The Ultimate Guide to Securing a $70,000 Car Loan: Your Path to Luxury Car Financing

The Ultimate Guide to Securing a $70,000 Car Loan: Your Path to Luxury Car Financing Carloan.Guidemechanic.com

The allure of a high-performance vehicle, a luxury SUV, or a premium sedan is a dream for many. When that dream car comes with a price tag around $70,000, it’s an exciting prospect that also brings significant financial considerations. Securing a car loan of this magnitude requires careful planning, a solid understanding of the financing landscape, and strategic execution. It’s not just about making a monthly payment; it’s about making a smart investment.

This comprehensive guide is designed to be your definitive resource for navigating the complexities of a $70,000 car loan. We’ll delve deep into every aspect, from understanding what lenders look for to mastering the application process and avoiding common pitfalls. Our goal is to equip you with the knowledge and confidence needed to not only get your car loan approved but also to secure the most favorable terms possible for your luxury car financing.

The Ultimate Guide to Securing a $70,000 Car Loan: Your Path to Luxury Car Financing

Understanding the Landscape of a $70,000 Car Loan

A $70,000 car loan represents a substantial financial commitment, moving you into a category of vehicles that offer superior performance, advanced technology, and luxurious comfort. This price point typically includes high-end models from brands like BMW, Mercedes-Benz, Audi, Lexus, or well-equipped versions of larger SUVs and sports cars. Financing a vehicle of this value is different from a standard car purchase, demanding a more robust financial profile and a more thorough approach to the loan process.

When you’re considering a high-value car loan like this, it’s crucial to understand that lenders will scrutinize your financial health more closely. They want to ensure you have the capacity to manage such a significant debt alongside your existing financial obligations. This means preparing yourself for a rigorous evaluation of your creditworthiness, income stability, and overall debt load.

The Pillars of Car Loan Approval: What Lenders Look For

Lenders assess several critical factors when evaluating an application for a $70,000 car loan. Understanding these pillars is the first step toward building a strong case for approval and securing competitive rates. Each element plays a vital role in painting a complete picture of your financial reliability.

Your Credit Score: The Unsung Hero

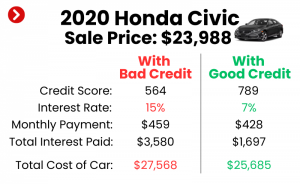

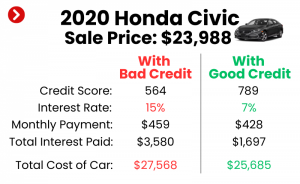

Your credit score is arguably the single most influential factor in securing any loan, especially one of this size. It acts as a financial report card, indicating your history of managing debt responsibly. For a $70,000 car loan, lenders typically look for excellent or very good credit scores, usually in the range of 700 or higher. A higher score signifies a lower risk to the lender, which translates directly into better interest rates and more favorable loan terms.

Based on my experience, individuals with credit scores below 680 might find it challenging to get approved for such a large loan at competitive rates. While approval is still possible, you might face higher interest rates, which significantly increases the total cost of the car over the loan term. It’s not just about getting approved; it’s about getting approved with terms that don’t burden you excessively.

Income and Debt-to-Income (DTI) Ratio: Can You Afford It?

Lenders need assurance that you have a stable and sufficient income to comfortably make your monthly car loan payments, in addition to all your other financial obligations. They will assess your gross monthly income and compare it against your total monthly debt payments. This calculation yields your debt-to-income (DTI) ratio.

Pro tips from us: Most lenders prefer a DTI ratio of 36% or lower, though some might go up to 43% for well-qualified applicants. For a $70,000 car loan, demonstrating a strong income relative to your existing debts is paramount. If your DTI is too high, it signals to lenders that adding another significant payment could stretch your finances too thin, increasing the risk of default.

The Power of a Substantial Down Payment

Making a significant down payment is one of the most effective strategies to strengthen your loan application. A larger down payment reduces the total amount you need to borrow, which in turn lowers your monthly payments and the overall interest paid over the life of the loan. More importantly, it demonstrates your commitment and reduces the lender’s risk.

For a $70,000 car loan, aiming for a down payment of at least 15-20% is highly recommended. This means putting down $10,500 to $14,000. Not only does this make your loan more attractive to lenders, but it also helps you avoid being "upside down" on your loan, where you owe more than the car is worth, especially considering vehicle depreciation.

Loan Term: Balancing Affordability and Total Cost

The loan term, or the length of time you have to repay the loan, significantly impacts your monthly payment and the total interest you’ll pay. Shorter terms typically mean higher monthly payments but less interest over time. Longer terms, while offering lower monthly payments, can lead to substantially more interest paid and a longer period of indebtedness.

Common mistakes to avoid are automatically opting for the longest possible loan term (e.g., 72 or 84 months) just to achieve the lowest monthly payment. While it might seem affordable in the short term, this strategy can drastically increase the total cost of your $70,000 car loan. It also means you’ll be making payments for many years, potentially past the point where the car still feels "new" or even before you’re ready to trade it in.

Vehicle Choice and Depreciation

Lenders also consider the value of the asset you’re financing. A $70,000 car will inevitably depreciate over time. Lenders assess the car’s expected depreciation and its loan-to-value (LTV) ratio to ensure that their investment is protected. If the car rapidly loses value, it could impact their ability to recoup losses if you default.

Some luxury or high-performance vehicles hold their value better than others. Researching the depreciation trends of your chosen vehicle can be beneficial. A car with strong resale value is generally more appealing to lenders, as it maintains a higher collateral value throughout the loan term.

Preparing for Your $70,000 Car Loan Application

Preparation is key to a smooth and successful car loan approval process. By getting your financial ducks in a row before you even start looking at cars, you put yourself in a position of strength.

Get Your Financial House in Order

Before applying for a $70,000 car loan, pull your credit reports from all three major bureaus (Experian, TransUnion, and Equifax). Review them meticulously for any errors or inaccuracies that could negatively impact your score. Dispute any discrepancies immediately. Knowing your current credit score gives you a realistic idea of where you stand and what kind of rates you might expect.

It’s also a good time to reduce any outstanding high-interest debt, such as credit card balances. Lowering your credit utilization ratio can positively impact your credit score and improve your DTI, making you a more attractive borrower. for more detailed strategies.

Budgeting Beyond the Monthly Payment

The cost of owning a $70,000 car extends far beyond the monthly loan payment. You must factor in insurance, maintenance, fuel, registration fees, and potential repair costs. Luxury vehicles often come with higher insurance premiums and more expensive parts and labor for servicing.

Create a realistic budget that accounts for all these additional expenses. Can you comfortably afford the car loan payment and all the associated ownership costs without straining your finances? Overlooking these details is a common pitfall that can lead to financial stress down the road.

Gathering Essential Documents

When you’re ready to apply, having all your documentation prepared will streamline the process. Typically, you’ll need:

- Proof of Identity: Driver’s license, passport.

- Proof of Residence: Utility bill, lease agreement.

- Proof of Income: Pay stubs (last few months), W-2 forms, tax returns (if self-employed), bank statements.

- Proof of Down Payment Funds: Bank statements showing sufficient funds.

- Vehicle Information: If you’ve already chosen a specific car, have its VIN and mileage ready.

Navigating the $70,000 Car Loan Application Process

With your financial house in order, it’s time to embark on the application journey. This stage involves making strategic decisions about where and how to apply for your luxury car financing.

The Crucial Step of Pre-Approval

For a $70,000 car loan, pre-approval is not just a recommendation; it’s a necessity. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a certain interest rate, pending a final vehicle choice. This process usually results in a soft credit inquiry, which doesn’t harm your score, though a full application will involve a hard inquiry.

Why is pre-approval so crucial? It empowers you. You walk into the dealership knowing exactly how much you can spend and what your interest rate will be. This separates the financing negotiation from the car price negotiation, giving you leverage and preventing the dealership from "packing" the loan with unfavorable terms. It also prevents emotional overspending, as you have a firm budget established beforehand.

Where to Seek Your Loan: Exploring Your Options

You have several avenues for securing a $70,000 car loan, each with its own advantages:

- Banks: Traditional banks often offer competitive rates for borrowers with excellent credit. They provide a sense of security and established relationships.

- Credit Unions: Known for their member-focused approach, credit unions can often offer some of the most competitive interest rates and personalized service, especially if you’re an existing member.

- Dealerships: While convenient, dealership financing might not always offer the best rates. They act as intermediaries, working with multiple lenders. Always compare their offer to your pre-approval.

- Online Lenders: The digital age has brought a plethora of online lenders who offer quick applications, competitive rates, and a wide range of options. Their speed and convenience can be appealing for a $70,000 car loan.

Comparing Loan Offers: Beyond Just the Interest Rate

Once you start receiving loan offers, it’s vital to compare them thoroughly. Don’t just look at the advertised interest rate. The Annual Percentage Rate (APR) is a more accurate measure, as it includes the interest rate plus any fees associated with the loan. A lower interest rate might look appealing, but if it comes with high origination fees, the APR could be higher than another offer with a slightly higher interest rate but no fees.

Also, scrutinize the fine print for any prepayment penalties, late payment fees, or other clauses that could impact your financial flexibility. Understanding all the terms ensures there are no surprises down the line. to become a true expert in loan comparison.

Strategies to Maximize Your $70,000 Car Loan Approval & Terms

Beyond the initial preparation, there are specific strategies you can employ to further enhance your chances of approval and secure the best possible terms for your luxury car financing.

Boost Your Credit Score (If Time Permits)

If you have a few months before you plan to buy, actively work on improving your credit score. Pay all bills on time, reduce revolving credit card debt, and avoid opening new credit lines. Even a small bump in your score can unlock significantly better interest rates for a $70,000 car loan.

Increase Your Down Payment

Every extra dollar you can put towards a down payment makes your application stronger. Even if you only increase your down payment by a few thousand dollars, it reduces the amount financed, lowers your monthly payment, and demonstrates even greater financial stability to the lender. This small effort can sometimes be the difference between a good rate and a great rate.

Consider a Co-Signer (If Necessary)

If your credit score or income is borderline for a $70,000 car loan, a co-signer with excellent credit and a strong financial history can significantly improve your chances of approval and help you secure better terms. However, ensure both parties understand the full implications: the co-signer is equally responsible for the debt.

Negotiate the Car Price

Pro tips from us: Always negotiate the price of the car separately from the financing. Dealerships often try to combine these, which can make it harder to see where you might be overpaying. With a pre-approval in hand, you can focus purely on getting the best price for the vehicle itself. A lower car price means you’ll need to borrow less, making your loan more manageable and attractive to lenders.

Common Pitfalls to Avoid When Financing a $70,000 Vehicle

Even with the best intentions, mistakes can happen. Being aware of common pitfalls can help you steer clear of them and ensure a smooth journey to car loan approval.

Not Doing Your Homework on Total Costs

One of the biggest mistakes is failing to account for the full cost of ownership. Beyond the loan payment, insurance, maintenance, and fuel for a $70,000 car can be significantly higher than for an average vehicle. Underestimating these costs can lead to buyer’s remorse and financial strain.

Skipping Pre-Approval

As mentioned, skipping pre-approval leaves you at a disadvantage at the dealership. You lose negotiation power and might end up with less favorable financing terms simply because you didn’t know your true borrowing capacity beforehand. Always get pre-approved before stepping onto the lot.

Focusing Solely on the Monthly Payment

Common mistakes to avoid are becoming fixated on achieving the lowest possible monthly payment without considering the total cost of the loan. While a low monthly payment seems appealing, it often means extending the loan term significantly, leading to paying thousands more in interest over the life of the loan.

Accepting the First Offer

Never accept the first loan offer you receive, whether it’s from your bank or the dealership. Always shop around and compare offers from multiple lenders. Even a half-percentage point difference in interest on a $70,000 car loan can save you hundreds, if not thousands, of dollars over the loan term.

Overlooking Additional Fees

Some lenders or dealerships might include various fees in the loan, such as origination fees, documentation fees, or extended warranty costs. Be diligent in reviewing all paperwork and questioning any fees you don’t understand or didn’t agree to. These can quickly add to the total cost of your luxury car financing.

Post-Approval: Driving Off with Confidence

Once your $70,000 car loan is approved and you’ve picked up your new vehicle, there are a few final steps to ensure everything is in order and to manage your new financial commitment responsibly.

Review Your Loan Agreement Meticulously

Before signing on the dotted line, read every single clause of your loan agreement. Ensure that all the terms, including the interest rate, loan term, monthly payment, and any agreed-upon fees, precisely match what you were offered and what you accepted. Never feel rushed during this process; it’s a significant financial commitment.

Finalizing Registration and Insurance

Your lender will typically require you to have full coverage insurance (comprehensive and collision) on your financed $70,000 car. This protects their asset in case of an accident or theft. Ensure your insurance is active before you drive the car off the lot. You’ll also need to complete the vehicle registration with your state’s DMV.

Managing Your Payments Responsibly

The most critical step post-approval is making your payments on time, every time. Set up automatic payments to avoid missing due dates, which can incur late fees and negatively impact your credit score. If your financial situation allows, consider making extra payments towards the principal. This can significantly reduce the total interest paid and shorten the loan term.

For more insights on managing your car loan and avoiding financial stress, we recommend exploring resources from trusted sources like the Consumer Financial Protection Bureau, which offers valuable guidance on consumer finance.

Conclusion: Your Journey to a $70,000 Car Loan Success

Securing a $70,000 car loan is a significant financial undertaking, but with the right approach, it is an entirely achievable goal. By understanding the key factors lenders consider, diligently preparing your finances, strategically navigating the application process, and avoiding common mistakes, you can significantly increase your chances of car loan approval and secure the most favorable terms for your dream vehicle.

Remember, the journey to luxury car financing is not just about the car itself, but about making a smart financial decision that aligns with your long-term goals. With the comprehensive insights provided in this guide, you are now well-equipped to embark on this journey with confidence, driving away in your desired $70k car with peace of mind.