The Invisible Road Ahead: What Happens When Your Car Loan Isn’t Reporting to Credit Bureaus?

The Invisible Road Ahead: What Happens When Your Car Loan Isn’t Reporting to Credit Bureaus? Carloan.Guidemechanic.com

The excitement of driving a new car is often matched only by the satisfaction of knowing you’re building a stronger financial future. For many, an auto loan is a cornerstone of their credit profile, a steady stream of on-time payments contributing significantly to a healthy credit score. But what if that vital piece of your financial puzzle goes missing? What if your car loan isn’t reporting to the credit bureau?

This isn’t just a minor inconvenience; it’s a significant roadblock that can hinder your credit-building efforts, impact future borrowing, and leave you feeling frustrated. As an expert blogger and professional SEO content writer, I’ve seen firsthand how often this issue arises and the confusion it causes. This comprehensive guide is designed to demystify the situation, explain why it happens, and arm you with the knowledge and steps needed to ensure your auto loan gets the credit it deserves. Let’s navigate this journey together.

The Invisible Road Ahead: What Happens When Your Car Loan Isn’t Reporting to Credit Bureaus?

The Unseen Impact: Why a Car Loan Not Reporting Matters

When you make consistent, on-time payments on any loan, especially an auto loan, you expect that positive activity to be reflected on your credit report. This information is crucial for your financial well-being. If your car loan isn’t reporting to the credit bureau, it’s like putting in all the work at the gym but never seeing the results on the scale.

Your Credit Score’s Foundation: Payment History

Payment history is arguably the most significant factor in calculating your credit score, typically accounting for 35% of your FICO score. It demonstrates your reliability as a borrower. Every single on-time car payment should ideally be a positive entry, building a robust history that reassures future lenders.

When this vital information is absent, your credit score misses out on a significant boost. It’s not just about avoiding negative marks; it’s about actively accumulating positive ones. Without your car loan showing up, a large chunk of your responsible financial behavior simply goes unnoticed by the system designed to track it.

The Thin File Dilemma: Building Credit From Scratch

For individuals with limited credit history, an auto loan is often one of the first major credit accounts they acquire. It serves as a crucial stepping stone, helping them establish a solid financial footprint. This is particularly true for young adults or newcomers to the credit system.

If this foundational loan isn’t reported, their credit file remains "thin," meaning it lacks sufficient data for credit bureaus to generate a strong score. A thin file can make it incredibly difficult to qualify for other forms of credit, like mortgages or personal loans, or even to secure favorable interest rates in the future. It’s like trying to build a house without a strong foundation.

Future Borrowing: The Ripple Effect

Credit reports are the primary tool lenders use to assess your creditworthiness. They want to see a history of responsible borrowing and repayment. If your car loan, which might be your largest or longest-standing debt, isn’t visible, lenders have less information to go on. This can lead to several negative outcomes.

You might be denied for future loans, offered higher interest rates, or required to put down a larger deposit. Lenders rely on a comprehensive view of your financial behavior, and an unreported auto loan creates a significant blind spot. Based on my experience, this can be incredibly frustrating, especially when you know you’ve been diligently making payments.

Decoding the Silence: Why Lenders Might Not Report Your Car Loan

It’s natural to assume all lenders report auto loans to the major credit bureaus (Experian, Equifax, and TransUnion). However, this isn’t always the case. There are several reasons why your car loan might not be reporting to the credit bureau. Understanding these can help you identify the root cause of the problem.

Small Lenders and Buy-Here, Pay-Here Dealerships

One of the most common reasons for an unreported car loan stems from the type of lender you’ve chosen. While large banks, credit unions, and major auto finance companies almost universally report to all three credit bureaus, smaller lenders or "buy-here, pay-here" dealerships often do not.

These smaller entities may lack the resources, the technical infrastructure, or even the direct agreements required to report to the national credit bureaus. Their business model might not prioritize credit building for their customers, focusing instead on direct lending relationships. They might also only report negative information, like defaults, but not positive payment history.

Manual Reporting and Administrative Glitches

Even with lenders that typically report, sometimes things fall through the cracks. Some smaller financial institutions might still rely on more manual processes for credit reporting, which increases the likelihood of human error. A simple administrative oversight, a data entry mistake, or a delay in processing can lead to your loan not appearing on your report.

Additionally, technical glitches or system updates at either the lender’s end or the credit bureau’s end can temporarily disrupt the reporting process. These aren’t malicious, but they are frustrating and require proactive intervention on your part.

The Loan Type: Some Don’t Qualify

In rare cases, the specific type of loan or the way it’s structured might prevent it from being reported. For instance, some informal loans or certain types of short-term financing might not fall under the categories that credit bureaus typically track. However, for standard auto loans, this is less common with established lenders.

It’s more likely to be an issue with highly specialized or non-traditional financing arrangements that are outside the conventional lending framework. Always clarify the reporting policy before committing to such an arrangement.

Deliberate Omission (Less Common, But Possible)

While less common, a lender might deliberately choose not to report, or they might only report negative information. This practice is generally frowned upon and can be detrimental to consumers, but it’s not illegal unless they’ve misrepresented their policies. This often ties back to the smaller, less regulated lenders mentioned earlier.

Pro tips from us: Always read your loan agreement carefully. If a lender makes verbal promises about reporting, ensure they are reflected in the written contract. If not, get a written statement confirming their reporting policy.

Signs Your Car Loan Isn’t Making Its Mark

You can’t fix a problem you don’t know exists. Being vigilant about your credit health is paramount. There are clear indicators that your car loan isn’t reporting to the credit bureau, and recognizing them early can save you a lot of hassle.

Regular Credit Report Checks: Your First Line of Defense

The most straightforward way to detect an unreported car loan is by regularly checking your credit reports. Under federal law, you are entitled to a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months. You can access these at AnnualCreditReport.com.

Make it a habit to review these reports thoroughly. Look for your auto loan listed under your open accounts. Check the lender’s name, the account number, the loan amount, and the payment history. If you don’t see your car loan listed, or if the information is incomplete or inaccurate, that’s your first major red flag.

Unexpected Credit Score Stagnation

Your credit score is dynamic; it changes as new information is added to your credit report. If you’ve been diligently making car payments on time for several months or even a year, and you notice your credit score isn’t improving as you’d expect, an unreported loan could be the culprit.

While many factors influence your credit score, consistent on-time payments on a significant loan like an auto loan should generally lead to a gradual increase, especially if you have a relatively new or thin credit file. If your score remains stagnant despite your efforts, it’s a good time to dig into your credit reports.

Taking Action: What to Do When Your Car Loan Isn’t Reporting

Discovering that your car loan isn’t reporting to the credit bureau can be disheartening, but it’s not a dead end. There are concrete steps you can take to rectify the situation. Persistence and meticulous record-keeping are your best allies here.

Step 1: Contact Your Lender Directly

Your first point of contact should always be your loan provider. Reach out to their customer service or, even better, their credit reporting department. Clearly explain the issue: your auto loan is not appearing on your credit reports.

Be prepared with your loan account number, personal identification, and the dates you’ve checked your credit reports. Ask them directly about their credit reporting policies and why your account isn’t being reported. Document everything: the date and time of your call, the name of the person you spoke with, and a summary of the conversation. If you can, follow up with a written letter or email, reiterating the conversation and your request. This creates a paper trail, which is invaluable if you need to escalate the issue.

Step 2: Gather Your Proof of Payments

While you’re discussing the issue with your lender, start compiling evidence of your consistent, on-time payments. This could include bank statements showing automatic debits, cancelled checks, or payment receipts. Having this documentation ready demonstrates your responsibility and provides undeniable proof of your payment history.

This evidence will be crucial if the lender disputes your claims or if you need to take further action with credit bureaus or regulatory bodies. It reinforces your position and makes it harder for anyone to dismiss your concerns.

Step 3: Dispute with the Credit Bureaus (If Lender is Unresponsive or Refuses)

If your lender is unhelpful, unresponsive, or outright refuses to report your loan, your next step is to dispute the omission directly with the credit bureaus. You’ll need to do this with each bureau where the loan is missing (Experian, Equifax, and TransUnion).

Each bureau has a formal dispute process, typically available online, by mail, or by phone. You will explain that your auto loan is missing from your report, provide your proof of payments, and include any communication you’ve had with your lender. The bureaus are legally obligated to investigate your claim within a certain timeframe, usually 30 days. For detailed information on your rights under the Fair Credit Reporting Act (FCRA), visit the Consumer Financial Protection Bureau’s (CFPB) website. They provide excellent resources on credit reporting disputes.

Step 4: Consider a Complaint with Regulatory Bodies

If all else fails, and your loan is still not reporting, you might need to involve regulatory agencies. You can file a complaint with the Consumer Financial Protection Bureau (CFPB) or your state’s Attorney General’s office. These bodies can investigate your complaint and, in some cases, compel lenders to take action.

Common mistakes to avoid are giving up too early or not documenting your efforts. Each step you take, every phone call, every email, every letter – keep a detailed record. This meticulous approach significantly strengthens your case.

Proactive Measures: Ensuring Your Auto Loan Builds Credit

Prevention is always better than cure. Before you even sign on the dotted line for a car loan, there are proactive steps you can take to ensure your investment in an automobile also translates into an investment in your credit health. This foresight can save you from the headache of a car loan not reporting to the credit bureau.

Before You Sign: Ask the Right Questions

When you’re shopping for an auto loan, don’t just focus on the interest rate and monthly payment. Make it a point to ask the lender directly about their credit reporting practices. Specifically, ask:

- "Do you report to all three major credit bureaus (Experian, Equifax, and TransUnion)?"

- "How often do you report (e.g., monthly, quarterly)?"

- "What is your policy regarding reporting positive payment history?"

Get these assurances in writing if possible, or make a note of who you spoke with and what they said. This simple conversation can provide immense peace of mind later on.

Choosing Your Lender Wisely

The choice of your lender plays a significant role in whether your loan will be reported. Generally, larger, more established financial institutions are more reliable when it comes to credit reporting. This includes:

- Major Banks: National and regional banks almost always report.

- Credit Unions: These member-owned institutions are known for their community focus and typically report to bureaus.

- Large Auto Finance Companies: Captive finance companies (e.g., Toyota Financial Services, Ford Credit) and independent large auto lenders have robust reporting systems.

Be wary of very small, local lenders or "buy-here, pay-here" dealerships unless you have explicit, written confirmation of their reporting practices. While they might offer loans to those with challenging credit, the trade-off can sometimes be a lack of credit-building potential. If you’re considering another auto financing option, our article on Understanding Different Types of Car Loans offers a detailed comparison to help you choose wisely.

Reviewing Loan Agreements Carefully

The loan agreement (or promissory note) is a legally binding document. Before you sign, take the time to read it thoroughly. Look for clauses related to credit reporting. While not all agreements explicitly state reporting practices, some might.

If you don’t see any mention, it’s another opportunity to ask questions and get clarification. Never assume; always verify. Understanding the terms and conditions upfront empowers you and helps prevent future surprises.

The Bigger Picture: Beyond Just One Loan

While addressing an unreported car loan is crucial, it’s also important to remember that it’s just one piece of your overall credit puzzle. Building and maintaining excellent credit is a continuous process that involves multiple financial habits and strategies.

Diversifying Your Credit Portfolio

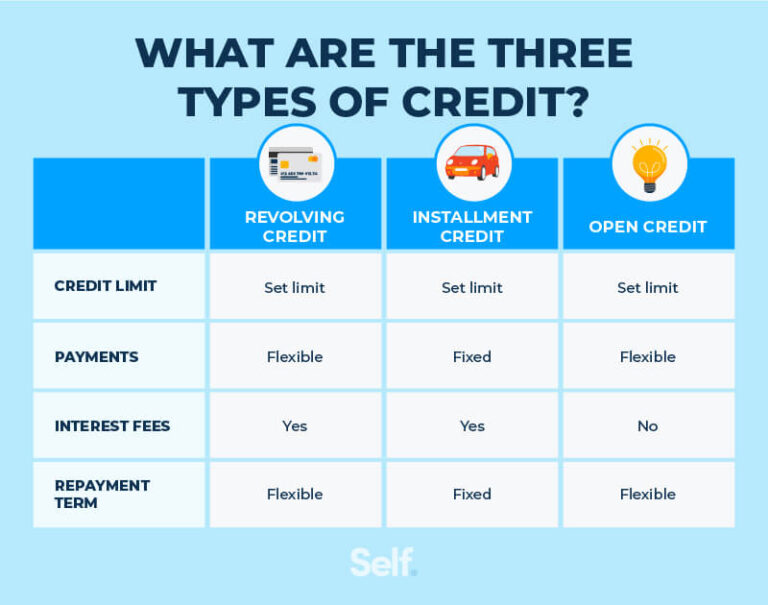

A healthy credit report isn’t just about having one type of loan. Lenders often look for a mix of credit types, such as installment loans (like car loans or mortgages) and revolving credit (like credit cards). This demonstrates your ability to manage different kinds of debt responsibly.

Once your car loan is reporting correctly, consider strategically adding other forms of credit to further diversify your portfolio. Just remember to only take on credit you truly need and can comfortably afford to repay.

The Power of Consistent, On-Time Payments

Regardless of the type of loan or credit account, the most powerful habit for building and maintaining a strong credit score is making all your payments on time, every single time. This is the bedrock of creditworthiness. Even if you faced issues with your car loan reporting, ensuring all your other accounts are paid punctually is non-negotiable.

For more insights on managing your overall credit health and improving your score, check out our guide on Improving Your Credit Score Fast. It provides actionable tips that complement the efforts you’re making with your auto loan.

Conclusion: Your Credit, Your Control

A car loan not reporting to the credit bureau can feel like an invisible burden, undermining your efforts to build a strong financial foundation. However, by understanding why this happens and knowing the precise steps to take, you empower yourself to resolve the issue.

Remember, your credit report is a reflection of your financial responsibility, and you have every right to ensure it is accurate and complete. Be proactive in checking your reports, diligent in communicating with your lenders, and persistent in advocating for your financial well-being. Your car loan is more than just a means to get from point A to point B; it’s a powerful tool for credit building when properly reported. Take control of your credit journey today!