The Ultimate Guide to Saving Big: How to Pay Less Interest on Your Car Loan

The Ultimate Guide to Saving Big: How to Pay Less Interest on Your Car Loan Carloan.Guidemechanic.com

For many, a car is an absolute necessity, and for most, that necessity comes with a car loan. While the excitement of a new vehicle is undeniable, the reality of interest payments can quickly dampen the thrill. High interest rates can add hundreds, even thousands, of dollars to the total cost of your car over the life of the loan, eating into your budget and delaying other financial goals.

But what if there was a way to significantly reduce that burden? What if you could take control and pay less interest on your car loan, saving yourself a substantial amount of money? The good news is, you absolutely can. This comprehensive guide, crafted from years of financial expertise, will break down actionable strategies that empower you to minimize the interest you pay, whether you’re about to buy a car or already have a loan.

The Ultimate Guide to Saving Big: How to Pay Less Interest on Your Car Loan

Our mission here is to equip you with the knowledge and tools to make smart financial decisions. By understanding the mechanics of car loan interest and applying proven techniques, you’ll not only save money but also build a stronger financial future. Let’s dive in and unlock the secrets to lower car loan interest.

Understanding Car Loan Interest: The Basics You Need to Know

Before we can strategize on how to pay less interest, it’s crucial to understand what interest is and how it’s calculated on a car loan. Essentially, interest is the cost of borrowing money. Lenders charge interest as a fee for letting you use their capital to purchase your vehicle. This fee is typically expressed as an annual percentage rate (APR).

The APR isn’t just the interest rate; it also includes certain fees associated with the loan, giving you a more complete picture of the total cost of borrowing. A higher APR means you’ll pay more for the privilege of borrowing. Your monthly payment is largely comprised of two parts: a portion that goes towards reducing your principal balance (the original amount you borrowed) and a portion that covers the interest charged.

Several key factors heavily influence the interest rate you’ll be offered. These include your credit score, the loan term (how long you have to pay it back), the size of your down payment, and even the type of lender you choose. Understanding these elements is the very first step in gaining control over your car loan costs. Based on my experience, many people overlook these fundamental aspects, leading to higher interest payments than necessary.

Strategy 1: Boost Your Credit Score Before You Apply

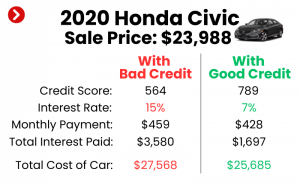

Your credit score is arguably the most critical factor influencing the interest rate you’ll receive on a car loan. Lenders use this three-digit number to assess your creditworthiness – essentially, how risky you are as a borrower. A higher credit score signals to lenders that you are responsible with credit and are likely to repay your loan on time, resulting in them offering you lower interest rates.

Conversely, a lower credit score suggests a higher risk, prompting lenders to charge a higher interest rate to compensate for that perceived risk. This difference can be substantial, often translating to thousands of dollars in extra interest paid over the life of the loan. Therefore, improving your credit score should be one of your top priorities before you even step foot in a dealership.

How to improve your credit score:

- Pay Your Bills On Time, Every Time: Payment history is the most significant component of your credit score. Missing payments, even by a few days, can severely damage your score. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Your Credit Utilization Ratio: This ratio compares the amount of credit you’re using to your total available credit. Aim to keep this below 30% on all your credit cards. Paying down existing credit card debt can quickly boost this ratio.

- Check Your Credit Report for Errors: Mistakes on your credit report can unfairly lower your score. Obtain a free copy of your credit report from each of the three major bureaus (Experian, Equifax, TransUnion) annually. If you find errors, dispute them immediately. You can get your free reports at AnnualCreditReport.com, an official source.

- Avoid Opening New Credit Accounts: Applying for multiple lines of credit in a short period can temporarily ding your score. New credit inquiries suggest you might be taking on too much debt.

- Don’t Close Old Accounts: The length of your credit history also plays a role. Older accounts, especially those in good standing, demonstrate a long track record of responsible borrowing.

Pro tip from us: Start this process months, if not a year, in advance of your car purchase. Building good credit takes time and consistent effort, but the savings on your car loan interest will be well worth it.

Strategy 2: Make a Substantial Down Payment

One of the most straightforward ways to reduce the interest you pay is to simply borrow less money in the first place. This is where a substantial down payment comes into play. A down payment is the initial amount of money you pay upfront for the car, which reduces the total amount you need to finance.

When you make a larger down payment, your principal loan amount decreases. Since interest is calculated on the principal balance, a smaller principal automatically means less interest accruing over time. It also signals to lenders that you have some skin in the game, making you a less risky borrower, which can sometimes lead to a slightly better interest rate offer.

While there’s no magic number, experts often recommend a down payment of at least 10-20% of the car’s purchase price. For example, on a $30,000 car, a 20% down payment would be $6,000, meaning you’d only finance $24,000. This significantly reduces your overall interest payments compared to financing the full $30,000. Common mistake to avoid is stretching yourself too thin by putting down too much, leaving you with no emergency savings. Find a balance that works for your budget.

Strategy 3: Shorten Your Loan Term

Car loan terms can range anywhere from 24 months to 84 months, or even longer. While a longer loan term might offer the appeal of lower monthly payments, it’s a financial illusion that costs you more in the long run. The longer you stretch out your payments, the more interest you’ll accrue over the life of the loan.

Think of it this way: with a longer term, you’re paying interest on the outstanding principal for a greater number of months. Even if the interest rate is the same, the sheer duration of the loan significantly increases the total interest paid. A shorter loan term means you pay off the principal faster, reducing the total amount of time interest has to accumulate.

The trade-off, of course, is that shorter loan terms typically come with higher monthly payments. You need to ensure that these higher payments are comfortably within your budget, allowing you to meet your financial obligations without strain. From my observations, people often choose longer terms for lower payments, without fully calculating the true cost. Run the numbers with a loan calculator to see the dramatic difference in total interest paid between a 48-month loan and a 72-month loan for the same principal and interest rate.

Strategy 4: Shop Around for Lenders (Don’t Settle!)

One of the biggest mistakes car buyers make is accepting the first financing offer they receive, often from the dealership. While convenient, dealership financing isn’t always the best deal. Just as you would shop around for the best price on a car, you should absolutely shop around for the best car loan.

Different lenders have different criteria and offer varying interest rates. Banks, credit unions, and online lenders all compete for your business, and this competition can work in your favor. Credit unions, in particular, are often known for offering highly competitive rates to their members.

Start by getting pre-qualified with several lenders before you even visit a dealership. Pre-qualification involves a soft credit pull, which won’t impact your credit score, and gives you an estimate of the interest rate you might receive. Having these pre-approved offers in hand gives you significant leverage at the dealership. You can use their offer to negotiate for an even better rate, or simply go with the outside lender if their terms are superior. For more tips on choosing the right lender, check out our guide on .

Strategy 5: Consider Refinancing Your Existing Car Loan

If you already have a car loan and feel like you’re paying too much interest, refinancing could be a game-changer. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms. This strategy is particularly effective if your credit score has improved since you first took out the loan, or if interest rates have generally dropped.

Many people refinance for several reasons: to secure a lower interest rate, to reduce their monthly payments (by extending the loan term, though this increases total interest), or to shorten their loan term (which increases monthly payments but reduces total interest). If your goal is to pay less interest, then refinancing to a lower rate and/or a shorter term is the way to go.

The refinancing process is similar to applying for an original loan. You’ll apply with various lenders, who will review your creditworthiness and the value of your vehicle. Be aware that some lenders might charge a refinancing fee, so factor that into your calculations to ensure the savings from a lower interest rate still make it worthwhile. Based on my experience, refinancing can be a game-changer for those who didn’t get the best deal initially or whose financial situation has significantly improved.

Strategy 6: Make Extra Payments Whenever Possible

This strategy might seem obvious, but its impact on reducing total interest paid is often underestimated. Paying more than your minimum monthly payment, even a small amount, can significantly accelerate the payoff of your car loan and drastically cut down on interest costs. Every extra dollar you pay typically goes directly towards reducing your principal balance.

Since interest is calculated on your outstanding principal, lowering that balance faster means less interest accrues over the remaining life of the loan. You can make extra payments in several ways:

- Round Up Your Payment: If your payment is $347, pay $350 or $375.

- Bi-Weekly Payments: Instead of one monthly payment, pay half of your payment every two weeks. This results in 26 half-payments per year, effectively making one extra full payment annually.

- Lump Sum Payments: Use bonuses, tax refunds, or other unexpected windfalls to make a significant extra payment.

- Direct Extra Payments to Principal: Always confirm with your lender that any extra payments are applied directly to the principal balance, not just counted as a pre-payment for future months’ regular payments.

Pro tip: Even small, consistent extra payments add up significantly over time. Automate an extra $25 or $50 to be paid with each monthly installment, and you’ll be amazed at the savings.

Strategy 7: Negotiate the Car Price, Not Just the Loan

This strategy is foundational yet frequently overlooked when focusing solely on interest rates. The lower the actual purchase price of the car, the less money you will need to borrow. And if you borrow less money, then by definition, you will pay less interest, regardless of the interest rate you secure.

Think of it this way: a $2,000 reduction in the car’s price directly translates to a $2,000 reduction in your principal loan amount. This saves you interest on that $2,000 for the entire term of your loan. Therefore, mastering your negotiation skills at the dealership is just as important as securing a low APR.

Tips for negotiating the car price:

- Do Your Research: Know the fair market value of the car you want before you go to the dealership. Use sites like Kelley Blue Book or Edmunds.

- Separate Negotiation: Try to negotiate the car’s price first, before discussing financing. Dealers often try to bundle these, which can make it harder to see the true cost of each.

- Be Prepared to Walk Away: Having the confidence to leave if the deal isn’t right is your strongest negotiation tool.

- Consider Used Cars: Often, buying a slightly used car can save you a significant amount on the purchase price, further reducing your loan principal and overall interest paid.

To master your negotiation skills, read our comprehensive article on .

Strategy 8: Avoid Add-ons and Extended Warranties (Unless Absolutely Necessary)

When you’re finalizing your car purchase, dealers often present a long list of add-ons: extended warranties, rustproofing, paint protection, fabric protection, GAP insurance, and more. While some of these might have legitimate value for certain buyers, many are significantly marked up and serve primarily to boost the dealer’s profit.

The critical point here is that if you roll the cost of these add-ons into your car loan, you are paying interest on them for the entire duration of your loan. An extended warranty costing $2,000 might seem like a small addition to your overall loan, but if you’re paying 6% interest on that $2,000 for five years, it adds extra cost without providing any immediate tangible benefit.

Carefully assess the true value of each add-on. If you decide you need an extended warranty, research third-party providers, as they often offer better coverage at a lower price than dealer-offered options. Common mistake: Getting pressured into expensive add-ons during the finance manager’s pitch without truly understanding their necessity or the added interest cost. Always ask for these costs to be itemized and consider them separately from the car’s price.

Strategy 9: Set Up Automatic Payments and Payment Reminders

While this strategy doesn’t directly reduce your interest rate, it plays a crucial role in preventing additional costs that can erode your savings. Setting up automatic payments ensures that your car loan payment is made on time, every single month. This prevents late fees, which can quickly add up, and more importantly, it protects your credit score.

Missing payments or making them late can severely damage your credit score, making it harder to get favorable rates on future loans (including potential refinancing). Some lenders even offer a slight interest rate discount (e.g., 0.25%) for customers who enroll in automatic payments. While seemingly small, every little bit helps in reducing your total interest paid.

Beyond preventing penalties, consistent on-time payments contribute positively to your credit history, strengthening your financial profile over time. This makes you a more attractive borrower, potentially unlocking even better interest rates if you decide to refinance in the future. Make it a habit: set it and forget it, or at least set up reliable reminders to ensure punctuality.

Common Mistakes to Avoid When Aiming for Lower Interest

Even with the best intentions, it’s easy to fall into common traps that can lead to paying more interest than necessary. Being aware of these pitfalls can help you navigate the car buying and loan management process more effectively:

- Focusing Only on the Monthly Payment: This is perhaps the most significant mistake. Dealerships often try to "sell" you on a monthly payment amount, rather than the total cost of the car and loan. A low monthly payment often means a longer loan term, leading to significantly more interest paid over time. Always ask for the total price, total interest, and total cost of the loan.

- Not Shopping Around for Loans: As discussed, accepting the first financing offer you get is a sure way to miss out on potentially lower rates. Always compare offers from multiple lenders.

- Ignoring Your Credit Score: Your credit score is your financial passport. Neglecting it before applying for a loan will almost certainly result in higher interest rates. Invest time in improving it.

- Not Reading the Fine Print: Always read your loan agreement thoroughly. Understand all fees, the exact interest rate, the loan term, and any prepayment penalties (though these are less common with car loans today). Don’t sign anything you don’t fully understand.

- Rolling Negative Equity into a New Loan: If you’re trading in a car that you owe more on than it’s worth (negative equity), rolling that balance into your new loan immediately puts you underwater and increases your principal, leading to more interest. Try to pay off negative equity separately if possible.

Conclusion: Take Control of Your Car Loan Interest

Paying less interest on your car loan isn’t about finding a secret loophole; it’s about being informed, strategic, and proactive. By understanding the factors that influence your interest rate and implementing the nine powerful strategies outlined in this guide, you can significantly reduce the total cost of your vehicle.

From boosting your credit score and making a solid down payment to shopping for the best lenders and making extra payments, each step contributes to substantial savings. Whether you’re in the market for a new car or looking to optimize an existing loan through refinancing, the power to pay less interest is firmly in your hands.

Don’t let high interest rates dictate your financial future. Take control, apply these expert-backed strategies, and enjoy the satisfaction of saving big on one of your most significant purchases. Start implementing these tips today, and watch your car loan become a manageable expense rather than a financial burden. Your wallet will thank you!