The Ultimate Guide to Securing a $50,000 Car Loan: Your Path to High-End Wheels

The Ultimate Guide to Securing a $50,000 Car Loan: Your Path to High-End Wheels Carloan.Guidemechanic.com

Dreaming of a new luxury SUV, a powerful sports car, or a feature-packed family vehicle that commands a $50,000 price tag? For many, securing a car loan of this magnitude can seem like a daunting challenge. However, with the right knowledge and strategic approach, financing a significant vehicle purchase is absolutely within reach.

This comprehensive guide is designed to empower you with everything you need to know about navigating the landscape of a $50,000 car loan. We’ll delve deep into the requirements, the application process, and expert tips to ensure you not only get approved but also secure the best possible terms. Our goal is to make this complex financial journey clear, manageable, and ultimately, successful for you.

The Ultimate Guide to Securing a $50,000 Car Loan: Your Path to High-End Wheels

Understanding the Landscape of a $50,000 Car Loan

A $50,000 car loan isn’t your average vehicle financing. This amount typically signifies a commitment to a premium vehicle, often a brand-new model, a high-spec SUV, a luxury sedan, or a robust truck. It requires a more robust financial profile and a clearer understanding of the lending process compared to smaller loan amounts.

Securing a $50,000 car loan means you’re looking for a substantial investment. Lenders view this as a higher-risk loan, which in turn means they will scrutinize your financial health more thoroughly. This isn’t just about affording the monthly payments; it’s about demonstrating long-term financial stability and a strong history of responsible borrowing.

Based on my experience in the automotive financing sector, buyers seeking this level of loan are often looking for specific features. These might include advanced safety technologies, superior performance, luxurious interiors, or enhanced reliability that comes with a higher price point. Understanding your "why" behind this significant purchase can help you stay focused throughout the process.

Key Pillars for Securing Your $50,000 Car Loan Approval

When applying for a substantial car loan of $50,000, lenders will assess several critical factors. These pillars determine your eligibility, the interest rate you’ll receive, and the overall terms of your loan. Mastering these aspects is paramount to a successful application.

1. Your Credit Score: The Foundation of Trust

Your credit score is arguably the most crucial factor when seeking a large car loan. It’s a three-digit number that represents your creditworthiness to lenders. A higher score indicates a lower risk, making lenders more willing to offer favorable terms.

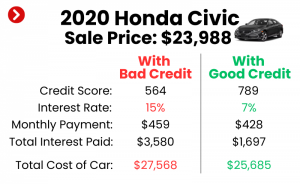

For a $50,000 car loan, you’ll ideally want a strong credit score. Generally, a FICO score of 700 or above is considered good, while scores above 760 are excellent. These scores unlock the lowest interest rates and the most flexible terms, significantly reducing your total cost of borrowing.

Common mistakes to avoid here include not checking your credit score before applying. Discrepancies or errors on your credit report can negatively impact your score, so it’s vital to review it periodically. You can get a free credit report from each of the three major bureaus (Experian, Equifax, TransUnion) annually.

2. Income and Debt-to-Income (DTI) Ratio: Can You Afford It?

Lenders need assurance that you have the income to comfortably manage the monthly payments for a 50000 car loan. They’ll look at your gross monthly income and your existing debt obligations. Your debt-to-income (DTI) ratio is a key metric they use.

Your DTI ratio is calculated by dividing your total monthly debt payments (including the prospective car payment) by your gross monthly income. Most lenders prefer a DTI ratio of 36% or less, though some might go up to 43% for well-qualified borrowers. A lower DTI indicates that you have more disposable income available for loan repayment.

Pro tips from us: Before applying, calculate your current DTI. If it’s on the higher side, consider paying down some existing debts to improve this ratio. This proactive step can significantly strengthen your application for a large car loan.

3. The Power of a Down Payment: Reducing Risk, Increasing Approval

A substantial down payment is a powerful tool when seeking a $50,000 car loan. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan. More importantly, it signals to lenders that you are financially committed to the purchase.

Lenders view a significant down payment as a risk mitigator. If you put down 10% to 20% or more, you’re immediately reducing the loan-to-value (LTV) ratio of the vehicle. This makes the loan less risky for the lender, potentially leading to better interest rates and easier approval.

Based on my experience, putting down at least 10% on a $50,000 vehicle is highly recommended, aiming for 20% if possible. This not only makes your loan more attractive to lenders but also helps you avoid being "upside down" on your loan (owing more than the car is worth) early in its term.

4. Vehicle Choice and Its Impact on Your Loan

The specific vehicle you choose plays a role in your 50000 car loan approval. Lenders typically prefer financing new or late-model used cars from reputable brands. These vehicles hold their value better, making them less risky as collateral.

An older or less reliable vehicle, even if it falls into the $50,000 price range, might present a higher risk to lenders. They consider the car’s resale value and its potential as collateral if you default on the loan. Newer vehicles generally have a more predictable depreciation schedule.

Ensure the vehicle you select aligns with the loan amount and your overall financial profile. A lender might be hesitant to approve a $50,000 loan for a car that historically has poor resale value or high maintenance costs, as these factors could impact your ability to repay.

5. Loan Term: Balancing Monthly Payments and Total Cost

The loan term, or the length of time you have to repay the loan, is another critical consideration for a $50,000 car loan. Common terms range from 36 to 84 months. While a longer term means lower monthly payments, it also means paying more in total interest over the life of the loan.

For example, extending a loan from 60 months to 72 months can reduce your monthly payment significantly. However, you’ll be paying interest for an additional year, which adds up. It’s a delicate balance between affordability and the total cost of the loan.

Pro tips from us: Always consider the total cost of the loan, not just the monthly payment. Use online calculators to compare different loan terms and see how they impact your overall expenditure. Aim for the shortest term you can comfortably afford without straining your budget.

The Application Process: Your Step-by-Step Guide to a $50,000 Car Loan

Navigating the application process for a $50,000 car loan can be straightforward if you’re prepared. Here’s a step-by-step guide to ensure a smooth and successful experience.

1. Assess Your Financial Health and Set a Realistic Budget

Before even looking at cars, take a deep dive into your finances. Understand your monthly income, fixed expenses, and discretionary spending. Determine how much you can truly afford for a monthly car payment, factoring in insurance, fuel, and maintenance.

Common mistakes to avoid are underestimating additional car ownership costs. A $50,000 car often comes with higher insurance premiums and potentially more expensive parts and service. Be realistic about your budget to prevent financial strain down the line.

2. Get Pre-Approved: Your Secret Weapon

One of the most powerful steps you can take is to get pre-approved for your 50000 car loan. Pre-approval means a lender has reviewed your financial information and provisionally agreed to lend you a specific amount at a certain interest rate. This is a game-changer.

Getting pre-approved gives you significant leverage at the dealership. You walk in as a cash buyer, knowing exactly how much you can spend and what your interest rate will be. This separates the financing negotiation from the car price negotiation, often leading to a better deal on both fronts. To learn more about the advantages, check out our article on Car Loan Pre-Approval Benefits.

3. Gather Necessary Documents

Lenders will require various documents to verify your identity, income, and financial stability. Having these ready will expedite the application process.

Typically, you’ll need:

- Proof of Identity: Driver’s license, passport.

- Proof of Income: Pay stubs (recent 2-3 months), W-2 forms, tax returns (if self-employed).

- Proof of Residency: Utility bill, lease agreement.

- Credit History: Lenders will pull this, but having reviewed your own is smart.

- Vehicle Information: Once you’ve chosen a car, details like VIN, make, model, and mileage will be required.

4. Shop Around for Lenders: Don’t Settle for the First Offer

Just as you’d shop for the best car, you should shop for the best loan. Don’t limit yourself to the dealership’s financing options immediately. Explore various lenders:

- Banks: Traditional financial institutions often offer competitive rates to existing customers.

- Credit Unions: Known for typically lower interest rates and more personalized service due to their member-owned structure.

- Online Lenders: Many reputable online platforms specialize in car loans and can offer quick approvals and competitive rates.

- Dealership Financing: While often convenient, compare their offers against your pre-approval to ensure you’re getting a good deal.

Based on my experience, applying to multiple lenders within a short window (typically 14-30 days) will count as a single hard inquiry on your credit report. This allows you to rate shop without significantly harming your credit score.

5. Choose Your Vehicle Wisely

With your pre-approval in hand, you can now confidently shop for your $50,000 vehicle. Focus on finding a car that not only meets your needs and desires but also fits comfortably within your budget, including insurance and running costs. Remember, the loan amount is just one piece of the financial puzzle.

6. Finalize the Deal: Read Every Word

Once you’ve chosen your vehicle and lender, it’s time to finalize the paperwork. This is where attention to detail is crucial. Carefully read every clause in the loan agreement.

Pro tips from us: Pay close attention to the Annual Percentage Rate (APR), total loan amount, payment schedule, and any early repayment penalties. Ensure there are no hidden fees or unexpected charges. If something isn’t clear, ask for clarification before signing.

Optimizing Your Loan Terms and Saving Money

Securing approval for a $50,000 car loan is a major achievement, but the work doesn’t stop there. Optimizing your loan terms can save you thousands of dollars over the life of the loan.

Negotiating Interest Rates: It’s Possible!

Many people don’t realize that interest rates are often negotiable, especially if you have excellent credit and a pre-approval in hand. Use competing offers from different lenders as leverage. If one lender offers a lower rate, see if your preferred lender can match or beat it.

Show them your best offer from another institution and politely ask if they can improve their terms. This strategy can significantly reduce your monthly payments and total interest paid on your 50000 car loan.

Understanding APR vs. Interest Rate

While often used interchangeably, the interest rate and Annual Percentage Rate (APR) are different. The interest rate is the cost of borrowing money, expressed as a percentage. The APR includes the interest rate plus any additional fees associated with the loan, such as administrative fees.

Always focus on the APR when comparing loan offers. It gives you a more accurate picture of the total cost of borrowing. A loan with a slightly lower interest rate but higher fees might actually have a higher APR than a loan with a slightly higher interest rate and no fees.

Refinancing Options: A Future Strategy

Even after you’ve secured your $50,000 car loan, keep an eye on interest rates. If market rates drop, or if your credit score significantly improves after a year or two of on-time payments, you might be able to refinance your car loan.

Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms. This can reduce your monthly payments or the total interest paid over the remaining term. This is a smart move for long-term savings.

Add-ons and Extras: What to Watch Out For

Dealerships often present various add-ons and extras during the financing process, such as extended warranties, gap insurance, paint protection, or VIN etching. While some might be valuable, others can be overpriced and unnecessary.

Common mistakes to avoid: Don’t feel pressured to buy these at the time of purchase. Research each add-on individually. Extended warranties, for instance, can often be purchased cheaper directly from the manufacturer or a third-party provider later. Gap insurance, however, can be a wise investment for a large car loan as it covers the difference if your car is totaled and you owe more than its market value.

Common Mistakes to Avoid When Getting a $50,000 Car Loan

Navigating a substantial loan like a $50,000 car loan requires careful planning. Avoiding common pitfalls can save you money, stress, and potential long-term financial headaches.

- Not Getting Pre-Approved: As discussed, skipping pre-approval means losing significant negotiation power and potentially accepting a higher interest rate. It’s one of the biggest mistakes borrowers make.

- Ignoring Your Budget: Falling in love with a car that’s outside your comfortable price range is easy. But committing to payments you can’t truly afford leads to financial strain and potential default. Always prioritize what you can afford over what you want.

- Focusing Only on Monthly Payments: Dealerships love to talk about low monthly payments by extending the loan term. While attractive, this often means paying substantially more in total interest. Always ask for the total cost of the loan over its lifetime.

- Not Checking Your Credit Report: Errors on your credit report can needlessly inflate your interest rate. Check your report well in advance, dispute any inaccuracies, and ensure your credit score accurately reflects your financial history. You can get free copies of your credit report from AnnualCreditReport.com, an external source recommended for this purpose.

- Skipping the Test Drive and Pre-Purchase Inspection: For any car, especially one worth $50,000, a thorough test drive is crucial. For used vehicles, a pre-purchase inspection by an independent mechanic can uncover hidden issues, saving you from buying a lemon.

- Not Understanding the Full Contract: Signing paperwork without fully comprehending every term, condition, and fee is a recipe for regret. Take your time, ask questions, and never sign anything you don’t understand.

Pro Tips from an Expert for Your $50,000 Car Loan

Based on my years in the industry, here are some actionable pro tips to ensure you have the best possible experience when securing a $50,000 car loan:

- Build a Strong Financial Profile: Start early. If you’re planning a large purchase, work on improving your credit score, reducing your DTI, and saving for a larger down payment well in advance. These efforts will pay dividends.

- Consider a Co-signer Strategically: If your credit isn’t stellar, or your DTI is high, a co-signer with excellent credit can help you get approved or secure a better rate. However, ensure both parties understand the full responsibility; the co-signer is equally liable for the loan. This should only be a consideration if absolutely necessary.

- Read the Fine Print on Everything: From the initial loan offer to the final sales contract, every detail matters. Don’t rush through it. Pay particular attention to interest rates, fees, penalties, and any clauses regarding early payoff.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, if the numbers don’t add up, or if you feel pressured, be prepared to walk away. There will always be another car and another deal. Your financial well-being is more important than any single purchase.

- Future-Proof Your Finances: Consider the long-term implications of a 50000 car loan. How will it affect your ability to save for a home, retirement, or other financial goals? Ensure this purchase aligns with your broader financial plan.

What if Your Credit Isn’t Perfect?

While a high credit score is ideal for a $50,000 car loan, it’s not always a deal-breaker if your credit isn’t perfect. However, you should be prepared for certain realities:

- Higher Interest Rates: Lenders will offset the increased risk with a higher interest rate. This will significantly increase the total cost of your loan.

- Larger Down Payment Required: You might need to make a more substantial down payment to demonstrate commitment and reduce the loan-to-value ratio for the lender.

- Shorter Loan Terms: Lenders might offer shorter loan terms to reduce their exposure to risk.

- Co-signer Option: As mentioned, a co-signer with excellent credit can be a viable path to approval.

- Focus on Improving Credit First: Pro tips from us: If your credit is truly struggling, consider delaying your large car loan purchase. Focus on improving your credit score by paying bills on time, reducing debt, and correcting any errors on your credit report. This foundational work will save you significant money in the long run. To learn more about building your credit, read our article on Understanding Your Credit Score.

Your Road Ahead: Driving Off with Confidence

Securing a $50,000 car loan is a significant financial undertaking, but with diligent preparation and a strategic approach, it’s an entirely achievable goal. By understanding the key factors lenders consider, meticulously preparing your application, and proactively optimizing your loan terms, you can confidently drive away in the vehicle of your dreams.

Remember, this isn’t just about getting approved; it’s about securing a loan that aligns with your financial well-being. Focus on your credit score, manage your debt-to-income ratio, save for a solid down payment, and shop around for the best rates. With these insights, you’re well-equipped to make an informed decision and embark on your journey with financial peace of mind. Drive safely and wisely!