The Ultimate Guide to Paying Off Your Car Loan Faster: Save Money, Gain Freedom

The Ultimate Guide to Paying Off Your Car Loan Faster: Save Money, Gain Freedom Carloan.Guidemechanic.com

The hum of a new engine, the gleam of fresh paint – owning a car brings a sense of independence and excitement. However, for many, that joy often comes with the steady drumbeat of monthly car loan payments. These commitments can feel like a financial anchor, stretching over years and silently accumulating substantial interest. If you’re looking to break free from this debt sooner, save money, and unlock a new level of financial freedom, you’ve come to the right place.

As an expert blogger and professional SEO content writer, I’ve delved deep into the world of personal finance. Based on my experience, paying off your car loan early is not just a dream; it’s an achievable goal with tangible benefits. This comprehensive guide will equip you with proven strategies, practical tips, and crucial insights to accelerate your car loan payoff journey. Let’s shift your financial future into high gear!

The Ultimate Guide to Paying Off Your Car Loan Faster: Save Money, Gain Freedom

Why Accelerate Your Car Loan Payoff? More Than Just Peace of Mind

Before diving into the "how," let’s explore the compelling reasons why paying off your car loan faster is a smart financial move. It’s about more than just having one less bill to worry about; it’s about strategic financial empowerment.

Save Substantial Money on Interest: This is perhaps the most direct and impactful benefit. Car loans are amortized, meaning a larger portion of your early payments goes towards interest. By paying off your principal faster, you reduce the total amount of interest accrued over the life of the loan. This can translate into hundreds, or even thousands, of dollars saved.

Boost Your Credit Score and Debt-to-Income Ratio: A lower debt-to-income (DTI) ratio is a green flag for lenders. Paying off a car loan significantly reduces your overall debt, which can improve your DTI and, consequently, your credit score. This positions you better for future financial endeavors, like securing a mortgage or other loans at favorable rates.

Gain Financial Flexibility and Free Up Cash Flow: Imagine that monthly car payment suddenly vanishing from your budget. The funds you once allocated to your loan can now be redirected towards other crucial financial goals. This could mean bolstering your emergency fund, investing for retirement, saving for a down payment on a home, or simply having more disposable income for your chosen lifestyle.

Achieve True Ownership and Build Equity Faster: Until your loan is paid off, the lender essentially owns a significant stake in your vehicle. By accelerating your payments, you gain full ownership sooner, freeing you from lienholders and enabling you to build equity in your asset more quickly. This provides a sense of security and control.

Reduce Financial Stress and Gain Peace of Mind: Debt, regardless of its size, can be a source of stress. Eliminating a significant monthly obligation like a car loan can lift a considerable burden from your shoulders. The psychological relief of being debt-free is invaluable, allowing you to focus on future financial growth rather than past commitments.

Understanding Your Car Loan: The Essential Basics

To effectively tackle your car loan, you first need to understand its fundamental components. Knowledge is power, especially when it comes to personal finance. Don’s just make payments; understand what each payment is doing.

Principal vs. Interest: What You’re Really Paying: Your car loan payment is divided into two main parts: the principal and the interest. The principal is the original amount of money you borrowed to buy the car. The interest is the cost of borrowing that money, charged by the lender. Early in your loan term, a larger portion of your payment goes towards interest, gradually shifting to more principal as the loan matures.

Annual Percentage Rate (APR): The True Cost of Borrowing: Your APR is the annual rate of interest charged to borrowers and is expressed as a percentage. It reflects the true cost of your loan, including certain fees, and helps you compare offers from different lenders. A lower APR means you’ll pay less interest over the life of the loan.

Loan Term: How Long You’re Committed: The loan term is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, or 72 months). While longer terms offer lower monthly payments, they almost always result in paying significantly more in total interest. Shorter terms mean higher monthly payments but less interest paid overall.

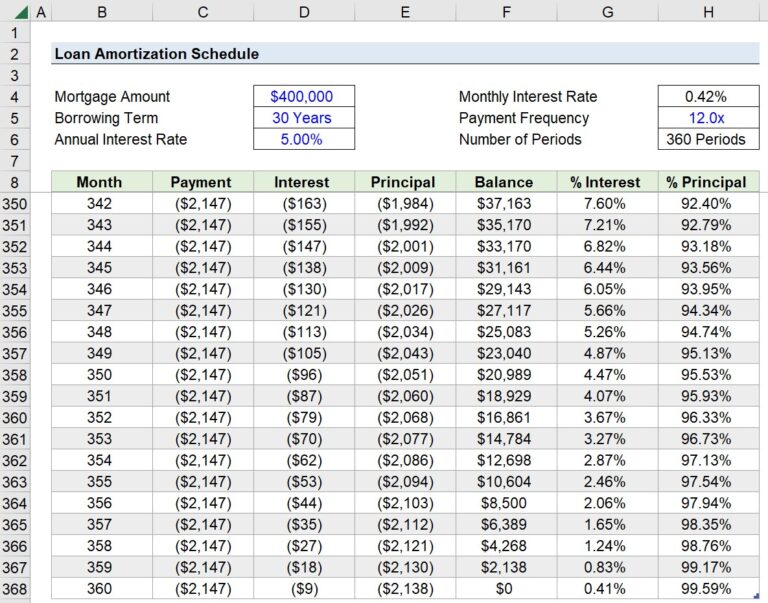

Amortization: The Payment Breakdown Over Time: Amortization is the process of paying off debt over time through regular, fixed payments. Each payment covers both interest and a portion of the principal. An amortization schedule shows how each payment is applied, illustrating the shift from interest-heavy to principal-heavy payments over the loan’s duration. Understanding this schedule can highlight just how much interest you can save by paying extra principal early on.

Checking for Prepayment Penalties: Before you start aggressively paying down your loan, it’s crucial to review your loan agreement for any prepayment penalties. Some lenders charge a fee if you pay off your loan early, designed to recoup lost interest. While less common with car loans than with mortgages, it’s always wise to confirm this detail. Pro tips from us: Always read the fine print!

Proven Strategies to Pay Off Your Car Loan Faster

Now that we understand the "why" and the "what," let’s dive into the actionable "how." These strategies, when applied consistently, can dramatically shorten your loan term and save you a substantial amount of money.

1. Make Extra Principal Payments

This is often the simplest and most effective method, based on my experience. Any amount you pay beyond your regular monthly payment can be designated to go directly towards your loan’s principal. Even small, consistent extra payments can make a significant difference over time.

To implement this, ensure you clearly instruct your lender that the additional funds are to be applied solely to the principal balance. Otherwise, the lender might apply the extra money to the next month’s payment, which doesn’t accelerate your payoff as effectively. Many online payment portals offer an option for "principal-only" payments. Even an extra $50 per month, when consistently applied, can shave months off your loan and save you hundreds in interest.

2. Embrace Bi-Weekly Payments

This strategy is a subtle yet powerful way to accelerate your payoff without feeling a huge pinch in your budget. Instead of making one full payment per month, you make half of your monthly payment every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments, which equates to 13 full monthly payments annually instead of the standard 12.

The extra payment each year goes directly towards reducing your principal, significantly shortening your loan term. Setting this up as an automatic transfer from your bank account makes it effortless. It’s a "set it and forget it" approach that delivers consistent results.

3. Strategically Refinance Your Car Loan

Refinancing involves taking out a new loan to pay off your existing car loan. This strategy is most effective if you can secure a lower Annual Percentage Rate (APR) than your current loan. A lower interest rate means more of your payment goes towards principal, and you’ll pay less overall.

Consider refinancing if your credit score has improved since you took out the original loan, or if market interest rates have dropped. You could also refinance to a shorter loan term, which will increase your monthly payment but drastically reduce the total interest paid and accelerate your payoff. Common mistakes to avoid are refinancing for a longer term just to lower monthly payments; while it might feel good in the short term, it almost always leads to paying more interest over the loan’s life. For a deeper dive into whether refinancing is right for you, check out our comprehensive guide on Car Loan Refinancing strategies.

4. Round Up Your Monthly Payments

This is a straightforward and painless way to chip away at your principal. Instead of paying the exact amount due, round up your payment to the nearest convenient figure. For example, if your payment is $342, round it up to $350 or even $400.

While the individual amounts might seem small, the consistency adds up. Over the course of several years, these rounded-up payments contribute significantly to reducing your principal balance. It’s an easy mental trick that makes debt reduction feel less like a chore and more like a small, consistent effort.

5. Apply Windfalls and Bonuses

Unexpected money, often referred to as "windfalls," presents a golden opportunity to make a substantial dent in your car loan. This includes funds like tax refunds, work bonuses, inheritance, or even birthday money. Instead of spending these funds on discretionary items, consider funneling them directly into your car loan.

A lump-sum payment can dramatically reduce your principal, leading to significant interest savings and a faster payoff. Pro tip: Before you even receive the money, earmark a portion (or all) of it specifically for your debt reduction goals. This proactive approach prevents impulsive spending and keeps you on track.

6. Trim Your Budget and Redirect Savings

One of the most powerful strategies involves finding extra money within your existing budget. Take a close look at your monthly spending. Are there areas where you can cut back, even temporarily? This could mean reducing dining out, canceling unused subscriptions, or finding cheaper alternatives for daily expenses.

Once you identify these savings, commit to redirecting that money directly to your car loan. Based on my experience, even seemingly small adjustments like cutting out a daily coffee or packing your lunch can free up a surprising amount of cash over a month. Need help getting started with budgeting? Our article on Effective Budgeting Strategies offers practical advice.

7. Consider a Side Hustle

If cutting expenses isn’t enough or you’ve already trimmed your budget to the bone, a side hustle can provide the extra income needed to accelerate your car loan payoff. This could involve freelancing in your area of expertise, driving for a ride-sharing service, selling crafts online, or taking on part-time work.

The key is to designate 100% of the income generated from your side hustle specifically towards your car loan. This allows you to make extra payments without impacting your primary budget or lifestyle, providing a powerful boost to your debt reduction efforts. It’s a proactive way to earn your way out of debt faster.

8. Debt Snowball or Avalanche (Focus on Your Car Loan)

While typically applied to multiple debts, the underlying principles of the debt snowball and avalanche methods can be adapted to accelerate a single car loan. The debt snowball method focuses on psychological wins by prioritizing the smallest debt first. If your car loan is your only or smallest debt, you’d apply all extra funds to it, gaining momentum as you see the balance drop.

The debt avalanche method prioritizes debts with the highest interest rates first, saving you the most money in interest over time. If your car loan has a high APR compared to other debts, applying extra payments to it first would be the financially optimal choice. In either case, the core idea is to intensely focus all available extra funds on this one debt until it’s gone.

Common Mistakes to Avoid When Paying Off Your Car Loan

While the goal is to pay off your loan faster, it’s equally important to avoid pitfalls that could hinder your progress or even cost you more in the long run.

Ignoring Prepayment Penalties: As mentioned earlier, always check your loan agreement for any fees associated with early payoff. While rare for car loans, it’s a critical detail that could negate some of your interest savings. Be informed before you act.

Not Specifying Principal-Only Payments: This is a recurring mistake. If you send extra money without explicitly stating it’s for the principal, the lender might apply it to future payments, meaning you won’t save as much interest or shorten your loan term as effectively. Always confirm your extra payments are correctly applied.

Refinancing to a Longer Term to Lower Payments: While a lower monthly payment might seem appealing, extending your loan term almost always means you’ll pay more in total interest. Only refinance if you can secure a lower interest rate and ideally maintain or shorten your loan term.

Neglecting Your Emergency Fund: Don’t deplete your emergency savings to pay off your car loan. An emergency fund (typically 3-6 months of living expenses) is your financial safety net. Without it, a sudden job loss or unexpected expense could force you into more debt. Prioritize building or maintaining this fund alongside your debt reduction efforts.

Life After Car Loan Payoff: What’s Next?

Congratulations! You’ve successfully paid off your car loan and achieved a significant financial milestone. But the journey doesn’t end there. This newfound financial freedom opens doors to even greater opportunities.

Build or Bolster Your Emergency Fund: With your car payment gone, redirect those funds to supercharge your emergency savings. A robust emergency fund provides unparalleled security and peace of mind.

Save for Your Next Car (or a Down Payment): Instead of immediately taking on another loan, start saving for your next vehicle purchase. Imagine paying cash for your next car, or at least making a substantial down payment to reduce future loan amounts and interest.

Invest for Your Future: With freed-up cash flow, you can now contribute more aggressively to retirement accounts, investment portfolios, or other wealth-building vehicles. Let your money start working harder for you.

Enjoy Your Financial Freedom: Reallocate the funds you were dedicating to your car loan towards experiences, personal growth, or simply enjoying the fruits of your disciplined labor. You’ve earned it!

Conclusion: Drive Towards Financial Freedom Today

Paying off your car loan early is a powerful step towards achieving greater financial freedom and security. It’s a commitment that requires discipline and strategic planning, but the rewards—significant interest savings, improved credit, and invaluable peace of mind—are well worth the effort.

By understanding the components of your loan, implementing proven strategies like making extra principal payments, embracing bi-weekly payments, or strategically refinancing, and avoiding common pitfalls, you can accelerate your journey to debt freedom. Don’t let your car loan dictate your financial future. Take control, apply these strategies, and drive towards a more prosperous tomorrow.

Start today, even with the smallest step. Every extra dollar you put towards your principal brings you closer to owning your car outright and unlocking new financial possibilities. For more resources on managing debt and improving your financial literacy, we recommend visiting the Consumer Financial Protection Bureau website.