The Ultimate Guide to Car Loans: Your Roadmap to Smart Auto Financing

The Ultimate Guide to Car Loans: Your Roadmap to Smart Auto Financing Carloan.Guidemechanic.com

The thrill of a new car, the freedom of the open road – it’s a dream many of us share. But for most people, turning that dream into a reality involves navigating the world of car loans. Understanding auto financing can feel daunting, yet it’s a crucial step in ensuring your new vehicle is an asset, not a financial burden.

This comprehensive guide is designed to demystify car loans. We’ll walk you through every aspect, from understanding the basics to securing the best possible deal. Our goal is to equip you with the knowledge and confidence to make informed decisions, transforming your car buying experience into a smooth and strategic journey.

The Ultimate Guide to Car Loans: Your Roadmap to Smart Auto Financing

Understanding the Basics: What Exactly is a Car Loan?

At its core, a car loan is a secured loan specifically designed to help you purchase a vehicle. When you take out a car loan, a lender provides you with the funds to buy the car, and in return, you agree to repay that amount, plus interest, over a predetermined period. The car itself typically serves as collateral for the loan.

This means that if you fail to make your payments, the lender has the right to repossess the vehicle. It’s a fundamental agreement that underpins almost all vehicle financing. Understanding this secured nature is the first step in responsible borrowing.

The money you borrow is known as the principal. The additional cost you pay for borrowing that money is the interest. Together, the principal and interest are repaid through regular monthly installments over the loan term, which can range from a few months to several years.

Types of Car Loans: Finding Your Perfect Fit

Not all car loans are created equal. Different situations call for different financing solutions. Knowing the various types available can help you identify the best option for your specific needs and financial standing.

New Car Loans

These loans are for purchasing brand-new vehicles directly from a dealership. New car loans typically come with some of the most attractive interest rates and longer repayment terms, often extending up to 72 or even 84 months. Lenders view new cars as less risky because they haven’t been subjected to wear and tear.

Eligibility for new car loans usually requires a good credit score and a stable income. The lower rates and longer terms can make monthly payments more affordable, but it’s important to remember that a longer term means paying more interest over the life of the loan. Always consider the total cost, not just the monthly payment.

Used Car Loans

If you’re buying a pre-owned vehicle, you’ll be looking at a used car loan. These loans can sometimes have slightly higher interest rates than new car loans because used vehicles are generally considered a higher risk to lenders due to potential mechanical issues and depreciation. The loan terms are also often shorter.

Lenders may have restrictions on the age and mileage of the used car they are willing to finance. For instance, some may not finance vehicles older than 10 years or with more than 100,000 miles. Always ensure the used car you’re considering passes a thorough inspection before committing to a loan.

Refinancing Car Loans

Refinancing involves taking out a new car loan to pay off your existing car loan. People typically refinance to secure a lower interest rate, reduce their monthly payments, or change their loan term. This can be a smart move if your credit score has significantly improved since you first took out the loan.

Based on my experience, refinancing can save you a substantial amount of money over the life of your loan. It’s particularly beneficial if market interest rates have dropped or if you initially accepted a high-interest rate due to limited options. Always compare the new loan’s terms and fees carefully against your current loan.

Lease Buyout Loans

If you’ve been leasing a car and decide you want to purchase it at the end of your lease term, a lease buyout loan is what you’ll need. This type of loan covers the residual value of the vehicle – the amount the car is estimated to be worth at the end of the lease agreement.

The decision to buy out a lease often depends on the car’s condition, its market value compared to the residual value, and your personal preference. It’s an important consideration if you’ve grown attached to your leased vehicle and wish to make it your own.

Bad Credit Car Loans

Even with a less-than-perfect credit history, securing a car loan is often possible. These are known as bad credit car loans. While the interest rates will typically be higher to offset the increased risk for the lender, they provide an opportunity to purchase a vehicle and, importantly, to rebuild your credit.

Lenders offering bad credit loans may require a larger down payment or a co-signer to mitigate their risk. Pro tips from us: Focus on making all payments on time to demonstrate financial responsibility, which will help improve your credit score over time.

Key Factors Influencing Your Car Loan

Several critical elements come into play when lenders assess your loan application and determine your interest rate. Understanding these factors will empower you to improve your chances of securing favorable terms.

Credit Score

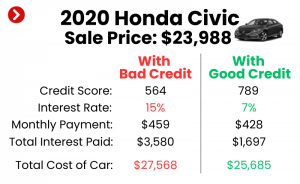

Your credit score is arguably the most significant factor influencing your car loan. This three-digit number, often a FICO or VantageScore, reflects your creditworthiness based on your payment history, outstanding debt, and credit length. A higher score signals less risk to lenders.

Lenders use your credit score to gauge your reliability in repaying debts. Borrowers with excellent credit (typically 720+) qualify for the lowest interest rates. Conversely, a lower score will result in higher interest rates, as lenders perceive a greater risk of default.

Pro tips from us: Always check your credit score and report before applying for a loan. This allows you to identify and dispute any errors that could negatively impact your eligibility.

Interest Rate (APR)

The interest rate, often expressed as an Annual Percentage Rate (APR), is the true cost of borrowing money. It’s the percentage of the principal loan amount that you pay to the lender each year. A lower APR means less money spent on interest over the life of the loan.

Interest rates can be fixed, meaning they stay the same throughout the loan term, or variable, meaning they can fluctuate. Most car loans are fixed-rate. It’s crucial to compare the APRs from different lenders, as even a small difference can save you hundreds or thousands of dollars.

Loan Term

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 60, 72, or 84 months). A shorter loan term generally means higher monthly payments but less total interest paid over the life of the loan.

Conversely, a longer loan term will result in lower monthly payments, making the car seem more affordable upfront. However, a common mistake to avoid is focusing solely on the lowest monthly payment. Longer terms lead to significantly more interest paid and can put you in a negative equity position (owing more than the car is worth) for a longer period.

Down Payment

A down payment is the initial amount of money you pay upfront towards the purchase of the car. It directly reduces the amount you need to borrow. Making a substantial down payment offers several advantages.

A larger down payment lowers your principal loan amount, which in turn reduces the total interest you’ll pay. It also signals financial stability to lenders and can help you secure a better interest rate. Furthermore, a good down payment helps you avoid being "upside down" on your loan, where the car’s value depreciates faster than you pay off the loan.

Debt-to-Income Ratio (DTI)

Lenders evaluate your debt-to-income (DTI) ratio to assess your ability to manage monthly payments. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income to cover new loan payments.

A high DTI might signal to lenders that you are already stretched thin financially, making you a higher risk. Lenders often prefer a DTI ratio below 36%, though some may approve loans with higher ratios depending on other factors.

Vehicle Type and Age

The type and age of the vehicle you intend to purchase also play a role in loan approval and interest rates. New cars, with their predictable depreciation schedules and manufacturer warranties, are generally seen as less risky than older, high-mileage used cars. Lenders are more confident in their ability to recover costs if a new car needs to be repossessed and resold.

Luxury vehicles or those with high-performance components might also be viewed differently than standard economy cars. This is due to varying resale values and potential repair costs, which can affect the car’s collateral value over time.

The Car Loan Application Process: A Step-by-Step Guide

Securing a car loan doesn’t have to be complicated. Following a structured approach can simplify the process and help you land the best possible deal.

Step 1: Assess Your Budget

Before you even look at cars, determine how much you can truly afford. This goes beyond just the monthly loan payment. Factor in insurance costs, fuel, maintenance, registration fees, and potential repair expenses.

A general rule of thumb is that your total car expenses, including the loan payment, shouldn’t exceed 10-20% of your take-home pay. Being realistic about your budget prevents financial strain down the road.

Step 2: Check Your Credit Score

Knowing your credit standing is paramount. Obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and your credit score. You can typically get one free report annually from AnnualCreditReport.com.

Review your report for any inaccuracies or fraudulent activity. Disputing and correcting errors can significantly improve your score, potentially leading to better loan terms.

Step 3: Gather Necessary Documents

Being prepared with your documents will streamline the application process. While requirements vary by lender, common documents include:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Pay stubs, W-2s, or tax returns (for self-employed).

- Proof of Residency: Utility bill or lease agreement.

- Proof of Insurance: Required before driving off the lot.

- Vehicle Information: If you already know which car you want.

Step 4: Get Pre-Approved (Highly Recommended)

Based on my experience, getting pre-approved for a car loan is one of the smartest moves you can make. Pre-approval means a lender has conditionally agreed to lend you a certain amount at a specific interest rate, based on your creditworthiness. This allows you to shop for a car with a clear budget and the confidence of a cash buyer.

Pre-approval offers from multiple lenders also provide leverage when negotiating with dealerships. You’ll know what external financing you qualify for, giving you a benchmark against any offers the dealership might present.

Step 5: Compare Offers from Multiple Lenders

Do not settle for the first loan offer you receive. Shop around! Contact various financial institutions, including banks, credit unions, and online lenders. Each lender has different criteria and rates.

Pro tips from us: Submit all your loan applications within a short window, typically 14-30 days. Credit bureaus often treat multiple inquiries for the same type of loan within this period as a single inquiry, minimizing the impact on your credit score.

Step 6: Read the Fine Print

Before signing any loan agreement, meticulously read every detail. Understand the interest rate (APR), the total loan amount, the repayment schedule, and any fees. Look out for prepayment penalties, which charge you for paying off your loan early, or hidden administrative fees.

Also, be aware of add-ons like GAP insurance, extended warranties, or service contracts. While some may be valuable, ensure you understand their cost and whether they are truly necessary for your situation.

Step 7: Negotiate and Finalize

Armed with your pre-approval and knowledge, you’re in a strong position to negotiate. If a dealership offers financing, compare it against your pre-approved rates. Sometimes, dealerships can beat external offers due to manufacturer incentives. Don’t be afraid to ask questions and negotiate not just the car price, but also the financing terms.

Once you’re satisfied with all the terms, finalize the paperwork. Ensure all verbal agreements are documented in writing before you sign.

Where to Get a Car Loan: Exploring Your Options

You have several avenues when it comes to securing a car loan, each with its own set of advantages.

Banks

Traditional banks are a common source for car loans. They often offer competitive rates for borrowers with good credit and provide a familiar, reliable lending experience. You might already have a relationship with a bank, which can sometimes streamline the application process.

However, banks can sometimes have stricter lending criteria compared to other options. It’s always worth checking with your current bank first, but don’t stop there.

Credit Unions

Credit unions are non-profit financial cooperatives owned by their members. They are renowned for offering some of the most competitive interest rates on car loans, often lower than traditional banks, because their primary goal is to serve their members, not generate profits.

Membership is usually required, but it’s often easy to join. For a deeper dive into the benefits of credit unions, consider exploring .

Online Lenders

The digital age has brought forth a plethora of online lenders specializing in auto financing. These platforms often offer quick application processes and rapid approval decisions, sometimes within minutes. They can also be a good option for borrowers with a range of credit scores, including those with less-than-perfect credit.

Online lenders offer convenience and the ability to compare multiple offers from the comfort of your home. Always ensure the online lender is reputable and secure before sharing your personal information.

Dealership Financing

Most car dealerships offer financing options directly through their finance departments. This can be very convenient, allowing you to handle the car purchase and financing in one place. Dealerships often work with a network of banks and captive lenders (lenders owned by the car manufacturer) to secure financing.

Pro tips from us: While convenient, always compare dealership offers against your own pre-approvals. Dealerships sometimes mark up interest rates to make a profit, but they can also offer promotional rates or incentives that are hard to beat. Always have an external offer to compare against.

Common Mistakes to Avoid When Getting a Car Loan

Navigating car financing can have pitfalls. Awareness of common mistakes can help you steer clear of costly errors.

One of the most frequent errors is not checking your credit score beforehand. This leaves you unaware of your standing and vulnerable to unfavorable terms. Another common mistake is failing to get pre-approved; without it, you lose significant negotiation power.

Focusing solely on the monthly payment is a classic trap. While a low monthly payment seems attractive, it often comes with an extended loan term and significantly more interest paid over time. Similarly, extending the loan term too long, beyond 60 or 72 months, can lead to paying much more in interest and being upside down on your loan for longer.

Skipping the down payment is another pitfall. A zero-down loan means you finance the entire purchase price, leading to higher monthly payments and interest. Furthermore, not reading the fine print can lead to unexpected fees, hidden clauses, or unfavorable terms you weren’t aware of.

Finally, ignoring additional costs like insurance, maintenance, and fuel, and only budgeting for the loan payment, can quickly lead to financial stress. A car is more than just its purchase price.

After You Get Your Loan: Smart Management

Once you’ve secured your car loan and driven off in your new vehicle, your financial journey isn’t over. Responsible loan management is key to minimizing costs and maintaining good credit.

Always make your payments on time, every time. Timely payments are crucial for maintaining a good credit score and avoiding late fees. Setting up automatic payments can help ensure you never miss a due date.

Consider making extra payments whenever possible. Even a small additional amount each month can significantly reduce the total interest you pay over the loan’s life and help you pay it off sooner. Understand your loan statements, noting the principal remaining, interest paid, and any fees.

If your financial situation improves or interest rates drop, consider refinancing your loan to potentially lower your interest rate or monthly payments. For more general advice on managing debt and improving your financial health, visit trusted resources like the Consumer Financial Protection Bureau (CFPB) at .

Conclusion

Securing a car loan is a significant financial decision, but it doesn’t have to be intimidating. By understanding the different types of loans, the factors that influence them, and the step-by-step application process, you empower yourself to make intelligent choices. Your credit score, interest rate, and loan term are all vital pieces of the puzzle.

Armed with this comprehensive knowledge, you’re now ready to approach car financing with confidence and clarity. Remember to do your research, compare offers, read the fine print, and always choose the option that best fits your financial goals. Your journey to smart auto financing starts here, paving the way for years of enjoyable driving.