The Ultimate Guide: Finding the Best Place For Your Car Loan

The Ultimate Guide: Finding the Best Place For Your Car Loan Carloan.Guidemechanic.com

Purchasing a car is an exciting milestone, whether it’s your very first set of wheels or an upgrade to your dream vehicle. However, the excitement can quickly turn into anxiety when faced with the complexities of financing. Securing the best place for a car loan isn’t just about finding the lowest monthly payment; it’s about understanding the entire process, securing favorable terms, and ultimately saving thousands of dollars over the life of your loan.

Based on my extensive experience in the financial and automotive sectors, navigating the car loan landscape can feel like a maze. There are countless options, each with its own advantages and pitfalls. This comprehensive guide is designed to empower you with the knowledge and strategies needed to confidently choose the right lender, ensuring you drive away with a great car and an even better deal.

The Ultimate Guide: Finding the Best Place For Your Car Loan

We’ll dive deep into the various types of lenders, critical factors affecting your eligibility and rates, and practical steps to secure the most advantageous auto loan options available. By the end of this article, you’ll be equipped to make an informed decision, securing a car loan that perfectly fits your financial situation.

Understanding Car Loans: The Essential Basics

Before we explore the "where," it’s crucial to understand the "what." A car loan is essentially an agreement where a lender provides you with funds to purchase a vehicle, and you agree to repay that amount, plus interest, over a set period. This agreement is formalized through a loan contract.

The primary goal is to find financing that offers the most favorable terms for your specific circumstances. This isn’t a one-size-fits-all scenario; what works for one borrower might not be ideal for another. Understanding the core components of a car loan will put you in a stronger negotiating position.

Key Terms You Need to Know

To truly grasp your car loan options, familiarize yourself with these fundamental terms:

- Annual Percentage Rate (APR): This is the true cost of borrowing money, expressed as a yearly percentage. It includes both the interest rate and any additional fees. A lower APR means a cheaper loan overall.

- Loan Term: This refers to the duration over which you will repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer term usually means lower monthly payments but more interest paid over time.

- Principal: This is the initial amount of money you borrow to purchase the car, excluding interest. As you make payments, the principal amount decreases.

- Interest: This is the cost you pay to the lender for borrowing the principal amount. It’s usually calculated as a percentage of the outstanding principal balance.

- Down Payment: This is the upfront cash amount you pay towards the purchase of the car. A larger down payment reduces the amount you need to borrow, often leading to better car loan rates and lower monthly payments.

Pro tips from us: Always focus on the total cost of the loan, not just the monthly payment. A longer term might seem appealing due to lower payments, but it almost always means paying significantly more in interest over the life of the loan.

Factors That Influence Your Car Loan Approval and Rates

Lenders assess several critical factors when evaluating your car loan application process. Understanding these elements allows you to optimize your financial standing before even applying, dramatically improving your chances of approval and securing the best car loan rates.

1. Your Credit Score: The Ultimate Indicator

Your credit score is arguably the most significant factor lenders consider. It’s a three-digit number that represents your creditworthiness, essentially a snapshot of your financial responsibility. A higher credit score signals lower risk to lenders.

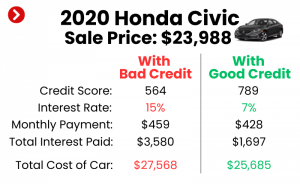

- Impact on Rates: Borrowers with excellent credit scores (generally 720+) qualify for the lowest car loan rates. Those with good credit (660-719) will still get competitive rates, while fair (620-659) or poor credit (<620) will likely face higher interest rates to offset the increased risk perceived by lenders.

- How to Improve It: Before applying, check your credit report for errors. You can also improve your score by paying bills on time, reducing existing debt, and avoiding new credit applications. Based on my experience, even a small improvement in your credit score can make a noticeable difference in your APR.

2. Down Payment: Your Financial Commitment

A substantial down payment demonstrates your financial commitment and reduces the amount you need to borrow. This directly impacts the loan-to-value (LTV) ratio, which lenders closely scrutinize.

- Benefits: A larger down payment can lead to lower interest rates, smaller monthly payments, and a reduced risk of becoming "upside down" on your loan (owing more than the car is worth). Aim for at least 10-20% of the car’s purchase price, if possible.

- Common Mistakes to Avoid: Not saving up for a down payment. While zero-down loans exist, they often come with higher interest rates and put you at greater financial risk.

3. Debt-to-Income (DTI) Ratio: Can You Afford It?

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your ability to manage additional debt.

- Lender’s Perspective: A lower DTI ratio indicates that you have more disposable income to cover your loan payments, making you a less risky borrower. Most lenders prefer a DTI ratio below 43%, though some may accept slightly higher for car loans.

- Improving Your DTI: Reducing existing debt (credit cards, personal loans) or increasing your income can lower your DTI, making you a more attractive candidate for a car loan.

4. Loan Term: Balancing Payments and Total Cost

The loan term directly affects your monthly payment and the total interest you’ll pay. It’s a delicate balance.

- Shorter Terms (e.g., 36-48 months): Higher monthly payments but significantly less interest paid over the life of the loan. You own the car outright faster.

- Longer Terms (e.g., 60-84 months): Lower monthly payments, making the car seem more affordable. However, you’ll pay substantially more in interest, and you risk owing more than the car is worth as it depreciates.

Pro tips from us: While lower monthly payments are tempting, always consider the total cost. Aim for the shortest loan term you can comfortably afford without straining your budget.

5. Vehicle Type and Age: Lender Risk Assessment

The type of vehicle you’re buying also plays a role. Lenders assess the car’s value and depreciation rate.

- New Cars: Generally qualify for lower car loan rates because they hold their value better initially and are seen as less risky collateral.

- Used Cars: Rates might be slightly higher due to greater depreciation and potential mechanical issues. The older the car, the higher the risk for the lender, potentially leading to higher rates or shorter maximum loan terms.

The Contenders: Where to Find Your Best Car Loan

Now that you understand the mechanics, let’s explore the various institutions where you can secure your auto loan. Each type of lender offers unique advantages and disadvantages, and the best place for a car loan often depends on your individual financial profile and preferences.

1. Dealership Financing: Convenience at a Cost?

Dealerships are often the first place people think of when seeking a car loan. They act as intermediaries, connecting you with various lenders they partner with.

- Pros:

- Convenience: It’s a one-stop shop. You can pick your car and arrange financing all in the same place, often on the same day.

- Special Offers: Dealerships frequently offer promotional rates, such as 0% APR or low-interest financing, especially on new vehicles from their brand. These are typically reserved for buyers with excellent credit.

- Flexibility: They might have more flexibility to work with different credit types by accessing a network of lenders.

- Cons:

- Limited Options: While they work with multiple lenders, it’s still a curated selection. You might not see the absolute best rates available in the broader market.

- Potential for Higher Rates: Without pre-approval from an outside source, you lack leverage. Dealerships might mark up the interest rate offered by their lending partners to earn a profit.

- Pressure Tactics: The sales environment can be high-pressure, potentially leading you to rush into a decision without fully comparing offers.

Based on my experience, always arrive at the dealership with a pre-approved loan in hand. This gives you a benchmark and significant negotiating power, ensuring you get the most competitive dealership financing.

2. Banks (Traditional Lenders): Stability and Competitive Rates

Your local or national bank is a traditional and reliable source for car loans. They are well-established institutions with clear lending criteria.

- Pros:

- Established Trust: Many people prefer to work with a bank they already have a relationship with.

- Competitive Rates: For borrowers with good to excellent credit, banks often offer very competitive car loan rates.

- Variety of Products: They can bundle your auto loan with other financial products, sometimes offering relationship discounts.

- In-Person Support: You can often speak directly with a loan officer for personalized guidance.

- Cons:

- Stricter Criteria: Banks tend to have more stringent credit requirements compared to some other lenders.

- Slower Approval Process: While many offer online applications, the full approval and funding process can sometimes take longer than with online-only lenders.

- Limited Flexibility for Bad Credit: If you have poor credit, banks might be less willing to lend or will offer much higher rates.

Pro tips from us: Always check with your existing bank first. They might offer special rates or a streamlined application process for their current customers.

3. Credit Unions: Member-Focused Advantages

Credit unions are non-profit financial cooperatives owned by their members. Their primary goal is to serve their members, often translating into more favorable loan terms.

- Pros:

- Lower Interest Rates: Credit unions are renowned for offering some of the lowest car loan rates in the market because they return profits to members in the form of better rates and fewer fees.

- Personalized Service: As member-owned institutions, they often provide a more personal and flexible lending experience.

- Flexible Terms: They might be more willing to work with borrowers who have less-than-perfect credit or unique financial situations.

- Membership Benefits: You might gain access to other financial services and benefits by becoming a member.

- Cons:

- Membership Requirements: You usually need to meet specific criteria to join a credit union (e.g., live in a certain area, work for a particular employer, or join an affiliated organization).

- Limited Branch Network: Compared to large banks, credit unions may have fewer physical branches, though many offer robust online services.

A common mistake to avoid is overlooking credit unions because you think you won’t qualify for membership. Many have surprisingly broad membership criteria, and a quick search could reveal a fantastic auto loan option.

4. Online Lenders: Speed, Convenience, and Wide Selection

The digital age has brought a surge of online-only lenders specializing in auto loans. These platforms leverage technology to streamline the application and approval process.

- Pros:

- Speed and Convenience: You can apply and often get pre-approved in minutes, all from the comfort of your home.

- Wide Comparison: Many online platforms act as marketplaces, allowing you to compare offers from multiple lenders simultaneously, often leading to very competitive car loan rates.

- Diverse Options: They cater to a broad spectrum of credit profiles, from excellent to bad credit car loan seekers.

- Transparency: Many online lenders pride themselves on clear, upfront terms and conditions.

- Cons:

- Less Personal Interaction: If you prefer face-to-face assistance, online lenders might not be ideal.

- Potential Overwhelm: The sheer number of options can sometimes be daunting without proper guidance.

- Vetting is Key: While many are reputable, it’s crucial to research and choose established online lenders.

Based on my experience, online lenders are excellent for quickly comparing a wide range of car loan options. Just ensure you’re using secure platforms and reading reviews before submitting personal information.

5. Peer-to-Peer (P2P) Lending Platforms: An Alternative Niche

While less common for direct car loans, P2P platforms like LendingClub or Prosper offer personal loans that can sometimes be used for car purchases.

- Pros:

- Alternative for Unique Situations: Can be an option for those who don’t fit traditional lending criteria.

- Potentially Competitive Rates: For borrowers with good credit, rates can be competitive.

- Cons:

- Not Directly Auto Loans: These are typically unsecured personal loans, meaning the car isn’t collateral. This can lead to higher interest rates than secured auto loans.

- Limited Availability: Not all platforms are suitable for large auto purchases.

- Higher Risk: Less regulation than traditional banks.

The Car Loan Application Process: A Step-by-Step Guide

Regardless of where you decide is the best place for your car loan, the general application process follows a similar path. Being prepared and proactive can significantly smooth the journey.

Step 1: Check Your Credit Score and Report

This is your starting point. Obtain a free copy of your credit report from AnnualCreditReport.com and review it thoroughly for inaccuracies. Your credit score will give you a realistic idea of the car loan rates you can expect.

Step 2: Determine Your Budget

Beyond the purchase price, factor in insurance, registration, maintenance, and fuel costs. Use an online car loan calculator to estimate different monthly payments based on various loan amounts, terms, and interest rates. This helps you understand what you can truly afford.

Step 3: Get Pre-Approved (Crucial Step!)

This is perhaps the single most powerful step you can take. Apply for pre-approval from 2-3 different lenders (banks, credit unions, online lenders). Pre-approval involves a soft credit pull (which doesn’t affect your score) and gives you a conditional offer for a specific loan amount and interest rate.

- Why it’s Crucial: A pre-approval letter arms you with an actual offer to take to the dealership. It transforms you from a mere shopper into a cash buyer, giving you immense negotiating power on the car’s price, separate from the financing.

Step 4: Compare Loan Offers

Once you have multiple pre-approvals, compare them meticulously. Look beyond just the monthly payment. Focus on:

- APR: The true cost of the loan.

- Total Loan Cost: How much you’ll pay over the entire term.

- Loan Term: Does it align with your financial goals?

- Fees: Are there any origination fees, prepayment penalties, or other hidden costs?

Step 5: Negotiate at the Dealership (If Applicable)

If you’re buying from a dealership, present your best pre-approved offer. See if the dealership can beat it. Often, they will try to match or even slightly improve your external offer to keep your business. This is where your pre-approval becomes a powerful bargaining chip.

Step 6: Finalize Your Loan

Once you’ve chosen the best offer, complete the final application. This will involve a hard credit inquiry, which might slightly ding your credit score temporarily. Sign all necessary documents and drive away in your new car!

Special Situations & Considerations

Not all car loan journeys are straightforward. Here are some specific scenarios and how to approach them.

Bad Credit Car Loans

If you have a lower credit score, don’t despair. Securing a bad credit car loan is possible, though it will likely come with higher interest rates.

- Strategies:

- Larger Down Payment: This significantly reduces the lender’s risk.

- Co-signer: A creditworthy co-signer can help you qualify for better rates.

- Subprime Lenders: Some lenders specialize in loans for individuals with poor credit. Research them carefully.

- Shorter Loan Term: While monthly payments will be higher, it can reduce total interest paid.

- Improve Credit First: If possible, take a few months to improve your credit score before applying.

Refinancing Your Car Loan

Have you already secured a car loan, but your financial situation has improved, or you found a better rate? Refinancing your car loan could save you a substantial amount.

- When to Refinance:

- Your credit score has improved significantly since you took out the original loan.

- Interest rates have dropped.

- You found a better offer from another lender.

- You want to lower your monthly payment (by extending the term, but beware of increased total interest).

- You want to shorten your loan term (to save on interest).

Pro tips from us: Refinancing is a great way to re-evaluate your loan terms. Many of the same lenders (banks, credit unions, online lenders) offer competitive refinancing options.

Co-Signers: A Helping Hand

A co-signer is someone who agrees to be equally responsible for the loan if you fail to make payments.

- Benefits: Can help you get approved for a loan or secure a better interest rate, especially if you have limited credit history or a low credit score.

- Considerations: It’s a significant responsibility for the co-signer, as their credit will be affected if you default.

Leasing vs. Buying: A Brief Comparison

While this article focuses on loans, it’s worth a brief mention of leasing.

- Buying: You own the car, build equity, and have no mileage restrictions. Ideal for long-term ownership.

- Leasing: You essentially rent the car for a set period, with lower monthly payments but no ownership. Ideal for those who want a new car every few years and drive predictable mileage.

Pro Tips for Securing the Absolute Best Car Loan

Leveraging years of industry insight, here are some actionable strategies to ensure you get the most advantageous auto loan options:

- Get Multiple Pre-Approvals: We can’t stress this enough. Comparing offers from at least three different lenders is non-negotiable for finding the best car loan rates. This also gives you powerful negotiation leverage at the dealership.

- Read the Fine Print: Before signing anything, thoroughly review the loan agreement. Understand all fees, the total interest, and any clauses regarding prepayment penalties or late payment charges. Don’t be afraid to ask questions.

- Don’t Focus Solely on the Monthly Payment: While important, a low monthly payment can hide a very long loan term and a much higher total cost. Always consider the APR and the total amount you’ll pay over the life of the loan.

- Negotiate Everything: Negotiate the car’s price first, separate from the financing. Then, use your pre-approved loan offers to negotiate the financing. Everything is potentially negotiable.

- Improve Your Credit Before Applying: If time allows, even a few months of diligent credit building can significantly impact your car loan rates. Pay down credit card balances and ensure all bills are paid on time.

Common Mistakes to Avoid When Getting a Car Loan

Based on my experience, many people make avoidable errors that cost them money and create unnecessary stress. Be aware of these pitfalls:

- Not Checking Your Credit Score: Going into the process blind leaves you vulnerable to whatever rate the lender offers. Know your standing!

- Only Applying at the Dealership: This is perhaps the biggest mistake. Relying solely on dealership financing means you miss out on potentially better rates from banks, credit unions, and online lenders.

- Ignoring the Total Cost of the Loan: As mentioned, don’t get fixated on the monthly payment. A longer term means more interest. Calculate the total interest paid over the life of the loan.

- Extending the Loan Term Too Much: While a 72- or 84-month loan might offer low monthly payments, you risk being "upside down" on your loan, and the depreciation of the car will outpace your payments.

- Falling for Unnecessary Add-ons: Dealerships often push extended warranties, GAP insurance (sometimes necessary, but compare prices!), and other extras. Research these thoroughly and only buy what you genuinely need.

- Lying on Your Application: Never provide false information. It can lead to loan denial, legal issues, or even fraud charges.

Conclusion: Drive Away with Confidence

Finding the best place for a car loan is a crucial step in the car-buying journey. It requires research, preparation, and a willingness to compare multiple offers. By understanding the factors that influence your loan, exploring the various lender types, and following our expert tips, you can navigate the process with confidence and secure financing that works best for your financial future.

Remember, the goal isn’t just to get approved, but to get approved for the most favorable terms possible. Whether you choose a credit union known for its low car loan rates, the convenience of online lenders auto loans, or the familiarity of your local bank, being an informed borrower is your greatest asset.

Don’t rush the process. Take your time, do your homework, and empower yourself with knowledge. This diligence will pay off, allowing you to enjoy your new vehicle without the burden of an unfavorable loan.

Looking for more financial insights? Explore our guide on or learn about . For detailed information on consumer financial protection, visit the Consumer Financial Protection Bureau (External Link).