The Hidden Dangers of Predatory Car Loans: Your Ultimate Guide to Identification and Avoidance

The Hidden Dangers of Predatory Car Loans: Your Ultimate Guide to Identification and Avoidance Carloan.Guidemechanic.com

Buying a car is a significant life event for most people. It represents freedom, convenience, and often, a major financial commitment. For many, securing an auto loan is a necessary step to make this dream a reality. However, beneath the gleaming allure of a new or used vehicle, a dark side of the auto finance industry lurks: predatory car loans. These aren’t just high-interest loans; they are manipulative financial products designed to trap vulnerable borrowers in a cycle of debt, often stripping them of their assets and financial stability.

Based on my experience working with countless individuals navigating the auto loan landscape, the threat of predatory lending is very real. It’s a complex issue, often disguised by appealing monthly payments or fast approvals, making it difficult for the average consumer to spot. This comprehensive guide aims to arm you with the knowledge and tools to identify, understand, and, most importantly, avoid predatory auto loans, ensuring your journey to car ownership is one of empowerment, not regret.

The Hidden Dangers of Predatory Car Loans: Your Ultimate Guide to Identification and Avoidance

What Exactly Are Predatory Car Loans? Unmasking the Deception

Predatory car loans are not merely expensive loans; they are financial instruments characterized by unfair, abusive, or deceptive terms that exploit a borrower’s lack of knowledge, urgent need for transportation, or limited credit options. The intent behind a predatory loan is often to generate excessive profit for the lender at the borrower’s long-term expense, rather than providing a fair financial service.

Unlike legitimate high-interest loans offered to borrowers with poor credit, which carry higher risk but are transparent about their terms, predatory loans often include hidden fees, inflated interest rates beyond reasonable market standards, and complex clauses designed to confuse or mislead. They capitalize on desperation, pushing borrowers into agreements they may not fully comprehend, leading to significant financial distress and even vehicle repossession. Understanding this core distinction is your first line of defense.

Common Characteristics of Predatory Car Loans: Red Flags You Must Recognize

Identifying a predatory car loan requires a keen eye for specific red flags. These characteristics often work in concert to create a financially debilitating package for the borrower. Let’s delve into the most prevalent signs you should never ignore.

1. Excessively High Interest Rates

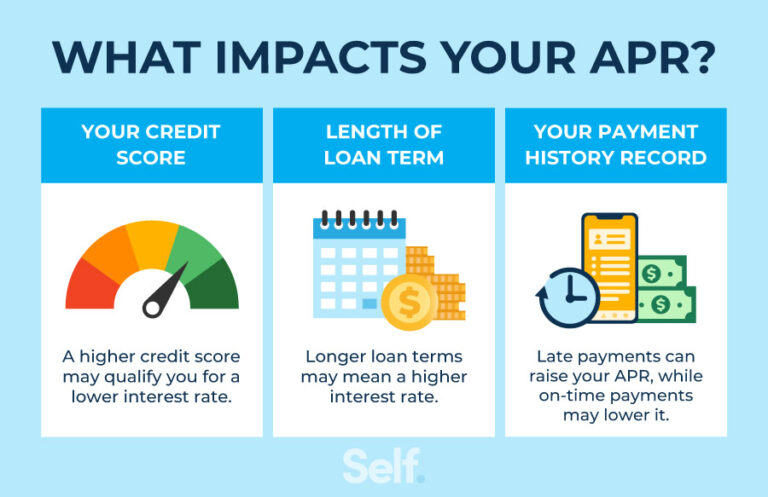

While high interest rates are expected for borrowers with low credit scores, predatory loans push these rates to extreme, unjustifiable levels. We’re talking about annual percentage rates (APRs) that can be upwards of 20%, 30%, or even higher, especially on older, less valuable vehicles. These rates are often disproportionate to the actual risk posed by the borrower, designed instead to maximize the lender’s profit.

A legitimate lender will assess your creditworthiness and offer a rate commensurate with the market and your risk profile. Predatory lenders, however, might offer a seemingly easy approval with little regard for your ability to repay, knowing that the exorbitant interest will quickly swell the loan balance. Always compare offered rates to national averages for similar credit profiles.

2. Hidden Fees and Charges

One of the most insidious tactics of predatory lenders is to bury various fees and charges deep within the loan contract. These can include excessive origination fees, documentation fees, processing fees, and even charges for services that are either unnecessary or never rendered. These hidden costs significantly increase the total amount you owe without adding any real value.

These fees are often presented as non-negotiable or standard, but in reality, they are inflated or entirely fabricated. Always demand a detailed breakdown of every single charge on your loan agreement. If a fee seems vague or unusually high, question it vigorously.

3. Loan Packing

Loan packing is a deceptive practice where lenders or dealerships add unnecessary or overpriced products and services into your auto loan without your full understanding or explicit consent. Common examples include extended warranties, GAP (Guaranteed Asset Protection) insurance, credit life insurance, or even VIN etching, all at inflated prices. These additions are often presented as mandatory or highly beneficial.

While some of these products can be valuable in certain situations, predatory lenders mark them up significantly or include them even when they don’t apply to your circumstances. This inflates the total loan amount, meaning you pay interest on these added products for the entire loan term, drastically increasing your overall cost. Always scrutinize every line item and ask for a clear explanation of each additional product.

4. "Yo-Yo" Financing or Spot Delivery Scams

This is a particularly cruel form of predatory lending. In a "yo-yo" scam, a dealership allows you to drive off the lot with a new car under the pretense that your financing has been approved. You might even sign a contract. However, days or weeks later, they contact you, claiming the financing fell through and demanding you return the car or agree to new, often much worse, loan terms (higher interest rates, larger down payment, etc.).

This tactic leaves borrowers in a vulnerable position, having already bonded with the vehicle and potentially sold their old car. They feel pressured to accept the new, predatory terms. Pro tips from us: Never drive off with a car unless the financing is 100% finalized and you have a copy of the final, approved loan agreement in hand.

5. Negative Equity Traps (Upside-Down Loans)

Predatory lenders often structure loans in a way that ensures you are "upside down" or have negative equity from day one, meaning you owe more on the car than it’s worth. This can happen by financing 120% or more of the car’s value, often by rolling over existing negative equity from a trade-in or including excessive fees.

Being upside down limits your options for selling or trading the vehicle, as you’d have to pay the difference out of pocket. It traps you in the current loan, making it difficult to escape or refinance without taking a significant financial hit. Understanding the car’s actual market value versus your loan amount is crucial.

6. Aggressive Sales Tactics and Pressure

Predatory lenders and dealerships often employ high-pressure sales tactics to rush you into signing a loan agreement before you have a chance to fully review it or seek independent advice. They might emphasize "today-only" deals, limited-time offers, or imply that your credit score makes this your only option. They create an environment of urgency and fear.

Such tactics are a major red flag. A reputable lender will give you ample time to consider your options, read the contract, and ask questions. Never make a significant financial decision under duress.

7. Balloon Payments

A balloon payment loan features low monthly payments for a set period, but at the end of the loan term, a single, large lump-sum payment (the "balloon") becomes due. If you can’t make this payment, you’ll likely have to refinance, potentially at higher rates, or face repossession. While not always predatory, they become so when the borrower is not fully informed or when the lender intends for the borrower to fail to make the balloon payment, thereby triggering additional fees or repossession.

Ensure you fully understand if your loan includes a balloon payment and have a clear plan for how you will manage it. If it’s sprung on you unexpectedly, it’s a sign of a predatory practice.

8. Lack of Transparency and Vague Terms

Predatory loan contracts are often filled with jargon, complex legal language, and vague clauses that make it difficult for the average person to understand their true obligations. They might rush through the paperwork, gloss over key terms, or refuse to provide clear explanations. This lack of transparency is deliberate, designed to obscure the predatory nature of the deal.

Always insist on clear, concise explanations for any term you don’t understand. If a lender or dealership is unwilling to provide this, walk away.

Who is Most Vulnerable to Predatory Car Loans?

While anyone can fall victim, certain groups are disproportionately targeted by predatory lenders. Common mistakes to avoid are often rooted in a lack of awareness or a sense of urgency.

- Borrowers with Bad or No Credit: These individuals often believe they have limited options and are more susceptible to "guaranteed approval" promises, even if the terms are terrible.

- First-Time Car Buyers: Lacking experience in auto financing, they may not know what constitutes a fair deal or how to negotiate.

- Individuals in Urgent Need of a Vehicle: Whether due to a job requirement or family necessity, desperation can lead people to accept unfavorable terms.

- Those with Limited Financial Literacy: A lack of understanding of interest rates, APRs, and loan structures makes it easy for predatory lenders to exploit.

- Low-Income Individuals: Often facing financial constraints, they may be swayed by seemingly low monthly payments, overlooking the total cost.

The Devastating Impact of Predatory Auto Loans

The consequences of entering a predatory car loan can be severe and far-reaching, impacting not just your finances but your overall well-being.

- Financial Ruin and Debt Spiral: High interest rates and hidden fees quickly inflate your loan balance, making it nearly impossible to pay down the principal. This can lead to a cycle of debt that’s incredibly difficult to escape.

- Credit Score Damage: Missing payments or having your vehicle repossessed due to an unaffordable loan will severely damage your credit score, making it harder to obtain future loans, rent an apartment, or even secure certain jobs.

- Vehicle Repossession: When you can no longer afford the inflated payments, the lender will repossess your vehicle, leaving you without transportation and still potentially owing a "deficiency balance" on a car you no longer own.

- Emotional Distress: The constant stress of financial struggle, the fear of losing your vehicle, and the feeling of being exploited can take a significant toll on your mental and emotional health.

How to Spot and Avoid Predatory Car Loans: Your Proactive Shield

Protecting yourself requires a proactive approach and a commitment to due diligence. Here are actionable steps to shield yourself from predatory auto loans.

1. Educate Yourself Before You Shop

Before you even step foot in a dealership or apply for a loan, take the time to understand auto financing basics. Learn about interest rates, APRs, loan terms, and how they impact the total cost of your loan. Knowledge is your most powerful weapon against deception. Understand the current market value of the car you’re interested in using resources like Kelley Blue Book or Edmunds.

2. Check Your Credit Score

Knowing your credit score and understanding your credit report is paramount. This allows you to anticipate the interest rates you might qualify for and spot discrepancies. You can get free copies of your credit report annually from AnnualCreditReport.com. If you have poor credit, focus on improving it before applying for a loan, if possible.

3. Get Pre-Approved from Multiple Lenders

One of the most effective strategies is to secure pre-approvals from several banks, credit unions, and online lenders before you visit a dealership. This gives you a baseline interest rate and loan terms to compare against any offers from the dealership. It empowers you to negotiate from a position of strength and walk away if the dealership’s offer is inferior.

4. Read the Fine Print (Every Single Word)

This cannot be emphasized enough. Do not rush through the contract. Take your time, read every clause, and understand every term. If you don’t understand something, ask for clarification. If the lender or dealership pressures you to sign quickly, it’s a major red flag. Bring a trusted friend or advisor if possible.

5. Don’t Feel Pressured – Be Ready to Walk Away

Never let a salesperson or lender rush you into a decision. If you feel uncomfortable, pressured, or something seems off, simply walk away. There are always other cars and other lenders. Your financial well-being is more important than a "deal."

6. Beware of "Guaranteed Approval" Promises

Any lender promising "guaranteed approval" regardless of your credit history is likely a predatory lender. While they might approve you, the terms of the loan will almost certainly be highly unfavorable and designed to exploit your desperate situation. Legitimate lenders always assess risk.

7. Scrutinize All Fees and Add-ons

Demand an itemized list of all fees and question anything that seems excessive, vague, or unnecessary. If you don’t want an extended warranty or GAP insurance, explicitly decline them. Remember, these are often negotiable or can be purchased separately at a lower cost elsewhere.

8. Never Sign Blank Documents

This is a cardinal rule. Never, under any circumstances, sign a blank or incomplete loan agreement. Predatory lenders could fill in unfavorable terms after you’ve signed, making them legally binding. Ensure all fields are filled in and accurate before putting your signature down.

9. Understand the Total Cost, Not Just Monthly Payment

Predatory lenders often focus solely on the monthly payment to make an expensive loan seem affordable. Always look at the total amount you will pay over the life of the loan, including principal and interest. A low monthly payment over a very long term can result in a significantly higher total cost.

10. Seek Independent Advice

If you’re unsure about a loan offer, consider consulting with a trusted financial advisor, an attorney, or a consumer protection agency before signing anything. An impartial third party can provide invaluable insights and spot red flags you might miss.

Pro tips from us: Always get all promises, especially regarding interest rates, down payments, or trade-in values, in writing before signing the final contract. Verbal agreements are often meaningless once the ink is dry.

What to Do If You’re Already in a Predatory Car Loan

Discovering you’re trapped in a predatory car loan can be disheartening, but you do have options. Don’t despair; take action.

- Review Your Contract Thoroughly: The first step is to fully understand the terms you agreed to. Look for any clauses that might be illegal or highly unusual.

- Contact the Lender: Explain your situation and try to negotiate better terms, such as a lower interest rate or a more manageable payment plan. Be prepared for resistance, but persistence can sometimes pay off.

- Refinance Your Loan: If your credit score has improved or interest rates have dropped, you might be able to refinance your auto loan with a different, reputable lender. This could significantly reduce your interest rate and monthly payments.

- Seek Legal Advice: If you believe you’ve been a victim of illegal or deceptive practices, consult with an attorney specializing in consumer law. They can advise you on your rights and potential legal recourse.

- File a Complaint: You can file a complaint with consumer protection agencies, such as the Consumer Financial Protection Bureau (CFPB) or your state’s Attorney General’s office. While they may not resolve your individual case, they can investigate and potentially take action against the lender.

Consumer Protection and Your Rights

Consumers are protected by various federal and state laws designed to prevent predatory lending practices. Key federal laws include the Truth in Lending Act (TILA), which requires lenders to disclose loan terms clearly, and the Equal Credit Opportunity Act (ECOA), which prohibits discrimination.

Agencies like the Consumer Financial Protection Bureau (CFPB) work to ensure that consumers are treated fairly by financial institutions. Knowing your rights empowers you to challenge unfair practices. You can learn more about your rights and how to file a complaint directly on the CFPB’s official website: https://www.consumerfinance.gov/

Conclusion: Your Vigilance is Your Best Defense

Predatory car loans pose a significant threat to financial well-being, but they are not insurmountable. By understanding their characteristics, recognizing the red flags, and adopting a proactive, informed approach, you can protect yourself and make sound financial decisions. Remember, buying a car should be an exciting and empowering experience, not a source of long-term debt and regret.

Always prioritize financial literacy, read every document, ask questions, and never be afraid to walk away from a deal that doesn’t feel right. Your financial future depends on it. Share this article to help others navigate the complex world of auto financing and avoid the pitfalls of predatory lending.