The Ultimate Guide: How To Be Approved For A Car Loan With Confidence (And Get the Best Rates!)

The Ultimate Guide: How To Be Approved For A Car Loan With Confidence (And Get the Best Rates!) Carloan.Guidemechanic.com

Dreaming of a new set of wheels? For many, a car isn’t just a luxury; it’s a necessity, providing freedom and access to work, family, and opportunities. However, the path to owning one often involves securing a car loan, a process that can feel daunting and complex. Understanding how to be approved for a car loan is the first crucial step towards driving off the lot with confidence.

Based on my experience as an expert in personal finance and automotive lending, navigating car loan applications can be straightforward if you’re well-prepared. This comprehensive guide will equip you with all the knowledge, strategies, and pro tips you need to not only get approved but also secure the best possible rates and terms. We’ll dive deep into every aspect, from boosting your credit score to understanding loan agreements, ensuring you’re empowered throughout your car buying journey.

The Ultimate Guide: How To Be Approved For A Car Loan With Confidence (And Get the Best Rates!)

Understanding Car Loans: The Essential Foundation

Before you even start browsing vehicles, it’s vital to grasp the fundamentals of what a car loan entails and what lenders look for. A car loan is essentially an agreement where a financial institution lends you money to purchase a vehicle, and you agree to repay that money, plus interest, over a set period.

Getting approved for a car loan isn’t just about finding a lender willing to give you money. It’s about demonstrating your reliability as a borrower. Lenders assess several key factors to determine their risk, which directly impacts whether you get approved, what interest rate you receive, and the overall terms of your loan. Understanding these elements from the outset will significantly improve your chances of a smooth approval process.

What Lenders Really Look For

When you apply for a car loan, lenders evaluate your financial profile to ensure you can consistently make your monthly payments. They are looking for a clear picture of your financial health and stability.

Here are the primary pillars of their assessment:

- Creditworthiness: This is often the first and most critical factor. Your credit score and credit history tell lenders how responsibly you’ve managed past debts.

- Income Stability: Lenders want to see a consistent and sufficient income stream to cover your potential car payments alongside your other financial obligations.

- Debt-to-Income (DTI) Ratio: This ratio measures how much of your gross monthly income goes towards debt payments. A lower DTI indicates you have more disposable income to take on new debt.

- Down Payment: A significant down payment reduces the amount you need to borrow, lowering the lender’s risk and potentially securing you better terms.

- Vehicle Value: The car itself serves as collateral for the loan. Lenders consider the vehicle’s market value to ensure it adequately covers the loan amount if you default.

Section 1: Building Your Loan-Worthy Profile – The Pre-Application Steps

The secret to a successful car loan approval often lies in the preparation you do before you even fill out an application. By focusing on these foundational elements, you can significantly enhance your appeal to lenders and unlock better financing options.

1. Your Credit Score: The Cornerstone of Car Loan Approval

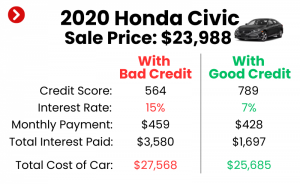

Your credit score is a three-digit number that summarizes your credit risk. For car loans, a higher score signals to lenders that you are a reliable borrower who pays bills on time. This single number can save you thousands of dollars in interest over the life of your loan.

What is a Credit Score and Why Does it Matter?

Credit scores, like FICO and VantageScore, are generated from the information in your credit report. They reflect your payment history, amounts owed, length of credit history, new credit, and credit mix. A strong score indicates a lower risk for lenders, making them more willing to offer you competitive interest rates. Conversely, a low score suggests higher risk, leading to higher rates or even denial.

Pro tip from us: Aim for a FICO score of 660 or higher for "prime" or "near-prime" rates. Scores above 720 generally qualify for the best rates available.

How to Check Your Credit Score and Report

You have a right to a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months. You can access these reports at annualcreditreport.com. Many credit card companies and banks also offer free credit score monitoring services.

Reviewing your report is crucial. It allows you to identify any errors or discrepancies that could be negatively impacting your score. Dispute any inaccuracies immediately, as correcting them can quickly boost your creditworthiness.

Strategies to Improve Your Credit Score

Even if your score isn’t perfect, there are actionable steps you can take to improve it before applying for a car loan. These strategies require discipline but yield significant results.

- Pay All Bills On Time, Every Time: Payment history is the most significant factor in your credit score. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Existing Debt: High credit card balances can hurt your credit utilization ratio (the amount of credit you’re using compared to your total available credit). Pay down revolving debts to below 30% of your credit limit.

- Dispute Errors on Your Credit Report: As mentioned, mistakes happen. Carefully review your report for accounts you don’t recognize or incorrect payment statuses.

- Keep Old Accounts Open: The length of your credit history positively impacts your score. Don’t close old, paid-off credit accounts, even if you don’t use them frequently.

- Avoid New Credit Inquiries: Each time you apply for new credit, a hard inquiry appears on your report, which can temporarily lower your score. Try to avoid opening new lines of credit in the months leading up to your car loan application.

2. Income Stability and Debt-to-Income (DTI) Ratio

Beyond your credit score, lenders want assurance that you have the financial capacity to take on a new monthly payment. This involves looking at your income and how it relates to your existing debt.

What is DTI and Why is it Crucial?

Your Debt-to-Income (DTI) ratio is calculated by dividing your total monthly debt payments by your gross monthly income. For example, if your monthly debt payments (credit cards, student loans, mortgage, etc.) are $1,000 and your gross monthly income is $4,000, your DTI is 25% ($1,000 / $4,000).

Lenders typically prefer a DTI ratio of 36% or less, though some might go higher, especially for car loans. A lower DTI signifies that you have ample income to handle additional debt, making you a less risky borrower.

How to Improve Your DTI

Improving your DTI ratio involves either increasing your income or decreasing your debt. Both are effective.

- Pay Down Existing Debts: Focus on reducing balances on credit cards, personal loans, or other installment debts.

- Avoid Taking on New Debt: Refrain from opening new credit cards or taking out personal loans before applying for your car loan.

- Consider a Side Hustle: If feasible, temporarily increasing your income can also help lower your DTI.

3. The Power of a Down Payment

A down payment is the initial amount of money you pay upfront for a car, reducing the total amount you need to borrow. This simple act carries significant weight with lenders.

Why a Down Payment Helps Your Approval Odds

Putting money down shows lenders that you are financially committed to the purchase and have some skin in the game. It also immediately reduces their risk, as the loan amount is smaller relative to the vehicle’s value. This often translates into better loan terms and a higher chance of approval.

Common mistakes to avoid are: skipping a down payment entirely, especially if your credit isn’t stellar. While 0% down loans exist, they often come with higher interest rates and can lead to negative equity faster.

Recommended Down Payment Percentages

While there’s no strict rule, a general guideline is to aim for at least 10% to 20% of the car’s purchase price for a new car. For a used car, a 10% down payment is often a good target. A larger down payment can lead to:

- Lower Monthly Payments: Less principal to pay off each month.

- Less Interest Paid Over Time: You’re borrowing less money overall.

- Reduced Risk of Negative Equity: You’ll be less likely to owe more than the car is worth, especially in the early years.

4. Budgeting for Success: What Can You Truly Afford?

Before falling in love with a specific car, establish a realistic budget. This isn’t just about the monthly loan payment; it’s about the total cost of ownership.

Calculating Your Affordability

Consider all potential expenses associated with car ownership:

- Monthly Loan Payment: Use online calculators to estimate payments based on different loan amounts, interest rates, and terms.

- Car Insurance: Get quotes for the specific make and model you’re considering. This can vary wildly.

- Fuel Costs: Estimate your average mileage and current gas prices.

- Maintenance and Repairs: Factor in routine servicing, tires, and potential unexpected repairs. Used cars often have higher maintenance costs.

- Registration and Taxes: These are often upfront costs or annual fees.

Based on my experience: Many first-time buyers underestimate these additional costs. A general rule of thumb is that your total car expenses (payment, insurance, fuel, maintenance) should not exceed 15-20% of your net monthly income.

Section 2: Navigating the Application Process – Step-by-Step for Success

Once your financial profile is optimized, you’re ready to tackle the application process. Strategic planning during this phase can save you time, stress, and money.

1. Getting Pre-Approved: Your Secret Weapon

Pre-approval is a game-changer in the car buying process. It means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a particular interest rate, before you’ve even chosen a car.

What is Pre-Approval and Why is it Beneficial?

Pre-approval gives you a clear understanding of your budget and what interest rate you can expect. It empowers you by separating the financing decision from the car selection process.

- Negotiating Power: You walk into the dealership knowing exactly what you can afford and what kind of rate you qualify for. This allows you to negotiate the car’s price more effectively, as you’re not reliant on the dealer’s financing options.

- Clarity on Your Budget: No more guessing games. You know your maximum loan amount and estimated monthly payment.

- Multiple Offers: You can get pre-approved by several lenders (banks, credit unions, online lenders) within a short window (typically 14-45 days) without multiple hits to your credit score. This allows you to compare offers and choose the best one.

Where to Get Pre-Approved

Don’t limit yourself to the dealership. Explore various options:

- Banks: Your current bank might offer competitive rates due to your existing relationship.

- Credit Unions: Often known for offering lower interest rates and more flexible terms to their members.

- Online Lenders: Companies like Capital One Auto Finance, LightStream, and Carvana (for their own inventory) provide quick and convenient online pre-approvals.

Pro tips from us: Always secure pre-approval from at least two or three independent lenders before visiting a dealership. This creates leverage and helps you ensure you’re getting a fair deal.

2. Gathering Your Documents: Be Prepared

A smooth application process requires having all necessary documents readily available. This demonstrates your preparedness and can expedite approval.

Here’s a checklist of common documents you’ll need:

- Proof of Income: Recent pay stubs (last 2-3 months), W-2 forms, tax returns (if self-employed or if requested).

- Proof of Residence: Utility bills (electricity, gas, water) or a lease agreement with your current address.

- Identification: Valid driver’s license or state-issued ID.

- Social Security Number: For credit checks.

- Insurance Information: You’ll need proof of insurance before driving off the lot.

- Trade-in Information (if applicable): Title, registration, and payoff amount for your current vehicle.

3. Choosing the Right Lender for Your Car Loan

While pre-approval helps, the final decision on where to get your loan depends on various factors. Not all lenders are created equal.

Comparing Lender Types

- Traditional Banks: Offer a range of products, potentially good rates for existing customers.

- Credit Unions: Member-owned, often have lower rates and more personalized service. Requires membership.

- Dealership Financing: Convenient, but their rates may not always be the most competitive. They often work with multiple lenders to find you a deal.

- Online Lenders: Fast, convenient, and can offer competitive rates.

When comparing offers, look beyond just the interest rate. Consider the Annual Percentage Rate (APR), which includes the interest rate plus any fees, giving you the true cost of borrowing. Also, compare loan terms (e.g., 36, 48, 60, 72 months) and any prepayment penalties.

4. The Application Itself: Honesty and Accuracy

When you formally apply for the loan, whether online or in person, ensure all information is accurate and truthful. Any discrepancies can delay or even derail your approval.

The lender will perform a hard inquiry on your credit report, which will temporarily ding your score by a few points. However, multiple inquiries for the same type of loan within a short window (e.g., 14-45 days, depending on the scoring model) are typically counted as a single inquiry, so don’t hesitate to shop around for rates.

Section 3: What If You Have Challenged Credit? Strategies for Bad Credit Car Loan Approval

Not everyone has a pristine credit history, and that’s okay. It’s still possible to get approved for a car loan, though the process might require a different approach and understanding.

Understanding Subprime Loans

If your credit score is below 620-660, you might be considered a "subprime" borrower. This doesn’t mean you can’t get a loan, but it typically means:

- Higher Interest Rates: Lenders take on more risk, so they charge more for the loan.

- Stricter Terms: You might be required to make a larger down payment or accept a shorter loan term.

- Fewer Lender Options: Not all lenders cater to subprime borrowers.

Strategies for Bad Credit Car Loan Approval

Even with challenged credit, there are effective ways to improve your chances of approval and secure the best possible terms.

- Larger Down Payment: This is perhaps the most impactful strategy. A substantial down payment reduces the loan amount and signals to lenders your commitment and ability to save, mitigating their risk.

- Find a Co-signer: A co-signer with good credit can significantly boost your approval odds. Their creditworthiness effectively backs your loan, providing an added layer of security for the lender. However, remember that the co-signer is equally responsible for the debt if you default.

- Opt for a Used Car: Used cars are generally less expensive, meaning you’ll need to borrow less money. This reduces the risk for lenders and can make approval easier, especially if you have a limited budget.

- Secured Car Loans: Some lenders offer secured personal loans where you put up collateral (like a savings account) to guarantee the loan. While less common for car purchases directly, it’s an option if other avenues fail.

- Special Finance Dealerships: Many dealerships specialize in working with buyers who have less-than-perfect credit. They have relationships with lenders who are more willing to approve subprime loans. Be cautious and thoroughly review all terms, as these loans often come with higher interest rates.

- Credit Rebuilding Through a Car Loan: If approved, making timely payments on your car loan can be an excellent way to rebuild your credit history. Each on-time payment reported to the credit bureaus will gradually improve your score, paving the way for better financial opportunities in the future.

Common mistakes to avoid are: getting pressured into a deal you don’t understand or can’t afford. With bad credit, some lenders might try to push additional products or excessively long loan terms. Always read the fine print.

Section 4: Finalizing Your Loan and Post-Approval Tips

You’ve done the hard work, secured an approval, and found your dream car. Now it’s time to finalize the paperwork and ensure you understand every aspect of your loan.

1. Reviewing the Loan Agreement: Read Every Word

This is not the time to rush. The loan agreement is a legally binding contract. Scrutinize every detail before you sign.

Pay close attention to:

- Interest Rate vs. APR: Understand the difference. APR (Annual Percentage Rate) is the true cost of your loan, including interest and fees. Focus on the APR for comparison.

- Loan Term: How many months will you be making payments? A longer term means lower monthly payments but more interest paid over time.

- Total Cost of the Loan: This figure shows you the sum of all payments, including principal and interest, over the life of the loan.

- Any Additional Fees: Look for origination fees, documentation fees, or prepayment penalties.

- Prepayment Penalties: Check if there are any charges for paying off your loan early. Ideally, you want a loan without these penalties.

Based on my experience: Many consumers gloss over the fine print, only to discover unexpected fees or terms later. Don’t be afraid to ask questions until you fully understand everything.

2. The Importance of Car Insurance

Before you can drive your new car off the lot, you’ll need to provide proof of insurance. Most lenders require comprehensive and collision coverage, as the car serves as collateral for the loan.

Get insurance quotes early in the process. The type of car you buy, your driving history, and even your location can significantly impact premiums.

3. What to Do If You’re Initially Denied

A denial isn’t the end of the road. It’s an opportunity to understand what went wrong and adjust your strategy.

- Ask Why: Lenders are legally required to provide a reason for denial. This feedback is invaluable.

- Review Your Credit Report Again: Check for new errors or missed issues that might have led to the denial.

- Seek a Co-signer: If the denial was due to insufficient credit history or income, a co-signer might help.

- Reapply with Different Terms: Consider a smaller loan amount, a larger down payment, or a less expensive vehicle.

- Work on Improving Your Credit: If credit score was the primary issue, focus on the strategies mentioned earlier to improve it over time before reapplying.

Conclusion: Drive Off with Confidence

Securing approval for a car loan doesn’t have to be a stressful ordeal. By taking a proactive and informed approach, you can significantly increase your chances of not only getting approved but also securing the most favorable terms and rates available. From meticulously improving your credit score and understanding your financial standing to strategically shopping for pre-approvals and diligently reviewing loan agreements, every step you take contributes to a smoother, more empowering car buying experience.

Remember, preparation is key. Show lenders you are a responsible borrower by demonstrating financial stability, a healthy credit profile, and a clear understanding of your budget. With this comprehensive guide, you are now equipped with the knowledge and pro tips to navigate the car loan landscape with confidence. Don’t just get a car; get the right car loan for you.

What are your experiences with car loan applications? Share your tips and questions in the comments below!