The Smart Way to Finance Your Next Ride: Navigating LendingTree Used Car Loans

The Smart Way to Finance Your Next Ride: Navigating LendingTree Used Car Loans Carloan.Guidemechanic.com

Purchasing a used car can be a brilliant financial move, offering significant savings and excellent value. However, the path to owning that perfect pre-owned vehicle often involves securing the right financing. This is where the world of auto loans comes in, and navigating it can feel like a complex maze. Fortunately, platforms like LendingTree have emerged as powerful tools, simplifying the search for the best LendingTree used car loan to fit your needs.

In this comprehensive guide, we’ll dive deep into everything you need to know about financing a used car through LendingTree. We’ll explore how this innovative marketplace works, what makes it a preferred choice for many, and crucially, how you can leverage its features to secure a loan that saves you money and stress. Our goal is to equip you with the knowledge to make informed decisions, ensuring your used car purchase is not just affordable, but smart.

The Smart Way to Finance Your Next Ride: Navigating LendingTree Used Car Loans

Why Choose a Used Car and How LendingTree Fits In

The allure of a brand-new car is undeniable, but the financial wisdom often points towards a used vehicle. New cars depreciate rapidly, losing a significant portion of their value the moment they’re driven off the lot. A used car, on the other hand, allows you to sidestep this initial depreciation hit, getting more car for your money. You can often afford a higher trim level or a more luxurious model that would be out of reach if bought new.

However, finding the right financing for a used car can sometimes be more challenging than for a new one. Lenders may view older vehicles as higher risk, potentially leading to higher interest rates or stricter terms. This is precisely where a platform like LendingTree shines, acting as a crucial intermediary in the auto loan marketplace.

LendingTree used car loan services are designed to demystify this process. Instead of you individually contacting multiple banks and credit unions, LendingTree does the legwork, connecting you with a network of lenders eager to offer you a loan. This competition among lenders is a huge advantage for you, the borrower, often leading to better rates and more favorable terms. It transforms a potentially arduous search into a streamlined, comparative shopping experience.

Unlocking Opportunities: How LendingTree Works for Used Car Financing

LendingTree operates as an online loan marketplace, not a direct lender itself. Think of it as a central hub where various financial institutions, from large national banks to smaller local credit unions, gather to offer their loan products. This model is particularly beneficial when you’re seeking a LendingTree used car loan, as it maximizes your chances of finding a competitive offer without the hassle of multiple applications.

When you submit a single loan request through LendingTree, your basic financial information is shared with multiple potential lenders within their network. These lenders then review your profile and, if they see a fit, will extend pre-qualified loan offers. This process is often completed within minutes, providing you with a snapshot of your financing options almost instantly.

The core advantage here is the power of comparison. Each offer you receive will detail the Annual Percentage Rate (APR), loan term, estimated monthly payment, and any associated fees. This transparency allows you to compare apples to apples, making an educated decision based on the numbers. It saves you countless hours of research and individual applications, all while potentially improving your chances of securing a lower interest rate. This marketplace approach fosters competition, which ultimately benefits you, the consumer, by driving down borrowing costs.

Your Step-by-Step Journey: The LendingTree Used Car Loan Application Process

Securing a LendingTree used car loan is designed to be straightforward, but understanding each step can significantly enhance your experience and outcomes. Based on my experience, a little preparation goes a long way.

Step 1: Gathering Your Information

Before you even visit the LendingTree website, it’s wise to have certain information at your fingertips. This includes personal details like your address, phone number, and Social Security number. You’ll also need financial specifics, such as your annual income, employment history, and any existing debts (mortgage, student loans, credit cards). Having these ready ensures a smooth and quick application.

It’s also beneficial to have an idea of your credit score. While LendingTree doesn’t require you to input it, knowing your score beforehand can help you set realistic expectations for the types of rates you might receive. Pro tips from us: check your credit report for any errors well in advance; disputes can take time to resolve.

Step 2: Completing the Online Form

Navigate to LendingTree’s auto loan section. You’ll be prompted to fill out a secure online form. This form asks for the information you gathered in Step 1, along with details about the car you intend to purchase (if known). Even if you haven’t picked out a specific vehicle yet, you can often apply for a general used car loan or pre-approval, which gives you a budget to shop with.

The form is user-friendly and typically takes only a few minutes to complete. Remember, accuracy is key here. Any discrepancies could delay your application or lead to less favorable offers.

Step 3: Receiving Multiple Offers

Once you submit your information, LendingTree’s system will quickly match you with lenders who are likely to approve your loan based on your profile. Within minutes, you’ll start seeing pre-qualified offers directly on your LendingTree dashboard or via email. This part of the process usually involves a "soft inquiry" on your credit, which does not impact your credit score.

Each offer will typically include the lender’s name, the proposed APR, the loan term (e.g., 36, 48, 60 months), and an estimated monthly payment. You might receive several offers, giving you a diverse range of options to consider.

Step 4: Comparing and Choosing the Best Loan

This is perhaps the most critical step. Don’t just jump at the first offer! Carefully compare each LendingTree used car loan offer you receive. Look beyond just the monthly payment. The APR is crucial as it represents the true annual cost of your loan, including interest and fees. A lower APR means you’ll pay less over the life of the loan.

Consider the loan term as well. A longer term might mean lower monthly payments, but it also means you’ll pay more in total interest over time. A shorter term, while having higher monthly payments, can save you a significant amount in interest. Look for any origination fees or prepayment penalties. Once you’ve identified an offer (or a few) that looks promising, you can proceed directly with that lender to complete their full application process, which typically involves a "hard inquiry" on your credit.

What Lenders Really Look For: Key Factors in Used Car Loan Approval

When you apply for a LendingTree used car loan, lenders evaluate several factors to determine your creditworthiness and the terms they’re willing to offer. Understanding these elements can help you prepare and improve your chances of securing the best possible rates.

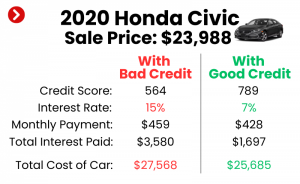

Credit Score: The Biggest Factor

Your credit score is arguably the most influential factor. It’s a numerical representation of your credit risk, reflecting your payment history, outstanding debts, length of credit history, and types of credit used. A higher credit score (generally above 670 for good credit) indicates to lenders that you are a responsible borrower, making you eligible for lower interest rates and more favorable terms. Conversely, a lower score might lead to higher rates or a requirement for a larger down payment. For more insights into managing your credit, check out our guide on . (Placeholder Internal Link 1)

Income and Debt-to-Income Ratio (DTI)

Lenders need to be confident that you can comfortably afford your monthly loan payments. They will assess your income to ensure it’s stable and sufficient. Your Debt-to-Income (DTI) ratio is also critical. This ratio compares your total monthly debt payments (including the proposed car loan) to your gross monthly income. A lower DTI (typically below 36-43%) signals to lenders that you have enough disposable income to handle new debt, making you a less risky borrower.

Vehicle Information

Unlike new car loans, the specifics of the used car you intend to buy play a more significant role. Lenders consider the car’s age, mileage, make, model, and its overall condition. Older vehicles or those with very high mileage might be viewed as higher risk because they are more prone to mechanical issues, which could affect your ability to repay the loan if unexpected repair costs arise. Lenders often use resources like Kelley Blue Book (KBB) or NADAguides to determine the car’s market value and ensure the loan amount doesn’t exceed its worth.

Down Payment

Making a substantial down payment can significantly improve your loan terms. A larger down payment reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest paid over the life of the loan. From a lender’s perspective, a significant down payment also demonstrates your commitment to the purchase and reduces their risk, as you have more equity in the vehicle from the start. Based on my experience, aiming for at least 10-20% down on a used car is a strong strategy.

Mastering the Process: Pro Tips for the Best LendingTree Used Car Loan

Securing the most advantageous LendingTree used car loan requires more than just filling out a form. These pro tips, based on years of helping individuals navigate financing, can put you in a prime position.

Boost Your Credit Score

This is foundational. Before you even think about applying for a loan, take steps to improve your credit score. Pay down existing debts, especially high-interest credit cards. Make all your payments on time. Avoid opening new credit accounts right before applying for a car loan. Even a small increase in your score can translate into significantly lower interest rates and thousands of dollars saved over the life of your loan.

Save for a Down Payment

As mentioned, a larger down payment is your best friend. It not only reduces your loan amount but also makes you a more attractive borrower to lenders. Aim for at least 10-20% of the car’s purchase price. This will give you more equity from the start, potentially allowing you to secure a lower APR and reduce the risk of becoming "upside down" on your loan (owing more than the car is worth).

Know Your Budget

Before you start shopping for cars or loans, determine how much you can truly afford each month. Factor in not just the loan payment, but also insurance, fuel, maintenance, and potential repair costs for a used car. Common mistakes to avoid are getting caught up in the excitement of a new vehicle and overextending your budget. Use online calculators to estimate total ownership costs.

Get Pre-Approved

This is a game-changer. Getting pre-approved through LendingTree gives you a solid understanding of how much you can borrow and at what interest rate before you step onto a dealership lot. This transforms you into a cash buyer, giving you significant leverage in negotiations with sellers. You can focus on negotiating the car’s price, knowing your financing is already secured.

Negotiate Wisely (Car Price, Not Just Loan)

Remember, your loan terms are tied to the car’s price. A lower purchase price means a lower loan amount, which can translate to lower monthly payments and less interest. Don’t be afraid to negotiate the price of the used car itself. Use market research tools like Kelley Blue Book to understand its fair value. With a pre-approval in hand, you can confidently walk away from deals that aren’t right for you.

Read the Fine Print

Once you’ve chosen an offer from a LendingTree partner, meticulously read the full loan agreement before signing. Understand all terms, conditions, fees, and clauses. Are there any prepayment penalties? What are the exact fees associated with the loan? To understand the nuances of different loan types, read our comprehensive article on . (Placeholder Internal Link 2) Don’t hesitate to ask the lender for clarification on anything you don’t understand.

Steering Clear of Pitfalls: Common Mistakes with Used Car Loans

Even with a powerful tool like LendingTree, certain missteps can cost you time and money. Based on my experience, being aware of these common mistakes can help you avoid them.

Not Getting Pre-Approved

As highlighted earlier, skipping pre-approval is a significant error. Without it, you walk into a dealership blind regarding your financing options. Dealers often mark up interest rates to increase their profit, and without a competitive pre-approved offer, you might unknowingly accept a higher rate than you qualify for. This leads to higher monthly payments and a greater total cost for your LendingTree used car loan.

Focusing Only on Monthly Payments

It’s tempting to fixate solely on the lowest possible monthly payment. However, a low monthly payment often comes with a longer loan term, meaning you’ll pay more in total interest over time. Common mistakes to avoid are extending your loan term too much just to reduce the payment. Always consider the total cost of the loan – the principal plus all interest and fees. Sometimes, a slightly higher monthly payment for a shorter term is the more financially sound choice.

Ignoring the Total Cost of the Loan

Beyond the monthly payment, many borrowers overlook the cumulative cost of interest. A difference of just a few percentage points in your APR can translate to thousands of dollars over a 5-year loan term. Always calculate the total amount you will pay back, including all interest. This holistic view helps you truly compare offers and understand the long-term financial impact of your LendingTree used car loan.

Not Checking the Car’s History and Condition

While LendingTree helps with financing, it doesn’t vet the car itself. This is your responsibility. Always get a Vehicle History Report (like Carfax or AutoCheck) to check for accidents, salvage titles, flood damage, and odometer fraud. More importantly, have an independent mechanic inspect the car before purchase. This small investment can save you from buying a lemon and facing expensive repairs down the line, which can severely impact your ability to pay off your loan.

Not Comparing Multiple Offers

The entire premise of LendingTree is to provide you with multiple offers. Common mistakes to avoid are stopping at the first decent offer you receive. Take the time to review all offers, comparing APRs, terms, and fees. Even a slight difference can save you hundreds, if not thousands, over the life of the loan. This due diligence is precisely why you use a marketplace like LendingTree.

Beyond Approval: What to Do After Securing Your Loan

Once your LendingTree used car loan is approved and you’ve chosen your lender, the process shifts to finalizing the purchase and getting your new-to-you vehicle on the road.

Finalizing the Purchase

With your loan pre-approval or approval in hand, you can confidently complete the car purchase. If you’re buying from a dealership, they will handle the paperwork with your chosen lender. If it’s a private sale, your lender will provide instructions on how to transfer funds and secure the title. Ensure all details about the car (VIN, mileage, price) match the loan agreement.

Registration and Insurance

Immediately after purchasing the car, you’ll need to register it with your local Department of Motor Vehicles (DMV) or equivalent agency. This typically involves submitting the title, proof of sale, and often, proof of insurance. Speaking of insurance, this is a non-negotiable step. Lenders require you to carry full coverage insurance (comprehensive and collision) on a financed vehicle to protect their investment. Obtain insurance quotes well in advance, as insurance costs for used cars can vary significantly based on the vehicle, your driving history, and your location. Don’t drive the car off the lot without proper insurance coverage.

Navigating LendingTree Used Car Loans with Less-Than-Perfect Credit

Having a less-than-stellar credit score doesn’t automatically disqualify you from securing a LendingTree used car loan. While it might mean you won’t get the absolute best rates, LendingTree’s vast network of lenders includes those specializing in loans for individuals with various credit profiles.

How LendingTree Can Still Help

LendingTree’s strength lies in its ability to connect you with a wide array of lenders. Some lenders are more willing to work with borrowers who have bad credit, often by offering slightly higher interest rates or requiring a larger down payment. By submitting one application, you still get access to these specialized lenders, saving you the frustration of individual rejections. It increases your chances of finding an offer, even if it’s not the prime rate.

Realistic Expectations

It’s crucial to set realistic expectations if your credit score is low. You will likely face higher interest rates compared to someone with excellent credit. This is how lenders mitigate the increased risk associated with a lower score. Be prepared for potentially higher monthly payments or a requirement for a larger down payment. Focus on finding a loan that is manageable within your budget, even if the APR is higher than you’d hoped.

Tips for Improving Your Chances

If you have bad credit, there are still steps you can take to improve your odds of approval and secure more favorable terms:

- Increase Your Down Payment: This is the most impactful step. A larger down payment reduces the loan amount and the lender’s risk.

- Find a Co-signer: If you have a trusted friend or family member with good credit who is willing to co-sign, it can significantly improve your chances of approval and secure a lower interest rate. Their creditworthiness effectively backs your loan.

- Choose a Less Expensive Car: Opting for a more affordable used car reduces the overall loan amount, making it a less risky proposition for lenders.

- Provide Proof of Stable Income: Lenders want assurance you can pay. Strong proof of stable employment and income can offset some credit concerns.

- Explain Your Situation (If Possible): If there are specific, explainable reasons for past credit issues (e.g., medical emergency), some lenders might be understanding, especially smaller credit unions.

Making the Smart Choice: Final Thoughts on LendingTree Used Car Loans

Financing a used car doesn’t have to be a daunting task. With platforms like LendingTree, you have a powerful ally in your corner, designed to streamline the process and empower you with choices. The ability to compare multiple LendingTree used car loan offers from diverse lenders without impacting your credit score (initially) is an invaluable advantage.

By understanding the application process, knowing what lenders look for, and implementing our pro tips, you can significantly increase your chances of securing the best possible financing for your next pre-owned vehicle. Remember, the ultimate goal is not just to get a loan, but to get the right loan – one that fits your budget, offers competitive terms, and contributes to your financial well-being.

Don’t settle for the first offer you receive or accept dealership financing without exploring your options. Take control of your used car financing journey. Visit LendingTree Auto Loans today to start comparing offers and drive away with confidence, knowing you’ve made a smart financial decision. Your perfect used car, backed by the perfect loan, awaits.