The Longest Car Loan Period: Unpacking the Pros, Cons, and Smart Strategies for Extended Auto Financing

The Longest Car Loan Period: Unpacking the Pros, Cons, and Smart Strategies for Extended Auto Financing Carloan.Guidemechanic.com

In today’s automotive market, buying a new or even a quality used car often means navigating a complex landscape of financing options. One term that has gained significant traction and sometimes trepidation is the "longest car loan period." What was once considered an outlier, such as an 84-month car loan, is now increasingly common, and even 96-month loans are making an appearance.

But what exactly does opting for the longest car loan period mean for your finances, your ownership experience, and your long-term financial health? This comprehensive guide will delve deep into the world of extended car loans, offering expert insights, practical advice, and a clear understanding of whether this financing strategy is right for you. We aim to equip you with the knowledge to make an informed decision, ensuring you drive away not just with a new car, but with financial peace of mind.

The Longest Car Loan Period: Unpacking the Pros, Cons, and Smart Strategies for Extended Auto Financing

What Exactly Constitutes a "Long" Car Loan Period?

Historically, a standard car loan period typically ranged from 36 to 60 months, or 3 to 5 years. Anything beyond that was considered extended. However, as car prices have steadily climbed, so too have the average loan terms.

Today, a "long" car loan generally refers to terms of 72 months (6 years), 84 months (7 years), or even 96 months (8 years). These extended durations have become a popular tool for car buyers seeking to reduce their monthly payments and make higher-priced vehicles more "affordable" on a month-to-month basis.

The Rise of Extended Car Loan Terms: Why They’re So Popular

The shift towards longer car loan periods isn’t accidental; it’s a direct response to several market forces and consumer demands. Understanding these drivers is crucial for grasping the current financing landscape.

Firstly, vehicle prices, both new and used, have seen substantial increases over the past decade. Technological advancements, safety features, and supply chain issues have all contributed to higher sticker prices. This means the same car that cost $25,000 five years ago might now cost $35,000 or more.

Secondly, consumers often prioritize the monthly payment amount above all else. When faced with rising car prices, lenders and dealerships respond by stretching out loan terms to keep those monthly figures manageable. A lower monthly payment can make a seemingly out-of-reach car appear affordable, drawing more buyers into the market.

Lastly, economic pressures and stagnant wage growth for many households mean that while car prices go up, disposable income doesn’t always follow suit. Extended loan terms offer a way to fit a necessary purchase into a tight budget, even if it means paying more over the long run.

Understanding the "Longest Car Loan Period" Landscape

When we talk about the absolute longest car loan periods, we’re typically looking at 84-month and 96-month terms. These represent the furthest extent most lenders are willing to go, though availability can vary widely.

Based on my experience working with countless car buyers and lenders, 84 months has become a relatively common offering, particularly for new vehicles and buyers with strong credit. Ninety-six-month loans are less ubiquitous but are definitely on the rise, often seen as a niche product for specific situations or vehicles.

Several factors influence whether you can qualify for these extended terms. Your credit score is paramount, as lenders see longer terms as inherently riskier. The type of vehicle also plays a role; newer, more expensive vehicles are generally more eligible for extended terms than older, less valuable ones.

The Allure of Longer Loan Terms: Benefits Explained

It’s easy to see why longer car loan periods appeal to so many buyers. They offer distinct advantages that can significantly impact your immediate financial situation. However, it’s crucial to weigh these benefits against the potential drawbacks.

Lower Monthly Payments

This is, without a doubt, the primary driver for opting for an extended car loan. By stretching your loan repayment over a longer duration, the principal amount is divided into smaller, more manageable installments each month. This can significantly reduce the immediate financial burden of owning a new vehicle.

For many individuals and families, a lower monthly payment is the difference between affording a reliable car and being priced out of the market. It frees up cash flow for other essential expenses, savings, or investments, making a higher-value car more accessible. This immediate budget relief is a powerful incentive, especially in uncertain economic times.

Increased Purchasing Power

With lower monthly payments, you might find that you can afford a more expensive car than you initially thought. This means you could potentially upgrade to a model with more features, better safety technology, or simply a higher trim level that would have been out of reach with a shorter loan term.

This increased purchasing power can be appealing for those who want a specific vehicle for family needs, work requirements, or simply personal preference. It allows buyers to avoid compromising on their desired vehicle specifications due to upfront cost constraints.

Flexibility in Budgeting

A lower car payment provides greater flexibility in your overall monthly budget. This extra wiggle room can be a lifeline if unexpected expenses arise, like medical bills or home repairs. It also allows you to allocate funds to other financial goals, such as building an emergency fund, paying down high-interest debt, or contributing more to retirement savings.

This financial breathing room can reduce stress and provide a sense of security, knowing that your car payment isn’t consuming a disproportionate amount of your income. It’s about optimizing your cash flow to meet all your financial obligations and aspirations.

Accessibility for Certain Buyers

For some buyers, particularly those with less-than-perfect credit or limited down payment funds, extended loan terms can be the only way to secure financing for a necessary vehicle. Lenders might be more willing to approve a loan if the monthly payment is low enough to fit within the borrower’s debt-to-income ratio.

This democratizes access to newer, more reliable transportation, which can be critical for employment, family responsibilities, and overall quality of life. While not ideal, it provides an entry point for those who might otherwise be unable to finance a car.

The Hidden Perils: Risks and Downsides of Extended Car Loans

While the benefits of extended car loans are clear, it’s critical to understand the substantial risks and financial downsides. These long-term consequences often outweigh the immediate gratification of a lower monthly payment. Based on my experience, many buyers initially focus solely on the monthly payment, overlooking the true total cost.

Higher Total Interest Paid

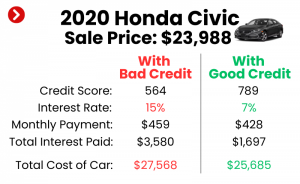

This is arguably the most significant drawback. The longer you take to repay a loan, the more interest accrues over the life of that loan. Even if the interest rate on an extended loan is the same as a shorter one (which it often isn’t, as longer terms typically carry higher rates), the sheer duration means you’ll pay significantly more in total interest.

For example, a $30,000 loan at 6% interest for 60 months might cost you around $4,700 in interest. The same loan for 84 months could easily push that interest total past $7,000. For 96 months, it could be well over $8,500. This extra cost can effectively make your car significantly more expensive than its sticker price.

Negative Equity (Upside Down) – A Major Concern

Negative equity, often called being "upside down" on your loan, occurs when the outstanding balance of your car loan is greater than the car’s actual market value. This is a very common and dangerous trap with extended car loans. Cars depreciate rapidly, especially in the first few years.

With a long loan term, your payments are stretched so thin that you pay off the principal very slowly. This means that for a significant portion of your loan term, your car’s value will likely be less than what you owe on it. This creates a precarious financial situation.

Depreciation vs. Loan Balance

The rapid depreciation of a vehicle, particularly a new one, works directly against the slow principal reduction of a long-term loan. Most cars lose 20-30% of their value in the first year alone, and continue to depreciate at a significant rate for several years. When you combine this with an 84- or 96-month payment schedule, you can spend years owing more than your car is worth.

This imbalance means that if your car is stolen, totaled in an accident, or you need to sell it prematurely, you could be left owing money on a car you no longer possess or have to make up the difference out of pocket. This is why gap insurance becomes almost a necessity for extended loans.

Longer Time to Ownership

While a shorter loan means higher monthly payments, it also means you pay off your car faster and achieve full ownership sooner. With an 84- or 96-month loan, you’re committed to that payment for a very long time. This can tie up your budget and limit your financial flexibility for nearly a decade.

Imagine still paying for a car you bought eight years ago. You might be ready for a new vehicle, but you’re still making payments on the old one, making it difficult to save for a down payment or take on a new loan.

Increased Risk of Mechanical Issues Post-Warranty

Most new car warranties expire around 36,000 to 60,000 miles, or 3 to 5 years. If you have an 84- or 96-month loan, you’ll be making payments for several years after your car is no longer covered by its original warranty. This means any significant mechanical issues, which become more likely as a car ages, will come directly out of your pocket.

This can lead to a double financial burden: a hefty monthly payment combined with expensive, unexpected repair bills. Pro tips from us: Always factor in potential maintenance costs when considering a long loan term.

Impact on Future Financial Goals

Committing to a long-term, expensive car payment can significantly hinder your ability to achieve other important financial goals. Saving for a down payment on a house, contributing to retirement, investing, paying for education, or even just building a robust emergency fund can become much harder when a large portion of your income is dedicated to a car payment for nearly a decade.

Common mistakes to avoid are underestimating how much this long-term commitment can delay your other financial aspirations. It’s crucial to look beyond the immediate month-to-month and consider the broader impact on your financial future.

Qualifying for the Longest Car Loan Periods

Securing an 84-month or 96-month car loan isn’t a given. Lenders view these extended terms as higher risk due to the prolonged commitment and increased potential for negative equity. Therefore, they typically require borrowers to meet stringent criteria.

First and foremost, you’ll need an excellent credit score. Lenders want to see a proven history of responsible borrowing and repayment. A score in the upper 700s or 800s significantly increases your chances. A strong credit profile signals to the lender that you are a reliable borrower, even over an extended period.

Secondly, a stable income and a favorable debt-to-income (DTI) ratio are crucial. Lenders will assess your ability to comfortably afford the monthly payments, even if they are lower. Your DTI ratio, which compares your total monthly debt payments to your gross monthly income, needs to be low enough to demonstrate you’re not overextending yourself.

Third, a significant down payment can make a big difference. Putting down 20% or more of the vehicle’s purchase price not only reduces the amount you need to borrow but also helps mitigate the risk of negative equity. It shows the lender your commitment and reduces their exposure.

Finally, the vehicle itself plays a role. Lenders are more likely to approve extended terms for newer, more reliable vehicles that are less likely to break down and maintain their value better. An older or high-mileage car will almost certainly not qualify for the longest loan periods.

Is an 84-Month or 96-Month Loan Right for You? A Decision Framework

Deciding on an extended car loan requires careful introspection and a thorough evaluation of your personal circumstances. There’s no one-size-fits-all answer.

Consider your personal financial situation. Do you have a stable job with good prospects for income growth? Do you have an emergency fund? How comfortable are you with a long-term debt commitment? If your financial situation is robust and predictable, the risks might be more manageable.

Next, think about your vehicle choice. Are you buying a car known for its reliability and strong resale value, or one that might depreciate quickly and require costly maintenance? A car that holds its value better reduces the risk of negative equity over a long term.

Your risk tolerance is also a key factor. Are you comfortable with the possibility of being upside down on your loan for several years? Are you prepared for potential out-of-warranty repairs? If these scenarios cause significant stress, a shorter loan might be a better fit.

Finally, explore alternative strategies. Could you save for a larger down payment? Would a slightly less expensive used car meet your needs without requiring such a long loan term? Sometimes, adjusting your expectations or saving a bit longer can lead to a much more financially sound decision.

Strategies to Mitigate Risks with Long-Term Car Loans

If, after careful consideration, you decide that an extended car loan is your best option, there are proactive steps you can take to minimize the inherent risks. These strategies require discipline and foresight.

Making Extra Payments: Even small, extra payments towards your principal each month can significantly reduce the total interest paid and shorten your loan term. Every dollar extra you pay goes directly towards reducing your loan balance, helping you build equity faster. This is one of the most effective ways to counteract the downsides of a long loan.

Refinancing: As your credit score improves or interest rates drop, you might be able to refinance your car loan for a lower interest rate or even a shorter term. This can save you a substantial amount of money over the remaining life of the loan. Always keep an eye on market conditions and your credit health.

Gap Insurance: Given the high risk of negative equity with extended loans, gap insurance is almost a non-negotiable. This insurance covers the "gap" between what you owe on your loan and your car’s actual cash value if it’s totaled or stolen. Without it, you could be stuck paying off a car you no longer have.

Maintaining the Vehicle: With a long loan, you’ll own the car for many years. Regular and diligent maintenance is crucial to ensure its longevity and reliability, especially after the manufacturer’s warranty expires. This helps prevent costly repairs that could compound your financial burden.

Selling Strategically: If you anticipate needing to sell your car before the loan is paid off, research its resale value trends. Try to time your sale when the car’s market value is likely to be closer to your outstanding loan balance, minimizing any potential losses from negative equity.

Expert Insights and Pro Tips

Based on my experience working with countless car buyers, here are some invaluable tips to navigate the world of car financing, especially when considering extended terms:

- Always compare offers from multiple lenders. Don’t just accept the financing offered by the dealership. Get pre-approved by banks, credit unions, and online lenders before you even step foot on the lot. This gives you leverage and ensures you get the best possible rate and terms.

- Understand the fine print. Don’t rush through the loan agreement. Read every line, understand all fees, and clarify any terms you don’t fully grasp. Pay close attention to prepayment penalties, which are rare but can exist.

- Focus on the total cost, not just the monthly payment. While the monthly payment is important for budgeting, the total amount you’ll pay over the life of the loan (principal + interest) is the true cost of the vehicle. Use online calculators to compare total costs across different loan terms and interest rates.

- Aim for a substantial down payment. The more you put down upfront, the less you need to borrow, which directly reduces your total interest paid and helps you avoid negative equity. A 20% down payment is often recommended as a good benchmark.

- Consider Certified Pre-Owned (CPO) vehicles. If a new car on an extended loan seems too risky, a CPO vehicle offers many of the benefits of a new car (inspected, often comes with an extended warranty) but at a lower price point, potentially allowing for a shorter, more manageable loan term.

Common Mistakes to Avoid When Considering Extended Car Loans

Navigating car financing can be tricky, and certain pitfalls are especially prevalent with extended loan terms. Being aware of these common mistakes can save you significant financial heartache.

One of the biggest errors is ignoring the total interest paid. Many buyers get fixated on the low monthly payment and fail to calculate the true, much higher, overall cost of the loan. Always use an amortization calculator to see the breakdown of principal and interest over time.

Another frequent mistake is underestimating depreciation. Cars lose value rapidly, and with a long loan, you’re almost guaranteed to be upside down for a significant period. This makes it difficult to sell or trade in your car without incurring a loss.

Skipping gap insurance is a dangerous gamble when you have an extended loan. If your car is totaled and you owe more than its market value, you’ll be personally responsible for the difference without this crucial coverage. It’s a small premium for significant protection.

Many buyers also fail to budget for maintenance and repairs, especially as the car ages beyond its warranty. With an 84- or 96-month loan, you will definitely encounter out-of-warranty issues. Not having funds set aside for these can lead to further debt or difficulty maintaining your vehicle.

Finally, rushing the decision is a pervasive error. Car buying should not be an impulse decision, especially when committing to such a long-term financial obligation. Take your time, research thoroughly, compare options, and don’t feel pressured by salespeople.

Conclusion: Making an Informed Decision About the Longest Car Loan Period

The longest car loan periods, such as 84-month and 96-month terms, offer an attractive solution for reducing monthly payments and accessing higher-priced vehicles. They provide immediate budget relief and increased purchasing power, which can be invaluable for many consumers. However, these benefits come with substantial long-term financial risks, including significantly higher total interest costs, a prolonged period of negative equity, and a longer commitment that can impact future financial goals.

As an expert in this field, my ultimate advice is to approach extended car loans with extreme caution and a full understanding of their implications. While they can be a viable option in specific, well-thought-out circumstances, they are rarely the most financially prudent choice. Always prioritize the total cost of the loan over just the monthly payment. Explore alternatives, make a substantial down payment, and if you do opt for a longer term, implement strategies to mitigate the risks.

Making an informed decision about your car loan is about balancing your immediate needs with your long-term financial health. By understanding the pros, cons, and smart strategies discussed here, you can drive away with a car that fits your lifestyle and a financing plan that aligns with your financial well-being.