The Ultimate Guide to ACU Car Loans: Drive Smarter, Not Harder

The Ultimate Guide to ACU Car Loans: Drive Smarter, Not Harder Carloan.Guidemechanic.com

Buying a car is a significant life event, often marking a new chapter, offering newfound freedom, or simply fulfilling a practical need. For many, securing the right financing is just as crucial as choosing the right vehicle. While traditional banks and dealership financing are common routes, a powerful, often overlooked option exists: the ACU car loan.

An ACU, or Accredited Credit Union, offers a unique and highly beneficial approach to car financing that can save you money, provide personalized service, and simplify the entire process. This comprehensive guide will dive deep into everything you need to know about securing an ACU car loan, exploring its advantages, navigating the application, and equipping you with the knowledge to make an informed decision. Get ready to drive smarter and unlock the best car financing solution for your needs.

The Ultimate Guide to ACU Car Loans: Drive Smarter, Not Harder

What Exactly is an ACU Car Loan? The Credit Union Advantage Explained

Before we delve into the specifics, let’s clarify what an ACU car loan entails. An ACU car loan is simply a vehicle loan provided by a credit union. But what makes a credit union different from a bank, and why does that matter for your car financing?

Credit unions are not-for-profit financial cooperatives owned by their members. Unlike banks, which are typically for-profit entities accountable to shareholders, credit unions operate to serve their members’ financial well-being. This fundamental difference translates into tangible benefits for borrowers, especially when it comes to loans.

Based on my experience in the financial sector, this member-centric approach means credit unions often offer more competitive interest rates and lower fees compared to traditional banks. Their primary goal isn’t to maximize profits but to provide valuable services and return earnings to their members in the form of better rates and fewer charges. This can make a substantial difference over the life of your car loan.

Why Consider an ACU Car Loan? Unpacking the Core Benefits

Choosing an ACU car loan can unlock a range of advantages that might not be available through other lenders. These benefits are rooted in the unique structure and mission of credit unions. Understanding them can help you see why this option deserves serious consideration.

1. Lower Interest Rates

One of the most compelling reasons to opt for an ACU car loan is the potential for lower interest rates. Because credit unions are not-for-profit, they can often pass savings directly to their members. This means your interest rate might be significantly lower than what a bank or dealership could offer.

A lower interest rate translates directly into a lower total cost for your vehicle over the loan term. Even a fraction of a percentage point difference can save you hundreds, or even thousands, of dollars over several years. This is particularly impactful on a large purchase like a car.

2. Flexible Loan Terms and Conditions

Credit unions are known for their flexibility when it comes to loan terms. They often work more closely with individual members to tailor loan structures that fit their specific financial situations. This personalized approach can be a huge advantage.

Whether you need a longer repayment period to lower your monthly payments or a shorter term to minimize interest paid, an ACU is often more willing to discuss and customize options. This flexibility can make car ownership more manageable and affordable for a wider range of budgets.

3. Personalized Member Service

When you’re a member of a credit union, you’re not just a customer; you’re an owner. This ownership translates into a much higher level of personalized service. Credit union staff often know their members by name and genuinely care about their financial success.

Pro tips from us: Don’t hesitate to engage with your credit union’s loan officers. They are often more accessible and willing to explain options, answer questions, and guide you through the process than larger, more impersonal institutions. This personal touch can make a complex financial decision feel much less daunting.

4. Community Focus and Member Benefits

Credit unions are deeply rooted in their communities. They often invest locally and prioritize the financial well-being of their members. This community focus often translates into additional benefits, such as financial education resources, community events, and sometimes even unique member-only perks.

Being part of a credit union means you’re part of a supportive financial ecosystem. This sense of belonging, combined with excellent rates and service, creates a comprehensive value proposition that goes beyond just the loan itself. It’s about building a long-term financial relationship.

The ACU Car Loan Application Process: A Step-by-Step Guide

Securing an ACU car loan involves a few distinct steps, some of which differ slightly from a traditional bank application. Understanding this process can help you prepare thoroughly and increase your chances of approval.

Step 1: Become a Member (If You Aren’t Already)

The first and most crucial step for an ACU car loan is membership. Since credit unions are member-owned, you must be a member to access their services, including loans. Membership eligibility varies by credit union but often includes criteria such as:

- Living, working, or worshipping in a specific geographic area.

- Being employed by a particular company or organization.

- Being related to an existing member.

- Affiliation with certain associations or groups.

Once you meet the eligibility criteria, becoming a member usually involves opening a savings account with a small deposit, often as little as $5 or $25. This simple act unlocks a world of financial services.

Step 2: Get Pre-Approved for Your Loan

One of the smartest moves you can make is to get pre-approved for your ACU car loan before you even step onto a dealership lot. Pre-approval gives you a clear understanding of how much you can borrow, at what interest rate, and under what terms.

Having a pre-approval letter in hand turns you into a cash buyer, giving you significant leverage during price negotiations with dealerships. It allows you to focus solely on the car’s price, rather than getting caught up in the financing details offered by the dealer, which may not be as favorable.

Step 3: Gather Necessary Documentation

When applying for an ACU car loan, you’ll need to provide certain documents to verify your identity, income, and financial standing. While specific requirements can vary, common documents include:

- Proof of Identity: Driver’s license, passport, or state ID.

- Proof of Address: Utility bill, lease agreement, or bank statement.

- Proof of Income: Pay stubs (from the last 1-2 months), W-2 forms, tax returns (for self-employed individuals).

- Employment Verification: Contact information for your employer.

- Vehicle Information (if already chosen): VIN, make, model, mileage.

Common mistakes to avoid are not having all your documents ready, which can delay the application process. Double-check with your credit union for their exact requirements.

Step 4: Submit Your Application

Once you’ve gathered all your documents and know your pre-approval status, you’ll formally submit your ACU car loan application. This can often be done online, over the phone, or in person at a branch.

A loan officer will review your application, credit history, and financial information. They may contact you for additional details or clarification. The goal is to ensure you meet their lending criteria and that the loan is affordable for you.

Step 5: Loan Approval and Funding

Upon approval, you’ll receive a loan offer outlining the interest rate, term, monthly payment, and any other conditions. Carefully review these terms and ask any questions you have before signing.

Once you accept and sign the loan agreement, the funds will be disbursed. If you’re buying from a dealership, the credit union can often send the funds directly to them. If it’s a private sale, the funds might be deposited into your account, or a check can be issued to the seller.

Navigating Eligibility: Who Qualifies for an ACU Car Loan?

While ACUs are known for their flexibility, there are still key eligibility criteria that determine who qualifies for an ACU car loan. Understanding these factors will help you assess your readiness.

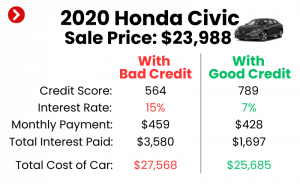

1. Credit Score Considerations

Your credit score plays a significant role in determining your eligibility and the interest rate you’ll receive. While credit unions are often more lenient than traditional banks, a healthier credit score will always lead to better loan terms.

Typically, lenders look for a FICO score in the good-to-excellent range (generally 670 and above) for the most favorable rates. However, credit unions are often willing to work with members who have fair credit (580-669), sometimes offering programs or options that might not be available elsewhere.

2. Debt-to-Income Ratio (DTI)

Lenders assess your ability to repay the loan by looking at your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments.

A general guideline is that lenders prefer a DTI of 36% or lower, though some may go up to 43% or even higher depending on other factors. If your DTI is high, consider paying down existing debts before applying for an ACU car loan.

3. Stable Employment History

A stable employment history demonstrates your ability to generate consistent income, which is crucial for loan repayment. Lenders typically look for at least two years of consistent employment with the same employer or within the same industry.

If you’ve recently changed jobs, be prepared to explain the circumstances. Self-employed individuals will need to provide additional documentation, such as tax returns, to prove consistent income over several years.

4. Vehicle Requirements

The vehicle you intend to purchase also impacts your loan eligibility. Lenders have criteria regarding the age, mileage, and type of car they are willing to finance. These requirements help protect the lender’s investment.

Many ACUs prefer to finance newer vehicles, typically those less than 7-10 years old with under 100,000-125,000 miles. Some may offer specific used car loan programs with different terms. Luxury or specialty vehicles might also have different lending guidelines.

5. Credit Union Membership

As mentioned earlier, active membership in the credit union is non-negotiable. Ensure you meet their specific membership criteria and have established your membership before applying for an ACU car loan. This is often the easiest requirement to fulfill.

Maximizing Your Chances: Tips for ACU Car Loan Approval

Want to boost your likelihood of getting approved for an ACU car loan with the best possible terms? Here are some actionable strategies.

1. Improve Your Credit Score

A higher credit score is your golden ticket to lower interest rates. Before applying, check your credit report for any errors and dispute them. Pay bills on time, reduce credit card balances, and avoid opening new lines of credit.

Based on my experience, even small improvements to your score can translate into significant savings over the life of your loan. For more insights into managing your credit, check out our guide on .

2. Reduce Existing Debt

Lowering your existing debt, especially revolving credit like credit cards, can significantly improve your debt-to-income ratio. This signals to lenders that you have more financial capacity to take on new debt.

Focus on paying down high-interest debts first. Even making extra payments on smaller balances can free up cash flow and improve your financial standing in the eyes of a lender.

3. Save for a Down Payment

A substantial down payment reduces the amount you need to borrow, which can lower your monthly payments and the total interest paid. It also shows the lender that you are financially responsible and have skin in the game.

Aim for at least 10-20% of the car’s purchase price. A larger down payment can also help you secure better loan terms, even if your credit isn’t perfect.

4. Get Pre-Approved (Seriously, Do It!)

We can’t stress this enough. Getting pre-approved empowers you as a buyer. It sets a clear budget, prevents you from overspending, and gives you a powerful negotiation tool at the dealership.

This step also gives you peace of mind, knowing your financing is secured before you commit to a specific vehicle. It transforms the car-buying experience from stressful to exciting.

5. Gather All Documents in Advance

Being organized is key. Have all your identification, income statements, and employment verification ready before you start the application process. This shows preparedness and can expedite the approval process.

Double-checking the credit union’s specific requirements can save you time and prevent delays. A smooth application process is often a sign of a responsible borrower.

ACU Car Loan vs. Traditional Bank Loans: A Comparative Look

When it comes to financing your next vehicle, you essentially have two main institutional choices: an ACU car loan or a loan from a traditional bank. While both provide funding, their underlying structures lead to distinct differences.

| Feature | ACU Car Loan (Credit Union) | Traditional Bank Loan |

|---|---|---|

| Ownership | Member-owned (not-for-profit) | Shareholder-owned (for-profit) |

| Interest Rates | Often lower due to non-profit status | Typically higher, profit-driven |

| Fees | Generally lower or fewer fees | Can have various fees (origination, late, etc.) |

| Customer Service | Personalized, member-centric, relationship-focused | Can be more transactional, less personalized |

| Flexibility | More willing to work with members on loan terms | Stricter, less flexible, standardized terms |

| Eligibility | Requires membership, may be more lenient on credit | No membership required, often stricter credit requirements |

| Community Focus | Strong community ties, local investment | Global/national focus, less local emphasis |

The table highlights a critical distinction: credit unions prioritize their members, leading to potentially better rates and service for an ACU car loan. Banks, by contrast, focus on shareholder returns, which can translate to higher costs for consumers.

Beyond the Initial Loan: Refinancing Your ACU Car Loan

Your financial situation isn’t static, and neither should your car loan be. Refinancing your ACU car loan can be a smart move in certain circumstances, potentially saving you money or adjusting your monthly payments.

When to Consider Refinancing

Refinancing involves taking out a new loan to pay off your existing car loan. You might consider this if:

- Interest Rates Have Dropped: If market rates have fallen since you took out your original loan, you could secure a lower rate.

- Your Credit Score Has Improved: A significantly improved credit score makes you eligible for better terms than when you first financed.

- You Need Lower Monthly Payments: Extending the loan term through refinancing can reduce your monthly outlay, though you might pay more interest overall.

- You Want to Shorten the Loan Term: If your financial situation has improved, you might refinance to a shorter term to pay off the car faster and reduce total interest.

- You Want to Remove a Cosigner: If a cosigner was needed initially, refinancing allows you to remove them once your financial standing is strong.

Pro tips from us: Always calculate the total cost of the new loan, including any fees, before committing to refinancing. Ensure the savings outweigh any potential costs.

Benefits of Refinancing with an ACU

Refinancing your car loan through an ACU offers the same core benefits as an initial ACU car loan: competitive rates, flexible terms, and personalized service. If you initially financed through a dealership or traditional bank, an ACU might be able to offer you a significantly better deal.

The process is similar to applying for a new loan, but instead of buying a car, you’re buying out your old loan. Gather your current loan details, financial documents, and apply to your ACU.

Common Pitfalls to Avoid When Securing an ACU Car Loan

Even with the advantages of an ACU car loan, there are still common mistakes that borrowers make. Being aware of these can help you navigate the process smoothly and avoid unnecessary headaches or costs.

1. Not Getting Pre-Approved

As emphasized earlier, skipping pre-approval is a significant misstep. Without it, you lack a firm budget and a strong negotiating position, making you vulnerable to less favorable financing offers from dealerships.

Common mistakes to avoid are letting the dealership handle all the financing. Always come prepared with your own financing options from an ACU or another lender.

2. Ignoring Your Credit Score

Your credit score is a powerful tool. Neglecting to check it, understand it, or work on improving it before applying for an ACU car loan can cost you significantly in higher interest rates.

Make a habit of regularly checking your credit report (you’re entitled to a free one annually from each of the three major bureaus). Address any inaccuracies promptly.

3. Focusing Only on the Monthly Payment

While the monthly payment is important, it shouldn’t be your sole focus. A low monthly payment might sound appealing, but it can often hide a longer loan term, a higher interest rate, or both, leading to paying much more over time.

Always consider the total cost of the loan, including the interest paid over the entire term. Sometimes, a slightly higher monthly payment for a shorter term can save you thousands.

4. Not Understanding All Loan Terms

Before signing any loan agreement, read every single line. Understand the interest rate, loan term, any fees (origination, late payment, early payoff penalties), and what happens if you miss a payment.

If anything is unclear, ask your ACU loan officer for clarification. A reputable credit union will be happy to explain every detail until you are comfortable. For a deeper understanding of consumer financial protection and best practices, resources like the Consumer Financial Protection Bureau (CFPB) provide invaluable information. You can learn more at .

Real-World Scenarios: Who Benefits Most from an ACU Car Loan?

While ACU car loans offer broad appeal, certain individuals and situations particularly stand to gain.

First-Time Car Buyers

For those embarking on their first car purchase, the personalized guidance and often more forgiving approach of an ACU can be incredibly valuable. They can help navigate the complexities of financing without overwhelming a new borrower.

The educational resources and attentive service can build confidence and set a strong foundation for future financial decisions.

Individuals with Good but Not Excellent Credit

If your credit score is good but not quite in the "excellent" tier, an ACU might offer more competitive rates than a traditional bank. Their member-focused model often means they’re willing to look beyond just a score and consider your overall financial picture and relationship with the credit union.

This can be a crucial difference in securing an affordable loan when other lenders might be less flexible.

Community-Minded Individuals

If you value supporting local institutions and prefer a financial relationship built on trust and mutual benefit, an ACU car loan aligns perfectly with those values. You’re investing in an organization that invests back into your community.

It’s a choice that feels good, knowing your financial transactions contribute to local well-being rather than distant corporate profits.

People Seeking Personalized Service

Tired of feeling like just another number? An ACU’s commitment to personalized service makes a real difference. Whether you have questions about the application, need help understanding terms, or face unexpected financial challenges, you’ll often find a more supportive and responsive team.

This human touch can significantly enhance your car buying and ownership experience.

If you’re still weighing your options between new and used vehicles, our article offers a detailed comparison to help you make an informed decision before finalizing your loan.

Conclusion: Drive Confidently with an ACU Car Loan

Navigating the world of car financing can be complex, but an ACU car loan stands out as a genuinely advantageous option for many. From competitive interest rates and flexible terms to unparalleled personalized service and a community-centric approach, credit unions offer a compelling alternative to traditional lenders.

By understanding the unique benefits, preparing for the application process, and avoiding common pitfalls, you can position yourself to secure a fantastic deal on your next vehicle. Remember, getting pre-approved and focusing on your overall financial health are key steps to unlocking the best possible terms.

Don’t just get a car loan; get a smarter car loan. Explore the ACU car loan options available to you, become a member of a credit union, and drive away with confidence, knowing you’ve made a financially savvy choice. Your journey to car ownership doesn’t have to be stressful; with an ACU, it can be a smooth, supportive, and ultimately rewarding experience.