The Ultimate Guide to 0 Percent Interest Car Loans: Unlocking the Deal of a Lifetime (or a Clever Trap?)

The Ultimate Guide to 0 Percent Interest Car Loans: Unlocking the Deal of a Lifetime (or a Clever Trap?) Carloan.Guidemechanic.com

The phrase "0 Percent Interest Car Loan" sounds like music to any car buyer’s ears. Imagine driving away in a brand new vehicle without paying a single cent in interest over the life of your loan. It’s a powerful incentive, often advertised with big, bold letters that capture immediate attention. But is this truly a financial golden ticket, or are there hidden complexities lurking beneath the surface?

As an expert blogger and professional SEO content writer, I’ve spent years dissecting financial offers and helping consumers make informed decisions. In this comprehensive guide, we’ll peel back the layers of 0% APR car financing. We’ll explore what these deals truly entail, who qualifies, and how to navigate the process to ensure you’re getting a genuinely good deal, not just a flashy one.

The Ultimate Guide to 0 Percent Interest Car Loans: Unlocking the Deal of a Lifetime (or a Clever Trap?)

This article is designed to be your definitive resource, offering actionable insights and professional tips. By the time you finish reading, you’ll possess the knowledge to confidently approach any 0 percent interest car loan offer, understanding both its immense potential and its potential pitfalls.

The Allure of Zero: What Exactly is a 0% Interest Car Loan?

At its core, a 0 percent interest car loan, often referred to as a "zero APR car financing" offer, means you pay no additional cost for borrowing money to purchase your vehicle. APR stands for Annual Percentage Rate, and it represents the yearly cost of your loan. With a 0% APR, that cost is, quite literally, zero.

This type of financing stands in stark contrast to traditional auto loans, where you typically pay an interest rate ranging from a few percent to upwards of 20% or more, depending on your creditworthiness and market conditions. Over several years, even a low-interest rate can add thousands of dollars to the total cost of your car. Eliminating this cost is a significant saving.

These coveted deals are almost exclusively offered by car manufacturers or their captive finance arms, rather than independent banks or credit unions. They are usually tied to specific new car models and are part of broader marketing strategies to stimulate sales. Understanding this fundamental distinction is crucial for your car buying journey.

The "Why": Why Do Dealerships Offer 0% APR?

It might seem counterintuitive for a lender to offer money without charging interest. However, there are several strategic reasons why dealerships and manufacturers roll out these attractive 0% financing car deals. They aren’t doing it purely out of generosity; there’s a clear business objective.

Firstly, 0 percent interest car loans are powerful marketing tools. They generate buzz and draw customers into showrooms who might not otherwise consider buying a new car. The "no interest" hook is incredibly compelling in a competitive market.

Secondly, manufacturers use these incentives to move specific inventory. This often includes slow-selling models, vehicles from the previous model year they need to clear out, or cars they want to promote. By offering a 0% loan, they can make less popular models more attractive to buyers.

Thirdly, these offers can be part of broader market competition. When one manufacturer offers 0% financing, others may follow suit to remain competitive. It becomes a race to offer the most appealing terms to potential buyers, ultimately benefiting those with excellent credit.

The Golden Ticket: Eligibility Requirements for a 0% Interest Car Loan

While the idea of a no interest auto loan is enticing, not everyone qualifies. Lenders offering these deals are taking on a higher risk (by foregoing interest revenue), so they impose stringent requirements. Meeting these criteria is your "golden ticket" to securing such a deal.

1. Your Credit Score: The Most Critical Factor

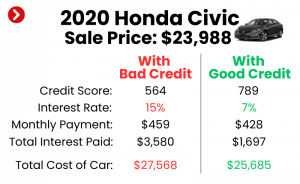

Without a doubt, your credit score is the single most important determinant for qualifying for a 0 percent interest car loan. Lenders typically require an excellent credit score, usually in the range of 720, 760, or even higher (FICO score). This indicates to the lender that you are a low-risk borrower with a proven history of managing debt responsibly.

Why is it so important? A high credit score signals financial discipline and a very low probability of default. Since the lender isn’t making money on interest, they need absolute confidence that you will repay the principal amount in full and on time. Based on my experience, many people get excited about 0% but haven’t checked their credit score. This is a common mistake.

Pro tip from us: Check your credit score before you even set foot in a dealership. Knowing your score empowers you and allows you to address any inaccuracies. If your score isn’t quite there yet, focus on improving it first. .

2. Down Payment: Often Required or Highly Beneficial

While not always explicitly stated as a requirement for 0% APR, a significant down payment can greatly improve your chances. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also shows your financial commitment to the purchase.

Some 0% financing car deals might explicitly require a minimum down payment, such as 10% or 20% of the vehicle’s purchase price. Even if it’s not mandated, putting more money down can result in lower monthly payments, making the loan more manageable.

3. Loan Term: Usually Shorter Durations

Don’t expect a 0 percent interest car loan to come with a sprawling 72- or 84-month term. These offers are almost always tied to shorter loan durations, typically 36, 48, or 60 months. The shorter the term, the higher your monthly payments will be, as you’re paying off the entire principal in a condensed timeframe.

Lenders prefer shorter terms because it reduces their exposure to risk over time. It also means you’ll own the car outright faster. Be realistic about whether you can comfortably afford these higher monthly payments before committing.

4. Specific Models: Not All Cars Qualify

It’s rare to find 0% APR on every vehicle on a dealership lot. These offers are typically limited to specific new car models, often those the manufacturer is trying to clear out, new releases, or vehicles that aren’t selling as quickly as anticipated. They are almost exclusively for new vehicles, not used cars.

Don’t go into a dealership with your heart set on a particular model and assume it will qualify for 0% financing. Always research which specific models and trims are eligible for the deal before you start shopping. This will save you time and potential disappointment.

5. Income & Debt-to-Income Ratio: Lender Assessment

Lenders will also evaluate your income and your debt-to-income (DTI) ratio. Your income needs to be sufficient to comfortably cover the higher monthly payments associated with a shorter 0% loan term. Your DTI ratio, which compares your total monthly debt payments to your gross monthly income, should be low.

A low DTI indicates that you’re not overextended financially and have enough disposable income to handle the new car payment. This provides further assurance to the lender that you can meet your repayment obligations.

The Process: How to Secure a 0% Interest Car Loan

Navigating the path to a 0 percent interest car loan requires a strategic approach. It’s more than just walking into a dealership and asking for the deal. Here’s a step-by-step guide based on best practices.

Step 1: Credit Score Check & Improvement

As reiterated, this is foundational. Obtain your credit reports from all three major bureaus (Equifax, Experian, TransUnion) and check your scores. Dispute any inaccuracies. If your score needs a boost, dedicate time to improving it before applying for any car loan. This proactive step will significantly increase your chances of securing the best terms.

Step 2: Research Qualifying Vehicles & Offers

Don’t wait until you’re at the dealership. Visit manufacturer websites, check automotive news sites, and consult financial publications to identify current 0% APR offers. Pinpoint the specific models and trims that are eligible. This focused research will prevent you from being swayed by non-qualifying vehicles.

Step 3: Get Pre-Approved (if possible)

While true 0% APR is often dealer-specific, understanding your general financing options is wise. Get pre-approved for a conventional low-interest car loan from your bank or credit union before visiting the dealership. This gives you a baseline interest rate to compare against and provides negotiating leverage. Even if you don’t use it, it shows you’re a serious buyer with financing secured.

Step 4: Understand the Fine Print

Before you get too deep, carefully read the terms and conditions of any advertised 0% offer. Look for details on eligibility, required down payments, and any specific vehicle restrictions. Sometimes, the offer is only available for a limited time or on a very specific trim level.

Step 5: Negotiate the Car Price Independently

This is where many buyers make a crucial mistake when pursuing a 0 percent interest car loan. They get so fixated on the "zero" that they forget to negotiate the actual purchase price of the vehicle. Dealers may be less willing to discount the car significantly if they’re also giving you 0% financing, aiming to recoup lost interest revenue through a higher sticker price.

Pro tip: Always negotiate the car’s price as if you were paying cash or arranging your own financing. Secure the best possible price first, then discuss the 0% financing option. If the price isn’t competitive, the 0% APR might not be as good of a deal as it seems. .

Step 6: Read the Contract Carefully

Once you’ve agreed on a price and are ready to finalize the loan, read every single line of the contract. Ensure the agreed-upon 0% APR is clearly stated and that there are no hidden fees or clauses that could change the terms later. Pay close attention to late payment penalties; sometimes, a single missed payment can revert your loan to a much higher interest rate.

The Trade-Offs: Pros and Cons of 0% Interest Car Loans

Like any financial product, 0 percent interest car loans come with their own set of advantages and disadvantages. It’s essential to weigh these carefully to determine if such an offer truly aligns with your financial situation and car buying goals.

Pros of a 0% Interest Car Loan:

- Significant Savings on Interest: This is the most obvious and compelling benefit. You save potentially thousands of dollars that would otherwise go to interest payments, making the total cost of the car much lower.

- Lower Overall Cost of Ownership: By eliminating interest, more of your monthly payment goes directly towards paying down the principal. This means you pay off the car faster and own it free and clear sooner.

- Potentially Lower Monthly Payments (if structured well): If you combine 0% APR with a reasonable loan term and a good down payment, your monthly payments can be very manageable compared to a loan with interest.

- Faster Debt Repayment: Without interest accumulating, you can pay down the principal balance more rapidly, reducing the time you are in debt for the vehicle.

- Builds Credit History: Successfully managing and repaying a 0% interest car loan demonstrates responsible borrowing, which can further strengthen your excellent credit score.

Cons of a 0% Interest Car Loan:

- Higher Purchase Price (Less Negotiation Room): As discussed, dealers might be less flexible on the vehicle’s price, as they’re not making money on interest. You might pay full sticker price or close to it.

- Limited Car Choice: These deals are often restricted to specific models, colors, or trim levels, limiting your options. You might not get the exact car you want.

- Shorter Loan Terms (Higher Monthly Payments): The shorter repayment period (e.g., 36-60 months) means your monthly payments will be higher than they would be for a longer-term loan, even with 0% interest. You need to ensure these payments fit your budget.

- Strict Eligibility Requirements: The need for an excellent credit score, a solid down payment, and a good debt-to-income ratio excludes a significant portion of potential buyers.

- Penalties for Late Payments: Be extremely careful here. Many 0% offers include a clause that if you miss even one payment, the interest rate can jump dramatically (e.g., to 15% or 20%) for the remainder of the loan.

- May Forgo Cash Incentives/Rebates: Sometimes, manufacturers offer a choice between 0% APR financing or a substantial cash rebate. You typically can’t have both. It’s crucial to calculate which option saves you more money overall.

Common Pitfalls and How to Avoid Them (Expert Insights)

Based on my experience helping countless consumers navigate car deals, I’ve seen several recurring mistakes when people chase the dream of a 0 percent interest car loan. Being aware of these common pitfalls can save you money and stress.

Mistake 1: Not Negotiating the Car Price

This is perhaps the biggest error. Buyers become so fixated on the "zero" in the interest rate that they completely forget to negotiate the actual sale price of the vehicle. Dealers know this and may be unwilling to offer significant discounts, knowing they’re already providing a highly attractive financing deal.

Pro tip: Always, always, always negotiate the car’s price first, as if you were paying cash. Once you have a firm price, then bring up the 0% financing option. If the dealer won’t budge on price, compare the total cost of the 0% deal versus a lower price with a slightly higher (but still competitive) interest rate.

Mistake 2: Ignoring the Loan Term and Monthly Payments

A 0% APR on a 36-month loan will have much higher monthly payments than a 5% APR on a 72-month loan. While the 0% saves you interest, if the monthly payments are beyond your budget, you risk defaulting or struggling financially.

Pro tip: Don’t just look at the interest rate. Calculate the exact monthly payment for the specific 0% term offered. Be honest with yourself about whether you can comfortably afford it without straining your budget. It’s better to pay a little interest on a longer term than to default on a 0% loan.

Mistake 3: Overlooking Alternative Incentives

Many manufacturers offer a choice: either a 0% interest car loan or a cash rebate. These rebates can sometimes be thousands of dollars. Buyers often jump for the 0% without calculating if the cash rebate, combined with a low-interest loan (say, 3-5% from a credit union), would actually save them more money overall.

Pro tip: Do the math! Get the firm price of the car with the 0% offer. Then, ask for the firm price with the cash rebate. Calculate the total cost of the car (price + interest) for both scenarios. You might be surprised to find that the cash rebate plus a low-interest loan is the better deal.

Mistake 4: Not Reading the Fine Print on Late Payment Penalties

The terms of a 0% interest car loan can be very strict. A common clause states that if you miss even one payment or pay late, your interest rate can immediately revert to a much higher, standard rate (e.g., 15-20%) for the remainder of the loan. This negates the entire benefit.

Pro tip: Understand all the conditions for maintaining your 0% rate. Set up automatic payments to ensure you never miss a due date. Be incredibly diligent about your payments.

Mistake 5: Assuming All Cars Qualify

It’s common for buyers to walk into a dealership, see a 0% ad, and assume it applies to the shiny new model they’ve been eyeing. In reality, these offers are often limited to specific, sometimes less popular, models or previous model years that the dealer needs to move.

Pro tip: Conduct thorough research on manufacturer websites to identify exactly which models and trims are eligible for 0% financing before you begin your search. This focused approach will save you time and potential frustration.

Is a 0% Interest Car Loan Right for You? A Decision Framework.

Deciding whether a 0 percent interest car loan is the best option for you requires an honest assessment of your financial situation and priorities.

Who Benefits Most from a 0% APR Loan?

- Individuals with Excellent Credit (760+): If your credit score is impeccable, you’re the prime candidate.

- Those with a Stable Income and Clear Budget: You can comfortably afford the potentially higher monthly payments associated with shorter loan terms.

- Buyers Prioritizing Long-Term Savings on Interest: Your main goal is to minimize the total cost of borrowing.

- People Who Don’t Mind Limited Car Choices: You’re flexible on the exact model, color, or features, as long as you get a great financial deal.

- Disciplined Payers: You are confident you will make every payment on time, every time, to avoid penalty APRs.

Who Should Reconsider a 0% APR Loan?

- Those with Lower Credit Scores: If your score isn’t in the excellent range, you likely won’t qualify, or the terms might not be as advertised.

- Buyers Needing More Flexible or Longer Loan Terms: If higher monthly payments are a stretch, a 0% loan with a short term could be financially risky.

- People Who Prioritize a Specific Car Model or Features: If your dream car isn’t on the 0% list, don’t force it.

- Individuals Who Value Cash Rebates More: Sometimes a significant rebate combined with a low-interest loan is a better overall deal.

- Buyers Prone to Missing Payments: The risk of a penalty APR is too high.

Consider your overall financial goals. Is saving interest your absolute top priority, even if it means less flexibility on the car or higher monthly payments? Or would you prefer a slightly higher interest rate for a longer term and lower monthly payments, or a significant cash rebate?

Beyond Zero: What if You Don’t Qualify?

Don’t despair if a 0 percent interest car loan isn’t within your reach. There are still many excellent ways to finance a car and save money.

- Focus on Improving Your Credit: This is always a worthwhile endeavor. Pay bills on time, reduce revolving debt, and monitor your credit report for errors. A better credit score will open doors to better loan terms in the future.

- Consider a Low-Interest Loan from a Credit Union or Bank: Often, local credit unions offer very competitive interest rates, sometimes even better than what major banks provide. Shop around for the best conventional rates.

- Look for Other Dealer Incentives: Beyond 0% APR, dealerships often offer other attractive incentives. These might include low APR loans (e.g., 1.9% or 2.9%), significant cash rebates, or special lease deals.

- Save for a Larger Down Payment: A substantial down payment reduces the amount you need to borrow, which can lead to better interest rates and lower monthly payments on any loan.

- Consider a Reliable Used Car: The used car market often offers incredible value. While 0% APR is almost exclusively for new cars, you can find excellent financing deals on certified pre-owned vehicles or simply reliable used cars that fit your budget.

Expert Insights and Final Recommendations

As an expert blogger and SEO content writer with a focus on financial literacy, my ultimate advice for anyone considering a 0 percent interest car loan is simple: be informed, be diligent, and be patient. Don’t let the allure of "zero" blind you to the bigger picture.

- Always Compare Total Costs: This is the golden rule of car buying. Don’t just look at the monthly payment or the interest rate in isolation. Calculate the total amount you will pay for the car under various scenarios (0% APR, cash rebate + low interest, etc.).

- Don’t Be Afraid to Walk Away: If the deal doesn’t feel right, if the price isn’t negotiable, or if the terms are too restrictive, be prepared to walk away. There will always be other deals and other cars.

- Knowledge is Your Best Negotiation Tool: The more you know about the car, the market, your credit, and the financing options, the stronger your position at the dealership.

- Leverage External Resources: Don’t hesitate to consult trusted external sources for general car buying advice and market insights. .

Conclusion

A 0 percent interest car loan can indeed be a fantastic financial opportunity, allowing you to save thousands of dollars on your vehicle purchase. However, it’s not a deal without its specific requirements and potential trade-offs. It demands excellent credit, careful attention to the fine print, and a strategic approach to negotiation.

By understanding the mechanics behind these offers, meticulously checking your eligibility, and diligently comparing all your options, you can confidently navigate the car buying process. Remember, the goal is not just to get a 0% loan, but to secure the best overall deal that aligns with your financial health and driving needs. Armed with the insights from this comprehensive guide, you are now well-equipped to make an informed decision and drive away with confidence.