The Road to Better Credit: How Much Can a Car Loan Truly Boost Your Score?

The Road to Better Credit: How Much Can a Car Loan Truly Boost Your Score? Carloan.Guidemechanic.com

Embarking on the journey of car ownership is an exciting milestone for many. Beyond the thrill of a new ride, securing an auto loan often presents a unique opportunity: the chance to significantly improve your credit score. But the big question on many minds is, "How much can a car loan improve your credit?" It’s not a simple yes or no answer, nor is it a guaranteed overnight miracle.

Based on my experience working with countless individuals navigating their financial paths, a car loan, when managed responsibly, can be a powerful catalyst for credit growth. However, its impact is nuanced, depending heavily on your current credit standing, payment discipline, and other financial behaviors. This comprehensive guide will delve deep into the mechanics, benefits, pitfalls, and strategies to maximize your car loan’s positive influence on your credit score, transforming it into a true pillar of your financial stability.

The Road to Better Credit: How Much Can a Car Loan Truly Boost Your Score?

Understanding Your Credit Score: The Foundation of Financial Health

Before we unpack how a car loan can influence your credit, it’s crucial to grasp what a credit score is and why it matters. Essentially, your credit score is a three-digit number that reflects your creditworthiness – your ability to manage and repay debt. Lenders use it to assess risk when you apply for loans, credit cards, or even apartments.

A higher score generally translates to better interest rates, more favorable loan terms, and easier access to financial products. Conversely, a lower score can make borrowing more expensive or even impossible. Your credit score is not static; it’s a dynamic reflection of your financial behavior, constantly evolving with every financial decision you make.

The most widely used credit scoring models, like FICO and VantageScore, consider several key factors:

- Payment History (35%): This is the single most important factor. Timely payments demonstrate reliability.

- Amounts Owed / Credit Utilization (30%): How much credit you’re using compared to your total available credit.

- Length of Credit History (15%): The age of your oldest account and the average age of all your accounts.

- Credit Mix (10%): Having a healthy variety of credit accounts (e.g., credit cards, installment loans).

- New Credit (10%): How many new credit accounts you’ve recently opened and hard inquiries on your report.

Understanding these components is the first step in strategically leveraging a car loan for credit improvement.

The Mechanics of a Car Loan and Your Credit Report

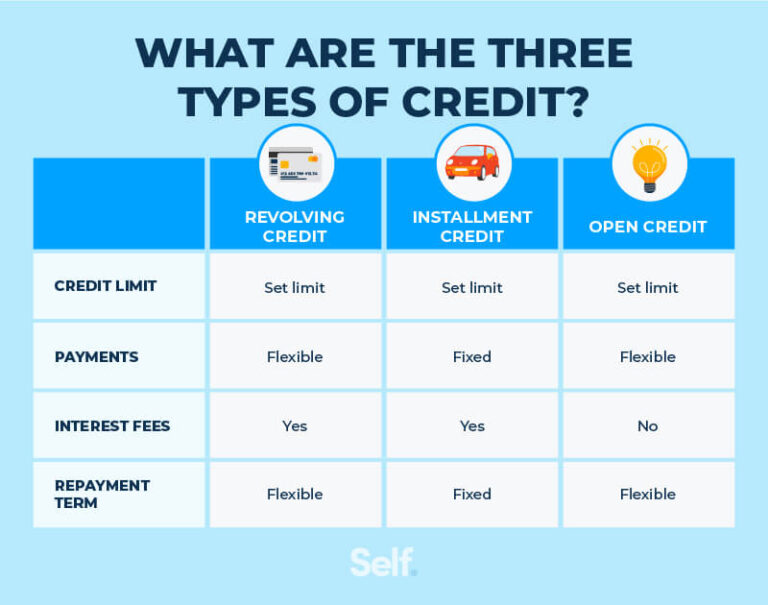

When you take out a car loan, it enters your credit report as an "installment loan." Unlike revolving credit (like a credit card, where you can borrow and repay repeatedly up to a limit), an installment loan has a fixed principal amount, a set number of regular payments, and a defined end date.

Initially, applying for a car loan typically results in a "hard inquiry" on your credit report. This occurs when a lender pulls your credit report to assess your risk. A single hard inquiry might cause a slight, temporary dip in your score, usually by a few points. However, credit scoring models are smart; they recognize that consumers shop around for the best rates. Multiple inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are usually treated as a single inquiry, minimizing their impact.

Once the loan is approved and reported to the credit bureaus, it becomes a new account on your credit file. This new account, with its principal amount and payment schedule, immediately begins to influence your credit score based on the factors mentioned above.

How a Car Loan Can Significantly Improve Your Credit

The potential for a car loan to boost your credit score is substantial, primarily because it touches upon several critical scoring factors simultaneously. Let’s explore these in detail.

1. Consistent, On-Time Payments: The Cornerstone of Credit Building

This is, without a doubt, the most powerful way a car loan can improve your credit. Payment history accounts for 35% of your FICO score, making it the largest determining factor. Each month you make your car payment on time, you are actively building a positive payment track record.

This demonstrates to lenders that you are a reliable borrower who honors financial commitments. Over months and years, a consistent history of timely car payments creates a strong foundation of creditworthiness. Even if your credit score starts low, diligently making payments on your auto loan can show significant improvement, often resulting in noticeable score increases over time.

2. Diversifying Your Credit Mix: A Balanced Portfolio

Your credit mix, which accounts for 10% of your FICO score, refers to the different types of credit you manage. Many people primarily have revolving credit, such as credit cards. Adding an installment loan, like a car loan, diversifies your credit portfolio.

Lenders appreciate seeing that you can responsibly manage different types of credit. It indicates a broader financial capability. Having a mix of both revolving and installment accounts can demonstrate a more robust and well-rounded financial profile, which can positively influence your credit score. It shows you’re not solely reliant on one type of credit, making you appear less risky.

3. Establishing a Longer Credit History: Time is Your Ally

The length of your credit history contributes 15% to your FICO score. This factor considers the age of your oldest account, the age of your newest account, and the average age of all your accounts. For individuals with a "thin" credit file – meaning they have few accounts or a short credit history – a car loan can be particularly beneficial.

A car loan typically has a term of several years (e.g., 3 to 7 years). As this account ages on your credit report, it steadily contributes to a longer credit history. This is especially valuable for younger individuals or those new to credit, helping them establish a solid foundation over time. Keeping this account open and in good standing for its full term will continue to add positive data to your credit file.

4. Lowering Credit Utilization (Indirectly): A Positive Side Effect

While credit utilization primarily applies to revolving credit, an installment loan can indirectly help your overall credit picture. When you take out a car loan, it adds a significant amount to your total debt, but it doesn’t affect your revolving credit utilization ratio in the same way.

However, if having a car loan helps you avoid relying heavily on credit cards for large purchases, it can prevent your revolving utilization from spiking. Furthermore, as you pay down your car loan, the outstanding balance decreases, which can improve your overall debt-to-income ratio in the eyes of some lenders, even if it doesn’t directly impact the credit utilization percentage that credit bureaus calculate for revolving accounts.

5. Building a Positive Payment Track Record: Demonstrating Responsibility

Every on-time payment on your car loan is a testament to your financial responsibility. This positive track record is highly valued by lenders. It’s not just about the numbers; it’s about the narrative your credit report tells.

A history of diligently making car payments signals that you are a reliable borrower. This positive narrative can make it easier to qualify for other loans in the future, such as a mortgage, and often at more attractive interest rates. Based on my experience, consistently demonstrating this level of financial discipline is the single most effective way to build and maintain an excellent credit score.

Potential Pitfalls: When a Car Loan Can Harm Your Credit

While a car loan offers significant potential for credit improvement, it’s not a foolproof strategy. Mismanaging an auto loan can just as easily damage your credit, sometimes severely. Common mistakes to avoid are crucial to understanding.

1. Late Payments or Defaults: The Quickest Way to Damage Credit

This is the most critical pitfall. Missing a car payment, or making it significantly late (typically 30 days or more past the due date), will be reported to credit bureaus and can cause a substantial drop in your credit score. A single 30-day late payment can knock dozens of points off your score, and subsequent late payments or a default can be even more devastating.

A vehicle repossession, which occurs if you default on your loan, is one of the most severe negative marks you can have on your credit report. It can stay on your report for up to seven years, making it incredibly difficult to obtain credit in the future.

2. Excessive Hard Inquiries: Too Much Shopping Around

While shopping for car loans, multiple inquiries within a short period are often grouped as one by credit scoring models. However, if you apply for many different types of loans over an extended period, each inquiry can cause a small, temporary dip in your score.

It’s wise to limit your loan applications to a concentrated period when you’re serious about purchasing. Applying for every loan under the sun without a clear strategy can make you look desperate for credit, which lenders view as a risk.

3. Taking on Too Much Debt: The Burden of Overextension

Committing to a car loan payment that stretches your budget too thin can lead to financial strain. If your monthly car payment, combined with other debt obligations, consumes too much of your income, you might struggle to make payments on time.

This can negatively impact your debt-to-income (DTI) ratio, a metric lenders use to assess your ability to manage monthly payments. A high DTI can signal to future lenders that you are overextended, even if you are making all your current payments on time.

4. Short Loan Terms with High Payments: A Recipe for Trouble

While a shorter loan term means you pay less interest overall, it also means higher monthly payments. If you choose a loan term that results in payments you can barely afford, you’re setting yourself up for potential late payments.

It’s far better to opt for a slightly longer term with a more manageable payment, even if it means paying a bit more in interest, if it ensures you can consistently pay on time. The positive impact of consistent, on-time payments far outweighs the small savings from a shorter, riskier loan term.

Strategies for Maximizing Credit Improvement with a Car Loan

To ensure your car loan is a credit-building powerhouse rather than a credit-damaging liability, proactive strategies are essential. Pro tips from us include focusing on responsible borrowing and diligent management.

1. Shop Smart for Your Loan: Research and Compare

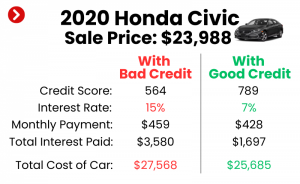

Don’t just take the first loan offer you receive. Research different lenders, compare interest rates, and understand all the terms and conditions. Getting pre-approved from a few lenders can give you leverage at the dealership and helps you understand what rates you qualify for. This also allows for the "rate shopping" grace period, where multiple inquiries count as one.

A lower interest rate means more of your payment goes towards the principal, and it makes the loan more affordable overall, reducing financial stress. Remember, a better loan deal can translate to an easier payment experience, which directly supports consistent, on-time payments.

2. Choose a Manageable Payment: Affordability is Key

Before you even start shopping for a car, determine what you can realistically afford for a monthly payment. Factor in not just the loan payment, but also insurance, fuel, maintenance, and potential parking costs. A payment that fits comfortably within your budget drastically reduces the risk of late payments.

It’s often tempting to stretch for a more expensive vehicle, but financial prudence dictates prioritizing affordability. A slightly less flashy car with a manageable payment is a much better choice for your credit health than a dream car that puts you in financial jeopardy.

3. Set Up Auto-Pay: Eliminate the Risk of Missed Payments

One of the simplest yet most effective strategies is to set up automatic payments from your bank account. This ensures your payment is always made on time, every single month, without you having to remember. It removes the human error factor and guarantees you’re building that crucial positive payment history.

Automating your payments removes stress and helps you avoid the severe penalties of late payments. It’s a fundamental step in ensuring your car loan works for your credit score.

4. Monitor Your Credit Report Regularly: Stay Informed

Regularly check your credit report from all three major bureaus (Experian, Equifax, and TransUnion) at AnnualCreditReport.com. This allows you to spot any errors, such as incorrect late payments, which can unfairly drag down your score. You can also monitor the progress of your car loan reporting and ensure everything is accurate.

Staying informed about your credit report is a proactive step in managing your financial health. It empowers you to dispute inaccuracies and ensure your efforts to build credit are correctly reflected.

5. Don’t Forget Your Other Credit: A Holistic Approach

While a car loan can be a powerful tool, it’s just one piece of the puzzle. Continue to manage all your other credit accounts responsibly. Keep your credit card utilization low, make all other loan payments on time, and avoid opening too many new credit accounts simultaneously.

A holistic approach to credit management ensures that while your car loan is working its magic, other aspects of your financial life aren’t undermining your efforts. All aspects of your credit profile contribute to your overall score.

The "How Much" Factor: Realistic Expectations for Credit Improvement

So, after all this, how much can a car loan actually improve your credit? The answer isn’t a fixed number, but rather a range that depends heavily on your starting point and consistent behavior.

For someone with very limited or no credit history, a car loan can have a dramatic impact. Establishing your first significant credit account and consistently making on-time payments can quickly build a foundation, potentially leading to score increases of 50 points or more over the first 12-24 months. In these cases, the car loan acts as a powerful first step in demonstrating creditworthiness.

If you have a fair credit score (e.g., in the 600s) and a history of some minor missteps, a car loan can also provide a substantial boost. By consistently making payments, you’re actively demonstrating a change in financial behavior. You might see your score climb 20-40 points or more as the positive payment history starts to outweigh older, negative information. The key here is consistency and time.

For individuals with already good or excellent credit (e.g., 700s and above), the impact might be less dramatic in terms of raw points. However, a car loan can still contribute by diversifying your credit mix and further solidifying your positive payment history. It reinforces your excellent standing rather than providing a massive jump. You might see a more modest increase, perhaps 5-15 points, but it contributes to maintaining and solidifying an already strong credit profile.

It’s crucial to understand that credit improvement is not an overnight miracle. It’s a gradual process. The most significant gains come from months and years of consistent, on-time payments. The longer you responsibly manage the loan, the more positive data accumulates on your credit report, leading to sustained improvement.

Beyond the Car Loan: A Holistic Approach to Credit Health

While a car loan can be a fantastic tool for credit improvement, it’s essential to remember that it’s just one component of a larger financial strategy. True credit health comes from a holistic approach to managing all your financial obligations.

Continue to use credit cards responsibly, keeping balances low (ideally under 30% of your credit limit, or even lower). If you have student loans or a mortgage, ensure those payments are always made on time. Regularly review your credit reports and scores to stay on top of your financial standing. Consider utilizing resources like the Consumer Financial Protection Bureau (CFPB) for guidance on credit management.

Developing strong financial literacy and disciplined habits will serve you far beyond the life of your car loan. It will pave the way for future financial goals, from homeownership to retirement.

Conclusion: Driving Towards a Stronger Credit Future

In summary, a car loan absolutely can improve your credit score, often significantly, but its impact is directly proportional to your responsibility as a borrower. By consistently making on-time payments, you build a positive payment history, diversify your credit mix, and lengthen your credit history – all critical factors that contribute to a higher credit score.

The "how much" factor is fluid, ranging from a modest boost for those with already excellent credit to a substantial jump of 50 points or more for individuals starting with thin or fair credit files. However, the potential for damage is equally real if payments are missed or the loan is mismanaged.

Approach your car loan with a clear strategy: secure a manageable loan, prioritize timely payments, and monitor your credit diligently. When handled wisely, a car loan isn’t just a means to get from point A to point B; it’s a powerful vehicle for driving your credit score towards a stronger, more secure financial future. Start building that positive credit history today!