The Ultimate Guide: How Much Credit Do I Need For A Car Loan? (And How to Get Approved!)

The Ultimate Guide: How Much Credit Do I Need For A Car Loan? (And How to Get Approved!) Carloan.Guidemechanic.com

Dreaming of a new set of wheels? For many, securing a car loan is the first major step towards making that dream a reality. But before you start browsing showrooms, a crucial question often pops into mind: "How much credit do I need for a car loan?"

It’s a fantastic question, and one that deserves a comprehensive answer. Far too often, people dive into the car buying process without understanding the financial landscape, only to be met with disappointment or unfavorable terms. As an expert in personal finance and auto lending, I can tell you this much: your credit score is undeniably a powerful player in this game, but it’s not the only factor.

The Ultimate Guide: How Much Credit Do I Need For A Car Loan? (And How to Get Approved!)

This in-depth guide is designed to be your definitive resource. We’ll demystify credit scores, explore what lenders truly look for, and equip you with the knowledge and strategies to secure the best possible car loan. Whether your credit is pristine or you’re working to improve it, you’ll find actionable advice here. Let’s hit the road!

Understanding the "Magic Number": What Credit Score Do Lenders Prefer?

First things first: there isn’t one single "magic number" that guarantees car loan approval. Instead, lenders use credit scores to assess your creditworthiness – essentially, how risky it is to lend you money. A higher score generally indicates a lower risk, opening doors to better interest rates and more flexible terms.

Based on my experience, most lenders categorize credit scores into ranges, and these ranges directly influence the loan offers you’ll receive.

The Credit Score Spectrum for Auto Loans:

- Excellent Credit (780-850 FICO Score): If you fall into this elite category, congratulations! You’re likely to receive the absolute best interest rates and loan terms available. Lenders see you as a very low risk. You’ll have your pick of financing options and can often negotiate favorable conditions.

- Good Credit (661-780 FICO Score): This is where most financially responsible individuals find themselves. With a good credit score, you’re in a strong position to secure competitive interest rates and favorable loan terms. While not the absolute lowest rates, they will be very attractive.

- Fair Credit (601-660 FICO Score): Don’t despair if your score is in this range. You can still get approved for a car loan, but expect slightly higher interest rates than those with good or excellent credit. Lenders might view you as a moderate risk, so you may need to shop around more.

- Poor Credit (500-600 FICO Score): Getting a car loan with poor credit is certainly possible, but it comes with challenges. You’ll likely face significantly higher interest rates, stricter terms, and may need to provide a larger down payment or a co-signer. Lenders see a higher risk here.

- Very Poor Credit (Below 500 FICO Score): While not impossible, securing a traditional car loan with a score below 500 can be very difficult. You’ll likely encounter subprime lenders, very high interest rates, and possibly require a substantial down payment or a co-signer with excellent credit. This is often a sign that credit repair is needed before applying.

Pro Tip from us: Even if your credit score is just "fair," don’t assume you’re stuck with the first offer. Always shop around and compare rates from different lenders. You might be surprised by the variations.

Demystifying Your Credit Score: What It Is and Why It Matters

Before we go further, let’s ensure we’re all on the same page about what a credit score actually represents. Your credit score is a three-digit number, primarily calculated by models like FICO (Fair Isaac Corporation) and VantageScore. These scores are derived from the information in your credit reports, which detail your borrowing and repayment history.

Lenders use these scores as a quick snapshot of your financial responsibility. For a car loan, it’s a critical tool for them to assess the likelihood of you repaying the debt on time. A higher score signals reliability, making you a more attractive borrower.

Key Factors Influencing Your Credit Score:

Understanding what builds your credit score is essential for improving it. Based on my experience, these are the five pillars that FICO and VantageScore models primarily consider:

- Payment History (Approx. 35% of FICO Score): This is the most significant factor. Paying your bills on time, every time, is paramount. Late payments, collections, bankruptcies, or foreclosures can severely damage your score.

- Why it matters: Lenders want to see a consistent track record of responsible repayment. If you’ve paid other debts on time, it suggests you’ll do the same for a car loan.

- Credit Utilization (Approx. 30% of FICO Score): This refers to the amount of credit you’re using compared to your total available credit. For example, if you have a credit card with a $10,000 limit and you’ve used $3,000, your utilization is 30%.

- Why it matters: Keeping your utilization low (ideally below 30%) signals that you’re not overly reliant on credit. High utilization can suggest financial distress.

- Length of Credit History (Approx. 15% of FICO Score): This factor considers how long your credit accounts have been open and the average age of those accounts. Longer histories with responsible use are generally better.

- Why it matters: A long history provides more data for lenders to assess your long-term financial behavior.

- Credit Mix (Approx. 10% of FICO Score): Having a healthy mix of different types of credit (e.g., credit cards, installment loans like student loans or mortgages) can positively influence your score.

- Why it matters: It demonstrates your ability to manage various forms of credit responsibly.

- New Credit (Approx. 10% of FICO Score): This includes recent credit applications and newly opened accounts. Applying for too much credit in a short period can temporarily lower your score.

- Why it matters: A sudden surge in new credit applications can be a red flag, indicating potential financial instability or an urgent need for funds.

Beyond the Score: Other Factors Lenders Consider for Car Loans

While your credit score is a major player, it’s not the only piece of the puzzle. Lenders look at your overall financial picture to make an informed decision. Ignoring these other factors is a common mistake many applicants make.

Here are other critical elements that influence car loan approval and terms:

- Debt-to-Income Ratio (DTI): This ratio compares your total monthly debt payments to your gross monthly income. For example, if your total monthly debt payments (including the new car loan) are $1,500 and your gross monthly income is $5,000, your DTI is 30%.

- Why it matters: Lenders prefer a lower DTI (often below 36-43%) as it indicates you have enough disposable income to comfortably manage your new car payment alongside existing obligations.

- Down Payment: The amount of money you pay upfront for the car. A larger down payment reduces the amount you need to borrow, thus lowering the lender’s risk.

- Why it matters: A significant down payment can improve your chances of approval, especially with a lower credit score, and can lead to better interest rates. It also means you’ll owe less than the car’s value sooner.

- Loan Term and Vehicle Type: The length of the loan (e.g., 36, 60, 72 months) and the type of vehicle (new vs. used, luxury vs. economy) also play a role. Longer terms often mean lower monthly payments but higher overall interest paid.

- Why it matters: Lenders assess the depreciation of the vehicle and the likelihood of you completing the loan term. A more expensive car or a very long loan term can increase the perceived risk.

- Employment Stability and Income: Lenders want to see a stable employment history and a consistent income source. This reassures them of your ability to make regular payments.

- Why it matters: Proof of steady income (pay stubs, tax returns) directly supports your capacity to repay the loan.

- Co-Signer: If you have a lower credit score or limited credit history, a co-signer with excellent credit can significantly boost your application. The co-signer agrees to be legally responsible for the loan if you default.

- Why it matters: A co-signer adds an extra layer of security for the lender, mitigating their risk.

How to Find Out Your Credit Score (The Smart Way)

You can’t effectively plan without knowing your starting point. Checking your credit score is a crucial first step, and thankfully, it’s easier than ever.

Here are the best ways to get your credit score:

- AnnualCreditReport.com: This is the only federally authorized website for free annual credit reports from the three major bureaus (Experian, Equifax, and TransUnion). While it provides your detailed credit report, some services also offer a free score. Reviewing your reports is vital to check for errors.

- Credit Card Providers: Many credit card companies now offer free access to your FICO or VantageScore as a perk for cardholders. Check your online banking portal or monthly statements.

- Credit Monitoring Services: Websites like Credit Karma (VantageScore), Experian (FICO Score 8), and others offer free credit scores and monitoring. While these are often "educational" scores and may differ slightly from what a lender sees, they provide a very good indication of your credit health.

- Loan Pre-Approval Processes: When you seek pre-approval for a car loan, lenders will often provide you with the credit score they pulled. This is a "soft inquiry" and won’t harm your score if done properly.

Common mistake to avoid: Don’t apply for multiple car loans without knowing your credit score first. Each "hard inquiry" from a lender can temporarily ding your score. Instead, get your score first, then strategize.

Strategies for Getting Approved (Even with Less-Than-Perfect Credit)

What if your credit score isn’t in the "excellent" range? Don’t lose hope! There are several proactive steps you can take to improve your chances of approval and secure better terms.

1. Improve Your Credit Score Before Applying

This is the most impactful long-term strategy. Even a modest bump in your score can translate into thousands of dollars saved on interest over the life of the loan.

- Pay bills on time: Set up reminders or automatic payments. Consistency is key.

- Reduce credit utilization: Pay down credit card balances. Aim for below 30% utilization, but lower is always better.

- Address errors on your credit report: Get copies of your credit reports and dispute any inaccuracies immediately. Errors can drag down your score.

- Avoid opening new credit accounts: Resist the urge to apply for new credit cards or loans in the months leading up to your car loan application.

- Become an authorized user: If a trusted family member has excellent credit, ask them to add you as an authorized user on one of their credit cards (they don’t even have to give you the card). Their good payment history can reflect positively on your report.

– (Placeholder for internal link)

2. Save for a Larger Down Payment

As mentioned, a larger down payment reduces the amount you need to borrow. This directly lowers the lender’s risk and can make them more willing to approve your loan, even with a lower credit score. It also means lower monthly payments for you.

3. Find a Co-Signer

If you have poor credit or limited credit history, a co-signer with excellent credit can significantly strengthen your application. Their good credit effectively "backs up" your loan.

- Important consideration: Your co-signer becomes legally responsible for the loan if you can’t make payments. Choose someone you trust implicitly, and ensure you understand the gravity of this commitment.

4. Explore Pre-Approval

Getting pre-approved from banks or credit unions before you step into a dealership is a game-changer. It gives you a clear idea of how much you can borrow, at what interest rate, and under what terms.

- Benefit: You’ll walk into the dealership with your own financing in hand, putting you in a stronger negotiating position for the car’s price. You’ll know if the dealer’s financing offer is truly better or worse.

5. Shop Around for Lenders

Don’t settle for the first offer you receive, especially if you have fair or poor credit. Different lenders have different criteria and risk appetites.

- Consider:

- Banks: Traditional banks often offer competitive rates for those with good credit.

- Credit Unions: These member-owned institutions often have more flexible lending criteria and can offer excellent rates, even for those with less-than-perfect credit.

- Online Lenders: Many online platforms specialize in auto loans and can offer quick approvals.

- Dealership Financing: While convenient, dealership financing sometimes marks up interest rates. Always compare their offer with your pre-approval.

6. Consider a Less Expensive Vehicle

Sometimes, the best strategy is to adjust your expectations. If your credit isn’t stellar, aiming for a brand-new, expensive car might be unrealistic.

- Benefit: A more affordable used car means a smaller loan amount, which is less risky for lenders. This can increase your chances of approval and result in lower monthly payments, giving you time to build your credit for a future upgrade.

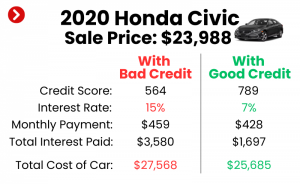

The "Bad Credit" Car Loan Reality: What to Expect

If your credit score is in the fair or poor range, it’s important to have realistic expectations. While getting a loan is possible, the terms will likely be different.

- Higher Interest Rates: This is the most significant consequence. Lenders charge higher interest rates to compensate for the increased risk they’re taking. This means you’ll pay significantly more over the life of the loan.

- Shorter Loan Terms: Lenders might prefer shorter loan terms (e.g., 36-48 months) to minimize their exposure to risk. This means higher monthly payments, but you’ll pay off the car faster.

- Larger Down Payment Requirement: As discussed, a substantial down payment becomes even more crucial with bad credit.

- What to Watch Out For: Be extremely cautious of "buy here, pay here" dealerships or lenders that don’t check credit at all. While they might offer quick approval, their interest rates are often exorbitant, and terms can be predatory. Always read the fine print!

The silver lining? If you manage a car loan responsibly – making all payments on time – it can be an excellent way to rebuild and improve your credit score for future financial endeavors.

Common Mistakes to Avoid When Applying for a Car Loan

Based on my years of observing consumers navigate the auto loan landscape, certain missteps appear repeatedly. Avoiding these can save you stress, time, and money.

- Not Checking Your Credit Report First: This is a cardinal sin. How can you prepare if you don’t know your standing? Always get your credit reports (and scores) before you start. This also allows you to dispute any errors.

- Focusing Only on Monthly Payments: It’s tempting to fixate on the lowest monthly payment. However, a low monthly payment often comes with a longer loan term, meaning you’ll pay significantly more in interest over time. Always consider the total cost of the loan.

- Applying Everywhere (Multiple Hard Inquiries): Each time a lender pulls your credit, it’s recorded as a "hard inquiry." Too many hard inquiries in a short period can temporarily lower your score. Group your loan applications within a 14-45 day window (depending on the scoring model) so they count as a single inquiry.

- Ignoring the Total Cost of the Loan: Beyond the monthly payment, factor in interest, fees, taxes, and insurance. The sticker price is just the beginning. A seemingly low interest rate can still result in a high total cost if the loan term is very long.

- Not Getting Pre-Approved: Walking into a dealership without a pre-approval is like walking into a negotiation blindfolded. You lose significant leverage when you don’t have an outside offer to compare.

Pro Tips for a Smooth Car Loan Journey

Ready to take control of your car loan experience? Here are some invaluable insights from an industry insider:

- Get Pre-Approved from Multiple Lenders: As emphasized, this is your superpower. Compare offers from at least three different sources (your bank, a credit union, an online lender) to find the best rate and terms.

- Negotiate the Car Price FIRST, Then the Financing: Keep these two aspects separate. Negotiate the absolute best price for the vehicle before discussing financing. Once you have a price you’re happy with, then present your pre-approved financing or see if the dealer can beat it.

- Read the Fine Print (All of It!): Do not sign anything you haven’t thoroughly read and understood. Pay attention to interest rates, fees, penalties for late payments, and early payoff clauses. Ask questions until you are completely clear.

- Understand ALL Fees: There can be various fees associated with a car loan (origination fees, documentation fees, etc.). Make sure you know what you’re paying for and if they are negotiable.

- Don’t Let the Dealer "Run Your Credit" Indiscriminately: If you have pre-approval, you don’t need the dealer to run your credit repeatedly. They may do a soft pull to verify, but be wary of multiple hard pulls without a clear reason.

- Consider Gap Insurance: If you’re financing a new car, especially with a low down payment, consider gap insurance. It covers the "gap" between what you owe on the loan and the car’s actual cash value if it’s totaled or stolen.

– (Placeholder for external link)

Conclusion: Preparation is Your Best Friend

Securing a car loan doesn’t have to be a daunting task. The amount of credit you need for a car loan isn’t a fixed figure; it’s a dynamic range influenced by your financial habits, the loan terms, and the lender’s policies.

The ultimate takeaway is this: preparation is your best friend. Understand your credit score, know what lenders are looking for, and take proactive steps to strengthen your financial position. By doing your homework, improving your credit where possible, and shopping smart, you’ll be well-equipped to drive away with a car loan that truly works for you, not against you.

Happy car hunting, and may your journey be smooth and financially sound!

What are your thoughts on car loans and credit scores? Share your experiences and questions in the comments below!