The Ultimate Guide to Recommended Car Loan Length: Navigating Your Auto Financing Journey

The Ultimate Guide to Recommended Car Loan Length: Navigating Your Auto Financing Journey Carloan.Guidemechanic.com

Buying a new or used car is an exciting milestone for many, but the excitement can quickly turn into anxiety when it comes to financing. One of the most critical decisions you’ll face, beyond choosing the car itself, is determining the right car loan length. This single factor profoundly impacts your monthly budget, the total cost of your vehicle, and your financial well-being for years to come.

As an expert blogger and professional in the automotive finance space, I’ve seen countless buyers make choices they later regret. My mission with this comprehensive guide is to empower you with the knowledge to make an informed decision about your recommended car loan length, ensuring you drive away not just with a new car, but with a smart financial plan. Let’s dive deep into the world of auto financing terms and uncover the strategies for securing the best deal for you.

The Ultimate Guide to Recommended Car Loan Length: Navigating Your Auto Financing Journey

Understanding Car Loan Lengths: The Basics

When we talk about car loan length, we’re referring to the loan term – the duration over which you agree to repay the borrowed money, plus interest. Loan terms are typically expressed in months, with common options ranging from 36, 48, 60, 72, to even 84 months. Each term presents a unique trade-off between your monthly payment and the total amount you’ll pay over the life of the loan.

The fundamental principle is straightforward: a shorter loan term generally means higher monthly payments but less total interest paid. Conversely, a longer loan term offers lower monthly payments, making the car seem more affordable upfront, but you’ll end up paying significantly more in total interest over time. It’s a delicate balance that requires careful consideration.

The Sweet Spot: What’s the Recommended Car Loan Length for Most Buyers?

Based on my experience analyzing thousands of auto financing scenarios, there isn’t a single "one-size-fits-all" recommended car loan length. Your ideal term depends on a confluence of personal financial circumstances, including your budget, credit score, the vehicle’s value, and how long you plan to keep the car. However, we can identify a "sweet spot" that balances affordability with financial prudence.

For most buyers, a 60-month (5-year) car loan often represents a widely accepted and manageable term. It typically offers a good balance between a reasonable monthly payment and a sensible total interest cost. While shorter terms are almost always better financially, 60 months strikes a practical chord for many middle-income households.

However, if your budget allows, aiming for a 36-month (3-year) or 48-month (4-year) loan is generally the most financially advantageous path. These shorter terms drastically reduce the total interest you pay and help you build equity in your vehicle much faster. Always strive for the shortest term you can comfortably afford without straining your monthly budget.

Key Factors Influencing Your Ideal Car Loan Length

Choosing the right car loan length isn’t just about picking a number; it’s about understanding the financial ecosystem surrounding your purchase. Several critical factors will guide you toward the most appropriate auto loan term.

1. Your Monthly Budget and Affordability

This is arguably the most immediate factor. Before you even look at cars, you need to establish a realistic budget for your monthly car payment. This isn’t just about what you can pay, but what you can comfortably pay without sacrificing other essential expenses or financial goals.

Pro tips from us: Never stretch your budget to fit a more expensive car. A lower monthly payment might seem attractive, but if it comes at the cost of an excessively long loan term, you could be paying far more in the long run. Use an online car loan calculator to see how different loan lengths impact your monthly outflow.

2. The Total Cost of Ownership

Many buyers fall into the trap of focusing solely on the monthly payment. However, a truly smart car purchase considers the total cost of ownership, which includes the vehicle’s price, interest paid, insurance, maintenance, and fuel. A longer loan term significantly increases the interest portion of this total cost.

For example, a $30,000 car financed at 6% interest over 60 months might cost you around $34,800 in total. The same car over 84 months could cost closer to $37,800. That’s a $3,000 difference just in interest.

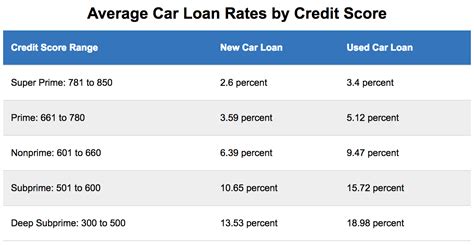

3. Current Interest Rates and Your Credit Score

Your credit score is a major determinant of the interest rate you’ll qualify for. A higher credit score typically translates to a lower interest rate, which can make even slightly longer terms more palatable. Conversely, a lower credit score often means higher interest rates, making shorter terms even more critical to minimize total costs.

Always shop around for the best interest rates before committing to a loan. Don’t just accept the financing offered by the dealership. Independent lenders, credit unions, and banks often have competitive offers.

4. Vehicle Depreciation: The Silent Killer of Value

Cars begin to depreciate the moment you drive them off the lot. Most vehicles lose a significant portion of their value in the first few years. Depreciation plays a critical role in your car loan length decision, particularly concerning negative equity.

A shorter loan term allows you to pay down the principal faster, building equity at a pace that often outruns depreciation. This helps you avoid the dreaded "upside down" scenario, where you owe more on the car than it’s worth.

5. Your Down Payment

A substantial down payment can significantly reduce the amount you need to finance. This, in turn, can allow you to opt for a shorter loan term with manageable monthly payments, or at least reduce the overall interest paid on a longer term.

Common mistakes to avoid are skimping on your down payment or even worse, making no down payment at all. While 0% down loans exist, they often lead to higher interest rates and a greater risk of negative equity early in the loan term. Aim for at least 10-20% down if possible.

6. Vehicle Reliability and Your Ownership Plans

Consider how long you realistically plan to keep the car. If you typically trade in your vehicle every 3-5 years, a loan term much longer than that could be problematic. You might still be paying off the car when you’re ready for a new one, potentially rolling negative equity into your next loan.

Also, think about the vehicle’s expected reliability. Financing an older, less reliable car for an 84-month term means you could still be making payments long after the car has started experiencing significant mechanical issues, adding unexpected repair costs on top of your loan.

A Deeper Dive into Specific Car Loan Lengths

Let’s break down the common car loan lengths and their implications, helping you understand which might be the best fit for your situation.

1. 36-Month (3-Year) Loan

- Pros: This is the gold standard for financially savvy buyers. You’ll pay the least amount of total interest, build equity very quickly, and be debt-free in a relatively short period. Your car will likely still be under warranty for most of the loan term, minimizing unexpected repair costs.

- Cons: The monthly payments will be the highest among all loan terms. This option is typically only feasible for buyers with a strong income and a comfortable budget.

- Who it’s for: Individuals or households with a high disposable income who prioritize minimizing interest costs and paying off debt quickly. If you can afford it, this is almost always the financially smartest choice.

2. 48-Month (4-Year) Loan

- Pros: Offers an excellent balance between manageable monthly payments and significant interest savings compared to longer terms. You’ll still build equity at a good pace and likely pay off the car before major depreciation or out-of-warranty repairs kick in.

- Cons: Monthly payments are still higher than the most common 60-month term, potentially stretching some budgets.

- Who it’s for: Buyers with a solid income who want to keep their total interest costs down without the burden of the highest monthly payments. It’s a very practical and financially sound option for many.

3. 60-Month (5-Year) Loan

- Pros: This is by far the most popular car loan length and often the most widely advertised. It offers significantly lower monthly payments than 36 or 48-month terms, making a broader range of vehicles seem affordable. It’s a sweet spot for many who balance monthly budget with total cost.

- Cons: You’ll pay more in total interest compared to shorter terms. You also build equity slower, increasing the risk of being "upside down" (owing more than the car is worth) during the initial years.

- Who it’s for: The majority of car buyers seeking a manageable monthly payment without extending the loan term to excessive lengths. It’s a reasonable compromise for many.

4. 72-Month (6-Year) Loan

- Pros: Offers significantly lower monthly payments, which can make more expensive vehicles accessible or ease the financial burden on tighter budgets.

- Cons: The total interest paid increases substantially. You are at a much higher risk of being upside down for a considerable portion of the loan term. Your car’s warranty may expire before the loan is paid off, leaving you vulnerable to repair costs while still making payments.

- Who it’s for: This option should be approached with caution. It’s generally considered for buyers who absolutely need lower monthly payments and have made a substantial down payment to mitigate the negative equity risk. Pro tips from us: If you opt for 72 months, ensure your car has excellent reliability and you plan to keep it for the entire loan term, or even longer.

5. 84-Month (7-Year) Loan

- Pros: Provides the absolute lowest possible monthly payments, making nearly any car seem "affordable" on a monthly basis.

- Cons: This is almost universally not recommended by financial experts. The amount of total interest paid is astronomical, and the risk of being upside down for the vast majority of the loan term is extremely high. You’ll likely be making payments long after the car has significantly depreciated, outlived its warranty, and potentially started requiring expensive repairs. The commitment is also incredibly long.

- Who it’s for: In extremely rare circumstances, and only with a very large down payment on a highly reliable vehicle, this might be considered if monthly cash flow is the absolute top priority. Common mistakes to avoid are choosing an 84-month loan simply because it makes a car you can’t truly afford seem within reach. This often leads to long-term financial strain.

The "Upside Down" Trap: Understanding Negative Equity

We’ve mentioned "upside down" a few times, and it’s a critical concept in auto financing. Being "upside down" or having negative equity means you owe more on your car loan than the car is currently worth. This situation is far more common with longer loan terms because the rate at which you pay down the principal is slower than the rate at which the car depreciates, especially in the early years.

Consequences of Negative Equity:

- Difficulty Selling or Trading In: If you try to sell or trade in your car while upside down, you’ll have to pay the difference out of pocket or roll it into your next car loan, perpetuating the cycle of debt.

- Insurance Issues: If your car is totaled or stolen, your insurance payout might not cover the full loan amount, leaving you to pay the remaining balance on a car you no longer have. This is why Gap Insurance is often recommended with longer terms.

Avoiding negative equity is a key reason to opt for a shorter car loan length and make a significant down payment.

Strategies for Choosing Your Ideal Car Loan Length

Now that you understand the factors and implications, let’s outline a strategic approach to selecting your ideal auto loan term.

1. Run the Numbers Thoroughly

Don’t guess. Use an online auto loan calculator to compare different loan terms, interest rates, and down payment amounts. See exactly how each scenario affects your monthly payment and, crucially, the total interest paid. This step is non-negotiable for smart car buying.

2. Budget First, Not Loan Term First

Instead of asking "What loan term gives me the lowest payment?", ask "What monthly payment can I comfortably afford, and what is the shortest loan term that fits that budget?" This mindset shift prioritizes your financial health over perceived affordability.

3. Consider Your Car’s Expected Lifespan and Your Ownership Plans

Align your loan term with how long you realistically expect to own the vehicle. If you’re buying a car known for its longevity and plan to keep it for 7-10 years, a 60-month loan might be fine. If you swap cars every 3-4 years, stick to a 36 or 48-month term to avoid being upside down when you’re ready for your next vehicle.

4. Aim for the Shortest Term Possible

Whenever your budget allows, lean towards a shorter loan term. The financial benefits of reduced interest and faster equity build-up are substantial. Think of it as an investment in your financial future.

5. Make a Larger Down Payment

This is one of the most effective ways to reduce your overall financing costs and gain flexibility with your loan term. A larger down payment means you borrow less, which translates to lower monthly payments and less interest paid over the life of the loan. It also helps mitigate the risk of negative equity.

6. Explore Refinancing Options

Life circumstances change, and sometimes your initial loan term might not be ideal down the road. If your credit score improves or interest rates drop, consider refinancing your car loan. This could allow you to shorten your loan term or secure a lower interest rate, saving you money in the long run.

Pro Tips for Smart Car Financing

Beyond choosing the right loan length, here are some expert insights to enhance your auto financing journey:

- Get Pre-Approved: Obtain pre-approval from banks or credit unions before you even step foot in a dealership. This gives you a benchmark interest rate and empowers you to negotiate financing with confidence.

- Understand All Fees: Beyond the interest rate, be aware of any origination fees, documentation fees, or other charges that might be rolled into your loan. Transparency is key.

- Don’t Forget About Other Costs: Your car payment isn’t your only car expense. Factor in insurance, fuel, maintenance, and potential repair costs when setting your overall car budget.

- Negotiate the Car Price First: Always negotiate the vehicle’s purchase price independently of the financing. Once you have a firm price, then discuss loan terms and interest rates. Combining these negotiations can confuse the process and potentially lead to a less favorable outcome. For more insights on getting the best deal, check out our guide on ‘Negotiating Your Car Price Like a Pro’.

- Boost Your Credit Score: A higher credit score can unlock significantly better interest rates, directly impacting your total loan cost and potentially allowing you a shorter, more favorable loan term. And if you’re wondering how your credit score plays a role, our article ‘Boosting Your Credit Score for a Car Loan’ has all the answers.

Common Mistakes to Avoid When Choosing Your Car Loan Length

Learning from the missteps of others is a valuable part of making informed decisions. Here are some common pitfalls to steer clear of:

- Focusing Only on the Monthly Payment: This is the most prevalent mistake. A low monthly payment might feel good initially, but if it’s achieved by stretching the loan term to 7 or 8 years, you’re likely paying thousands more in interest.

- Stretching the Loan Term Excessively: While a longer term makes a car "affordable," it can quickly lead to negative equity and significant overspending on interest. Resist the temptation to take the longest term available.

- Not Factoring in Depreciation: Ignoring how quickly a car loses value can lead to being upside down, creating financial headaches if you need to sell or trade in early.

- Skipping a Down Payment: While convenient, zero down payment loans often result in higher interest rates, larger monthly payments (for a given term), and a greater risk of negative equity.

- Not Shopping Around for Rates: Accepting the first financing offer, especially from a dealership, can cost you hundreds or even thousands of dollars over the life of the loan. Always compare offers from multiple lenders. For a deeper understanding of current auto loan rates and trends, you can refer to trusted financial resources like Bankrate’s auto loan guides.

Conclusion: Make an Informed Decision on Your Car Loan Length

Choosing the recommended car loan length is a pivotal decision in your car buying journey. It’s a balancing act between immediate affordability and long-term financial prudence. While a 60-month loan often serves as a practical benchmark, aiming for a shorter term like 36 or 48 months, if your budget allows, is almost always the more financially intelligent choice.

By understanding the interplay of interest rates, depreciation, your budget, and the total cost of ownership, you can confidently select an auto loan term that serves your needs without compromising your financial stability. Remember, a smart car purchase isn’t just about the car itself; it’s about making wise financial decisions that leave you in a better position down the road. Drive smart, not just fast!