The Ultimate Guide to Car Loan Credit Requirements: Navigating Your Path to Automotive Ownership

The Ultimate Guide to Car Loan Credit Requirements: Navigating Your Path to Automotive Ownership Carloan.Guidemechanic.com

Securing a car loan is a significant step towards automotive freedom, but for many, the path to approval feels shrouded in mystery. At the heart of this process lies your credit, a crucial factor that dictates not only whether you’ll get approved but also the terms of your loan, including that all-important interest rate. Understanding the credit required for a car loan is not just about knowing a magic number; it’s about comprehending a complex interplay of financial health indicators that lenders scrutinize.

This comprehensive guide will demystify the credit requirements for car loans, providing you with an in-depth understanding of what lenders look for, how your credit impacts your loan, and actionable strategies to improve your chances of approval. Whether you boast an excellent credit history, are navigating the waters with fair credit, or are starting from scratch, this article is your definitive resource for securing the best possible car loan.

The Ultimate Guide to Car Loan Credit Requirements: Navigating Your Path to Automotive Ownership

Understanding the Foundation: What is a Credit Score and Why Does it Matter for Car Loans?

Before diving into specific score ranges, it’s essential to grasp what a credit score represents. Essentially, it’s a three-digit number, primarily generated by models like FICO or VantageScore, that encapsulates your creditworthiness. This number provides lenders with a snapshot of your financial reliability, indicating how likely you are to repay borrowed money based on your past borrowing behavior.

For car loans, your credit score is the primary gatekeeper. Lenders use it as their initial assessment tool to gauge the risk involved in lending to you. A higher score signals lower risk, potentially unlocking more favorable interest rates and terms. Conversely, a lower score suggests a higher risk, often leading to less attractive offers or even denial.

Based on my experience, many people underestimate the profound impact a few points on their credit score can have over the life of a car loan. Even a seemingly small difference in your interest rate can translate into thousands of dollars in extra payments over several years. Therefore, knowing your score and understanding its implications is the first critical step.

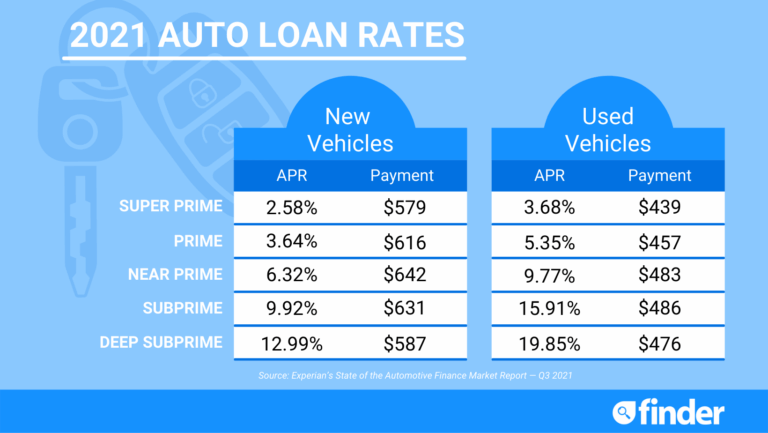

The Credit Score Spectrum: What’s Considered "Good," "Average," and "Poor" for a Car Loan?

The range of credit scores typically spans from 300 to 850, with different tiers signaling varying levels of creditworthiness. While there isn’t a universally "required" minimum score for a car loan, lenders generally categorize scores to determine eligibility and pricing.

Let’s break down what each tier typically means for your car loan prospects:

Excellent Credit (780-850)

Borrowers in this tier are considered prime candidates for car loans. With an excellent credit score, you represent the lowest risk to lenders, making you eligible for the most competitive interest rates and the most flexible loan terms. Approval is generally swift and straightforward.

Lenders will actively compete for your business, often leading to multiple favorable offers. This allows you to shop around and choose the deal that best suits your financial situation, maximizing savings on interest over the loan term. You’ll likely encounter minimal resistance in getting approved for the car of your choice, assuming other factors like income are also strong.

Good Credit (670-739)

Having a good credit score puts you in a strong position to secure a car loan with very good rates. While perhaps not the absolute lowest rates available to those with excellent credit, you’ll still be offered attractive terms that are significantly better than what individuals with lower scores receive.

Lenders view borrowers in this range as reliable, indicating a history of responsible credit management. You should expect a relatively smooth application process and access to a wide range of financing options from various lenders. This score range often serves as a comfortable benchmark for many mainstream lenders.

Fair/Average Credit (580-669)

If your credit score falls into the fair or average category, getting a car loan is still very much possible, but you might face slightly higher interest rates compared to those with good or excellent credit. Lenders perceive a moderate level of risk, meaning they might impose stricter conditions or require a larger down payment.

You might need to work a bit harder to find the best deal, as some prime lenders might offer less favorable terms or require additional documentation. However, many reputable lenders specialize in working with borrowers in this range. Pro tips from us: Don’t settle for the first offer; shop around diligently and consider securing pre-approval.

Poor/Bad Credit (300-579)

Securing a car loan with poor or bad credit presents the most significant challenge. Lenders consider borrowers in this category to be high-risk, which translates into much higher interest rates, often referred to as subprime loans. While approval is tougher, it is by no means impossible.

You’ll likely need to seek out lenders who specialize in subprime auto loans, or "bad credit car loans." These lenders are willing to take on higher risk but compensate for it by charging substantially higher interest rates and sometimes requiring a significant down payment or a co-signer. Common mistakes to avoid are jumping at the first offer without understanding the full cost or falling prey to predatory lending practices.

No Credit History

This category is unique because it doesn’t necessarily indicate "bad" credit, but rather a lack of a track record. Lenders have no history to assess your repayment behavior, making you an unknown risk. This can be as challenging as having poor credit, especially for young adults or new immigrants.

Strategies for those with no credit often involve securing a co-signer with good credit, making a substantial down payment, or exploring "first-time buyer" programs offered by some dealerships or credit unions. Some lenders also offer specific programs designed to help individuals establish credit while financing a vehicle.

Beyond the Score: Other Critical Factors Lenders Consider

While your credit score is undeniably a cornerstone of the car loan application, it’s not the only factor lenders evaluate. A holistic assessment of your financial situation ensures they have a complete picture of your ability and willingness to repay the loan.

Here are other critical elements that influence your car loan approval and terms:

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a lower DTI, typically below 43%, as it indicates you have sufficient income to manage additional debt. A high DTI suggests you might be overextended, making you a higher risk.

- Payment History: Even with a good score, a recent history of missed payments on other loans or credit cards can be a red flag. Lenders want to see consistent, on-time payments, as this is the most significant indicator of future repayment reliability.

- Credit Utilization: This refers to the amount of credit you’re currently using compared to your total available credit. High utilization (e.g., maxing out credit cards) suggests financial strain and can negatively impact your credit score and loan approval chances. Aim to keep this below 30%.

- Length of Credit History: A longer credit history, especially one filled with positive repayment behavior, generally bodes well for loan applications. It provides lenders with more data points to assess your long-term reliability.

- Credit Mix: Having a diverse mix of credit accounts, such as a credit card (revolving credit) and an installment loan (like a student loan or personal loan), can positively impact your score. It shows you can responsibly manage different types of credit.

- Recent Credit Inquiries: While checking your own credit (a "soft inquiry") doesn’t hurt your score, applying for multiple lines of credit within a short period (a "hard inquiry") can temporarily ding it. Too many hard inquiries can signal to lenders that you’re desperate for credit, which is a risk factor.

- Down Payment: A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also demonstrates your financial commitment and can significantly improve your chances of approval, especially with less-than-perfect credit.

- Vehicle Age/Type: Lenders often view newer vehicles as less risky because they retain their value better and are less prone to immediate mechanical issues. Older, high-mileage vehicles might be harder to finance or come with higher interest rates.

Pro tips from us: Don’t just focus on the score; meticulously review all these factors. Addressing any weaknesses in these areas can dramatically improve your loan prospects, even if your score isn’t perfect.

Navigating the Challenges: Car Loans with Less-Than-Perfect Credit

For those with fair, poor, or no credit, securing a car loan can feel like an uphill battle. However, it’s a battle that can be won with the right strategies and realistic expectations.

Subprime Lenders and Their Offerings

When prime lenders (banks, credit unions) are hesitant, subprime lenders step in. These institutions specialize in lending to individuals with lower credit scores. While they offer a lifeline, it comes at a cost. You should expect significantly higher Annual Percentage Rates (APRs), often in the double digits, reflecting the increased risk they undertake.

Loan terms might also be shorter, leading to higher monthly payments, or conversely, stretched out to make payments seem more affordable, but ultimately costing you more in interest over time. It’s crucial to thoroughly read and understand all terms and conditions before committing.

The Role of a Co-signer

If your credit is weak or nonexistent, a co-signer can be a game-changer. A co-signer, typically someone with excellent credit, agrees to be equally responsible for the loan if you default. This reduces the lender’s risk, making them more likely to approve your application and offer better terms.

However, the decision to ask someone to co-sign should not be taken lightly. It carries significant risk for the co-signer, as their credit will be negatively impacted if you miss payments. It’s a commitment that requires open communication and mutual trust.

"Buy Here, Pay Here" Dealerships

These dealerships offer in-house financing, meaning they are both the seller and the lender. They often cater specifically to individuals with bad credit or no credit, as they don’t rely on traditional credit scores for approval. While this offers accessibility, it often comes with very high interest rates and limited vehicle choices.

Based on my observations working with countless individuals, "buy here, pay here" dealerships should generally be considered a last resort. Always compare their offers to other financing options, as the total cost of the vehicle can be substantially higher.

Strategies to Improve Your Chances and Secure Better Terms

Even if your credit isn’t where you want it to be, there are proactive steps you can take to enhance your eligibility and secure more favorable car loan terms.

- Check Your Credit Report Regularly: Start by knowing exactly where you stand. Obtain copies of your credit reports from all three major bureaus (Experian, Equifax, TransUnion). You can get a free copy annually from each bureau through AnnualCreditReport.com. This is a critical first step.

- Dispute Any Errors: Mistakes on your credit report are surprisingly common. Carefully review each account for inaccuracies, fraudulent activity, or outdated information. Disputing errors can quickly boost your score.

- Pay Bills On Time, Every Time: Payment history is the most impactful factor in your credit score. Make sure all your credit card bills, utility payments, and existing loan payments are made on or before their due dates. Even one missed payment can significantly hurt your score.

- Reduce Existing Debt: Lowering your credit utilization ratio by paying down credit card balances can positively impact your score. A lower debt burden also improves your debt-to-income ratio, making you more attractive to lenders.

- Make a Larger Down Payment: This is one of the most effective strategies, especially if your credit is less than perfect. A substantial down payment reduces the loan amount, thereby decreasing the lender’s risk and potentially lowering your interest rate.

- Get Pre-Approved: Before you even step into a dealership, understanding the ins and outs of car loan pre-approval can save you significant money. Read our article: The Ultimate Guide to Car Loan Pre-Approval. Pre-approval gives you a concrete loan offer, allowing you to negotiate with dealerships from a position of strength and compare rates.

- Consider a Co-signer (Wisely): If your credit is truly weak, a co-signer can be a viable option. Just ensure both parties fully understand the responsibilities and risks involved.

- Build Your Credit Over Time: For a deeper dive into improving your credit, check out our guide on How to Boost Your Credit Score Fast. This is a long-term strategy, but every positive action builds your financial foundation.

- Save for a Larger Down Payment: Directly impacts loan terms. The more you put down upfront, the less you need to borrow, which often leads to better interest rates and lower monthly payments.

The Application Process: What to Expect

Once you’ve prepared your credit and explored your options, the car loan application process itself is fairly standardized.

You’ll typically fill out an application form, providing personal and financial information. Lenders will require documents such as proof of income (pay stubs, tax returns), proof of residence (utility bills), and identification (driver’s license). They will then pull your credit report and evaluate your overall financial profile.

Upon approval, you’ll receive a loan offer outlining the Annual Percentage Rate (APR), the loan term (number of months), and the total loan amount. It’s crucial to understand every detail, especially the APR, which represents the true annual cost of borrowing. Don’t hesitate to negotiate for better terms or explore other offers if you feel the initial one isn’t competitive.

Real-World Scenarios and Expert Advice

To illustrate the impact of credit, consider two hypothetical borrowers:

-

Scenario A: Excellent Credit (750 FICO)

- Loan Amount: $25,000

- Loan Term: 60 months

- Interest Rate: 4.5% APR

- Monthly Payment: ~$466

- Total Interest Paid: ~$2,960

-

Scenario B: Fair Credit (620 FICO)

- Loan Amount: $25,000

- Loan Term: 60 months

- Interest Rate: 10.5% APR

- Monthly Payment: ~$537

- Total Interest Paid: ~$7,220

As you can see, the difference in interest rates between excellent and fair credit can result in thousands of dollars in additional costs over the life of the loan. This vividly demonstrates why understanding the credit required for a car loan and actively working to improve it is so vital.

Based on my observations working with countless individuals, the biggest mistake people make is not doing their homework before stepping onto the dealership lot. Knowledge is power in car buying. By understanding your credit, getting pre-approved, and being prepared, you position yourself for success.

Conclusion: Your Credit is Your Key to the Open Road

Navigating the world of car loans can seem daunting, but by understanding the pivotal role your credit plays, you can approach the process with confidence and clarity. The credit required for a car loan isn’t a fixed barrier but rather a dynamic indicator that reflects your financial responsibility and influences every aspect of your loan terms.

Whether you’re aiming for the lowest possible interest rate with excellent credit or strategizing to secure a loan with a less-than-perfect score, proactive steps are key. By monitoring your credit, addressing any issues, making a solid down payment, and exploring all your financing options, you empower yourself to make informed decisions. Remember, a car loan is a significant financial commitment, and understanding its intricacies will not only save you money but also set you on a path to a healthier financial future. Drive smart, not just hard.