The Definitive Guide: What’s the Minimum Credit Score For A Car Loan (And How to Get Approved)

The Definitive Guide: What’s the Minimum Credit Score For A Car Loan (And How to Get Approved) Carloan.Guidemechanic.com

The dream of a new car often comes with a looming question: "What’s the minimum credit score for a car loan?" It’s a query that can cause anxiety, especially if you’re unsure about your credit standing. Securing an auto loan is a significant financial step, and your credit score plays a pivotal role in not just getting approved, but also in determining the terms and interest rate you’ll receive.

This comprehensive guide will demystify the relationship between your credit score and car loans. We’ll explore what lenders truly look for, break down the credit score tiers, and provide actionable strategies to help you navigate the auto financing landscape, regardless of your current credit situation. Our ultimate goal is to equip you with the knowledge to drive away with the best possible deal, making this a truly informative and unique resource.

The Definitive Guide: What’s the Minimum Credit Score For A Car Loan (And How to Get Approved)

Understanding Your Credit Score: The Foundation of Auto Loans

Before diving into the specifics of auto loans, it’s crucial to understand what a credit score is and why it holds such sway with lenders. Essentially, your credit score is a three-digit number that represents your creditworthiness. It’s a snapshot of your financial reliability, compiled from your credit history.

The most widely used scoring model is FICO, which ranges from 300 to 850. Lenders use this score to quickly assess the risk associated with lending you money. A higher score indicates a lower risk, while a lower score suggests a higher risk of default. This assessment directly influences their decision to approve your loan and the interest rate they offer.

Why Lenders Prioritize Your Credit Score

Lenders, whether banks, credit unions, or dealership finance departments, use your credit score as their primary tool for risk management. They want to know that you have a history of borrowing money and paying it back responsibly. Your score provides a concise summary of your past financial behavior, including payment history, amounts owed, length of credit history, new credit, and credit mix.

Based on my experience working with countless individuals navigating the auto loan market, understanding these fundamental credit score ranges is the first and most critical step. It allows you to set realistic expectations and strategize effectively. Without a clear picture of your own credit, you’re essentially walking into negotiations blind, which is a common mistake many car buyers make.

Is There a "Minimum" Credit Score for a Car Loan? The Reality

Here’s the truth: there isn’t a single, universally defined minimum credit score for a car loan. Unlike some other forms of lending, auto loans can be approved across a wide spectrum of credit scores. However, while there might not be a hard-and-fast numerical cutoff, there are practical minimums and significant implications for different credit tiers.

The real distinction isn’t just about getting approved; it’s about the quality of the approval. Someone with a lower credit score might get approved, but they will likely face much higher interest rates, less favorable terms, and potentially require a larger down payment or a co-signer. Conversely, a strong credit score opens the door to competitive rates and more flexible options.

The Spectrum of Auto Loan Borrowers

Lenders typically categorize borrowers into different tiers based on their credit scores. These tiers dictate the type of loan programs available and the associated risk pricing. Understanding these categories is key to knowing where you stand and what to expect.

We generally divide borrowers into "prime" and "subprime" categories. Prime borrowers typically have higher credit scores and are considered lower risk, qualifying for the best rates. Subprime borrowers have lower scores, are considered higher risk, and face more stringent terms and significantly higher interest rates.

Credit Score Tiers and What They Mean for Your Car Loan

Let’s break down the common FICO credit score ranges and what each means for your prospects when seeking a car loan. This detailed overview will give you a clearer picture of what kind of offers you can expect.

Excellent Credit (780-850)

Borrowers in this range are considered top-tier. They have a proven history of managing credit exceptionally well, making them very low-risk.

If your score falls here, you’re likely to qualify for the absolute best interest rates available, often advertised as promotional rates. Lenders will compete for your business, offering flexible terms and potentially requiring little to no down payment. Your approval chances are virtually guaranteed, assuming other factors like income are also strong.

Very Good Credit (740-779)

This tier also represents a highly creditworthy borrower. While not at the absolute peak, these scores are still considered excellent by most lenders.

You’ll still receive very competitive interest rates and favorable loan terms. Your approval process will be smooth, and you’ll have a wide array of lenders eager to finance your vehicle. This range often qualifies for rates very close to those with excellent credit.

Good Credit (670-739)

This is a solid credit range, indicating a reliable borrower. The majority of consumers fall into this category.

With a good credit score, you can expect favorable interest rates, though perhaps not the absolute lowest. You’ll have many options for lenders and shouldn’t face significant hurdles in getting approved. This is generally considered the benchmark for a "good" auto loan experience.

Fair Credit (580-669)

This is where the discussion around the minimum credit score for a car loan often begins. Borrowers in this range are considered moderate risk. They might have a few late payments in their history or a shorter credit history.

While approval is still very possible, you should expect higher interest rates compared to those with good or excellent credit. Lenders might also require a larger down payment or prefer a shorter loan term to mitigate their risk. It’s crucial to shop around in this tier, as offers can vary significantly between lenders.

Poor Credit (300-579)

Securing a car loan with a poor credit score is the most challenging. Borrowers in this range are considered high-risk due to past financial difficulties, bankruptcies, or a very limited credit history.

You will likely face very high interest rates, often in the double digits, and more restrictive loan terms. Many traditional lenders might decline your application, forcing you to seek out subprime lenders or those specializing in bad credit auto loans. A substantial down payment and/or a co-signer will significantly improve your chances here. Pro tips from us: Even within these tiers, individual circumstances matter greatly. Lenders will look at your entire financial picture, not just the score in isolation.

Factors Beyond Your Credit Score That Influence Approval

While your credit score is undeniably important, it’s not the only piece of the puzzle. Lenders consider several other factors when evaluating your auto loan application. Understanding these can significantly bolster your chances, even if your minimum credit score for a car loan is on the lower side.

Income and Debt-to-Income (DTI) Ratio

Lenders want assurance that you can comfortably afford your monthly car payments. They’ll look at your gross monthly income and your existing debt obligations. Your Debt-to-Income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income, is a critical metric. A lower DTI ratio indicates you have more disposable income to cover new debt, making you a more attractive borrower.

A general rule of thumb is that lenders prefer a DTI ratio below 43%, though some auto lenders might go slightly higher. They’ll want to see stable employment and a reliable income source.

Down Payment

A significant down payment reduces the amount you need to borrow, which directly lowers the lender’s risk. If you put down a substantial portion of the car’s price, you’re less likely to "go underwater" on the loan (owing more than the car is worth).

Common mistakes to avoid are underestimating the power of a solid down payment. Even a small down payment can make a difference, but 10-20% is often recommended, especially if you have a fair or poor credit score. It shows commitment and reduces the loan-to-value (LTV) ratio.

Loan-to-Value (LTV) Ratio

The LTV ratio compares the amount you’re borrowing to the vehicle’s actual market value. Lenders prefer a lower LTV because it means they’re financing a smaller percentage of the car’s value. A high LTV, particularly for a used car, can signal higher risk.

A strong down payment is the best way to achieve a favorable LTV ratio. Some lenders might have strict LTV limits, especially for older or high-mileage vehicles.

Loan Term

The loan term refers to the length of time you have to repay the loan. Shorter terms typically mean higher monthly payments but lower overall interest paid. Longer terms mean lower monthly payments but significantly more interest paid over the life of the loan.

Lenders often view shorter terms as less risky because there’s less time for the car to depreciate below the outstanding loan balance. While tempting, be cautious of very long terms (e.g., 72 or 84 months), as they can lead to being upside down on your loan and paying excessive interest.

Vehicle Type (New vs. Used)

Lenders often perceive new cars as less risky than used cars. New cars typically have a higher residual value, are less prone to immediate mechanical issues, and usually come with manufacturer warranties. This can sometimes make it easier to secure a loan for a new car, even with a slightly lower credit score, compared to a very old or high-mileage used car.

However, the total loan amount for a new car is usually higher, so your income and DTI still need to support the larger payment.

Cosigner

If your credit score is on the lower end, or if you have a limited credit history, a cosigner can be a game-changer. A cosigner is someone with excellent credit who agrees to take on responsibility for the loan if you fail to make payments.

This significantly reduces the lender’s risk, often allowing you to qualify for better rates and terms than you would on your own. However, it’s a serious commitment for the cosigner, as their credit will also be impacted if you miss payments.

Strategies for Getting a Car Loan with a Less-Than-Ideal Credit Score (Fair or Poor)

Don’t despair if your credit score isn’t in the "excellent" range. While you might not get the absolute best rates, there are still effective strategies to secure a car loan, even if your current minimum credit score for a car loan is fair or poor.

1. Save for a Larger Down Payment

As discussed, a larger down payment is your most powerful tool. It directly reduces the amount you need to borrow, lowers the lender’s risk, and can lead to more favorable loan terms. Aim for at least 10-20% of the vehicle’s price if possible.

This upfront investment shows lenders you’re serious and committed, potentially offsetting some of the risk associated with a lower credit score. It also reduces your monthly payments, making the loan more manageable.

2. Consider a Cosigner with Good Credit

If you have a trusted friend or family member with a strong credit history, asking them to cosign can dramatically improve your chances of approval and secure a better interest rate. Ensure both you and the cosigner understand the full implications.

Their credit score will be on the line, so consistent, on-time payments are paramount. This is an excellent way to get approved when your own credit might not quite meet a lender’s traditional minimum credit score for a car loan.

3. Explore Dealership Financing (Bad Credit Auto Loans)

Many dealerships have relationships with a variety of lenders, including those specializing in subprime auto loans. While these loans come with higher interest rates, they are designed for individuals with less-than-perfect credit.

Be prepared for higher rates and potentially stricter terms. Always compare offers from multiple dealerships and lenders to ensure you’re getting the best deal possible.

4. Check with Credit Unions

Credit unions are non-profit financial institutions known for often being more flexible and offering better rates than traditional banks, especially for members. If you’re a member of a credit union, or eligible to join one, it’s definitely worth checking their auto loan options.

They tend to have a more personal approach to lending and might be more willing to work with borrowers who have a fair or even slightly poor credit score, particularly if you have an established relationship with them.

5. Get Pre-Approved Before You Shop

One of the smartest moves you can make is to get pre-approved for a car loan before you step onto a dealership lot. Pre-approval gives you a clear idea of how much you can borrow, at what interest rate, and under what terms.

This empowers you to negotiate like a cash buyer, focusing on the car’s price rather than getting bogged down in financing details at the dealership. It also prevents you from falling in love with a car you can’t afford. For a deeper dive into improving your credit, check out our guide on .

6. Shop Around for Lenders

Never take the first loan offer you receive, especially if you have a lower credit score. Apply with multiple banks, credit unions, and online lenders within a short timeframe (usually 14-45 days). Multiple inquiries within this window are typically counted as a single hard inquiry for FICO scoring purposes, minimizing the impact on your score.

Comparing offers can save you thousands of dollars over the life of the loan. Different lenders have different risk appetites and lending criteria.

7. Lower Your Expectations (Initially)

If your credit is a challenge, you might need to adjust your expectations regarding the type of car you can afford. Consider a more modest, reliable used car rather than a brand-new luxury vehicle.

A less expensive car means a smaller loan amount, which is easier to get approved for and has lower monthly payments. This also allows you to make timely payments and rebuild your credit for future, better auto loans.

The Impact of Your Credit Score on Interest Rates

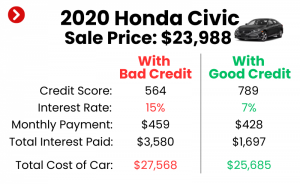

The direct correlation between your credit score and the interest rate you receive on a car loan cannot be overstated. This is where the true cost of a lower minimum credit score for a car loan becomes evident. A difference of just a few percentage points in your Annual Percentage Rate (APR) can translate into thousands of dollars over the life of the loan.

Consider this hypothetical example for a $30,000 car loan over 60 months:

- Excellent Credit (780+): APR 4.0%

- Monthly Payment: ~$552

- Total Interest Paid: ~$3,120

- Good Credit (670-739): APR 7.0%

- Monthly Payment: ~$594

- Total Interest Paid: ~$5,640

- Fair Credit (580-669): APR 12.0%

- Monthly Payment: ~$667

- Total Interest Paid: ~$10,020

- Poor Credit (300-579): APR 18.0%

- Monthly Payment: ~$762

- Total Interest Paid: ~$15,720

As you can see, the difference between an excellent credit score and a poor one can mean paying over $12,000 more in interest for the same car. This stark reality underscores why maintaining a healthy credit score is so vital. It’s not just about getting approved; it’s about minimizing the long-term financial burden. For more detailed information on understanding auto loan interest rates, you can consult resources like the Consumer Financial Protection Bureau (CFPB) .

Preparing for Your Car Loan Application: A Checklist

Thorough preparation is your best friend when applying for a car loan. Following this checklist will not only streamline the process but also improve your chances of securing favorable terms, regardless of your specific minimum credit score for a car loan situation.

- Check Your Credit Report (and Dispute Errors): Obtain free copies of your credit report from AnnualCreditReport.com. Review them carefully for any inaccuracies or errors. Disputing and correcting these can potentially boost your score.

- Know Your Credit Score: Get your actual FICO score. Many credit card companies offer this for free. Knowing your score empowers you to understand your standing and prepare for negotiations.

- Determine Your Budget: Don’t just think about the monthly payment. Calculate how much you can truly afford for the car’s price, insurance, fuel, maintenance, and registration.

- Gather Necessary Documents: Have your identification (driver’s license), proof of income (pay stubs, tax returns), proof of residence (utility bills), and any trade-in vehicle information ready.

- Get Pre-Approved: As mentioned, secure pre-approval from multiple lenders (banks, credit unions, online lenders) before visiting dealerships. This gives you leverage and a benchmark. Before you even start car shopping, it’s crucial to understand .

- Save for a Down Payment: The more you can put down, the better your chances and terms will be.

Common Mistakes to Avoid When Seeking a Car Loan

Navigating the auto loan process can be tricky, and many common pitfalls can cost you money and stress. Being aware of these mistakes can help you avoid them and secure a better deal, even if you’re concerned about the minimum credit score for a car loan.

- Not Checking Your Credit First: Going into the process blind is a major disadvantage. You won’t know what kind of rates to expect or if there are errors to fix.

- Applying to Too Many Lenders at Once (Indiscriminately): While shopping around is good, submitting applications to dozens of lenders over an extended period can lead to multiple hard inquiries, which can temporarily lower your credit score. Focus your applications within a concentrated shopping period.

- Not Shopping Around for Rates: Relying solely on the dealership’s financing offer without comparing it to outside lenders can result in paying significantly more in interest.

- Focusing Only on the Monthly Payment: A low monthly payment might seem attractive, but it often comes with a longer loan term and much higher total interest paid. Always consider the total cost of the loan. Pro tips from us: Always ask for the total amount you will pay, including all interest and fees, not just the monthly installment.

- Buying More Car Than You Can Afford: It’s easy to get caught up in the excitement of a new vehicle. Stick to your budget and avoid being pressured into buying a car that will strain your finances.

- Not Understanding the Loan Terms: Read all paperwork carefully. Understand the APR, loan term, any prepayment penalties, and all fees before signing. If you have questions, ask them.

Conclusion

The journey to securing a car loan, particularly when considering the minimum credit score for a car loan, is multi-faceted. While there isn’t a single magic number that guarantees or denies approval, your credit score is undeniably a cornerstone of the process. It dictates not just your eligibility, but critically, the interest rate and terms you’ll receive, ultimately impacting the total cost of your vehicle.

By understanding your credit score, preparing thoroughly, and employing smart strategies like saving for a down payment or exploring various lenders, you can significantly improve your chances of getting approved for an auto loan with favorable terms. Even if your credit score is currently fair or poor, options exist, though they may come with higher costs. Remember, every on-time payment you make on a car loan is an opportunity to build or rebuild your credit, paving the way for even better financial opportunities in the future.

Don’t let the question of a "minimum credit score" deter you. Instead, empower yourself with knowledge and proactive steps. Share your experiences or questions in the comments below – we’d love to hear how you navigated your car loan journey!