The Ultimate Guide to Paying Off Your Car Loan In Full: Achieve Financial Freedom Faster

The Ultimate Guide to Paying Off Your Car Loan In Full: Achieve Financial Freedom Faster Carloan.Guidemechanic.com

The open road awaits, and the thought of driving a car that is truly, unequivocally yours—free from the shackles of monthly payments—is incredibly appealing. For many, a car loan represents a significant chunk of their budget, often stretching over several years. But what if you could accelerate that timeline? What if you could wave goodbye to those payments much sooner than planned?

In this comprehensive guide, we’ll dive deep into the world of paying off your car loan in full. We’ll explore not just how to do it, but why it might be one of the smartest financial moves you can make, and when it might be better to hold off. Our goal is to equip you with the knowledge and strategies to confidently navigate your path to car ownership freedom, making this article your ultimate resource for achieving that debt-free dream.

The Ultimate Guide to Paying Off Your Car Loan In Full: Achieve Financial Freedom Faster

Why Consider Paying Off Your Car Loan Early? Unlocking a World of Benefits

Deciding to pay off your car loan ahead of schedule isn’t just about ticking an item off your financial to-do list; it’s about strategically enhancing your financial well-being. The advantages extend far beyond simply closing an account. Let’s explore the compelling reasons why many people choose this accelerated path.

Significant Savings on Interest Payments

This is often the most immediate and tangible benefit. Car loans, like most loans, accrue interest over time. The longer you carry a balance, the more interest you pay. By paying off your car loan in full early, you dramatically reduce the principal balance, which in turn reduces the total interest charged over the life of the loan. This means more of your hard-earned money stays in your pocket rather than going to the lender.

Imagine a loan with a 6% interest rate over 60 months. Even an extra payment or two can shave off months and hundreds, if not thousands, of dollars in interest. It’s a direct return on your investment, guaranteed.

Embrace True Financial Freedom and Reduce Stress

There’s an undeniable psychological burden that comes with carrying debt. Each month, that car payment looms, a constant reminder of an obligation. Eliminating this debt can be incredibly liberating. It frees up a significant portion of your monthly budget, which can then be redirected towards other financial goals, like saving for a down payment on a house, investing, or building an emergency fund.

Based on my experience, one of the most liberating financial feelings is shedding recurring debt. The peace of mind that comes with knowing your vehicle is entirely yours, without a monthly obligation, is truly invaluable. It removes a layer of financial stress that many people don’t realize they’re carrying until it’s gone.

Improve Your Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is a crucial metric lenders use to assess your ability to manage monthly payments and repay debts. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI ratio indicates less financial risk.

By eliminating your car loan, you effectively reduce your total monthly debt payments, thereby improving your DTI ratio. This can make it easier to qualify for other loans in the future, such as a mortgage, and potentially secure better interest rates because you appear to be a less risky borrower.

Gain Full Ownership and Control Over Your Asset

When you have a car loan, the lender typically holds the title to your vehicle until the loan is fully repaid. This means they have a lien on your car. While you drive it, you don’t fully own it. Once you pay off the loan, the lender releases the lien, and you receive the clear title.

This gives you complete control over your asset. You can sell it, trade it in, or even use it as collateral for a future loan (though we generally advise against that) without needing to involve the original lender. It simplifies any future transactions involving your vehicle.

Simplify Future Vehicle Transactions

Thinking about trading in your car for a newer model, or perhaps selling it privately? If you still have an outstanding loan, these processes become more complex. You’ll need to coordinate with your lender to get a payoff quote and ensure the lien is released before the sale or trade can be finalized.

With a fully paid-off car, the process is streamlined. You hold the title, making transactions much quicker and smoother. This flexibility can be a major advantage when market conditions are favorable for selling or buying.

Is Paying Off Your Car Loan Early Always the Right Move? Considerations to Weigh

While the benefits of paying off your car loan in full are compelling, it’s not always the best financial decision for everyone. There are several factors you should carefully consider before channeling all your extra cash towards your car debt. A balanced perspective is key to making the right choice for your unique situation.

Opportunity Cost: Where Else Could Your Money Go?

Every dollar you use to pay down your car loan is a dollar that can’t be used for something else. This is known as opportunity cost. If you have other debts with significantly higher interest rates, such as credit card debt (which often carries interest rates of 18% or more), paying those off first usually makes more financial sense. The interest savings from high-interest debt will almost always outweigh the savings from a relatively lower-interest car loan.

Similarly, if you have robust investment opportunities that consistently yield returns higher than your car loan’s interest rate, you might consider investing that money instead. However, this comes with market risk, unlike the guaranteed savings from paying off debt.

Protect Your Emergency Fund

One of the most common mistakes to avoid is depleting your emergency savings to pay off a loan. An emergency fund is crucial for covering unexpected expenses like job loss, medical emergencies, or home repairs. It acts as a financial safety net.

Pro tips from us suggest that you should always maintain at least three to six months’ worth of living expenses in an easily accessible, liquid savings account before considering aggressive debt repayment strategies. Don’t sacrifice your financial security for a faster car loan payoff.

Check for Prepayment Penalties

While less common with car loans than with mortgages, some loan agreements include prepayment penalties. These are fees charged by the lender if you pay off your loan earlier than scheduled, designed to recoup some of the interest they would have earned.

Before making any large extra payments, carefully review your loan agreement or contact your lender directly to confirm if any prepayment penalties apply. If a penalty exists, calculate whether the interest savings still outweigh the penalty fee. Most modern car loans do not have these, but it’s always wise to check.

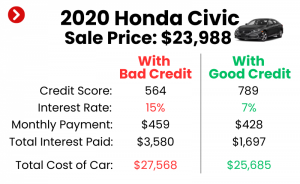

Your Interest Rate Matters

The interest rate on your car loan is a critical factor. If you have a very low interest rate (e.g., 0-3%), the financial incentive to pay it off early is less significant. In such cases, your money might generate better returns elsewhere, or it could be better used to tackle higher-interest debts.

Conversely, if your interest rate is high (e.g., 7% or more), the savings from early repayment become much more substantial, making it a highly attractive option. Evaluate your current interest rate in the context of your overall financial picture.

Effective Strategies for Paying Off Your Car Loan Faster

Once you’ve decided that paying off your car loan in full is the right move for you, the next step is to implement effective strategies. There are several proven methods you can use to accelerate your debt repayment, each with its own merits.

1. Making Consistent Extra Payments

This is perhaps the most straightforward and effective strategy. Any amount you pay over your minimum monthly payment goes directly towards reducing your principal balance, which in turn reduces the total interest you’ll pay.

- Bi-Weekly Payments: Instead of making one full payment each month, divide your monthly payment by two and pay that amount every two weeks. Because there are 52 weeks in a year, you’ll end up making 26 half-payments, which equates to 13 full monthly payments instead of 12. This subtle shift can shave months off your loan term and save you significant interest.

- One Extra Payment Per Year: If bi-weekly isn’t feasible, aim to make just one additional full payment each year. You can do this by paying an extra 1/12th of your monthly payment each month, or by making a lump-sum payment whenever you receive a windfall.

- Rounding Up Payments: If your monthly payment is, say, $347, consider rounding it up to $350 or even $400. That small extra amount consistently applied adds up over time without feeling like a huge sacrifice.

When making extra payments, always specify to your lender that the additional funds should be applied directly to the principal balance. Otherwise, they might apply it to future interest or even hold it as a credit, which doesn’t accelerate your payoff.

2. Refinancing Your Car Loan

Refinancing involves taking out a new loan to pay off your existing car loan. This strategy can be incredibly powerful if you can secure a lower interest rate or a shorter loan term.

- Lower Interest Rate: If your credit score has improved since you first took out the loan, or if market rates have dropped, you might qualify for a significantly lower interest rate. This reduces the cost of borrowing and means more of your payment goes towards the principal.

- Shorter Loan Term: You could also refinance for a shorter term. While this might increase your monthly payment, it drastically reduces the total interest paid and gets you to debt freedom much faster.

- When to Consider Refinancing: This is a great option if your credit has improved, interest rates have fallen, or if you initially took out a long-term loan (e.g., 72 months) and now want to shorten it. For a deeper dive into refinancing, check out our guide on .

3. The "Debt Snowball" or "Debt Avalanche" Method

These popular debt repayment strategies can be adapted for car loans, especially if you have multiple debts.

- Debt Snowball: You focus on paying off your smallest debt first, while making minimum payments on all others. Once the smallest debt is paid, you take the money you were paying on it and add it to the minimum payment of your next smallest debt. This method builds momentum and motivation. If your car loan is your smallest debt, this can be a powerful way to eliminate it quickly.

- Debt Avalanche: With this method, you focus on paying off the debt with the highest interest rate first, while making minimum payments on all others. Once that’s paid, you move to the debt with the next highest interest rate. This method saves you the most money on interest over time. If your car loan has your highest interest rate, this is the financially optimal strategy.

4. Applying Windfalls and Unexpected Income

Did you get a work bonus? A tax refund? An inheritance? A generous gift? Instead of spending these unexpected windfalls, consider dedicating a portion (or all) of them to your car loan. Lump-sum payments can significantly reduce your principal balance and accelerate your payoff timeline dramatically.

Even smaller windfalls, like money saved from a frugal month or a side gig payment, can be directed towards your loan. Every extra dollar makes a difference.

5. Cutting Unnecessary Expenses

To free up more money for extra payments, take a critical look at your budget. Are there areas where you can cut back?

- Review Subscriptions: Cancel unused streaming services, gym memberships, or app subscriptions.

- Dining Out: Reduce the frequency of restaurant meals and coffee shop visits. Cooking at home is often much cheaper.

- Entertainment: Find free or low-cost entertainment options.

- Shopping: Practice mindful spending and avoid impulse purchases.

Every dollar saved from these categories can be channeled directly towards paying off your car loan in full.

6. Increasing Your Income

Sometimes, cutting expenses isn’t enough, or there’s simply not much left to cut. In such cases, increasing your income can be the fastest route to accelerating your car loan payoff.

- Side Hustles: Consider freelancing, driving for a ride-share service, delivering food, or taking on temporary gigs.

- Overtime: If available at your current job, picking up extra hours can provide a boost to your income.

- Sell Unused Items: Declutter your home and sell items you no longer need on online marketplaces.

Any additional income generated can be exclusively dedicated to your car loan, making a significant impact on your payoff speed.

The Step-by-Step Process to Pay Off Your Car Loan In Full

Once you’ve chosen your strategies and gathered your funds, the final steps to complete the payoff are crucial. Doing this correctly ensures you gain full ownership and avoid any future headaches.

Step 1: Review Your Loan Documents

Before anything else, pull out your original loan agreement. Look for:

- Your current interest rate.

- Any mention of prepayment penalties.

- The exact name of your lender.

- Your loan account number.

Understanding these details will guide your next actions and help you avoid any surprises.

Step 2: Contact Your Lender for a Payoff Quote

Do not simply send your calculated balance. Interest accrues daily, so the amount you think you owe might not be the exact amount required to close the loan. Contact your lender (via phone, their online portal, or a branch visit) and request a "10-day payoff quote." This quote will provide the precise amount you need to pay, including any accrued interest, valid for a specific period (usually 7-10 days).

Make sure to ask for the exact method they prefer for receiving a final payment (e.g., wire transfer, certified check, online payment).

Step 3: Make the Final Payment

Send the exact amount specified in the payoff quote by the deadline. It’s often best to use a payment method that provides proof of delivery, such as a certified check or a wire transfer, especially for larger sums.

Double-check that your account number is clearly noted on the payment. This ensures the funds are correctly applied to your specific loan.

Step 4: Obtain Your Lien Release

This is a critical step! After receiving your final payment, the lender is legally obligated to release the lien on your vehicle. This process can take a few days or even weeks, depending on the lender and your state’s regulations.

- Follow Up: If you don’t receive confirmation within a reasonable timeframe, contact your lender to inquire about the status of the lien release.

- Receive Your In most states, once the lien is released, the lender will either mail you the clear title to your car, or they will electronically notify your state’s Department of Motor Vehicles (DMV) that the lien has been satisfied. You may then need to apply for a new title with the lien removed.

- External Link: For general information on vehicle titles and liens, you can consult resources like the Consumer Financial Protection Bureau’s (CFPB) auto loan guidance.

Step 5: Update Your Auto Insurance

Once your car loan is paid off, you are no longer required to carry comprehensive and collision insurance for the benefit of the lender. While it’s usually wise to maintain these coverages for your own protection, you now have the freedom to adjust your policy as you see fit.

Contact your insurance provider to remove the lender as a "loss payee" on your policy. This ensures that any future claims will be paid directly to you.

What Happens After You Pay Off Your Car Loan? Celebrating Your Achievement!

Congratulations! You’ve successfully navigated the process of paying off your car loan in full. This is a significant financial milestone that deserves recognition. But what comes next?

First and foremost, take a moment to celebrate this achievement. You’ve worked hard, made sacrifices, and now you’re debt-free on your vehicle. This is a big win for your financial health.

Beyond the celebration, this new financial freedom opens up several opportunities. You now have that extra money from your former car payment available each month. This is a perfect opportunity to redirect those funds strategically. Consider boosting your emergency fund, increasing contributions to your retirement accounts, or saving for a down payment on a home. You could also start saving for your next car, perhaps even paying cash for it.

Once your car loan is gone, consider exploring strategies for building long-term wealth, as discussed in our article . The discipline you used to pay off your car loan can now be applied to other areas of your financial life, setting you up for even greater success.

Conclusion: Drive Towards a Debt-Free Future

Paying off your car loan in full is more than just a financial transaction; it’s a step towards greater financial independence and peace of mind. By saving on interest, reducing stress, and gaining full control of your asset, you position yourself for a stronger financial future.

Whether you choose to make extra payments, refinance, utilize windfalls, or employ a combination of strategies, the key is consistency and commitment. Remember to weigh the pros and cons for your personal situation, ensuring you maintain a robust emergency fund and address any higher-interest debts first.

Take the insights from this guide, apply the actionable strategies, and start your journey towards driving a truly debt-free vehicle. The road to financial freedom is within reach, and with your car loan behind you, you’ll be accelerating towards it faster than ever before.