The Ultimate Guide to Bancorpsouth Car Loans: Navigating Your Path to Vehicle Ownership

The Ultimate Guide to Bancorpsouth Car Loans: Navigating Your Path to Vehicle Ownership Carloan.Guidemechanic.com

The open road calls, and for many, the dream of a new or reliable used vehicle is a powerful one. However, turning that dream into a reality often involves navigating the complex world of auto financing. When considering a significant investment like a car, choosing the right financial partner is paramount. This is where institutions like Bancorpsouth (now part of Cadence Bank) come into play, offering tailored solutions to help you get behind the wheel.

Securing a car loan is more than just getting approved; it’s about finding terms that align with your financial health and future goals. This comprehensive guide will meticulously explore everything you need to know about Bancorpsouth car loans, from the types of financing available to the intricacies of the application process, common pitfalls, and expert strategies for securing the best deal. Our goal is to empower you with the knowledge to make an informed, confident decision, ensuring your journey to vehicle ownership is as smooth as possible.

The Ultimate Guide to Bancorpsouth Car Loans: Navigating Your Path to Vehicle Ownership

Understanding Bancorpsouth (Cadence Bank): A Trusted Financial Partner

Before diving into the specifics of car loans, it’s crucial to understand the institution behind them. Bancorpsouth, a well-established regional bank, merged with Cadence Bank in 2021, operating under the Cadence Bank name. This merger created a larger, more robust financial entity with a strong presence across the southeastern United States. Their long-standing commitment to local communities and personalized service has made them a trusted name in banking.

Choosing a reputable financial institution for your auto loan provides a significant advantage. Based on my experience, working with established banks like Bancorpsouth (Cadence Bank) offers a level of security, transparency, and customer support that might not always be present with smaller or less-regulated lenders. Their history of serving individuals and businesses means they understand the local economic landscape and can often provide more personalized solutions. This foundational trust is a critical component when embarking on a major financial commitment like a car loan.

Bancorpsouth Car Loans: What Financing Options Do They Offer?

Bancorpsouth (Cadence Bank) typically offers a range of auto financing options designed to meet diverse needs, whether you’re buying new, used, or looking to refinance an existing loan. Understanding these options is the first step toward finding the perfect fit for your situation.

New Car Loans

For those eyeing a brand-new vehicle, Bancorpsouth provides financing solutions specifically for new car purchases. These loans usually come with competitive interest rates due to the vehicle’s inherent value and lower risk profile. New car loans often feature flexible terms, allowing you to choose a repayment schedule that fits your budget.

When considering a new car loan, it’s important to remember that the vehicle depreciates rapidly from the moment it leaves the lot. While new car loans often have lower interest rates, the total loan amount is typically higher, leading to larger monthly payments. Carefully evaluate your budget and the long-term cost before committing to a new car purchase.

Used Car Loans

Purchasing a used car can be a smart financial move, offering excellent value and often lower insurance costs. Bancorpsouth also extends financing for pre-owned vehicles, catering to individuals looking for more budget-friendly options. The terms and conditions for used car loans can vary slightly compared to new car loans, primarily due to factors like the vehicle’s age and mileage.

When applying for a used car loan, lenders will often consider the age and mileage of the vehicle you intend to purchase. Older or higher-mileage vehicles might be subject to different lending criteria or slightly higher interest rates due to perceived higher risk. It’s always a good practice to have the used car thoroughly inspected before finalizing any financing.

Auto Loan Refinancing

Perhaps you already have a car loan but are looking for better terms. Auto loan refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable monthly payments. This can be an excellent strategy to save money over the life of the loan or to adjust your monthly budget.

Refinancing makes sense if your credit score has improved since you first took out the loan, or if market interest rates have dropped. It can also be beneficial if you need to lower your monthly payments by extending the loan term, though this will likely increase the total interest paid over time. Bancorpsouth offers refinancing options, providing an opportunity to reassess your current auto loan and potentially improve your financial situation.

The Bancorpsouth Car Loan Application Process: A Step-by-Step Guide

Navigating the application process for a car loan can seem daunting, but breaking it down into manageable steps makes it much clearer. Bancorpsouth (Cadence Bank) strives to make this process as straightforward as possible.

The Power of Pre-Approval

One of the most valuable steps you can take is getting pre-approved for a car loan. Pre-approval means the bank has conditionally agreed to lend you a certain amount of money at a specific interest rate, based on your creditworthiness. This is a game-changer when you’re shopping for a vehicle.

Pro tips from us: Always get pre-approved before stepping onto the dealership lot. This gives you a clear budget, transforms you into a cash buyer, and significantly strengthens your negotiation position. You’ll know exactly how much you can afford, and you won’t be swayed by dealer-offered financing that might not be in your best interest.

Required Documentation for Your Application

To ensure a smooth application, gathering all necessary documents beforehand is crucial. While requirements can vary slightly, common items Bancorpsouth will request include:

- Proof of Identity: A valid government-issued ID, such as a driver’s license or passport. This verifies who you are.

- Proof of Income: Recent pay stubs (typically two to three months), W-2 forms, or tax returns if you are self-employed. Lenders need to confirm your ability to repay the loan.

- Proof of Residency: Utility bills, a lease agreement, or mortgage statements to confirm your address.

- Social Security Number: Essential for a credit check.

- Vehicle Information (if applicable): For a specific car, you’ll need details like the VIN, make, model, and mileage. For refinancing, your current loan statements will be required.

Having these documents ready will expedite the application process and demonstrate your preparedness to the lender.

Online vs. In-Branch Application

Bancorpsouth (Cadence Bank) typically offers both online and in-branch application options, providing flexibility for applicants.

- Online Application: This method offers convenience, allowing you to apply from anywhere at any time. It’s often quicker for initial submission and pre-approvals. However, it might lack the personalized interaction of an in-person visit.

- In-Branch Application: Visiting a branch allows you to speak directly with a loan officer. This can be beneficial if you have complex questions, need personalized advice, or prefer face-to-face interaction. The loan officer can guide you through the paperwork and clarify any terms.

Choose the method that best suits your comfort level and schedule. Both routes lead to the same goal: securing your Bancorpsouth car loan.

Key Factors Influencing Your Bancorpsouth Car Loan

Several critical elements weigh heavily on whether your loan application is approved and what interest rate you receive. Understanding these factors will help you prepare and optimize your chances for favorable terms.

The Indispensable Role of Your Credit Score

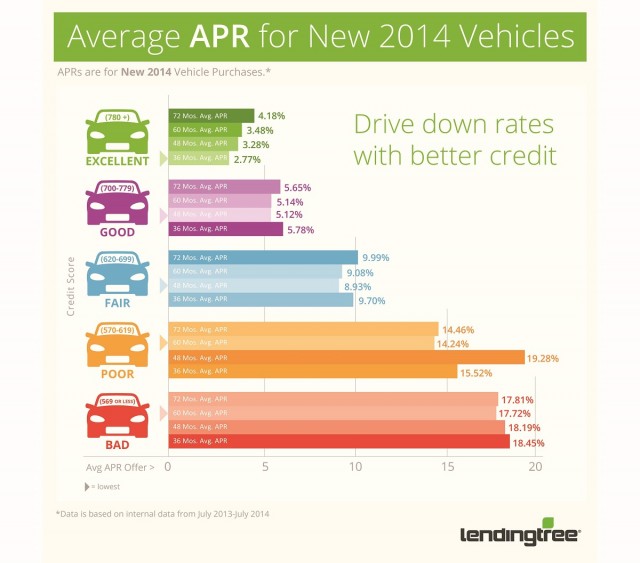

Your credit score is arguably the most significant factor in securing an auto loan and determining your interest rate. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repayment. Lenders use it to assess the risk of lending to you.

Generally, higher credit scores (e.g., 700+) indicate a lower risk and typically qualify you for the best interest rates. Scores in the mid-range (600s) might still get approved but at higher rates, while lower scores (below 600) could face challenges or significantly higher rates. Bancorpsouth, like other lenders, will perform a hard inquiry on your credit report during the application process.

Your Debt-to-Income Ratio (DTI)

Another crucial metric lenders evaluate is your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. For example, if your total monthly debt (rent/mortgage, credit card payments, student loans) is $1,500 and your gross monthly income is $4,000, your DTI is 37.5% ($1,500 / $4,000).

Lenders prefer a lower DTI, as it suggests you have ample income to manage additional debt, like a car loan. While there’s no universal cutoff, many lenders prefer a DTI of 36% or lower, though some might go up to 43-50% depending on other factors. A high DTI can signal that you’re already overextended, potentially impacting your loan approval.

The Impact of Loan Term

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). The loan term directly influences your monthly payment and the total interest you’ll pay over the life of the loan.

- Shorter Terms: Result in higher monthly payments but lower total interest paid because you’re paying off the principal faster. This is generally the most cost-effective option if you can afford the higher payments.

- Longer Terms: Lead to lower monthly payments, making the loan seem more affordable in the short term. However, you’ll pay significantly more in total interest over the life of the loan, and you run the risk of owing more on the car than it’s worth (being "upside down" or "underwater") as it depreciates.

Carefully consider the trade-off between monthly affordability and the total cost of the loan when selecting a term.

The Advantage of a Down Payment

Making a down payment means paying a portion of the car’s purchase price upfront. While not always mandatory, a down payment can significantly improve your loan terms and overall financial position.

A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay. It also signals to the lender that you are committed to the purchase, potentially leading to better interest rates. Furthermore, a substantial down payment helps prevent you from being underwater on your loan, especially with a new car’s rapid depreciation.

Vehicle Specifics

The car itself plays a role in the loan decision. Lenders consider the age, mileage, make, and model of the vehicle.

New cars generally qualify for better rates due to their higher value and lower risk of mechanical issues. Used cars are assessed based on their current market value, condition, and expected lifespan. Very old or high-mileage vehicles might be harder to finance or come with higher interest rates, as their resale value and reliability are lower.

Understanding Bancorpsouth Car Loan Interest Rates and Fees

A thorough understanding of interest rates and any associated fees is crucial for comparing loan offers and truly knowing the cost of your Bancorpsouth car loan.

APR vs. Interest Rate: Knowing the Difference

While often used interchangeably, the interest rate and Annual Percentage Rate (APR) are distinct and important.

- Interest Rate: This is the percentage charged by the lender for borrowing the principal amount. It represents the cost of borrowing before any additional fees are factored in.

- Annual Percentage Rate (APR): The APR is a broader measure of the total cost of borrowing, expressed as a yearly percentage. It includes the interest rate plus any additional fees, such as origination fees or administrative costs, that are part of the loan. Therefore, the APR provides a more accurate picture of the true cost of your loan. Always compare APRs when evaluating different loan offers.

For a deeper dive into how interest rates are calculated and how they impact your loan, you might find our article on particularly helpful.

Factors Affecting Your Rate

Your interest rate is not arbitrarily set; it’s influenced by several key factors:

- Credit Score: As mentioned, a higher credit score typically leads to a lower interest rate, as you’re deemed a lower risk.

- Loan Term: Shorter loan terms often come with slightly lower interest rates because the lender’s money is tied up for less time.

- Market Conditions: General economic conditions and the Federal Reserve’s interest rate policies can influence prevailing auto loan rates across the board.

- Lender’s Policies: Each lender has its own risk assessment models and pricing strategies, leading to variations in rates.

Potential Fees to Be Aware Of

While auto loans are generally straightforward, it’s always wise to inquire about any potential fees. Bancorpsouth aims for transparency, but common fees associated with auto loans (though not always present with all lenders) can include:

- Origination Fees: A fee charged by the lender for processing the loan.

- Late Payment Fees: Penalties incurred if you miss a payment deadline.

- Prepayment Penalties: Very rare in auto loans, but some loans might charge a fee if you pay off the loan early. Always confirm if your loan has this clause.

Always read your loan agreement carefully and ask your Bancorpsouth loan officer about any fees you don’t understand.

Common Mistakes to Avoid When Applying for a Car Loan

Based on my experience, many individuals make preventable mistakes that can cost them money or even lead to loan denial. Being aware of these common pitfalls can help you navigate the process more effectively.

Not Checking Your Credit Report Beforehand

One of the biggest oversights is not reviewing your credit report before applying. Your credit report may contain errors that negatively impact your score. Discovering these issues after a loan denial is too late.

Proactively obtain your free credit reports from all three major bureaus (Experian, Equifax, TransUnion) well in advance. Correct any inaccuracies to ensure your credit score accurately reflects your financial history.

Skipping the Pre-Approval Step

As highlighted earlier, forgoing pre-approval means you’re going into a dealership without a clear budget or external financing offer. This leaves you vulnerable to potentially higher dealer-arranged interest rates and puts you at a disadvantage during price negotiations.

Always secure pre-approval from Bancorpsouth or another lender first. It empowers you and gives you a benchmark for comparison.

Focusing Only on the Monthly Payment

While a comfortable monthly payment is important, fixating solely on it can be a costly mistake. Dealerships might try to stretch out the loan term to lower the monthly payment, which often results in paying significantly more in total interest over the life of the loan.

Always look at the total cost of the loan, including the principal, interest, and any fees. A lower monthly payment isn’t always the cheapest option in the long run.

Not Shopping Around for Rates

Assuming the first offer you receive is the best one is a common error. Different lenders have different criteria and rates. Even a half-percentage point difference can save you hundreds, if not thousands, of dollars over the life of a loan.

Common mistakes to avoid are signing without fully understanding the terms or comparing offers. Take the time to get quotes from multiple lenders, including Bancorpsouth, credit unions, and other banks.

Ignoring the Total Cost of the Loan

Beyond the monthly payment and interest rate, consider all associated costs. This includes the car’s purchase price, sales tax, registration fees, and any add-ons like extended warranties or GAP insurance.

Factor these into your overall budget. While some add-ons can be beneficial, others might be overpriced or unnecessary, increasing your total loan amount and interest.

Pro Tips for Securing the Best Bancorpsouth Car Loan

To truly maximize your chances of getting the most favorable terms on your Bancorpsouth car loan, consider these expert strategies.

Improve Your Credit Score

If you’re not in a rush, take steps to boost your credit score before applying. Pay down existing debts, make all payments on time, and avoid opening new credit accounts. Even a small improvement in your score can lead to a better interest rate and significant savings.

Save for a Larger Down Payment

The more you can put down upfront, the less you’ll need to borrow. A substantial down payment not only reduces your monthly payments and total interest but also makes you a more attractive borrower to Bancorpsouth. Aim for at least 10-20% of the vehicle’s purchase price if possible.

Gather All Documents Beforehand

Being organized saves time and stress. Have all your identification, income verification, and residency proofs readily available when you apply. This demonstrates preparedness and can speed up the approval process.

Know Your Budget Inside and Out

Before you even start looking at cars or applying for loans, meticulously review your personal budget. Determine how much you can comfortably afford for a monthly car payment, factoring in insurance, fuel, and maintenance costs. Don’t let a lender or dealership convince you to exceed your financial comfort zone.

Negotiate Effectively

If you’re buying from a dealership, remember that both the car’s price and the loan terms are often negotiable. With your Bancorpsouth pre-approval in hand, you have leverage. Focus on negotiating the car’s purchase price separately from the financing to avoid confusion and ensure you’re getting the best deal on both fronts.

For general banking information and to learn more about Cadence Bank’s services, you can visit their official website: https://cadencebank.com/

Beyond Bancorpsouth: What to Consider

While Bancorpsouth (Cadence Bank) is a strong contender for your auto financing needs, it’s always prudent to explore your options. This approach ensures you’re truly getting the best deal for your specific circumstances.

Credit unions, for instance, are known for often offering very competitive interest rates, as they are member-owned and not-for-profit. Online lenders also provide a convenient way to compare multiple offers quickly, often with streamlined application processes. Dealership financing can be convenient, but always compare their offers to your pre-approval to ensure you’re not paying more.

Ultimately, the best car loan is one that fits your budget, has favorable terms, and comes from a lender you trust. For more general advice on navigating the car acquisition process, you might find our article on insightful.

Conclusion: Your Smart Path to Vehicle Ownership with Bancorpsouth

Securing a car loan is a significant financial decision that impacts your budget for years to come. By understanding the offerings, process, and key factors involved with Bancorpsouth (Cadence Bank) car loans, you’re well-equipped to make an informed choice. From new and used car financing to refinancing options, Bancorpsouth provides a range of solutions backed by a commitment to customer service and community trust.

Remember, preparation is key. Getting pre-approved, understanding your credit score, knowing your budget, and diligently comparing offers are all vital steps toward securing the most favorable terms. By avoiding common mistakes and leveraging our expert tips, you can confidently navigate the world of auto financing and drive away with a car loan that truly works for you. Your journey to vehicle ownership should be exciting, not stressful, and with the right financial partner, it absolutely can be.