The Ultimate Guide to Car Loan Terms: How Many Months Are Car Loans & What’s Best For You?

The Ultimate Guide to Car Loan Terms: How Many Months Are Car Loans & What’s Best For You? Carloan.Guidemechanic.com

Buying a new car is an exciting milestone, often accompanied by the equally significant decision of how to finance it. For most, this means taking out a car loan. While the monthly payment often grabs the spotlight, a crucial factor that impacts everything from total cost to long-term financial health is the loan’s duration—or, how many months are car loans typically structured for?

Understanding car loan lengths is more than just knowing a number; it’s about making an informed financial decision that aligns with your budget and goals. In this comprehensive guide, we’ll dive deep into the world of car loan terms, exploring common durations, their pros and cons, and helping you determine the best fit for your unique situation. Let’s demystify the numbers and empower you to drive off with confidence!

The Ultimate Guide to Car Loan Terms: How Many Months Are Car Loans & What’s Best For You?

Standard Car Loan Lengths: The Industry Norms

When you walk into a dealership or apply for a loan, you’ll quickly notice that car loan terms usually come in standard increments. These durations have become the industry norm because they strike a balance between affordability for lenders and manageable payments for borrowers. Knowing these common lengths is your first step in understanding the landscape.

Based on my extensive experience in automotive financing, the vast majority of car loans fall within a specific range. You’ll most frequently encounter terms of 36, 48, 60, and 72 months. These periods have been the backbone of auto financing for decades, offering various payment structures to suit different budgets.

A 36-month loan means you’ll be making payments for three years, while a 72-month loan extends that commitment to six years. Each increment represents a significant difference in both your monthly outlay and the total interest you’ll pay over the life of the loan.

In recent years, particularly with rising car prices, longer terms have become increasingly prevalent. It’s now not uncommon to see 84-month (seven-year) and even 96-month (eight-year) car loans being offered. While these extended terms might seem appealing due to their lower monthly payments, they come with a distinct set of financial implications that every borrower should thoroughly understand.

The Trade-Offs: Shorter vs. Longer Loan Terms

Choosing a car loan length isn’t about finding a universally "best" option. Instead, it’s about balancing your immediate financial comfort with your long-term monetary goals. Every loan term presents a unique set of advantages and disadvantages. Let’s break down the key trade-offs between shorter and longer durations.

The Appeal of Shorter Loan Terms (e.g., 36-48 Months)

Opting for a shorter car loan term, typically between 36 and 48 months, is often the financially savvier choice for those who can manage the higher monthly payments. These loans are designed to get you out of debt faster and save you a considerable amount of money in interest over time.

One of the most significant benefits is the lower total interest paid. Because you’re paying off the principal balance more quickly, the lender has less time to accrue interest charges. This directly translates to a lower overall cost for your vehicle. You’ll find that the difference in total interest can be substantial, even on the same car with the same interest rate, just by shortening the term.

Furthermore, shorter terms mean you build equity in your vehicle much faster. Equity is the difference between your car’s value and what you still owe on the loan. Building equity quickly reduces your risk of being "upside down" or in a negative equity situation, where you owe more than the car is worth. This faster equity build-up also means you’ll be debt-free sooner, freeing up that monthly payment for other financial goals like savings or investments.

Pro tips from us: If your budget allows, always lean towards the shortest term you can comfortably afford. It’s a disciplined approach that pays dividends in the long run. Shorter terms also often come with slightly lower interest rates from lenders, as they perceive less risk over a shorter repayment period.

The Allure and Risks of Longer Loan Terms (e.g., 72-84 Months)

Conversely, longer car loan terms, such as 72, 84, or even 96 months, have become increasingly popular for a compelling reason: lower monthly payments. In an era of rising vehicle prices, stretching out the repayment period makes more expensive cars seem more affordable on a month-to-month basis.

The primary advantage of a longer term is the reduced burden on your monthly budget. A lower payment can make it easier to afford the car you want, or simply keep more cash flow available for other expenses. For some buyers, this is the only way they can comfortably afford their desired vehicle.

However, the allure of a low monthly payment often masks significant long-term financial drawbacks. The most prominent of these is the substantially higher total interest paid. While your monthly payment is lower, you’re paying interest for a much longer period, leading to a significantly higher overall cost for the car. The difference can sometimes amount to thousands of dollars extra over the life of the loan.

From years of observing car buyers, a common mistake to avoid is stretching a loan just to get a car you can’t truly afford. This often leads to financial strain down the road. Longer terms also increase your risk of negative equity, where your car depreciates faster than you pay off the loan. This means you could owe more than the car is worth for a significant portion of the loan term, creating a precarious situation if you need to sell or trade in the vehicle.

Factors Influencing Your Ideal Car Loan Length

Determining the "best" car loan length for you isn’t a one-size-fits-all answer. It’s a highly personal decision influenced by a variety of financial and lifestyle factors. Carefully considering each of these will help you pinpoint the term that makes the most sense for your unique circumstances.

-

Your Budget and Monthly Payment Comfort: This is arguably the most critical factor. Your monthly car payment should fit comfortably within your overall budget without straining your finances. It’s not just about affording the payment, but also having enough left for insurance, fuel, maintenance, and other living expenses. Don’t let a desire for a particular car push you into an unmanageable monthly commitment.

-

Interest Rates: Longer loan terms typically come with higher interest rates. Lenders view extended repayment periods as riskier, and they price that risk into the interest rate. A higher interest rate, combined with a longer term, significantly amplifies the total cost of your loan. Always compare the Annual Percentage Rate (APR) across different loan terms.

-

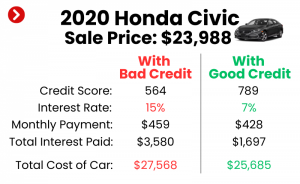

Your Credit Score: A strong credit score is your golden ticket to better loan terms, including lower interest rates and more flexible repayment options. Lenders offer their most competitive rates to borrowers with excellent credit, which can make even a slightly longer term more palatable due to reduced interest charges. Conversely, a lower credit score might limit your options to longer terms with higher rates, increasing your total cost.

-

Down Payment Amount: The more money you put down upfront, the less you need to borrow. A substantial down payment reduces your principal loan amount, which can then allow you to choose a shorter loan term with a manageable monthly payment. It also instantly builds equity in your vehicle and reduces your risk of negative equity.

-

Vehicle Depreciation: Cars begin to lose value the moment they’re driven off the lot. Some vehicles depreciate faster than others. If you choose a very long loan term, the rate at which your car loses value can easily outpace the rate at which you pay down your loan. This creates a significant risk of negative equity, which we’ll discuss in more detail shortly.

-

Your Financial Goals: Are you striving for debt freedom? Do you prioritize saving for a house or retirement? A shorter car loan term aligns better with a goal of quickly eliminating debt and freeing up cash flow. If your priority is simply the lowest possible monthly outlay, even if it means higher overall cost, then a longer term might appeal, but understand the trade-offs.

-

Warranty Period: Consider the vehicle’s warranty. If your loan term extends significantly beyond the manufacturer’s bumper-to-bumper warranty, you risk facing expensive repair costs while still paying off the loan. Aligning your loan term closer to the warranty period can provide peace of mind.

Pro tip: Utilize online car loan calculators to model different scenarios. Input various loan amounts, interest rates, and terms to see how your monthly payment and total interest change. This hands-on approach provides invaluable insight into finding your sweet spot.

The Pitfalls of Extended Car Loan Terms

While the lower monthly payments of extended car loans are undeniably attractive, they come with a set of significant financial pitfalls that borrowers must be fully aware of. Ignoring these risks can lead to considerable financial stress down the road.

One of the most concerning issues is negative equity, often referred to as being "upside down" on your loan. This occurs when the outstanding balance on your car loan is greater than the current market value of your vehicle. With longer loan terms, especially those stretching to 72, 84, or even 96 months, your car depreciates faster than you pay off the principal. This means you could owe more than your car is worth for several years into the loan, leaving you in a vulnerable position.

Being in a negative equity situation creates serious challenges if you need to sell your car, or if it’s totaled in an accident. If you sell, you’ll have to pay the difference out of pocket to satisfy the loan. If it’s totaled, your insurance payout might not cover the entire loan balance, leaving you responsible for the remaining amount. This is where GAP (Guaranteed Asset Protection) insurance becomes crucial, but it’s an additional cost that adds to your overall car ownership expense.

Another pitfall is the increased risk of mechanical issues. As cars age, they inevitably require more maintenance and repairs. If you’re still paying off a 7-year loan on a 5-year-old car, you could be faced with significant repair bills while simultaneously making loan payments. This double financial burden can quickly become overwhelming, especially if the repairs are unexpected.

There’s also the opportunity cost to consider. The extra money you’re paying in interest over an extended loan term could have been put to better use. Imagine investing that money, saving for a down payment on a house, or contributing to your retirement fund. The longer your loan, the more of your money is tied up in interest, rather than working for your future.

Finally, long terms can make it difficult to upgrade your vehicle. If you’re stuck in negative equity, trading in your car means rolling that outstanding balance into a new loan, instantly putting you upside down on your next vehicle. This can create a never-ending cycle of debt that’s incredibly hard to break free from.

Common mistake to avoid are: Thinking solely about the monthly payment and ignoring the total cost of the loan and the potential for negative equity. Always look at the bigger financial picture.

How to Determine Your Best Car Loan Length

With all this information, how do you pinpoint the best car loan length for your personal situation? It requires a strategic approach, combining self-assessment with diligent research.

-

Thoroughly Assess Your Financial Situation:

- Start by creating a detailed budget. Understand your monthly income versus your expenses. How much disposable income do you genuinely have for a car payment?

- Consider your current debt load. Adding a new car payment should not jeopardize your ability to manage existing obligations.

- Factor in other car-related expenses: insurance, fuel, maintenance, and potential repairs. These are ongoing costs that will impact your real monthly automotive budget.

-

Prioritize Your Goals:

- Is your top priority to minimize the total amount of interest paid and achieve debt freedom quickly? If so, aim for the shortest term you can afford.

- Is your primary concern a low monthly payment to maintain cash flow, even if it means paying more in total interest? In this case, a longer term might be necessary, but ensure you understand the associated risks like negative equity.

-

Shop Around for Rates and Terms from Multiple Lenders:

- Don’t just accept the first offer you receive, especially from the dealership. Prequalify with several banks, credit unions, and online lenders before you even step foot on the lot.

- Compare the Annual Percentage Rate (APR) and different term options each lender provides. This allows you to see how various loan lengths impact your payments and total cost across different institutions. For more tips on finding the best car loan rates, check out our guide on .

-

Consider a Substantial Down Payment:

- As mentioned, a larger down payment reduces the amount you need to borrow, which can significantly shorten your ideal loan term. Aim for at least 10-20% of the vehicle’s purchase price, if possible. This immediately builds equity and lowers your monthly payments.

-

Use Online Calculators:

- Experiment with various loan scenarios using online car loan calculators. Input different terms (e.g., 36, 48, 60, 72 months) and interest rates to visualize the impact on your monthly payment and total interest. This practical exercise can be incredibly eye-opening. For general advice on loan calculations, you can explore resources like Investopedia’s guide on loan amortization.

Beyond the Months: Other Key Considerations

While the loan term is a major piece of the puzzle, a few other elements can influence your overall car loan experience and should be part of your decision-making process.

-

Prepayment Penalties: Before signing, always check your loan agreement for any prepayment penalties. Some lenders charge a fee if you pay off your loan early. While less common now, it’s vital to confirm this, especially if you plan to make extra payments or pay off the loan ahead of schedule.

-

Refinancing Options: Your financial situation might change, or interest rates might drop after you’ve secured your initial loan. Understanding that refinancing is often an option can provide flexibility. You might be able to reduce your interest rate or adjust your loan term later on.

-

GAP Insurance: If you opt for a longer loan term or make a small down payment, consider GAP insurance. This covers the "gap" between what you owe on your loan and what your car’s actual cash value is if it’s totaled or stolen. It’s an extra cost, but it can save you from significant financial loss in unforeseen circumstances.

Conclusion: Driving Off with Confidence

The question of "how many months are car loans" is far more nuanced than simply picking a number. It’s a critical financial decision that impacts your monthly budget, your long-term debt, and your overall financial well-being. There’s no single "best" car loan length; instead, the ideal term is one that perfectly balances your immediate affordability with your long-term financial goals.

By understanding the trade-offs between shorter and longer terms, assessing your personal financial situation, and diligently shopping around for the best rates and conditions, you empower yourself to make a truly informed choice. Avoid the common mistake of focusing solely on the lowest monthly payment. Instead, consider the total cost of the loan, the risks of negative equity, and how quickly you can achieve debt freedom.

Making a thoughtful decision about your car loan length is an investment in your financial future. Drive off with confidence, knowing you’ve secured a deal that aligns with your budget and helps you achieve your goals.

Explore our other articles on car buying like to further enhance your automotive knowledge! Share your experiences with different car loan terms in the comments below – your insights could help other readers make smarter decisions!