexible, and you may need to jump through a few more hoops during the application process. However, by strategically preparing and exploring the right avenues, you can significantly improve your chances of approval. This loan can even serve as a stepping stone to rebuild your credit over time.

Key Strategies to Boost Your Chances of Approval

Securing a car loan with a 550 credit score requires a proactive and well-thought-out strategy. It’s about mitigating risk for the lender and presenting yourself as the most reliable borrower possible. Let’s break down the most effective approaches.

A. Save for a Significant Down Payment

Based on my experience, a solid down payment is often the single most impactful factor in getting approved for a car loan with a low credit score. A substantial down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. It also demonstrates your commitment and financial discipline.

Lenders see a larger down payment as a sign of good faith and a buffer against potential default. For instance, if you’re borrowing $15,000 for a car, putting down $3,000 (20%) instantly reduces the loan amount to $12,000. This smaller loan principal makes the deal more attractive to subprime lenders. Aim for at least 10-20% of the car’s purchase price, but if you can put down more, do it. Every extra dollar significantly improves your standing.

B. Consider a Co-signer with Excellent Credit

Bringing in a co-signer with a strong credit history can dramatically increase your chances of approval. A co-signer essentially guarantees the loan, promising to make payments if you fail to do so. This significantly reduces the risk for the lender, as they have a second, more creditworthy individual to pursue if issues arise.

Pro tips from us: Ensure your co-signer fully understands their responsibility before they agree. Their credit score will also be affected if you miss payments, and it can strain relationships. A good co-signer is someone with an excellent credit score (700+), stable income, and a strong sense of trust in your ability to repay. This strategy can help you secure better interest rates and terms than you would qualify for on your own.

C. Explore Subprime Lenders & Dealerships That Specialize in Bad Credit

Traditional banks are often not the best place to start when you have a 550 credit score. Instead, focus your efforts on lenders who specialize in subprime auto loans. These include credit unions, online lenders, and specific dealership finance departments.

Many online lenders, such as Capital One Auto Finance, LightStream, and others, have programs designed for individuals with challenging credit. They assess a broader range of factors beyond just your credit score. "Buy Here, Pay Here" dealerships are another option, where the dealership itself is the lender. While they offer high approval rates, common mistakes to avoid are jumping at the first offer from a ‘Buy Here, Pay Here’ lot without comparison shopping. Their interest rates are typically very high, and terms can be less favorable, so exercise extreme caution and read every detail of the contract.

D. Get Pre-Approved Before Visiting the Dealership

Pre-approval is a powerful tool in your car buying journey, especially with a low credit score. It involves applying for a loan directly with a lender before you’ve even picked out a car. If approved, you’ll receive an offer detailing the maximum loan amount, interest rate, and terms you qualify for.

This process offers several benefits. Firstly, it gives you a clear budget, so you know exactly what you can afford. Secondly, it empowers you during negotiations at the dealership, as you already have financing secured. You can walk in with confidence, knowing your financing is handled, and focus solely on the car’s price. Many pre-approval applications result in a "soft inquiry" on your credit, which doesn’t harm your score, unlike the "hard inquiry" that occurs when you finalize a loan.

E. Choose the Right Vehicle for Your Situation

With a 550 credit score, aiming for a brand-new, expensive luxury car is generally not a wise move. Focus on practicality and affordability. A reliable used car is often the best choice, as it comes with a lower sticker price, which means a smaller loan amount and therefore less risk for the lender.

Opt for a vehicle that is known for its reliability and fuel efficiency. Lower monthly payments are crucial when you have a higher interest rate, and a car with good gas mileage and low maintenance costs will keep your overall expenses down. Your goal should be to secure a car that meets your transportation needs without overextending your budget.

F. Be Prepared with Comprehensive Documentation

Lenders who work with bad credit scores often require more documentation to verify your financial stability. Being prepared with all necessary paperwork can expedite the approval process and demonstrate your reliability. Gather these documents before you apply:

- Proof of Income: Recent pay stubs (last 2-3 months), tax returns, or bank statements.

- Proof of Residence: Utility bills, lease agreement, or mortgage statements.

- Proof of Insurance: You’ll need full coverage insurance before driving off the lot.

- Identification: Driver’s license or state ID.

- References: Sometimes lenders ask for personal or professional references.

Having everything in order shows the lender that you are organized and serious about the loan. It helps paint a picture of stability beyond just your credit score.

The Application Process for Bad Credit Car Loans

The application process for a car loan with a 550 credit score might involve a few more steps than for someone with excellent credit. Be prepared for lenders to scrutinize your application more closely.

Start by gathering all the documents we discussed previously. Then, strategically apply to a few different lenders within a short timeframe (usually 14-45 days, depending on the credit scoring model). This allows multiple hard inquiries to be treated as a single inquiry for scoring purposes, minimizing the impact on your credit score. Focus on credit unions, online subprime lenders, and dealerships with dedicated bad credit financing departments.

When filling out applications, be completely honest and accurate. Any discrepancies could lead to delays or outright rejection. Be ready to discuss your financial situation openly and explain any past credit issues. Your willingness to communicate and provide context can sometimes sway a lender’s decision.

What to Expect: High Interest Rates and Other Terms

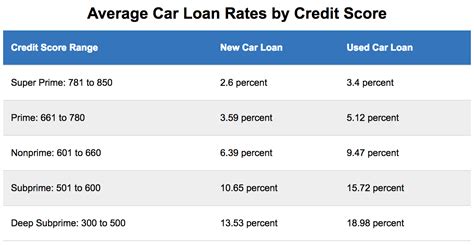

One of the most significant realities of getting a car loan with a 550 credit score is the higher interest rate. This is simply a reflection of the increased risk the lender is taking on. While someone with excellent credit might get an APR (Annual Percentage Rate) of 3-7%, you could be looking at rates ranging from 15% to 25% or even higher.

The APR includes not only the interest rate but also any additional fees associated with the loan, giving you the true cost of borrowing. A higher APR means your monthly payments will be significantly larger, and you’ll pay substantially more over the life of the loan. For example, a $15,000 loan at 20% interest over 60 months will cost you thousands more than the same loan at 5%.

You might also encounter longer loan terms (e.g., 72 or 84 months) which result in lower monthly payments but dramatically increase the total interest paid. Carefully evaluate the total cost of the loan, not just the monthly payment. Avoid stretching out the loan term too much, as it can lead to negative equity (owing more than the car is worth) and higher overall expenses.

Building Your Credit for the Future: A Golden Opportunity

While securing a car loan with a 550 credit score comes with its challenges, it also presents a valuable opportunity to improve your financial standing. This loan can be a powerful tool for credit rebuilding if managed responsibly.

The most crucial step is making every single payment on time, every month. Payment history is the biggest factor in your credit score (35% of your FICO score). Consistently making timely payments will demonstrate to credit bureaus that you are a reliable borrower, slowly but surely raising your score.

As your credit score improves, you might even be able to refinance your car loan down the road for a lower interest rate, saving you a significant amount of money. For more detailed steps on improving your credit score, check out our guide on . Beyond your car loan, consider other credit-building strategies like secured credit cards or credit builder loans to accelerate your progress.

Red Flags and Avoiding Predatory Lending

When you have a low credit score, you become a target for less scrupulous lenders. It’s vital to be vigilant and recognize the red flags of predatory lending practices. Common mistakes to avoid include feeling pressured into signing a deal without fully understanding it.

- Exorbitant Fees: Be wary of excessive origination fees, application fees, or hidden charges that inflate the total cost of the loan.

- Pressure Tactics: Lenders who rush you to sign without giving you time to read the contract or ask questions are a major red flag.

- Lack of Transparency: If a lender is unwilling to clearly explain the interest rate, APR, or total cost of the loan, walk away.

- Unrealistic Promises: Beware of anyone promising guaranteed approval regardless of your credit score, or offering rates that seem too good to be true for your credit situation.

- Negative Equity Traps: Some lenders might encourage you to roll negative equity from an old car into a new loan, burying you in debt.

Always read the fine print, ask questions, and never sign anything you don’t fully understand. If something feels off, it probably is. You can also consult resources like the Consumer Financial Protection Bureau (CFPB) for guidance on avoiding auto loan scams and understanding your rights as a borrower: Consumer Financial Protection Bureau – Auto Loans.

Pro Tips for Success

To maximize your chances of securing a car loan with a 550 credit score and making it a positive experience, consider these expert tips:

- Don’t Settle for the First Offer: Even with bad credit, it’s crucial to shop around. Compare offers from at least 2-3 different lenders to find the best terms available to you.

- Read the Fine Print Carefully: Understand every clause, fee, and condition in the loan agreement before you sign. Don’t hesitate to ask for clarification on anything you don’t understand.

- Budget Realistically: Beyond the car payment, factor in insurance (which will be higher with a new loan and potentially a higher-risk driver), fuel, maintenance, and registration costs. Your total car expenses should comfortably fit into your budget.

- Know Your Financial Limits: Just because you’re approved for a certain amount doesn’t mean you should borrow it all. Stick to a loan amount and monthly payment that you are absolutely confident you can afford without strain.

Conclusion: Your Road to a Car Loan is Open

Securing a car loan with a 550 credit score is undoubtedly a challenge, but it is far from an impossible dream. By approaching the situation with knowledge, preparation, and a strategic mindset, you can navigate the complexities of subprime auto lending successfully. The journey might involve higher interest rates and more stringent terms, but it also presents a valuable opportunity to demonstrate financial responsibility and actively rebuild your credit for a brighter financial future.

Remember, this car loan isn’t just about getting new wheels; it’s about proving your creditworthiness. By making timely payments and managing your finances diligently, you’ll open doors to better financial opportunities down the line. Take a deep breath, prepare thoroughly, and step confidently onto your path to car ownership. Considering other financing options or want to learn more about different loan types? Our article on might be helpful.