The Ultimate Guide to 0 Percent APR Car Loans: Drive Away with Zero Interest?

The Ultimate Guide to 0 Percent APR Car Loans: Drive Away with Zero Interest? Carloan.Guidemechanic.com

Imagine driving off the lot in a brand-new car, knowing you won’t pay a single cent in interest on your loan. For many car buyers, a 0 percent APR car loan sounds like an absolute dream – a financial golden ticket. It’s an offer that can save you thousands of dollars over the life of your loan, making that new vehicle feel even more attainable.

However, like most incredible deals, a 0% APR car loan often comes with specific conditions and requirements. It’s not a universal offer, and qualifying for it requires a strategic approach and a clear understanding of the fine print. In this super comprehensive guide, we’ll peel back the layers of these enticing offers, helping you understand if a zero-interest car loan is truly within your reach and if it’s the best financial move for you.

The Ultimate Guide to 0 Percent APR Car Loans: Drive Away with Zero Interest?

What Exactly is a 0 Percent APR Car Loan?

At its core, a 0 percent APR (Annual Percentage Rate) car loan means you borrow money to purchase a vehicle, but you pay absolutely no interest on the amount borrowed. Essentially, you’re only paying back the principal amount of the car’s price. This is a significant departure from standard car loans, where interest can add substantial costs to your total purchase.

These types of loans are typically offered by car manufacturers or dealerships as a powerful incentive to boost sales, especially for new models or to clear out previous year’s inventory. They are a marketing tool designed to attract highly qualified buyers. While the concept is straightforward, the execution involves several layers of eligibility and terms that savvy buyers must understand.

The Allure of Zero Interest: Why It’s So Attractive

The appeal of a 0% APR car loan is undeniable. The most significant benefit is the massive savings on interest charges. Over a typical car loan term of 60 or 72 months, even a low-interest rate of 3-5% can amount to thousands of dollars. Eliminating this cost means more money stays in your pocket or can be used for other financial goals.

Furthermore, these loans can lead to faster debt payoff. Since every payment goes directly towards the principal, you’re reducing your outstanding balance more quickly. This sense of accelerated financial freedom is a major draw for many consumers looking to manage their debt efficiently.

Who Qualifies? The Golden Borrower Profile

Based on my experience helping countless clients navigate car financing, qualifying for a 0% APR car loan isn’t for everyone. Lenders and manufacturers reserve these highly competitive rates for borrowers who present the lowest risk. You’ll need to demonstrate an impeccable financial history and strong repayment capability.

Here’s a breakdown of the typical "golden borrower profile" that lenders seek:

1. Excellent Credit Score

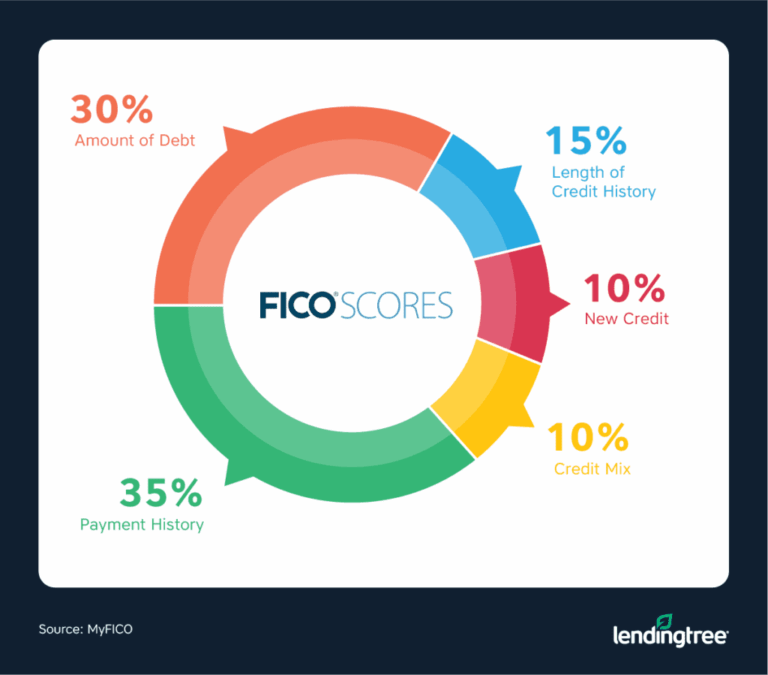

This is arguably the most critical factor. To be considered for a 0% APR offer, you’ll almost certainly need an excellent credit score, generally considered to be in the 750-850 FICO range. Lenders view a high credit score as proof of your reliability in managing debt and making payments on time.

A score in this range indicates a history of responsible borrowing, low credit utilization, and a diverse credit mix. Without this stellar credit, it’s highly unlikely you’ll meet the stringent requirements for zero interest.

2. Strong Income & Low Debt-to-Income Ratio

Lenders want to see that you have a stable and sufficient income to comfortably afford the monthly payments, which can often be higher with 0% APR loans due to shorter terms. They will also scrutinize your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income.

A low DTI (ideally below 36%) signals that you’re not overextended financially. It assures the lender that you have ample disposable income to handle the car payment without strain, even if unexpected expenses arise.

3. Stable Employment History

A consistent employment history demonstrates financial stability and a reliable income stream. Lenders typically look for several years of continuous employment with the same employer or within the same industry. Frequent job changes or gaps in employment can raise red flags, making you appear a higher risk.

They want to see a predictable financial future to ensure consistent loan repayment. This stability is a key indicator of your ability to meet your financial obligations over the loan term.

4. Significant Down Payment (Often Preferred, Sometimes Required)

While not always a strict requirement, making a substantial down payment can significantly improve your chances of approval. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also shows your commitment and financial discipline.

Some 0% APR offers might implicitly favor those with down payments, or the terms might be more favorable if you put more money down. Based on my experience, aiming for at least 10-20% down is a smart strategy, even if not explicitly mandated.

The "Catches" and Hidden Truths: Reading the Fine Print

While the "0 percent" sounds fantastic, it’s crucial to understand that these offers are not simply handouts. There are often trade-offs and specific conditions designed to protect the lender and manufacturer. Common mistakes to avoid are focusing solely on the "zero" and overlooking the crucial details.

Here are the "catches" you absolutely need to be aware of:

1. Shorter Loan Terms

One of the most common trade-offs for 0% APR is a shorter loan term. While traditional car loans might stretch to 72 or even 84 months, 0% APR offers are frequently limited to 36, 48, or 60 months. A shorter term means fewer payments.

This results in significantly higher monthly payments compared to a longer-term loan with interest. While you save on interest, your monthly budget needs to be able to absorb this larger financial commitment.

2. Higher Monthly Payments

Directly related to shorter terms, higher monthly payments are a non-negotiable aspect of most 0% APR deals. Let’s say you’re buying a $30,000 car. Over 60 months at 0% APR, your payment is $500/month. Over 72 months at 4% APR, your payment might be closer to $460/month, but you’d pay over $3,000 in interest.

You need to assess if your budget can comfortably handle these elevated payments. Don’t let the allure of zero interest blind you to the practical reality of your monthly cash flow.

3. Limited Vehicle Selection

0% APR offers are typically tied to specific new car models, trims, or even individual vehicles on the lot. Manufacturers use these incentives to move particular inventory, often slower-selling models, or to boost sales of newly released cars. You might not find a 0% APR deal on the most popular, in-demand models.

This means you might have less flexibility in choosing your preferred color, features, or even the specific model you initially wanted. Be prepared for potentially limited options.

4. Dealership vs. Manufacturer Offers

It’s important to distinguish between manufacturer-backed 0% APR offers and dealership-specific promotions. Manufacturer offers are usually more reliable and transparent. Dealership offers might have more hidden clauses or require additional purchases (like extended warranties) to qualify.

Always confirm if the 0% APR is a factory incentive or a dealer special. Pro tips from us: Manufacturer offers are generally published on their official websites, making them easier to verify.

5. Less Negotiation on Car Price (Often)

When a dealership offers 0% APR, they are already providing a significant financial incentive. This often means they are less willing to negotiate on the actual sticker price of the car. They’ve effectively "given" you the interest savings, so they won’t want to cut into their profit margin further.

You might have to choose between a 0% APR deal or a cash rebate/discount. Sometimes, taking a low-interest loan with a significant cash discount might actually save you more money overall. Always do the math!

6. Strict Eligibility Criteria

As mentioned earlier, the qualification standards are exceptionally high. If your credit score is even slightly below the prime threshold, or if your debt-to-income ratio is a bit too high, you simply won’t qualify. There’s usually very little wiggle room.

Don’t assume you’ll qualify just because you have "good" credit; you need "excellent" credit.

7. Penalties for Late Payments (Interest Reverts)

This is a critical point that many borrowers overlook. Most 0% APR loans come with a deferred interest clause. If you make even one late payment, or if you default on the loan, the promotional 0% APR can be immediately revoked.

At that point, all the interest that would have accrued from the beginning of the loan can be retroactively applied. This can turn a fantastic deal into a financial nightmare very quickly. Always make your payments on time, every time.

Navigating the Application Process

Securing a 0% APR car loan requires careful planning and a strategic approach. It’s not just about showing up at the dealership and hoping for the best.

Here’s how to navigate the process effectively:

1. Check Your Credit Score First

Before you even step foot in a dealership, know where you stand. Obtain your credit report and score from all three major bureaus (Experian, Equifax, TransUnion). Correct any errors you find. This gives you a realistic idea of your eligibility and prevents any surprises.

Familiarize yourself with your FICO score, as this is what most auto lenders use.

2. Get Pre-Approved (Even for 0%)

While 0% APR offers are typically tied to manufacturer financing, getting pre-approved for a standard car loan from your bank or credit union is a smart move. This gives you a benchmark interest rate. You’ll know what kind of rate you qualify for if the 0% APR doesn’t work out, or if a cash rebate with a low-interest loan proves to be a better deal.

It also gives you leverage at the dealership; you’re coming in with your own financing already secured.

3. Research Specific Deals

Don’t wait for the dealer to tell you about 0% APR offers. Proactively research manufacturer websites (e.g., Ford, Honda, Toyota, GM) for current incentives and promotions. These offers are usually advertised clearly during specific sales periods.

Knowing the exact terms and eligible models beforehand empowers you during negotiations.

4. Negotiate the Car Price First

Based on my experience, one of the savviest moves is to negotiate the price of the car before discussing financing. Dealerships often try to combine these discussions, which can obscure the true cost. Get the best possible price on the vehicle itself.

Once you have an agreed-upon price, then pivot to the financing options, including the 0% APR offer. This ensures you’re not paying a premium on the car just to get the zero interest.

5. Read the Fine Print (Meticulously)

This cannot be stressed enough. Get a copy of the loan agreement and read every single line before signing. Pay close attention to:

- The actual APR (confirm it’s 0%).

- The loan term.

- Monthly payment amount.

- Late payment penalties and if interest reverts.

- Any additional fees or charges.

- Any clauses about pre-payment penalties (rare with car loans but worth checking).

If you don’t understand something, ask for clarification until you do.

Pros of a 0% APR Car Loan

Despite the stringent requirements and potential catches, a 0% APR car loan can be incredibly advantageous if you qualify and manage it correctly.

Here are the primary benefits:

1. Significant Savings

The most obvious and compelling advantage is the elimination of interest costs. This translates directly into substantial savings over the life of the loan, often thousands of dollars. These savings mean the total cost of your vehicle is exactly its sticker price (plus taxes and fees), nothing more.

You keep more of your hard-earned money in your pocket.

2. Faster Debt Payoff

With every payment going entirely towards the principal, you’re paying down your car loan debt much faster than with a traditional interest-bearing loan. This accelerates your journey to being debt-free.

Reducing your debt load quickly can free up your budget for other financial goals, such as saving for a home or retirement.

3. Build Credit (If Managed Well)

Even though it’s a 0% interest loan, it’s still an installment loan that gets reported to credit bureaus. Making all your payments on time and in full will demonstrate excellent credit management. This positive payment history can further boost your credit score.

This strengthens your financial profile for future borrowing needs, such as a mortgage.

Cons of a 0% APR Car Loan

While the benefits are attractive, it’s equally important to acknowledge the downsides and potential pitfalls of these specialized loans.

Consider these cons carefully:

1. Strict Qualification

As detailed earlier, the eligibility bar is set very high. If your credit isn’t top-tier, or your financial situation isn’t perfect, you simply won’t qualify. This can be disappointing and lead to wasted time if you haven’t prepared.

Many hopeful buyers find themselves ineligible, leading them to other financing options.

2. Limited Choices

You often have to compromise on your desired vehicle. The 0% APR offers are tied to specific models, trims, or inventory that the manufacturer wants to move. This might mean settling for a car that isn’t exactly what you envisioned.

Your perfect car might not be available with a 0% APR deal, forcing a trade-off between the car and the financing.

3. Higher Monthly Payments

The shorter loan terms associated with 0% APR mean larger monthly payments. If your budget is tight, these higher payments could put a strain on your finances. This could make it difficult to save or cover other expenses.

A high monthly payment can lead to financial stress if your income fluctuates or unexpected costs arise.

4. Potential for Reverted Interest

The deferred interest clause is a serious risk. If you miss a payment, even by a day, you could lose the 0% APR and be charged all the accrued interest from day one. This negates all the potential savings.

This risk means you must be absolutely diligent with your payment schedule.

5. Less Price Negotiation Power

Because the 0% APR is a significant incentive, dealerships are often less flexible on the car’s sticker price. You might end up paying more for the vehicle itself than you would if you opted for a cash rebate and a standard low-interest loan.

Always compare the total cost: a higher price with 0% APR vs. a lower price with a low-interest rate.

Is a 0% APR Car Loan Right for You?

Deciding if a 0% APR car loan is the right choice comes down to a careful self-assessment of your financial situation and priorities.

When it’s a great fit:

- You have excellent credit: Your score is 750+ and your financial history is spotless.

- You have a stable income and low DTI: You can comfortably afford the higher monthly payments without stress.

- The eligible car is exactly what you want: The specific model and trim that qualify for 0% APR aligns perfectly with your needs and desires.

- You’ve negotiated a fair price: You’ve ensured you’re not overpaying for the car just to get the zero interest.

- You’re disciplined with payments: You’re confident you’ll make every payment on time, every time, to avoid reverting interest.

When you should reconsider:

- Your credit isn’t stellar: You’re unlikely to qualify, and pursuing these offers might lead to multiple hard inquiries on your credit report.

- Your budget is tight: Higher monthly payments could strain your finances and increase the risk of missing a payment.

- The eligible cars aren’t what you need: Don’t settle for a car you don’t truly want just for the 0% APR.

- You could get a better deal elsewhere: Sometimes, a significant cash rebate combined with a low-interest loan from an external lender can result in greater overall savings.

- You’re prone to late payments: The risk of losing the 0% APR and incurring retroactive interest is too high.

Alternatives to 0% APR Loans

If a 0% APR car loan isn’t feasible or isn’t the best option for your situation, don’t despair. There are plenty of other viable financing avenues available.

Consider these alternatives:

1. Low-Interest Loans (Traditional)

Many banks, credit unions, and online lenders offer competitive interest rates for car loans, especially if you have good credit. These rates, while not 0%, can still be very affordable. You might find more flexible terms, longer repayment periods (leading to lower monthly payments), and a wider selection of vehicles.

Shop around for the best rates; even a difference of 1-2% can save you hundreds over the loan term.

2. Cash Purchase

If you have sufficient savings, paying for a car outright with cash eliminates any interest costs and the burden of monthly payments. This gives you complete ownership and no financial commitments. However, it means tying up a significant portion of your liquid assets.

Consider if using cash is the best allocation of your funds, or if those funds could generate a higher return elsewhere.

3. Used Car Loans

Used cars are generally more affordable than new ones, which means you’ll need to borrow less money. Interest rates on used car loans might be slightly higher than for new cars, but the lower principal amount often results in lower overall interest paid.

This can be a smart financial move if you’re looking for value and don’t need the latest model.

4. Leasing

Leasing a car means you’re essentially renting it for a fixed period (usually 2-4 years) and then returning it or buying it at the end of the term. You only pay for the depreciation of the car during the lease period, not its full purchase price. This results in lower monthly payments compared to buying.

Leasing is ideal for those who like to drive a new car every few years, have predictable mileage, and prefer lower upfront costs.

Pro Tips from Us: Your Expert Blogger

As an expert blogger who has followed the auto industry and consumer finance for years, I’ve seen common patterns and learned valuable lessons. Here are some pro tips to guide you:

- Always Compare Total Cost: Don’t get fixated on the "0%" alone. Always calculate the total cost of the car with the 0% APR versus the total cost with a cash rebate and a low-interest loan. Sometimes, the cash rebate can save you more money overall, even with a small interest rate.

- Don’t Get Fixated on 0% Alone: The perfect car for you might not be eligible for a 0% APR deal. Don’t compromise on your needs or preferences just to chase zero interest. The right car for the right price, with a reasonable interest rate, is often a better long-term solution.

- Read Every Single Line: I cannot emphasize this enough. The fine print is where potential issues hide. Take your time, ask questions, and don’t feel pressured to sign anything until you fully understand it.

- Beware of Upselling: Dealerships make money on financing, add-ons (like extended warranties, paint protection, gap insurance), and accessories. They might push these harder if they’re not making money on interest. Only purchase what you truly need and have researched.

- Know Your Budget: Go into the car-buying process with a clear, firm understanding of your maximum monthly payment and total budget. Stick to it. This prevents emotional overspending.

Common Mistakes to Avoid Are…

Even the savviest buyers can fall into traps when dealing with enticing offers like 0% APR. Based on my observations, here are some common mistakes to actively avoid:

- Not Checking Your Credit Score: Going in blind leaves you vulnerable. You won’t know if you truly qualify, and you might accept a less favorable offer out of ignorance.

- Ignoring the Fine Print: This is a recipe for disaster. Overlooking deferred interest clauses or strict payment terms can turn a dream deal into a nightmare.

- Focusing Only on Monthly Payment: While important, the monthly payment alone doesn’t tell the whole story. Consider the total cost of the car, including any hidden fees or if you’re overpaying the sticker price.

- Falling for Add-Ons You Don’t Need: Dealerships will try to upsell. Be firm and only purchase what genuinely adds value to you. Most add-ons are significantly marked up.

- Delaying Payment: With 0% APR, a single late payment can revert your interest. This is one loan where you absolutely cannot afford to be late. Set up automatic payments if necessary.

Conclusion: Drive Smart, Not Just Interest-Free

A 0 percent APR car loan can be a truly fantastic financial opportunity, offering significant savings and faster debt payoff. However, it’s a privilege reserved for the most creditworthy borrowers who are also prepared to navigate the strict terms and potential trade-offs. It’s not a free ride, but rather a carefully constructed incentive.

By understanding the qualification criteria, diligently reading the fine print, and strategically approaching the negotiation process, you can determine if this dream deal aligns with your financial reality. Remember, the ultimate goal is to make an informed decision that gets you into the right car at the best overall value, whether that’s with zero interest or a competitive low-interest rate. Drive smart, and your car-buying journey will be a success!

External Link Example: For more information on understanding your credit score and reports, visit the Consumer Financial Protection Bureau (CFPB) website at https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/.