The Definitive Guide to Credit Score For Car Loan: How to Drive Away with the Best Deal

The Definitive Guide to Credit Score For Car Loan: How to Drive Away with the Best Deal Carloan.Guidemechanic.com

Dreaming of a new car? Whether it’s a sleek sedan, a spacious SUV, or a rugged truck, securing the right car loan is often the first step to turning that dream into a reality. But before you even set foot on a dealership lot, there’s one crucial factor that lenders scrutinize above all else: your credit score. Understanding your credit score for a car loan isn’t just important; it’s absolutely essential for determining the interest rates you’ll pay, the terms of your loan, and ultimately, how much you’ll spend over the lifetime of your vehicle.

In this comprehensive guide, we’ll dive deep into everything you need to know about how your credit score impacts your car loan. We’ll explore what credit scores mean, what lenders look for, strategies for securing a loan with various credit profiles, and actionable steps you can take to improve your score for the best possible deal. Our goal is to equip you with the knowledge to navigate the car loan process confidently, ensuring you drive away with not just a great car, but also a smart financial agreement.

The Definitive Guide to Credit Score For Car Loan: How to Drive Away with the Best Deal

What Exactly is a Credit Score and Why Does It Matter for Car Loans?

Before we talk about car loans, let’s clarify what a credit score is. Simply put, a credit score is a three-digit number, typically ranging from 300 to 850, that represents your creditworthiness. It’s a numerical summary of your financial history, indicating how reliably you’ve managed debt in the past. This score is calculated by credit bureaus (like Experian, Equifax, and TransUnion) using complex algorithms that analyze information from your credit report.

For car loans, your credit score serves as a critical indicator to potential lenders. They use this score to quickly assess the risk associated with lending you money. A higher credit score signals to lenders that you are a responsible borrower who pays debts on time, making you a low-risk candidate. Conversely, a lower score suggests a higher risk, potentially due to missed payments or high debt levels.

Lenders aren’t just being difficult; they’re protecting their investment. A car loan is a significant financial commitment, and they want to ensure they’ll be repaid. Your credit score provides a snapshot of your financial reliability, directly influencing their decision to approve your loan and the terms they offer.

Understanding Credit Score Ranges for Car Loans

Credit scores aren’t just a single number; they fall into different ranges, each signifying a different level of creditworthiness. While specific ranges can vary slightly between scoring models (like FICO Score and VantageScore), the general categories remain consistent. Knowing where your score stands is the first step in understanding your options for a car loan.

Here’s a breakdown of the typical credit score ranges and what they generally mean for securing a car loan:

-

Excellent (781-850): Borrowers in this category have an impeccable payment history, low credit utilization, and a long history of responsible credit use. If your score falls here, you’re considered a prime borrower. You can expect to qualify for the absolute best interest rates, most favorable loan terms, and potentially require a lower down payment. Lenders will be eager to offer you competitive deals.

-

Good (661-780): A good credit score indicates a solid history of managing credit responsibly, though perhaps with a minor hiccup or two in the past, or a shorter credit history. You’re still seen as a low-risk borrower. With a score in this range, you’ll likely qualify for very good interest rates and favorable loan terms, though perhaps not the absolute lowest rates available to those with excellent credit.

-

Fair (601-660): This range suggests that while you’ve managed credit, there might be some areas for improvement. Perhaps you have a few late payments, a relatively high credit utilization, or a limited credit history. Lenders view borrowers in this category as a moderate risk. You can still get a car loan, but you might face higher interest rates and potentially stricter loan terms compared to those with good or excellent credit.

-

Poor (501-600): A poor credit score often indicates a history of significant financial challenges, such as multiple missed payments, collections, or even bankruptcy. Borrowers in this range are considered high-risk. While getting a car loan is still possible, it will be more challenging. You can expect significantly higher interest rates, shorter loan terms, and a higher likelihood of requiring a substantial down payment or a co-signer.

-

Very Poor (300-500): This range signifies severe credit issues. Obtaining a traditional car loan will be extremely difficult, if not impossible, without significant additional measures like a very large down payment or a strong co-signer. Interest rates, if a loan is offered, will be exorbitant.

Pro Tip from Us: Don’t guess your credit score; know it! Before you even start looking at cars, pull your credit report and score from one of the major credit bureaus or a reputable credit monitoring service. This gives you a clear picture of your financial standing and helps you set realistic expectations. Based on my experience, checking your score first empowers you to negotiate better and avoids unpleasant surprises at the dealership. You can obtain a free copy of your credit report annually from each of the three major credit bureaus at AnnualCreditReport.com.

How Your Credit Score Directly Impacts Your Car Loan

The relationship between your credit score for a car loan and the actual loan terms you receive is direct and profound. It’s not just about getting approved; it’s about the entire cost of borrowing.

-

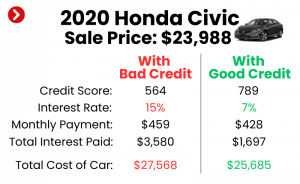

Interest Rates: This is arguably the most significant impact. A higher credit score typically translates to a lower Annual Percentage Rate (APR). Even a few percentage points difference in your APR can save you thousands of dollars over the life of a car loan. For example, on a $30,000 car loan over 60 months, the difference between a 3% APR and a 7% APR could mean paying an extra $4,000 in interest alone.

-

Loan Terms and Duration: Lenders are often more flexible with borrowers who have excellent credit. They might offer longer loan terms (e.g., 72 or 84 months) with competitive rates, which can lower your monthly payments. Conversely, with a lower credit score, lenders might be hesitant to offer extended terms, pushing you towards shorter loan periods with higher monthly payments to mitigate their risk.

-

Down Payment Requirements: While a down payment is always a good idea, it becomes almost a necessity with a lower credit score. Lenders may require a larger down payment to approve your loan, as it reduces the amount they need to finance and demonstrates your commitment to the purchase. With a high credit score, you might be able to secure a loan with a minimal or even no down payment.

-

Approval Odds: This is the most obvious impact. An excellent credit score makes you a highly desirable borrower, increasing your chances of quick and easy approval. As your score decreases, so do your approval odds with traditional lenders, making it necessary to explore alternative financing options.

-

Additional Fees and Charges: Some lenders might impose additional fees or charges on borrowers with lower credit scores to offset the perceived risk. These could include origination fees or other administrative costs that add to the overall expense of the loan.

Based on my experience, many consumers underestimate the power of their credit score until they see the numbers. The difference in total cost between a prime borrower and a subprime borrower on the exact same car can be astronomical, easily reaching several thousand dollars over the loan’s duration. It pays, quite literally, to have a strong credit profile.

Getting a Car Loan with Less-Than-Perfect Credit

What if your credit score isn’t in the "excellent" or "good" range? Don’t despair. While it might require a bit more effort and strategic planning, securing a car loan with a fair or even poor credit score is absolutely possible. You’ll just need to be prepared for potentially different terms and explore various avenues.

Here are several effective strategies for getting a car loan when your credit is less than ideal:

-

Consider a Co-Signer: A co-signer is someone with a strong credit history who agrees to be equally responsible for the loan if you default. This significantly reduces the risk for the lender, as they have another party to pursue for repayment. A co-signer can help you qualify for a loan and potentially secure a much better interest rate than you could on your own. Ensure both parties understand the responsibilities involved.

-

Make a Larger Down Payment: A substantial down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. If you can put down 20% or more of the car’s purchase price, you significantly improve your chances of approval and might even qualify for a better interest rate, even with a lower credit score. It shows lenders you have skin in the game.

-

Opt for a Less Expensive or Used Car: Instead of aiming for a brand-new, top-of-the-line vehicle, consider a more affordable used car. The smaller loan amount associated with a less expensive vehicle makes it less risky for lenders. This can increase your approval odds and make the monthly payments more manageable.

-

Explore Subprime Lenders: Traditional banks and credit unions often have strict credit score requirements. Subprime lenders specialize in offering loans to individuals with lower credit scores. While their interest rates are typically higher, they are an option when others aren’t. Always compare offers from several subprime lenders to ensure you’re getting the best possible terms.

-

Check with Credit Unions: Credit unions are member-owned financial institutions that often offer more flexible lending criteria and competitive rates, even for members with fair credit. Their focus on member welfare can sometimes translate into more understanding and accommodating loan options. It’s always worth checking with your local credit union.

-

Get Pre-Approved: Even with fair credit, seeking pre-approval from multiple lenders is a smart move. This allows you to compare offers without commitment and gives you a clear idea of what loan terms you qualify for before you visit a dealership. It also gives you leverage in negotiations.

-

Be Prepared for Higher Interest Rates: With a lower credit score, you should anticipate higher interest rates. Factor this into your budget and understand that the total cost of the car will be higher. Your primary goal might be to get approved for a reliable vehicle, with a plan to refinance for a better rate once your credit score improves.

Common Mistakes to Avoid When Applying for a Car Loan

Navigating the car loan process can be tricky, and certain missteps can cost you money, damage your credit, or lead to regret. Knowing what to avoid is just as important as knowing what to do.

Common mistakes to avoid are:

-

Applying Everywhere at Once: Each loan application results in a "hard inquiry" on your credit report, which can temporarily lower your score. While multiple inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are often grouped as one for scoring purposes, spreading applications out over months can be detrimental. Focus on a few pre-approvals first.

-

Not Checking Your Credit Report for Errors: Your credit report is the foundation of your credit score. Errors, such as incorrect late payments or accounts that aren’t yours, can artificially lower your score. Always review your report thoroughly and dispute any inaccuracies immediately. A clean report can significantly boost your credit score for a car loan.

-

Focusing Only on the Monthly Payment: While an affordable monthly payment is important, fixating solely on it can lead to agreeing to longer loan terms or higher interest rates than necessary. A longer term means you pay more interest over time, and a high interest rate means more of your payment goes towards interest, not the principal. Always consider the total cost of the loan.

-

Not Knowing Your Budget: Before you even look at cars, establish a realistic budget. This includes not just the car payment, but also insurance, fuel, maintenance, and registration fees. Getting approved for a loan you can’t comfortably afford monthly is a recipe for financial stress and potential default.

-

Skipping the Pre-Approval Process: Walking into a dealership without a pre-approved loan offer puts you at a disadvantage. You won’t know if the dealership’s financing offer is competitive, and you might feel pressured to accept less favorable terms. Pre-approval gives you negotiating power.

Steps to Improve Your Credit Score for a Better Car Loan Deal

Improving your credit score for a car loan isn’t an overnight process, but consistent effort can yield significant results. Even small improvements can lead to better loan terms and substantial savings.

Here’s a strategic approach to boosting your credit score:

-

Pay All Bills On Time, Every Time: Payment history is the most crucial factor in your credit score, accounting for about 35%. Make it a priority to pay all your bills – credit cards, utility bills, student loans, etc. – on or before their due dates. Set up automatic payments or reminders to avoid missing a payment.

-

Reduce Your Credit Utilization Ratio: This refers to the amount of credit you’re using compared to your total available credit. Lenders prefer to see a low utilization, ideally below 30%. If you have a credit card with a $10,000 limit and a $5,000 balance, your utilization is 50%, which is too high. Pay down credit card balances to lower this ratio.

-

Avoid Opening New Credit Accounts Unnecessarily: Each new credit application results in a hard inquiry, which can slightly ding your score. Additionally, new accounts lower the average age of your credit history, another factor in your score. Only apply for credit when absolutely necessary.

-

Keep Old Accounts Open: While you might not use old credit cards, keeping them open (as long as they don’t have annual fees) can be beneficial. They contribute to a longer credit history and a higher overall available credit limit, which can help your utilization ratio.

-

Regularly Monitor Your Credit Report: As mentioned earlier, errors on your credit report can harm your score. Regularly check your reports from all three major bureaus (Experian, Equifax, TransUnion) for inaccuracies and dispute them immediately. A free annual report is available from AnnualCreditReport.com.

-

Diversify Your Credit Mix (Carefully): Having a mix of credit types (e.g., installment loans like car loans or mortgages, and revolving credit like credit cards) can positively impact your score. However, don’t open new accounts just to diversify; let it happen naturally as your financial needs evolve.

-

Become an Authorized User (with caution): If a trusted family member with excellent credit adds you as an authorized user to one of their long-standing, well-managed credit card accounts, their positive payment history can reflect on your credit report. Ensure they maintain responsible credit habits, as their mistakes could also affect you.

These steps, taken consistently over time, can significantly improve your credit score for a car loan, opening doors to better rates and more favorable terms when you’re ready to buy your next vehicle.

The Pre-Approval Process: A Smart Move for Any Credit Score

Regardless of your credit standing, getting pre-approved for a car loan is a highly recommended strategy. It’s a proactive step that puts you in a much stronger position when you’re ready to negotiate with dealerships.

Here’s why pre-approval is a smart move:

-

Know Your Buying Power: Pre-approval gives you a concrete understanding of how much you can borrow, the interest rate you qualify for, and the estimated monthly payments. This empowers you to shop for cars within your budget, avoiding the disappointment of falling in love with a car you can’t afford.

-

Negotiating Leverage: Walking into a dealership with a pre-approved loan offer in hand is like having cash. You’re a serious buyer, and you have an alternative financing option if the dealership’s offer isn’t competitive. This gives you significant leverage to negotiate better terms, not just on the loan but potentially on the car’s price itself.

-

Focus on the Car, Not the Financing: With financing sorted, you can concentrate on finding the right vehicle that meets your needs and budget, rather than feeling pressured by financing discussions. It streamlines the buying process significantly.

-

No Obligation to Accept: Getting pre-approved doesn’t obligate you to take that specific loan. You can still explore other options, including financing through the dealership. It simply provides a benchmark against which to compare all other offers.

-

Minimal Impact on Credit Score: While a pre-approval does involve a "soft inquiry" (or sometimes a hard inquiry depending on the lender), applying for multiple pre-approvals within a short window (typically 14-45 days) is usually treated as a single inquiry by credit scoring models. This allows you to rate shop without significantly harming your score.

To get pre-approved, you’ll typically fill out an application with a bank, credit union, or online lender, providing personal and financial information. The lender will then perform a credit check and, if approved, issue you a letter stating the maximum loan amount, interest rate, and terms for which you qualify.

The Role of Down Payment and Trade-In

Beyond your credit score, your down payment and any vehicle you trade in play a crucial role in securing favorable car loan terms. These factors can often mitigate the impact of a less-than-perfect credit score.

-

Down Payment: A down payment is the initial sum of money you pay upfront towards the purchase of the car. The larger your down payment, the less money you need to borrow, which directly reduces the lender’s risk. For individuals with lower credit scores, a substantial down payment can be the key to getting approved or securing a more reasonable interest rate. It shows financial commitment and reduces the loan-to-value ratio.

-

Trade-In: If you have an existing vehicle, trading it in at the dealership can serve a similar purpose to a cash down payment. The value of your trade-in is deducted from the purchase price of the new car, reducing the amount you need to finance. This can be particularly beneficial if your current car has significant equity (its market value is higher than what you still owe on it).

Pro tips from us: Always research the value of your trade-in beforehand using resources like Kelley Blue Book or Edmunds. This prevents you from accepting a low-ball offer from the dealership. Similarly, try to save up for the largest down payment you can reasonably afford. A good rule of thumb is aiming for at least 20% of the vehicle’s price, especially for new cars, to avoid being "upside down" on your loan (owing more than the car is worth).

Conclusion: Drive Away Confidently with Your Credit Score in Command

Your credit score for a car loan is undeniably a powerful determinant in your car buying journey. It influences everything from your approval chances to the interest rate you pay, and ultimately, the total cost of your vehicle. Understanding this crucial number and actively managing it empowers you to make smarter financial decisions and secure the best possible deal.

By taking the time to check your credit score, understand its impact, and implement strategies to improve it, you position yourself as a responsible borrower. Whether you have excellent credit or are working to rebuild it, the knowledge shared in this guide provides a roadmap to navigating the car loan landscape with confidence. Don’t let your credit score be a mystery; take control, plan wisely, and prepare to drive away in the car of your dreams with a loan that makes financial sense.

Start by checking your credit reports today and begin your journey towards a better car loan. Remember, every step you take to improve your credit is an investment in your financial future!

For more insights into managing your credit, check out our article on . You might also find our guide on helpful for your next purchase.

For detailed information on FICO scores and how they are calculated, visit the official FICO website at FICO.com.