The Road Ahead: Navigating Your Car Loan’s Impact On Your Credit Score

The Road Ahead: Navigating Your Car Loan’s Impact On Your Credit Score Carloan.Guidemechanic.com

Buying a car is a significant milestone for many, offering freedom, convenience, and a sense of accomplishment. For most, this journey involves securing a car loan, a financial commitment that can last several years. What many don’t fully realize, however, is the profound and lasting car loan impact on credit score. This isn’t just about getting approved; it’s about understanding how this major financial product can shape your financial future.

As an expert blogger and professional SEO content writer, I’ve seen countless individuals make decisions about car loans without fully grasping the credit implications. This article will serve as your ultimate guide, meticulously detailing every facet of how an auto loan interacts with your credit score. We’ll explore the initial application, the ongoing payment period, and strategies to ensure your car loan becomes a powerful tool for building, rather than damaging, your credit.

The Road Ahead: Navigating Your Car Loan’s Impact On Your Credit Score

Understanding Your Credit Score: The Foundation of Financial Health

Before diving into the specifics of car loans, it’s crucial to understand what your credit score is and why it holds so much weight. Essentially, your credit score is a three-digit number that summarizes your creditworthiness. It’s a quick snapshot for lenders, indicating how likely you are to repay borrowed money.

Most commonly, you’ll encounter FICO scores and VantageScores, both widely used by lenders. These scores are derived from the information within your credit reports, which are detailed records of your borrowing and repayment history. A higher score signifies lower risk to lenders, opening doors to better interest rates and more favorable loan terms.

Why Does Your Credit Score Matter for a Car Loan?

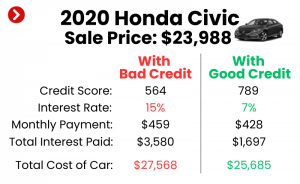

Your credit score directly influences several critical aspects of your car loan. Firstly, it dictates your approval chances. Lenders use your score to assess your risk profile; a low score might lead to a denial or require a co-signer. Secondly, and perhaps most importantly, your score determines the interest rate you’ll be offered.

A strong credit score can save you thousands of dollars over the life of your car loan through lower interest payments. Conversely, a poor score means higher interest rates, significantly increasing your total cost of ownership. Understanding this direct correlation is the first step in leveraging your car loan to your advantage.

Key Factors Influencing Your Credit Score

Your credit score isn’t a mysterious number; it’s calculated based on several well-defined categories. Grasping these components is vital for anyone considering a car loan, as they highlight the areas where your auto loan will have the most significant impact.

1. Payment History (35% of FICO Score): The Cornerstone

This is, without a doubt, the most critical factor. Your payment history reflects whether you pay your bills on time. Every late payment, especially those 30, 60, or 90 days past due, can severely damage your score. A car loan, with its regular monthly installments, presents a consistent opportunity to demonstrate responsible payment behavior.

Consistently making your car loan payments on time is the single best way to positively influence your credit score. It shows lenders you are reliable and can manage your financial obligations effectively. This positive habit forms the bedrock of a strong credit profile.

2. Amounts Owed / Credit Utilization (30% of FICO Score): Managing Your Debt

This factor looks at how much credit you’re using compared to how much credit you have available. For revolving credit like credit cards, keeping your utilization below 30% is generally recommended. While a car loan is an installment loan (a fixed amount borrowed over a set period), the total loan amount contributes to your overall debt burden.

A very high car loan amount relative to your income or other credit limits could indirectly affect this factor by increasing your overall debt-to-income ratio. This ratio, while not a direct scoring factor, is a crucial metric lenders consider when evaluating new applications. Managing your total debt wisely is key.

3. Length of Credit History (15% of FICO Score): Time and Experience

This factor considers how long your credit accounts have been open and how long it’s been since you used them. A longer credit history, especially with well-managed accounts, generally leads to a higher score. A car loan, often spanning several years, becomes a long-term fixture on your credit report.

Successfully managing a car loan for an extended period demonstrates your ability to handle long-term financial commitments. This adds maturity and stability to your credit file, which is viewed favorably by credit scoring models. It’s a testament to your sustained financial responsibility.

4. New Credit (10% of FICO Score): The Application Effect

This category evaluates how many new credit accounts you’ve recently opened and how many hard inquiries appear on your report. A hard inquiry occurs when a lender pulls your credit report to make a lending decision. While necessary for a car loan, too many inquiries in a short period can slightly ding your score.

However, credit scoring models are smart. They often recognize "rate shopping" for specific loan types, like auto loans or mortgages. Multiple inquiries for the same type of loan within a concentrated period (usually 14-45 days, depending on the scoring model) are often treated as a single inquiry, minimizing the negative impact.

5. Credit Mix (10% of FICO Score): Diversification is Key

Credit mix looks at the different types of credit accounts you have, such as revolving credit (credit cards) and installment loans (car loans, mortgages, student loans). Having a healthy mix demonstrates your ability to manage various forms of credit responsibly. A car loan adds an installment loan to your credit portfolio.

For individuals with limited credit history, or primarily revolving credit, adding an installment loan like a car loan can positively diversify their credit mix. This shows lenders you can handle different types of financial products, broadening your credit profile.

The Initial Impact: Applying for a Car Loan

The moment you apply for a car loan, your credit score begins to feel its effects. Understanding these initial changes can help you navigate the application process strategically.

Hard Inquiries: What They Are and Their Effect

When a lender reviews your credit report to decide whether to grant you a loan, it generates a "hard inquiry." This inquiry is recorded on your credit report and can cause a small, temporary dip in your credit score, typically by a few points. This dip usually lasts for a few months but the inquiry itself remains on your report for two years.

It’s a natural part of the lending process. Don’t let the fear of a hard inquiry deter you from seeking the best rates. The impact is generally minor and short-lived, especially when balanced against the potential savings from securing a lower interest rate.

Shopping Around: How Multiple Inquiries Are Treated

Based on my experience, many people worry about applying to multiple dealerships or lenders for a car loan, fearing numerous hard inquiries will decimate their score. However, credit scoring models are designed to account for this. As mentioned earlier, FICO and VantageScore models typically recognize a "rate shopping window."

This means that multiple inquiries for the same type of loan (like an auto loan) within a specific timeframe – often 14 to 45 days – are usually counted as a single inquiry. This allows you to compare offers from various lenders without undue penalty, ensuring you get the most competitive interest rate available. Pro tips from us: always shop for your loan before you fall in love with a car.

Loan Approval: What Lenders Look For Beyond the Score

While your credit score is a primary factor, lenders also consider other elements during the approval process. They’ll look at your debt-to-income (DTI) ratio, which compares your monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments.

They also consider your employment history, income stability, and down payment amount. A substantial down payment reduces the loan amount, making you a less risky borrower. Your overall financial stability, beyond just your score, plays a crucial role in securing favorable terms.

The Ongoing Impact: Managing Your Car Loan

Once approved and driving your new car, the real long-term car loan impact on credit score begins. This period offers significant opportunities to either bolster your credit or inadvertently damage it.

Positive Impact: Building a Strong Credit Foundation

A car loan, when managed responsibly, can be an excellent tool for credit building. It provides a structured way to demonstrate your financial reliability over an extended period.

-

Payment History: The Most Crucial Factor

Consistently making on-time payments is paramount. Each month, when your payment is reported to the credit bureaus, it reinforces a positive payment history. This is the single biggest contributor to a healthy credit score. Based on my experience, individuals who prioritize timely payments on their auto loans often see steady and significant improvements in their credit scores, especially if they started with a limited credit history. It’s a powerful testament to your reliability. -

Credit Mix: Diversifying Your Portfolio

Adding an installment loan, like a car loan, to your credit report diversifies your credit mix. If your credit file previously consisted only of credit cards (revolving credit), a car loan shows you can manage different types of debt. This diversification is seen favorably by credit scoring models, contributing to a more robust credit profile. It proves your versatility as a borrower. -

Building Credit History: Especially for New Borrowers

For those just starting their credit journey, a car loan can be an invaluable first step. It establishes a payment history and length of credit history, two vital components of your credit score. Successfully managing your first major loan demonstrates to future lenders that you are a responsible borrower, paving the way for other financial milestones like a mortgage. It’s a stepping stone to greater financial opportunities.

Negative Impact: Pitfalls to Avoid

Unfortunately, a car loan can also severely damage your credit if not managed carefully. Common mistakes to avoid are neglecting payment due dates or overextending yourself financially.

-

Missed or Late Payments: Severe Consequences

Missing a payment or making it more than 30 days late is a red flag on your credit report. A single late payment can cause your score to drop significantly, sometimes by dozens of points. Multiple late payments can compound this damage, making it much harder to secure future credit or obtain favorable interest rates. The impact of a late payment can linger on your report for up to seven years. -

Defaulting on the Loan: Repossession and Long-Term Damage

If you consistently fail to make payments, the lender may repossess your vehicle. A repossession is a severe negative mark on your credit report, comparable to a bankruptcy in its severity. It will drastically lower your credit score and remain on your report for seven years, making it incredibly difficult to obtain any new credit in the future. This is a scenario to avoid at all costs. -

High Debt-to-Income Ratio: Affecting Future Borrowing

While the car loan itself might not directly impact your credit utilization, a large car loan payment can significantly increase your debt-to-income (DTI) ratio. Lenders use DTI to assess your ability to take on additional debt. A high DTI might prevent you from getting approved for other loans, like a mortgage, even if your credit score is otherwise good. It indicates you’re stretched thin financially.

Strategies for Maximizing Positive Impact & Minimizing Negative

Now that you understand the mechanics, let’s explore actionable strategies to ensure your car loan is a credit-building asset, not a liability.

1. Making Payments on Time, Every Time

This is non-negotiable. Set up automatic payments from your bank account to ensure you never miss a due date. If automatic payments aren’t an option, mark your calendar, set reminders, or use budgeting apps. Consistency is key here. Every single on-time payment reinforces a positive credit history.

2. Understanding Your Loan Terms

Before you sign, read your loan agreement thoroughly. Know your interest rate, monthly payment amount, due date, and any fees for late payments or early payoff. A clear understanding prevents surprises and helps you budget effectively. Don’t be afraid to ask questions until everything is crystal clear.

3. Considering a Shorter Loan Term (If Affordable)

While a longer loan term means lower monthly payments, it often results in paying more interest over time. A shorter loan term, if your budget allows, means you’ll pay off the debt faster and accrue less interest. This also means the positive payment history is established and concluded sooner, freeing up your debt capacity.

4. Refinancing Your Car Loan: When and Why

If your credit score has significantly improved since you initially took out your car loan, or if interest rates have dropped, refinancing could be a smart move. Refinancing replaces your old loan with a new one, potentially at a lower interest rate, which can save you money and reduce your monthly payment. This can free up cash flow for other financial goals.

For a deeper dive into understanding your credit report and how it impacts refinancing, check out our comprehensive guide on .

5. Monitoring Your Credit Report

Regularly review your credit reports from all three major bureaus (Experian, Equifax, and TransUnion). You can get a free copy of your report annually from AnnualCreditReport.com. Look for any errors or inaccuracies, especially regarding your car loan payments, and dispute them immediately. This proactive approach protects your credit.

6. Pro Tips for Car Loan Success

- Down Payment Power: A larger down payment reduces the amount you need to borrow, which can lead to lower monthly payments and less interest paid over the life of the loan. It also shows lenders you have skin in the game, making you a more attractive borrower.

- Budget Wisely: Don’t just focus on the monthly payment. Factor in insurance, fuel, maintenance, and registration fees when calculating the true cost of car ownership. An affordable car loan fits comfortably within your overall budget.

- Avoid Excessive Add-ons: While tempting, many dealership add-ons (extended warranties, paint protection) can significantly increase your loan amount. Carefully consider if these are truly necessary or if you can purchase them separately for less.

- Build an Emergency Fund: Having an emergency fund can prevent you from missing car loan payments if unexpected expenses arise. This financial cushion is invaluable for maintaining your credit health.

Special Considerations

The car loan impact on credit score can vary based on individual circumstances and the strategies employed.

Car Loans for Bad Credit: Is It Possible? What to Expect

Yes, it is possible to get a car loan with bad credit, but it comes with caveats. Lenders offering "bad credit auto loans" typically charge much higher interest rates to compensate for the increased risk. You might also be required to make a larger down payment or secure a co-signer. While it can be an opportunity to rebuild credit, the high cost means careful consideration is paramount.

Co-signers: How They Impact Both Scores

If you have limited or poor credit, a co-signer with good credit can significantly improve your chances of loan approval and secure a better interest rate. However, a co-signer shares equal responsibility for the loan. If the primary borrower misses payments, both credit scores will be negatively affected. It’s a significant commitment for the co-signer.

Paying Off Your Car Loan Early: Good or Bad for Credit?

Paying off your car loan early is generally a good financial move as it saves you money on interest. From a credit score perspective, it usually has a neutral to slightly positive effect. It closes an account in good standing, which is positive. However, it also reduces your length of credit history if it was one of your oldest accounts, and removes an installment loan from your credit mix. The financial savings usually outweigh any minor, temporary credit score nuances. Always check for prepayment penalties before paying off early.

If you’re curious about different types of credit and how they affect your score, explore our article on .

For more detailed information on FICO scores and how they are calculated, visit the official FICO website at https://www.myfico.com/credit-education.

Conclusion: Driving Towards a Healthier Credit Future

The car loan impact on credit score is undeniably significant, touching every aspect of your financial reputation. From the initial hard inquiry to the final payment, every action you take reverberates through your credit file. By understanding how credit scores work and adopting responsible borrowing habits, your car loan can become a powerful vehicle for credit building.

Remember, consistent on-time payments are your greatest asset. Pair this with wise financial planning, active credit monitoring, and a clear understanding of your loan terms, and you’ll not only enjoy the freedom of the open road but also steer your credit score towards a stronger, healthier future. Drive smart, and your financial journey will be much smoother.

What has been your experience with car loans and their impact on your credit? Share your thoughts and tips in the comments below!