The Ultimate Guide to a Smart Car Loan Search: Secure Your Best Auto Loan Rates

The Ultimate Guide to a Smart Car Loan Search: Secure Your Best Auto Loan Rates Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is exciting, but the process of securing financing can often feel overwhelming. Many prospective car owners jump straight into looking at cars without first understanding the crucial steps of a strategic car loan search. This guide is designed to empower you with the knowledge and tools needed to navigate the complexities of auto financing, ensuring you secure not just any loan, but the best car loan rates for your financial situation.

A well-executed car loan search is more than just finding a lender; it’s about understanding your financial standing, comparing offers, and making informed decisions that save you thousands over the life of your loan. We’ll delve deep into every aspect, from preparing your finances to decoding loan terms and avoiding common pitfalls. By the end of this article, you’ll be equipped to approach your next auto loan with confidence and clarity, making it a truly smart financial move.

The Ultimate Guide to a Smart Car Loan Search: Secure Your Best Auto Loan Rates

1. Laying the Foundation: Before You Begin Your Car Loan Search

Before you even step foot in a dealership or browse online car listings, a crucial preliminary stage is required. A smart car loan search begins with introspection and financial preparation. This foundational work will significantly influence the rates and terms you qualify for, setting you up for success.

Understand Your Vehicle Needs and Budget

The first step in any car purchase, and consequently your auto loan search, is to define your needs. Are you looking for a brand-new vehicle with the latest features, or is a reliable used car a better fit for your lifestyle and budget? Each option comes with different implications for financing.

New cars typically offer lower interest rates due to their higher value and lower risk to lenders, but they also come with a higher purchase price and rapid depreciation. Used cars, while generally more affordable upfront, might have slightly higher interest rates, especially for older models, as lenders perceive a greater risk. Carefully consider the total cost of ownership, including insurance, maintenance, and fuel, beyond just the monthly loan payment.

Know Your Credit Score: Your Financial Report Card

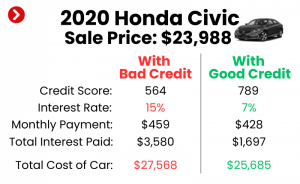

Your credit score is arguably the most significant factor influencing your car loan rates. It’s a three-digit number that tells lenders how risky it is to lend you money. A higher score signifies a lower risk, translating into better interest rates and more favorable loan terms.

Based on my experience, many people skip checking their credit score until they’re already at the dealership, putting them at a significant disadvantage. Knowing your score beforehand allows you to address any inaccuracies or take steps to improve it if needed. You are entitled to a free credit report from each of the three major credit bureaus (Equifax, Experian, TransUnion) once every 12 months. Review these reports for errors and understand your current credit standing.

Calculate Your Ideal Car Budget

Beyond the sticker price of the car, your budget for an auto loan must encompass several elements. This includes your potential down payment, the maximum monthly payments you can comfortably afford, and the overall total cost.

Pro tips from us: Don’t just focus on the monthly payment. A lower monthly payment might seem attractive, but it often comes with a longer loan term, meaning you pay significantly more in total interest. Aim for a down payment of at least 10-20% for a new car and ideally more for a used car. This reduces the amount you need to borrow, lowers your monthly payments, and helps you avoid being "upside down" on your loan, where you owe more than the car is worth. Factor in other costs like insurance premiums, registration fees, and potential maintenance, as these contribute to the real cost of owning a car.

2. The Car Loan Search Begins: Where to Look for Financing

Once your financial groundwork is complete, it’s time to actively start your car loan search. There are several avenues to explore, each with its own advantages and disadvantages. Diversifying your search can lead to more competitive offers and better terms for your auto loan.

Dealership Financing: Convenience at a Cost?

Dealerships often advertise attractive financing options, sometimes even 0% APR deals for well-qualified buyers on new vehicles. They act as intermediaries, working with a network of banks and finance companies to secure a loan for you. This can be incredibly convenient, as you can shop for a car and arrange financing all in one place.

However, convenience can sometimes come at a cost. While dealerships have access to multiple lenders, they might prioritize lenders who offer them the highest commission, not necessarily the lowest car loan rates for you. It’s also harder to separate the car price negotiation from the loan negotiation, which can lead to confusion. Always remember that the dealer is a business, and their primary goal is profit.

Banks and Credit Unions: Traditional Lenders

Traditional financial institutions like banks and credit unions are excellent places to start your independent car loan search. If you have an existing relationship with a bank, they might offer you preferred rates. Credit unions, being non-profit organizations, are often known for offering some of the most competitive auto loan rates due to their member-focused structure.

Applying with banks and credit unions allows you to secure pre-approval, which we’ll discuss shortly. This puts you in a stronger negotiating position at the dealership, as you’ll know your financing terms before you even discuss the car price. It also allows you to focus solely on the car price negotiation, without the added pressure of arranging financing simultaneously.

Online Lenders: Speed, Variety, and Comparison

The digital age has brought a wealth of online lenders specializing in car loans. These platforms offer speed, convenience, and the ability to compare multiple offers from various lenders with just a few clicks. Websites dedicated to car loan search comparison can be incredibly useful tools.

Online lenders often have lower overheads than traditional banks, which can sometimes translate into better rates. They are also excellent for borrowers with less-than-perfect credit, as some specialize in subprime auto loans, although at higher interest rates. The key advantage here is the ability to quickly gather several competitive quotes, giving you leverage in your decision-making process.

3. Decoding the Loan: Key Terms and Factors in Your Car Loan Search

Understanding the terminology associated with auto loans is crucial to making an informed decision. Don’t let confusing jargon deter you; mastering these concepts will empower you during your car loan search.

Annual Percentage Rate (APR): Your True Cost of Borrowing

The Annual Percentage Rate (APR) is arguably the most important number in your car loan search. It represents the total cost of borrowing money for a year, expressed as a percentage. Unlike a simple interest rate, APR includes not only the interest charged but also any additional fees associated with the loan, such as origination fees.

A lower APR means a lower total cost for your loan. Even a difference of one or two percentage points can save you hundreds, if not thousands, of dollars over the life of the loan. When comparing loan offers, always focus on the APR, not just the advertised interest rate, to get an accurate picture of the true cost.

Loan Term: The Duration of Your Payments

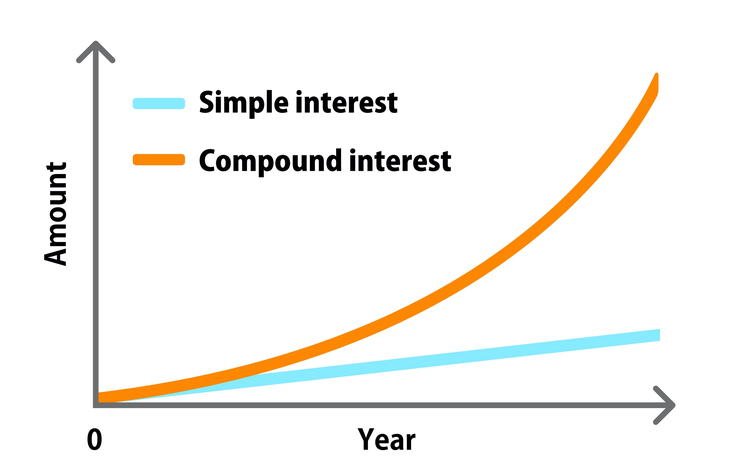

The loan term refers to the length of time you have to repay your auto loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). The loan term directly impacts your monthly payment and the total interest you’ll pay.

A shorter loan term means higher monthly payments but significantly less interest paid over the life of the loan. Conversely, a longer loan term offers lower monthly payments, making the car seem more affordable in the short term, but it results in substantially more interest paid overall. Common mistakes to avoid are focusing solely on monthly payments and extending the loan term unnecessarily. While a 72- or 84-month loan might seem attractive, the amount of interest you accrue can be substantial, and you might end up owing more than the car is worth for a significant portion of the loan.

Down Payment: Your Upfront Investment

A down payment is the initial amount of money you pay towards the purchase of the car, reducing the amount you need to borrow. A larger down payment is always beneficial for several reasons.

Firstly, it lowers your monthly payments. Secondly, it reduces the total interest you’ll pay over the life of the loan. Thirdly, and very importantly, it helps prevent you from being "upside down" on your loan. Cars depreciate rapidly, especially new ones. A substantial down payment ensures you have equity in the vehicle from the start, protecting you if you need to sell the car sooner than expected or if it’s totaled in an accident.

Trade-in Value: Leveraging Your Current Vehicle

If you have an existing vehicle, its trade-in value can significantly impact your new car loan. When you trade in a car, its value is typically applied directly to the purchase price of your new vehicle, effectively acting as a down payment.

Pro tips from us: Always research your car’s trade-in value before going to the dealership. Use online valuation tools like Kelley Blue Book or Edmunds. This knowledge gives you leverage in negotiation. Furthermore, consider selling your old car privately if you’re looking to maximize its value, as private sales often yield more than dealer trade-ins, though they require more effort.

4. The Application Process: Step-by-Step Guidance for Your Car Loan Search

Navigating the application process can seem daunting, but breaking it down into manageable steps makes your car loan search much smoother. This structured approach will increase your chances of securing favorable terms.

Get Pre-Approved: Shop with Confidence

One of the most powerful tools in your car loan search arsenal is pre-approval. This involves applying for a loan with a bank, credit union, or online lender before you visit a dealership. If approved, you’ll receive a conditional loan offer outlining the maximum amount you can borrow, the interest rate (APR), and the loan term.

From my years in the industry, I’ve seen that pre-approval transforms you from a mere shopper into a cash buyer in the eyes of the dealership. You walk in knowing exactly how much financing you have and at what rate. This allows you to negotiate the car’s price separately, without the added pressure of financing. If the dealership can beat your pre-approved rate, fantastic! If not, you have a solid backup.

Gathering Your Documents

When applying for a car loan, lenders will require certain documents to verify your identity, income, and financial stability. Having these ready will expedite the process.

Typically, you’ll need:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2s, or tax returns (especially for self-employed individuals).

- Proof of Residency: Utility bill or lease agreement.

- Social Security Number: For credit checks.

- Vehicle Information: If you’ve already chosen a specific car (VIN, make, model).

Submitting Multiple Applications (Smartly)

During your car loan search, it’s wise to apply to several lenders to compare offers. However, be mindful of how multiple applications can impact your credit score. Each application results in a "hard inquiry" on your credit report, which can temporarily lower your score by a few points.

The good news is that credit bureaus understand consumers shop around for loans. They typically treat multiple hard inquiries for the same type of loan (like an auto loan) within a short period (usually 14-45 days, depending on the scoring model) as a single inquiry. So, aim to submit all your loan applications within a focused window to minimize the impact on your credit score while maximizing your chances of finding the best rates.

Reviewing and Comparing Loan Offers

Once you receive multiple loan offers, it’s time to meticulously compare them. Don’t just look at the monthly payment. Focus on the APR, the total interest paid over the life of the loan, any fees (like origination or prepayment penalties), and the flexibility of the loan terms.

Create a simple spreadsheet if needed to line up each offer side-by-side. Pay close attention to any fine print. Are there any hidden fees? Is there a penalty for paying off the loan early? A thorough comparison ensures you pick the offer that truly aligns with your financial goals.

5. Advanced Strategies for a Smarter Car Loan Search

Beyond the basics, there are several advanced strategies that can further optimize your car loan search and lead to even greater savings. These insights separate the average borrower from the truly savvy car owner.

Refinancing Your Car Loan: A Second Chance at Better Rates

Even if you’ve already secured an auto loan, your car loan search doesn’t have to end. Refinancing your car loan means taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

When should you consider refinancing?

- Your credit score has improved: If you’ve diligently paid your bills and seen your score rise, you might qualify for a much better rate.

- Interest rates have dropped: Market rates fluctuate. If current rates are lower than when you initially financed, refinancing could save you money.

- You want to lower monthly payments: Refinancing can extend your loan term, reducing monthly payments (though potentially increasing total interest).

- You want to shorten the loan term: If your finances have improved, you might want to pay off the loan faster to save on interest.

Refinancing can be a powerful tool for financial optimization, but always calculate the total savings to ensure it’s a worthwhile move after considering any new fees.

Understanding Loan Fees: Beyond the APR

While APR is comprehensive, some fees might be presented separately or buried in the fine print. Being aware of these during your car loan search can prevent unpleasant surprises.

- Origination Fees: A fee charged by the lender for processing the loan.

- Documentation Fees: Charged by dealerships for preparing paperwork.

- Prepayment Penalties: Some loans charge a fee if you pay off the loan early. Always check for this, especially if you plan to make extra payments.

- Late Payment Fees: Standard for missed payments.

Always ask for a complete breakdown of all fees associated with the loan, both from the lender and the dealership.

Guaranteed Asset Protection (GAP) Insurance: Is It Worth It?

GAP insurance is an optional coverage that pays the difference between what you owe on your auto loan and your car’s actual cash value if your vehicle is stolen or totaled. Since cars depreciate quickly, especially new ones, you can easily owe more than the car is worth, leaving you with a financial deficit after an insurance payout.

Pro tips for savvy buyers: While often offered by dealerships, you can typically find GAP insurance from your own auto insurer or other third-party providers at a lower cost. It’s most beneficial if you made a small down payment, financed for a long term (e.g., 72+ months), or bought a car that depreciates rapidly. If you made a large down payment or are financing for a short term, you might not need it.

Cosigners: When to Use One and the Risks Involved

If you have a limited credit history or a low credit score, a lender might require a cosigner to approve your car loan. A cosigner is someone with good credit who agrees to be equally responsible for the loan. If you fail to make payments, the cosigner is legally obligated to pay.

While a cosigner can help you secure a loan and potentially better rates, it’s a significant responsibility for them. Their credit score will be affected by the loan, and any missed payments will harm their credit as well as yours. Only consider a cosigner if both parties fully understand the implications and have a strong, trusting relationship.

6. Common Pitfalls and How to Avoid Them During Your Car Loan Search

Even with the best intentions, it’s easy to fall into common traps during your car loan search. Being aware of these pitfalls is the first step to avoiding them, ensuring a smoother and more financially sound car-buying experience.

Ignoring Your Credit Score: The Cost of Ignorance

As mentioned earlier, your credit score is paramount. A common mistake during a car loan search is neglecting to check your credit score and report before applying for financing. This ignorance can lead to accepting higher interest rates than you deserve or even being denied a loan altogether.

Take the time to pull your reports, dispute any errors, and if possible, work on improving your score for a few months before your car purchase. Even a slight improvement can lead to significant savings on your auto loan.

Not Shopping Around: Settling for the First Offer

Relying solely on dealership financing or the first offer you receive is a surefire way to pay more than you need to. Dealerships often mark up interest rates to increase their profit, and without external offers, you have no leverage.

Pro tips from us: Always get at least three to four loan offers from different sources – banks, credit unions, and online lenders – before finalizing your decision. Use these offers to negotiate for the best possible rate, even with the dealership. Competition works in your favor.

Extending Loan Terms Too Much: The Hidden Cost

The allure of low monthly payments from a very long loan term (e.g., 72 or 84 months) is powerful. However, this is one of the most significant financial traps in the car loan search. While your monthly outlay is smaller, the total interest paid skyrockets.

For instance, on a $25,000 loan at 6% APR, a 60-month term costs about $483/month with total interest of $3,969. An 84-month term drops the payment to $364/month, but the total interest balloons to $5,595 – an extra $1,626! Furthermore, you risk being "upside down" on your loan for a much longer period. Always strive for the shortest loan term you can comfortably afford.

Falling for Unnecessary Add-ons: Inflating Your Loan Amount

When you’re in the finance office at a dealership, you might be presented with a range of add-ons: extended warranties, fabric protection, paint sealant, VIN etching, rust proofing, and even service contracts. While some of these might have value, many are highly profitable for the dealership and can significantly inflate your auto loan amount and, consequently, your interest payments.

Carefully evaluate each add-on. Do you truly need it? Can you get it cheaper elsewhere (e.g., extended warranty from a third party)? Don’t feel pressured to say yes. Remember, these additions increase the total amount you finance, costing you more in interest over time. Focus on the car and the loan first, then consider extras separately.

Conclusion: Your Empowered Car Loan Search Journey

Navigating the world of car loan search can seem daunting, but armed with the comprehensive knowledge shared in this guide, you are now well-equipped to make informed, strategic decisions. From understanding your credit score to comparing car loan rates across various lenders and decoding complex terms like APR and loan terms, every step you take with this knowledge will lead you to a better financial outcome.

Remember, a successful auto loan search isn’t about rushing into the first offer. It’s about diligent preparation, smart comparison shopping, and asking the right questions. By focusing on your financial health, leveraging pre-approval, and understanding the true cost of borrowing, you can avoid common pitfalls and secure financing that aligns perfectly with your budget and goals.

Don’t let the excitement of a new car overshadow the importance of a savvy financial decision. Take control of your car loan search today, apply the strategies outlined here, and drive away with confidence, knowing you’ve secured the best possible deal. Your future self (and your wallet) will thank you.

Further Reading:

- For more insights into managing your credit, check out our article on .

- If you’re still weighing new vs. used, our comprehensive guide on can help.

- For general consumer finance advice and tools, visit the Consumer Financial Protection Bureau (CFPB) website.