The Ultimate Guide to a Good Credit Score for a Car Loan: Drive Your Dream Car with Confidence

The Ultimate Guide to a Good Credit Score for a Car Loan: Drive Your Dream Car with Confidence Carloan.Guidemechanic.com

Imagine cruising down the highway in your dream car, the sun shining, your favorite music playing. For many, that dream feels distant, often shadowed by concerns about financing. The truth is, securing a great car loan isn’t just about the car; it’s profoundly about your credit score.

Your credit score is more than just a number; it’s a powerful financial report card that lenders use to assess your trustworthiness. When it comes to something as significant as a car loan, this score can be the difference between getting approved with a low interest rate or facing higher payments, or even outright rejection.

The Ultimate Guide to a Good Credit Score for a Car Loan: Drive Your Dream Car with Confidence

In this comprehensive guide, we’re going to demystify the world of credit scores and car loans. We’ll explore what a "good" score truly means, why it holds so much power, and most importantly, how you can cultivate and leverage an excellent credit profile to secure the best possible financing for your next vehicle. Get ready to take the driver’s seat of your financial future!

What Exactly is a Credit Score, and Why Does It Matter for a Car Loan?

Before we dive deep, let’s establish a foundational understanding. A credit score is a three-digit number, typically ranging from 300 to 850, that represents your creditworthiness. It’s generated by complex algorithms from information in your credit report, which details your borrowing and repayment history.

When you apply for a car loan, lenders don’t just look at your income. They want to know how reliable you’ve been in paying back money you’ve borrowed in the past. Your credit score provides a quick, standardized snapshot of that reliability.

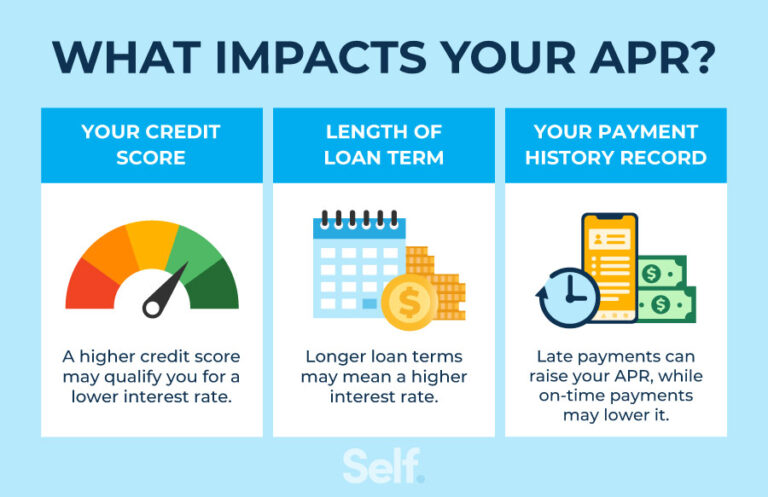

For a car loan specifically, your score dictates several crucial aspects. It directly influences your approval chances, the interest rate you’ll be offered, the length of your loan term, and sometimes even the down payment required. A higher score signals less risk to the lender, opening the door to more favorable terms and significant savings over the life of the loan.

Defining "Good": What Credit Score Do You Need for a Car Loan?

The term "good" is subjective in many contexts, but in the realm of credit scores for car loans, there are fairly clear benchmarks. While different scoring models exist (FICO and VantageScore are the most common), they generally categorize scores into similar tiers.

Let’s break down what these tiers typically mean for auto loan applicants:

Excellent Credit: 780-850

If your score falls into this range, you’re in an enviable position. Lenders view you as an extremely low-risk borrower, almost guaranteeing approval for competitive rates. You’ll likely qualify for the absolute lowest advertised interest rates and have the most flexibility in loan terms.

Good Credit: 670-739

This is the sweet spot for many borrowers. With a good credit score, you’re considered a reliable applicant and will likely be approved for most car loans. While your interest rates might not be the absolute rock-bottom, they will still be very attractive and significantly lower than those offered to individuals with fair or poor credit.

Fair Credit: 580-669

Applicants in this range are often approved, but usually with higher interest rates. Lenders see a moderate risk, meaning they’ll charge more to offset that perceived risk. You might also be asked for a larger down payment or have fewer choices for loan terms.

Poor Credit: 300-579

Securing a traditional car loan with a score in this range can be challenging. You might face rejections, or if approved, prepare for significantly higher interest rates, stringent terms, and potentially needing a co-signer or a very large down payment. Subprime lenders specialize in this tier, but their rates are notoriously high.

Pro tips from us: Always aim for the "good" or "excellent" range. Even a small improvement in your score can translate into thousands of dollars saved on interest over a five or six-year car loan. Understanding these tiers is your first step towards strategic borrowing.

The Power of Your Score: How It Impacts Your Car Loan Offer

The difference between an "excellent" and "fair" credit score might seem like just a few points, but its financial impact on a car loan is profound. It’s not just about getting approved; it’s about the cost of borrowing.

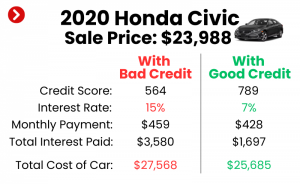

Consider this: A car loan of $30,000 over five years.

- With excellent credit (e.g., 760 FICO): You might qualify for an interest rate as low as 4-6%. Your monthly payment could be around $560-$575.

- With good credit (e.g., 690 FICO): Your rate might be 6-9%. Monthly payments could rise to $580-$600.

- With fair credit (e.g., 620 FICO): Rates could jump to 10-15% or even higher. This could push your monthly payment to $635-$685, adding thousands to the total cost of the car.

These aren’t just hypothetical numbers. Based on my experience in the financial sector, these rate disparities are very real and can dramatically affect your budget. The higher your interest rate, the more money you pay the lender in addition to the principal loan amount. Over five or six years, that extra interest can easily equate to the cost of another vacation or a significant down payment on a house.

Furthermore, a strong credit score can give you leverage. You might negotiate better terms, secure a lower down payment, or even gain access to promotional rates that are only offered to the most creditworthy borrowers.

Deconstructing Your Credit Score: The 5 Key Factors

To improve your credit score for a car loan, you first need to understand what makes it tick. Your FICO score, which is widely used by auto lenders, is built upon five primary factors, each weighted differently.

1. Payment History (35% of your score)

This is the single most important factor. It records whether you pay your bills on time. Late payments, especially those 30, 60, or 90+ days past due, severely damage your score.

A consistent history of on-time payments, whether for credit cards, previous loans, or even utility bills reported to credit bureaus, builds a strong foundation. Lenders want to see reliability and responsibility.

2. Amounts Owed / Credit Utilization (30% of your score)

This factor looks at how much credit you’re using compared to your total available credit. For instance, if you have a credit card with a $10,000 limit and a $5,000 balance, your utilization is 50%.

Experts generally recommend keeping your credit utilization below 30% across all your credit accounts. High utilization suggests you might be over-reliant on credit, which lenders view as a risk.

3. Length of Credit History (15% of your score)

This factor considers how long your credit accounts have been open, and how long it’s been since you used them. A longer credit history with responsible behavior generally translates to a higher score.

It provides lenders with more data points to assess your long-term financial habits. Don’t be too quick to close old, unused credit card accounts, as this can shorten your average credit age.

4. New Credit (10% of your score)

This factor examines how many new credit accounts you’ve opened recently and how many hard inquiries appear on your report. Each time you apply for new credit (like a new credit card or loan), a "hard inquiry" is typically made, which can temporarily ding your score.

Applying for multiple lines of credit in a short period can signal to lenders that you’re in financial distress or taking on too much debt, making you a higher risk.

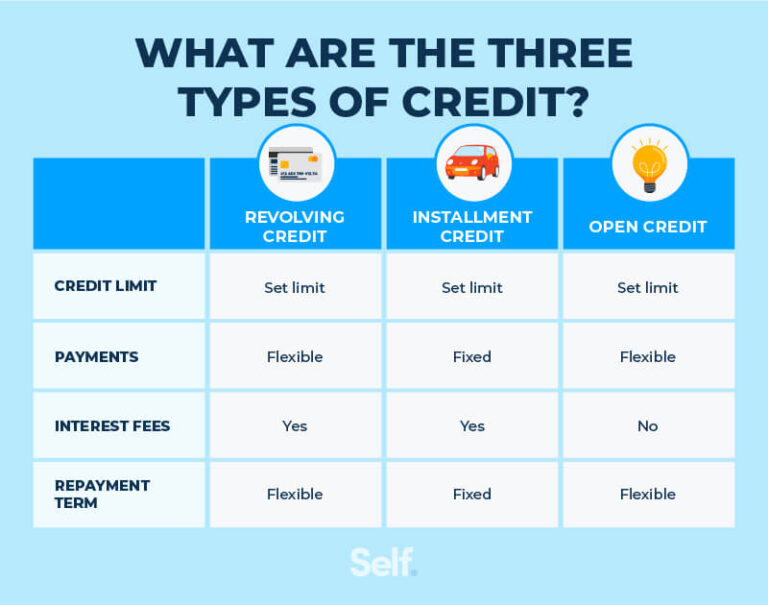

5. Credit Mix (10% of your score)

This factor assesses the different types of credit you have, such as revolving credit (credit cards) and installment loans (mortgages, auto loans, student loans). Having a healthy mix demonstrates your ability to manage various types of debt responsibly.

While it’s the smallest factor, a diverse credit portfolio can show a well-rounded financial profile. However, never take on debt you don’t need just to improve your credit mix.

Strategic Steps to Boost Your Credit Score for a Car Loan

Improving your credit score isn’t an overnight process, but with consistent effort, you can make significant strides. Here are actionable steps to take before you walk into a dealership.

1. Obtain and Review Your Credit Reports

This is your starting point. You’re entitled to a free copy of your credit report from each of the three major bureaus (Experian, Equifax, TransUnion) once every 12 months via AnnualCreditReport.com.

Scrutinize these reports for any errors, inaccuracies, or signs of identity theft. Even a small mistake can negatively impact your score. If you find errors, dispute them immediately with the credit bureau.

2. Pay All Bills On Time, Every Time

As we discussed, payment history is paramount. Set up automatic payments for all your bills, especially credit cards and other loans. If you’re struggling, contact your creditors before a payment is due to discuss options.

Based on my experience, consistently paying bills on time is the single most impactful action you can take to improve your credit score. Even one missed payment can set you back significantly.

3. Reduce Your Credit Utilization

Focus on paying down your credit card balances. Aim to keep your total credit card utilization below 30%, but ideally below 10% for the best impact.

If you have multiple cards, concentrate on paying down the one with the highest balance relative to its limit first. This strategy can quickly boost your score.

4. Avoid Opening New Credit Accounts

In the months leading up to your car loan application, refrain from applying for new credit cards, personal loans, or even store credit. Each hard inquiry can slightly lower your score, and a cluster of them can send a negative signal to auto lenders.

Allow your credit profile to stabilize and mature before introducing new variables.

5. Keep Old Accounts Open

Unless an old credit card carries an annual fee you can’t justify, it’s often better to keep it open, even if you don’t use it frequently. Closing an old account shortens your average credit history and can increase your credit utilization ratio if it has a high limit.

If you must close an account, consider one that is newer or has a lower credit limit.

6. Consider a Secured Credit Card or Credit Builder Loan

If your credit score is very low or you have limited credit history, these tools can help. A secured credit card requires a cash deposit as collateral, which often becomes your credit limit. A credit builder loan puts your loan amount into a savings account while you make payments, only releasing it once the loan is paid off.

Both options allow you to demonstrate responsible repayment behavior, which is then reported to credit bureaus.

What If You Have Bad Credit? Options and Pitfalls to Avoid

Even with a less-than-ideal credit score, securing a car loan isn’t impossible, but it requires a more strategic approach. It’s crucial to understand your options and be aware of potential traps.

1. Get a Co-Signer

A co-signer with excellent credit can significantly improve your chances of approval and help you secure a better interest rate. This person legally agrees to be responsible for the loan if you fail to make payments.

Important consideration: This is a major responsibility for the co-signer, as it impacts their credit too. Ensure you can make payments consistently to protect their credit and your relationship.

2. Make a Larger Down Payment

A substantial down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It can make you a more attractive borrower even with a lower credit score.

A larger down payment also means lower monthly payments and less interest paid over the life of the loan.

3. Explore Credit Unions

Credit unions are member-owned financial institutions that often have more flexible lending criteria and may be more willing to work with individuals who have fair or poor credit, sometimes offering better rates than traditional banks.

They tend to prioritize their members’ financial well-being over maximizing profits.

4. Look for Subprime Lenders (with caution)

There are lenders who specialize in loans for individuals with poor credit. While they offer a path to car ownership, their interest rates are significantly higher, sometimes reaching double-digits or even 20%+.

Common mistakes to avoid are blindly accepting the first offer from a subprime lender. Shop around, understand all terms, and ensure you can genuinely afford the payments. High interest can lead to a cycle of debt.

5. Consider "Buy Here, Pay Here" Dealerships (as a last resort)

These dealerships often provide financing directly, without relying on traditional banks. While approval is almost guaranteed, their interest rates are typically the highest in the industry, and the car selection might be limited.

Pro tips from us: If you must use a "buy here, pay here" option, ensure they report your payments to credit bureaus. This is crucial for rebuilding your credit. Otherwise, you’re just making high payments without any long-term benefit to your credit profile.

The Car Loan Application Process and Your Credit Score

Understanding how your credit score interacts with the application process can save you stress and money.

1. Get Pre-Approved

Before you even step foot on a dealership lot, get pre-approved for a loan. You can do this with your bank, credit union, or an online lender. Pre-approval gives you a clear idea of how much you can borrow and at what interest rate, based on your credit score.

This turns you into a cash buyer at the dealership, allowing you to negotiate the car price separately from the financing, potentially saving you thousands.

2. Rate Shopping and Hard Inquiries

When you apply for a loan, a "hard inquiry" is made on your credit report. Multiple hard inquiries in a short period can negatively affect your score. However, credit scoring models are smart. They understand that when you’re rate shopping for a car loan, you’re not trying to open multiple lines of credit.

Most models treat multiple auto loan inquiries within a 14-45 day window as a single inquiry, minimizing the impact on your score. So, shop around for the best rates within a focused period.

3. Don’t Let Dealerships Run Excessive Credit Checks

When you’re at the dealership, they might ask to run your credit with multiple lenders. While some checks are necessary, be wary of them running it with an excessive number of lenders without your explicit consent. Each unnecessary hard inquiry can have a minor, temporary negative impact.

Be firm and ask them to use the pre-approval you already have, or to limit their inquiries to a select few lenders.

Maintaining Good Credit: The Long-Term Game

Securing a great car loan isn’t the end of your credit journey; it’s another chapter. Maintaining good credit after getting your loan is just as important for your future financial health.

1. Consistent On-Time Payments

This is non-negotiable. Your car loan payments will be reported to credit bureaus. Missing payments will quickly damage the score you worked so hard to build. Set up auto-pay, if possible, to ensure you never miss a due date.

2. Avoid Overextending Yourself

Don’t take on more debt than you can comfortably manage. Just because you have a good score doesn’t mean you should max out credit cards or apply for other loans unnecessarily.

Keep your credit utilization low and maintain a healthy debt-to-income ratio.

3. Monitor Your Credit Regularly

Continue to check your credit reports annually for accuracy. Consider using free credit monitoring services offered by credit card companies or financial apps, which often provide monthly updates to your score.

Early detection of errors or fraudulent activity can save you a lot of headache and protect your financial standing.

4. Financial Literacy is Key

Stay informed about personal finance. Understanding concepts like interest, APR, debt consolidation, and budgeting will empower you to make smarter financial decisions throughout your life. For more in-depth knowledge on managing debt, you might want to explore articles like .

Common Mistakes to Avoid When Seeking a Car Loan

Navigating the car loan landscape can be tricky. Here are some common pitfalls that people fall into, which you should actively avoid:

- Not checking your credit score beforehand: Going into a dealership blind means you don’t know what rates you truly qualify for, putting you at a disadvantage.

- Applying for too much credit: As mentioned, too many hard inquiries in a short period can harm your score.

- Focusing only on the monthly payment: While important, a low monthly payment over an extended loan term (e.g., 72 or 84 months) can mean paying significantly more in interest over the life of the loan. Always look at the total cost of the loan.

- Ignoring the fine print: Always read the loan agreement carefully before signing. Understand all fees, terms, and conditions.

- Falling for "guaranteed approval" scams: If it sounds too good to be true, it probably is. These often come with predatory interest rates and unfavorable terms.

- Letting your car loan go into default: This is one of the most damaging actions for your credit score and can lead to vehicle repossession. If you’re struggling, communicate with your lender immediately.

Conclusion: Drive Towards Your Financial Goals with Confidence

Your credit score is an indispensable tool in your financial arsenal, especially when it comes to securing a car loan. It’s the key that unlocks lower interest rates, more flexible terms, and ultimately, a more affordable path to owning your desired vehicle. By understanding what constitutes a good score, how it’s calculated, and the strategic steps to improve it, you empower yourself to make informed decisions.

Remember, building and maintaining excellent credit is a journey, not a sprint. It requires discipline, consistency, and a proactive approach to your financial health. Start by getting your free credit report, paying your bills on time, and keeping your credit utilization in check. These simple yet powerful actions will set you on the right track.

Don’t let the fear of a bad credit score deter you from your dream car. Instead, use this knowledge as your roadmap. With a solid credit score in hand, you’re not just buying a car; you’re investing in your financial future and driving away with the peace of mind that comes from a smart, well-negotiated deal. For more insights into smart financial planning, consider exploring resources like the Consumer Financial Protection Bureau’s advice on auto loans: External Link: https://www.consumerfinance.gov/consumer-tools/auto-loans/.

Now, go forth, check your score, and prepare to drive your dream car with confidence and financial savvy!