The Ultimate Guide: 10 Steps To Getting A Car Loan Approved With Confidence

The Ultimate Guide: 10 Steps To Getting A Car Loan Approved With Confidence Carloan.Guidemechanic.com

Buying a new car is an exciting milestone, but the journey to getting behind the wheel often involves a critical step: securing a car loan. For many, this process can feel daunting, filled with financial jargon and complex requirements. However, understanding the steps to getting a car loan can transform this anxiety into a confident, informed decision.

This comprehensive guide is designed to demystify auto financing, providing you with an in-depth roadmap to navigate the entire process. From understanding your credit score to signing on the dotted line, we’ll cover everything you need to know to secure a favorable car loan and drive away with peace of mind.

The Ultimate Guide: 10 Steps To Getting A Car Loan Approved With Confidence

Why Understanding Car Loans Matters More Than You Think

A car loan isn’t just a simple agreement; it’s a significant financial commitment that can impact your budget for years. A well-structured loan can save you thousands of dollars in interest, while a hasty decision can lead to financial strain. That’s why being prepared and informed is your best asset.

Based on my experience in personal finance, many people jump into car shopping without fully understanding their borrowing power or the intricacies of loan agreements. This often leads to higher interest rates or less favorable terms. Our goal here is to empower you to avoid those common pitfalls.

Let’s dive into the essential steps to getting a car loan that truly works for you.

Step 1: Understand Your Credit Score and Report

Your credit score is arguably the most crucial factor lenders consider when you apply for an auto loan. It’s a three-digit number that represents your creditworthiness, essentially telling lenders how reliable you are at repaying debts. A higher score typically translates to lower interest rates and better loan terms.

What is Your Credit Score?

Your credit score, primarily FICO and VantageScore, is calculated based on information in your credit report. This report details your borrowing history, including past loans, credit card usage, payment history, and any bankruptcies. Lenders use this score to assess the risk associated with lending you money.

For example, a score above 700 is generally considered "good," while scores above 750 are "excellent," often qualifying you for the most competitive rates. If your score is below 600, you might still get a loan, but expect higher interest rates.

How to Check Your Credit Score and Report

Before even thinking about a car, pull your credit report from all three major bureaus: Experian, Equifax, and TransUnion. You are entitled to a free report from each bureau once every 12 months via AnnualCreditReport.com. Review these reports carefully for any inaccuracies or errors.

Based on my experience, finding and disputing errors on your credit report can significantly boost your score. Even a small improvement can make a difference in your interest rate, potentially saving you hundreds or thousands of dollars over the life of the loan.

Pro tip from us: Don’t just check your score; scrutinize your full report. Identify any late payments, collections, or accounts you don’t recognize. Disputing these can take time, so start this process well in advance of applying for a loan.

Step 2: Assess Your Financial Health and Budget

Understanding what you can realistically afford is paramount. This isn’t just about the monthly payment; it’s about the total cost of car ownership, including insurance, fuel, maintenance, and potential repairs. Rushing into a loan without a clear budget is a common mistake to avoid.

Calculate Your Debt-to-Income (DTI) Ratio

Lenders look at your debt-to-income (DTI) ratio, which is the percentage of your gross monthly income that goes towards debt payments. A lower DTI ratio indicates you have more disposable income to cover new loan payments, making you a less risky borrower. Most lenders prefer a DTI ratio below 36%, though some may go higher.

To calculate your DTI, add up all your monthly debt payments (credit cards, student loans, mortgage, etc.) and divide that sum by your gross monthly income. This gives you a clear picture of your current financial obligations.

Determine Your Affordable Monthly Payment

Create a detailed budget that includes all your income and expenses. Be realistic about what you can comfortably afford each month for a car payment, without straining your other financial commitments. Remember, the goal is financial stability, not just a new car.

Consider using an online car loan calculator to estimate payments based on different loan amounts, interest rates, and terms. This will help you visualize how various scenarios impact your monthly budget.

Step 3: Save Up for a Down Payment

Making a down payment is one of the smartest moves you can make when getting a car loan. It immediately reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan.

Benefits of a Substantial Down Payment

A larger down payment signals to lenders that you are a serious and committed buyer, often leading to better interest rates. It also helps you avoid being "upside down" on your loan, a situation where you owe more than the car is worth, especially common with new cars due to immediate depreciation.

Many financial experts recommend a down payment of at least 10% for a used car and 20% for a new car. This not only lowers your financial burden but also provides a buffer against rapid depreciation.

How Much Should You Aim For?

Even a small down payment is better than none, but strive for as much as you can comfortably save. The more you put down upfront, the less risk you carry and the stronger your position becomes in negotiations. This is a critical step in the steps to getting a car loan that many overlook.

Consider setting up a dedicated savings account for your down payment. Automate transfers from your checking account to build your fund steadily over time.

Step 4: Research Loan Options and Lenders

Don’t just walk into a dealership and accept their first financing offer. Shopping around for a car loan can save you a significant amount of money. There are several types of lenders, and each might offer different rates and terms based on your credit profile.

Explore Your Options

- Banks: Traditional banks are a common source for auto loans. If you have an existing relationship, they might offer competitive rates.

- Credit Unions: Often known for lower interest rates and more flexible terms than traditional banks, credit unions are excellent options, especially if you’re a member.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others specialize in online auto loans, offering quick approvals and competitive rates.

- Dealership Financing: While convenient, dealership financing often involves a markup from the actual lender’s rate. It’s best to have pre-approval from another source before considering their offer.

Pro tips from us: Get at least three different loan offers from various lenders before visiting a dealership. This gives you leverage during negotiations and ensures you’re getting the best possible rate.

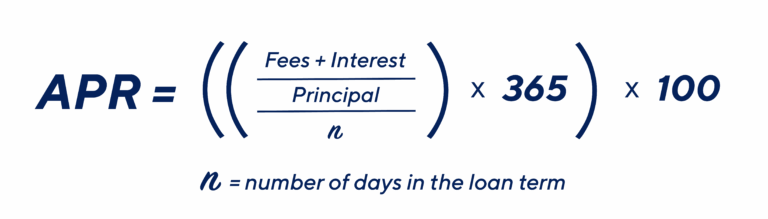

Compare Interest Rates and APR

Don’t just look at the interest rate; focus on the Annual Percentage Rate (APR). The APR includes not only the interest rate but also any additional fees associated with the loan, giving you a more accurate picture of the total cost of borrowing. A lower APR means a cheaper loan.

Step 5: Get Pre-Approved for a Loan

Getting pre-approved for a car loan is perhaps the most powerful step in the entire process. It transforms you from a speculative buyer into a cash buyer, giving you immense confidence and negotiation power at the dealership.

What is Pre-Approval?

Pre-approval means a lender has reviewed your credit and financial information and has conditionally agreed to lend you a specific amount of money at a particular interest rate. This typically involves a "soft" credit inquiry, which doesn’t harm your credit score.

This crucial step gives you a clear understanding of your budget before you even step foot on a car lot. You’ll know exactly how much you can spend, which prevents you from falling in love with a car outside your price range.

Benefits of Pre-Approval

- Set Budget: You know your maximum loan amount, preventing overspending.

- Negotiation Power: You can negotiate the car’s price as if you’re paying cash, separating the car purchase from the financing.

- Faster Process: Speeds up the buying process at the dealership.

- Shop Smart: Focus on cars you can genuinely afford.

Common mistakes to avoid are: skipping pre-approval and letting the dealership control the financing discussion from the start. This often leads to less favorable terms.

Step 6: Shop for Your Car (Smartly)

With pre-approval in hand, you’re ready to find your dream car. However, smart shopping goes beyond just finding a vehicle you like. It involves staying within your budget and being wary of additional costs.

Stick to Your Pre-Approved Budget

Resist the temptation to look at cars that exceed your pre-approved loan amount. Dealerships are skilled at upselling, and it’s easy to get carried away. Remember, your pre-approval is your financial guardian.

Consider both new and used car options. Used cars often offer better value and avoid the steep depreciation hit new cars experience. If you’re looking for tips on choosing between new and used, you might find our article on "Navigating the New vs. Used Car Debate" helpful. (Internal Link Simulation)

Negotiate the Car Price, Not the Monthly Payment

Always negotiate the total purchase price of the vehicle first, before discussing financing or trade-ins. Dealerships often try to focus on the monthly payment, which can obscure the actual price of the car and lead you to pay more over time.

Knowing your pre-approved loan amount empowers you to walk away if the car’s price, after negotiation, doesn’t fit your budget.

Step 7: Gather Required Documents

Once you’ve found the car and negotiated a price, the lender will need to verify your information. Having all your documents ready will streamline the final approval process. This is a straightforward but essential part of the steps to getting a car loan.

Essential Documents You’ll Need

- Proof of Identity: Driver’s license, passport, or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, tax returns (especially if self-employed), or bank statements.

- Proof of Residence: Utility bills (electricity, water), lease agreement, or mortgage statement.

- Proof of Insurance: You’ll need to show proof of auto insurance before driving off the lot. Get quotes beforehand.

- Vehicle Information: The car’s VIN (Vehicle Identification Number), make, model, year, and mileage.

Pro tips from us: Organize these documents in a folder or digital file before you head to the dealership or finalize your online loan application. This preparedness reflects positively on you and speeds up the entire process.

Step 8: Review Loan Offers Carefully

This is where your research from Step 4 pays off. Compare the offers you’ve received from various lenders, including any the dealership might present. Don’t rush this stage; understanding the terms is crucial.

Key Aspects to Compare

- Interest Rate/APR: This is the primary cost of borrowing. Always compare the APR, not just the interest rate.

- Loan Term: The length of time you have to repay the loan (e.g., 36, 48, 60, 72 months). Longer terms mean lower monthly payments but more interest paid over time.

- Monthly Payment: Ensure this fits comfortably within your budget.

- Total Cost of the Loan: Multiply the monthly payment by the loan term, then add your down payment to see the total amount you’ll pay for the car.

- Prepayment Penalties: Check if there are any fees for paying off your loan early. Ideally, avoid loans with these penalties.

Based on my experience, many people get fixated on the lowest monthly payment without considering the total cost. A longer loan term might offer a lower payment, but you’ll pay significantly more in interest over the years.

Step 9: Understand the Fine Print and Close the Deal

Before signing anything, read every line of the loan agreement. If something is unclear, ask questions until you fully understand it. This document is a legally binding contract.

What to Look Out For

- Exact Figures: Ensure the loan amount, interest rate, term, and monthly payment match what was agreed upon.

- Fees: Check for any hidden fees, such as origination fees, documentation fees, or processing fees.

- Optional Add-ons: Dealerships often offer extended warranties, GAP insurance, or other add-ons. Understand what they are, their cost, and if they are truly necessary for you. You can often purchase these separately and sometimes cheaper.

- Early Repayment Penalties: Reconfirm there are no penalties if you decide to pay off the loan ahead of schedule.

Once you’re satisfied with all the terms and have asked all your questions, you’ll sign the loan documents. The dealership will typically handle the title transfer and registration paperwork for you.

Step 10: Post-Approval and Responsible Ownership

Congratulations, you’ve successfully navigated the steps to getting a car loan and driven off with your new vehicle! However, the journey doesn’t end there. Responsible ownership is key to maintaining your financial health and protecting your investment.

Make Timely Payments

Your payment history is a major factor in your credit score. Make every payment on time, every month. Consider setting up automatic payments from your bank account to avoid missing deadlines. This consistency will improve your credit score over time, which can be beneficial for future loans.

Consider Refinancing

If your credit score improves significantly after a year or two, or if interest rates drop, you might be able to refinance your car loan for a lower interest rate. This can reduce your monthly payments or the total interest paid. Our guide on "When to Refinance Your Auto Loan" offers more insights into this process. (Internal Link Simulation)

Protect Your Investment

Keep up with regular maintenance, secure adequate insurance, and drive safely. A well-maintained car retains its value better, and proper insurance protects you financially in case of an accident or theft.

For more detailed information on managing your auto loan, you can consult reputable sources like the Consumer Financial Protection Bureau (CFPB) for unbiased advice on financial products. (External Link Simulation: https://www.consumerfinance.gov/consumer-tools/auto-loans/)

Common Mistakes to Avoid When Getting a Car Loan

Based on my extensive experience, here are some critical errors people often make:

- Not Checking Your Credit First: Going in blind puts you at a disadvantage.

- Skipping Pre-Approval: You lose significant negotiation power at the dealership.

- Focusing Only on Monthly Payments: This can lead to longer loan terms and higher overall costs.

- Ignoring the APR: The interest rate alone doesn’t tell the whole story; the APR does.

- Not Shopping Around for Loans: Accepting the first offer is rarely the best offer.

- Buying Too Much Car: Overextending your budget can lead to financial stress.

- Not Reading the Fine Print: You must understand every term before signing.

- Adding Unnecessary Extras: Dealership add-ons can significantly inflate your loan amount.

Pro Tips from Us for a Smooth Car Loan Journey

- Improve Your Credit Score: Before applying, take steps to pay down debt, make on-time payments, and keep credit utilization low.

- Save Aggressively for a Down Payment: The more you put down, the better your terms and the less you’ll pay in interest.

- Have an Emergency Fund: Ensure you have savings to cover unexpected car repairs or other financial emergencies.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right or you’re pressured, don’t hesitate to leave and find a better option. Your financial well-being is more important than a car.

- Understand Your Trade-In Value Separately: Negotiate your trade-in as a distinct transaction from the car purchase and loan.

Conclusion: Drive Away with Confidence

Getting a car loan doesn’t have to be a stressful ordeal. By following these 10 comprehensive steps to getting a car loan, you’ll approach the process with knowledge, preparation, and confidence. Understanding your credit, budgeting wisely, shopping for the best loan, and carefully reviewing all offers will empower you to make an informed decision that aligns with your financial goals.

Remember, your ultimate goal is not just to get a car, but to secure a car loan that fits comfortably into your budget and helps you build a positive financial future. With this guide, you’re well-equipped to do just that. Happy driving!