The Ultimate Guide to Securing a Car Loan with a 700 Credit Score

The Ultimate Guide to Securing a Car Loan with a 700 Credit Score Carloan.Guidemechanic.com

Dreaming of a new set of wheels? For many, buying a car is an exciting milestone, but the financing aspect can often feel daunting. This is where your credit score steps in, acting as a powerful key to unlock favorable loan terms. If you possess a 700 credit score, you’re in an excellent position to navigate the auto loan market with confidence.

A 700 credit score for a car loan signifies that you are a reliable borrower in the eyes of lenders. It opens doors to better interest rates, more flexible terms, and a smoother approval process. This comprehensive guide will delve deep into how your 700 credit score can transform your car buying experience, offering insights, strategies, and expert tips to help you secure the best possible deal.

The Ultimate Guide to Securing a Car Loan with a 700 Credit Score

Understanding Your 700 Credit Score in the Auto Loan Landscape

Before diving into the specifics of car loans, it’s crucial to understand what a 700 credit score truly represents. Credit scores typically range from 300 to 850, and a 700 score falls squarely into the "Good" category, often bordering on "Very Good" depending on the scoring model used. This places you in a desirable bracket for lenders.

A credit score of 700 indicates a history of responsible financial behavior. It suggests that you generally pay your bills on time, manage your credit utilization effectively, and have a stable credit history. Lenders view borrowers with this score as lower risk, which translates directly into significant advantages when seeking a car loan.

What Does a 700 Score Mean for Auto Financing?

For auto lenders, a 700 credit score is a strong indicator of creditworthiness. You are perceived as someone who is likely to make consistent, on-time payments throughout the life of the loan. This reduces the risk for the lender, making them more willing to offer you attractive terms.

In the world of car loans, borrowers are often categorized into tiers based on their credit scores. With a 700 score, you’re firmly in the "prime" or "near-prime" borrower category. This distinction is critical because it directly influences the rates and conditions you’ll be offered.

The Advantages You Unlock with a 700 Credit Score for Car Loans

Having a 700 credit score isn’t just a number; it’s a financial asset that provides tangible benefits when you’re looking to finance a car. These advantages can save you a significant amount of money over the life of your loan and make the entire car buying process much more pleasant.

Let’s explore the key benefits you can expect to enjoy.

1. Lower Interest Rates

One of the most significant advantages of a 700 credit score is access to lower interest rates. Lenders use your credit score to assess the likelihood of you defaulting on a loan. A higher score means lower risk, and lower risk means they can offer you a more competitive interest rate.

Based on my experience as an SEO content writer and financial observer, even a small difference in interest rate can result in hundreds, if not thousands, of dollars in savings over the loan term. For instance, on a $30,000 car loan over 60 months, reducing your interest rate from 7% to 4% could save you over $2,500 in total interest paid. This directly impacts your overall cost of ownership.

2. Better Loan Terms and Flexibility

With a 700 credit score, you’re not just limited to lower rates; you also gain more flexibility in loan terms. Lenders are often willing to offer longer repayment periods without significantly increasing the interest rate. This can lead to lower monthly payments, making your desired car more affordable.

You might also have access to more favorable conditions, such as fewer fees or less stringent down payment requirements. This flexibility allows you to tailor the loan to better fit your personal financial situation, giving you greater control over your budget.

3. More Loan Options and Lender Competition

A good credit score puts you in a position of power. Banks, credit unions, and other financial institutions will actively compete for your business. This competition is excellent for you, the borrower, as it encourages lenders to offer their best rates and terms to secure your loan.

You’ll find a wider array of financing options available, from traditional banks to online lenders specializing in auto loans. This increased choice means you can shop around more effectively, compare offers, and ultimately select the loan that truly serves your best interests.

4. Reduced Down Payment Requirements

While making a down payment is always a good idea, a 700 credit score can reduce the pressure to put down a large sum upfront. Lenders may be more comfortable approving you with a smaller down payment, or even no down payment at all, due to your demonstrated creditworthiness.

However, keep in mind that a larger down payment still benefits you. It reduces the total amount borrowed, thereby lowering your monthly payments and the total interest paid over time. It also helps you avoid being "upside down" on your loan, where you owe more than the car is worth.

5. Easier and Faster Approval Process

Lenders spend less time scrutinizing applications from individuals with strong credit scores. This translates to a quicker and smoother approval process for you. You’ll likely experience less paperwork and fewer requests for additional documentation.

This expedited process means you can get behind the wheel of your new car sooner. It also reduces the stress often associated with loan applications, making the entire car buying journey more enjoyable.

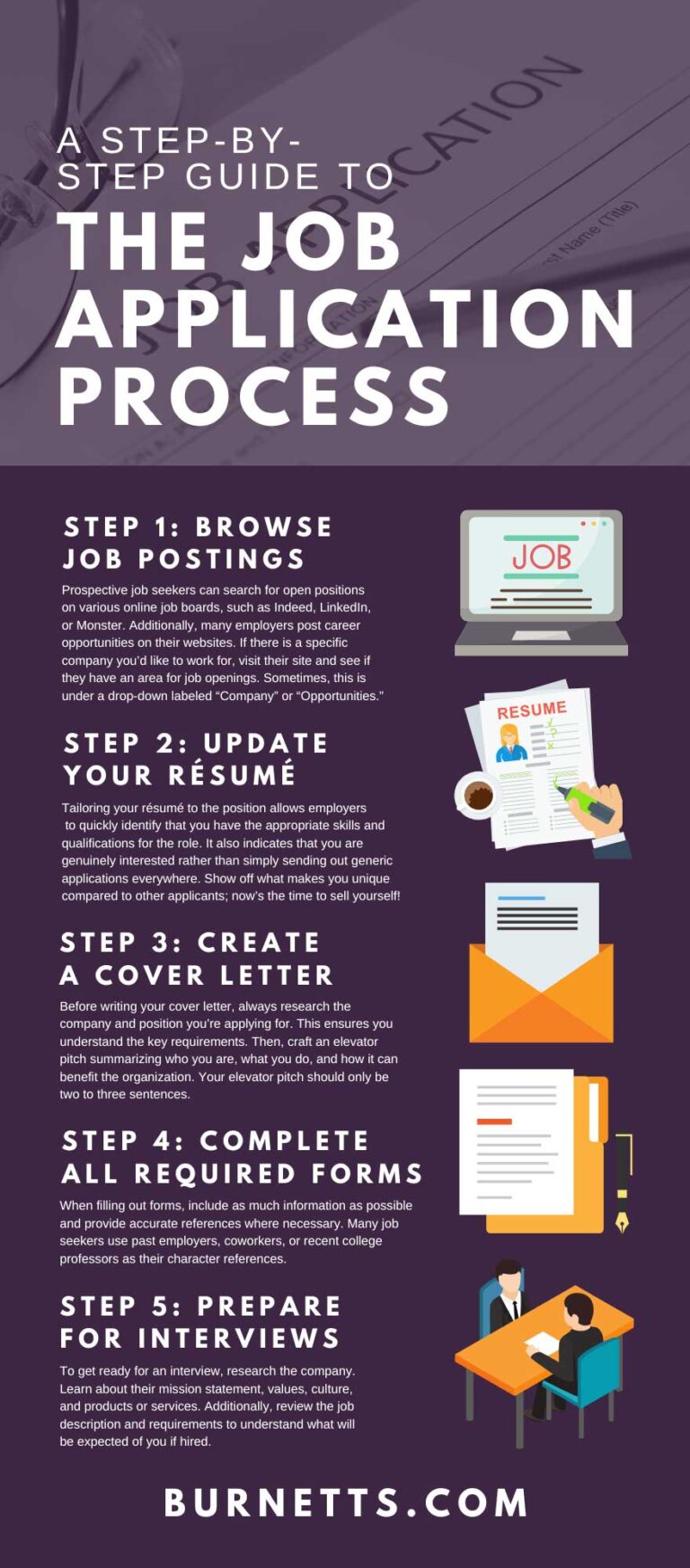

Navigating the Car Loan Application Process with a 700 Credit Score

Even with an excellent credit score, a strategic approach to obtaining your car loan is essential. Knowing the steps and being prepared can further enhance your chances of securing the most favorable terms.

Here’s a step-by-step guide to help you navigate the process effectively.

Step 1: Get Your Credit Report in Order

Even with a 700 credit score, it’s always wise to review your full credit report from all three major bureaus (Experian, Equifax, TransUnion). Check for any inaccuracies or errors that could potentially lower your score or raise red flags with lenders. Dispute any discrepancies immediately.

Understanding the factors that contribute to your score, such as payment history, credit utilization, and length of credit history, empowers you. This insight helps you maintain or even slightly improve your score before applying. For a deeper dive into credit management, consider reading our article on (placeholder for internal link).

Step 2: Determine Your Budget

Before you even look at cars, establish a clear and realistic budget. This involves more than just the car’s sticker price or a comfortable monthly payment. Factor in additional costs like insurance, registration fees, maintenance, and fuel.

Pro tips from us: Use an online car loan calculator to estimate different payment scenarios based on varying interest rates and loan terms. Remember, a car is a depreciating asset, so ensure your budget accounts for its long-term cost. Don’t let a great interest rate tempt you into buying a car you truly can’t afford.

Step 3: Get Pre-Approved

This is perhaps the most crucial step for anyone with a good credit score. Getting pre-approved for a loan means a lender has conditionally agreed to lend you a certain amount of money at a specific interest rate, based on your financial information. This pre-approval gives you immense negotiating power at the dealership.

Shop around with multiple lenders – banks, credit unions, and online lenders – to compare pre-approval offers. Since all credit inquiries for a similar type of loan within a short window (typically 14-45 days) are often treated as a single inquiry, you can compare without significantly impacting your score.

Step 4: Shop for Your Car

Armed with your pre-approval, you can now confidently shop for your vehicle. You know exactly how much you can spend, and you’re essentially walking into the dealership as a cash buyer. This allows you to focus solely on negotiating the car’s price, rather than getting caught up in financing details at the same time.

Consider whether a new or used car best fits your needs and budget. A 700 credit score will benefit you in either scenario, but interest rates for new cars are often slightly lower than for used cars due to the perceived lower risk.

Step 5: Finalize Your Loan

Once you’ve chosen your car and negotiated the best price, review all loan documents carefully. Compare the dealership’s financing offer with your pre-approval. Sometimes, dealerships can beat your pre-approved rate, but always ensure you understand all fees and terms.

Never feel rushed to sign. Read every line of the contract, paying close attention to the interest rate, loan term, total amount financed, and any additional fees or add-ons. If you need help understanding common loan terms, our article on (placeholder for internal link) can be a useful resource.

Factors Beyond Your 700 Credit Score That Lenders Consider

While a 700 credit score is a powerful asset, it’s not the only factor lenders evaluate. They look at your overall financial picture to ensure you can comfortably manage the new debt. Understanding these additional considerations can further strengthen your loan application.

Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is a critical metric for lenders. It compares your total monthly debt payments (including the new car loan) to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover your new car payments.

Lenders generally prefer a DTI ratio below 36%, though some may go higher. Even with a 700 credit score, a very high DTI could make lenders hesitant, as it suggests you might be stretched too thin financially.

Income Stability

Lenders want assurance that you have a steady and reliable source of income to make your payments. They will typically ask for proof of employment, such as pay stubs, W-2 forms, or tax returns if you’re self-employed. A consistent employment history is a significant plus.

Long-term employment with the same company or a stable career path reassures lenders of your ability to maintain payments. Conversely, frequent job changes might be viewed with more scrutiny, even with a strong credit score.

Down Payment

As mentioned earlier, while a 700 credit score can reduce down payment requirements, offering a larger down payment always strengthens your application. It reduces the amount you need to borrow, lowering the lender’s risk and potentially securing an even better interest rate.

A substantial down payment also demonstrates your commitment to the purchase and your ability to save money. This financial prudence is highly regarded by lenders and can further enhance your profile as a reliable borrower.

Vehicle Age and Type

The specific car you’re buying also plays a role in the loan decision. Lenders perceive newer cars as less risky because they typically have a higher resale value and are less prone to immediate mechanical issues. Older or high-mileage vehicles might come with slightly higher interest rates or require a larger down payment.

The type of vehicle (e.g., luxury sports car vs. economical sedan) can also influence lender perception. Extremely expensive or niche vehicles might be viewed with more caution, especially if they are difficult to resell.

Loan Term Length

The length of your loan term affects both your monthly payment and the total interest paid. While a 700 credit score can help you secure a longer term with a reasonable rate, lenders still consider the risk associated with very long terms (e.g., 84 months).

Longer terms mean the car depreciates more significantly over the loan period, increasing the risk of negative equity. Lenders might offer slightly higher rates for extended terms to offset this increased risk.

Common Mistakes to Avoid When Applying for a Car Loan (Even with a 700 Score)

Even with the advantage of a 700 credit score, it’s easy to make missteps that could cost you money or complicate the loan process. Being aware of these common pitfalls can help you navigate the journey smoothly.

Common mistakes to avoid are:

1. Not Shopping Around for Rates

Relying solely on the financing offered by the car dealership is a frequent mistake. While dealership financing can sometimes be competitive, it’s not always the best option. Failing to compare offers from multiple banks, credit unions, and online lenders means you might miss out on a significantly lower interest rate.

Always get pre-approved from at least two or three external lenders before stepping into a dealership. This gives you a benchmark and leverage during negotiations.

2. Ignoring Your Budget

It’s tempting to get excited about a car that’s slightly out of your budget, especially when a great interest rate makes the monthly payment seem affordable. However, neglecting your overall financial picture can lead to financial strain down the road.

Always stick to the budget you established in Step 2. Remember to account for all car-related expenses, not just the loan payment.

3. Focusing Only on Monthly Payments

Dealers often try to "sell" you on a monthly payment rather than the total cost of the car. They might stretch out the loan term to lower the monthly payment, which can make a more expensive car seem affordable. This often results in paying significantly more interest over the loan’s life.

Always look at the total price of the car, the interest rate, and the full cost of the loan over its entire term. Don’t let a low monthly payment obscure a bad overall deal.

4. Letting the Dealer Run Too Many Credit Checks

Each time a hard inquiry is made on your credit report, it can temporarily ding your score. While shopping for a car loan within a specific window (typically 14-45 days) is usually grouped as one inquiry by credit scoring models, letting numerous dealerships run multiple checks can be detrimental.

Provide your pre-approval letter and clearly state that you already have financing. If they insist on running their own checks, ensure they only do so for specific, competitive offers.

5. Not Reading the Fine Print

Loan agreements can be complex, filled with jargon and small print. Skipping over these details is a major mistake. You could miss hidden fees, unfavorable terms, or clauses that aren’t in your best interest.

Take your time to read the entire loan contract. Ask questions about anything you don’t understand. If possible, review the contract away from the high-pressure environment of the dealership. Understanding the terms helps you avoid unexpected surprises later. For more information on understanding loan terms, you can refer to trusted external sources like the Consumer Financial Protection Bureau’s guide on auto loans: https://www.consumerfinance.gov/consumer-tools/auto-loans/

Maximizing Your 700 Credit Score Advantage

With a 700 credit score, you’re already in a fantastic position. However, there are additional steps you can take to further maximize your advantage and secure an even better deal on your car loan.

Consider a Larger Down Payment

Even if your credit score means you don’t need a large down payment, consider making one if you can. A larger down payment reduces the principal amount you borrow, which translates to lower monthly payments and less interest paid over the life of the loan. It also helps you build equity in your vehicle faster.

Keep Your Debt-to-Income Ratio Low

Before applying for the loan, try to pay down any existing high-interest debt, especially credit card balances. This will lower your DTI ratio, making you an even more attractive borrower to lenders. A lower DTI signifies greater financial stability.

Negotiate the Car Price First

Always negotiate the price of the car separately from the financing. If you’re pre-approved, you already have your financing secured. This allows you to focus all your energy on getting the best possible price for the vehicle itself, without the distraction of loan terms.

Be Prepared with Documentation

Having all necessary documents ready can expedite the loan approval process. This includes proof of income (pay stubs, W-2s), identification, proof of residence, and any trade-in vehicle details. Being prepared shows professionalism and efficiency, which lenders appreciate.

What if Your Score is Close to 700 or You Want to Improve It Further?

Perhaps your score is 680 and you’re aiming for that 700 mark, or you’re at 700 and want to push it even higher. A slightly higher score can sometimes mean an even better rate. Here are some actionable steps to improve your credit score:

Pay Bills on Time, Every Time

Your payment history is the most significant factor in your credit score. Make sure all your credit card, loan, and utility bills are paid by their due dates. Consider setting up automatic payments to avoid missing a deadline.

Reduce Credit Card Balances

Your credit utilization ratio (how much credit you’re using compared to your total available credit) is another major factor. Aim to keep your credit card balances below 30% of your available credit, and ideally even lower, around 10%. Paying down balances can quickly boost your score.

Avoid New Credit Inquiries

Each time you apply for new credit, a hard inquiry is placed on your report, which can temporarily lower your score by a few points. Try to avoid opening new credit lines in the months leading up to your car loan application.

Monitor Your Credit Report Regularly

Regularly check your credit reports for errors. Incorrect information can negatively impact your score. You can get a free copy of your credit report from each of the three major credit bureaus once a year through AnnualCreditReport.com.

Real-Life Scenarios and Success Stories

Imagine Sarah, who had a 705 credit score. She followed the steps, got pre-approved by her credit union for a 4% interest rate, and then walked into the dealership. The dealer tried to offer her 6.5%, but because she had her pre-approval, she confidently countered. The dealership, wanting her business, matched her pre-approved rate, saving her thousands over a 5-year loan.

Or consider Mark, who with his 710 credit score, was able to secure a low-interest loan with a minimal down payment on a reliable used SUV. His good credit allowed him to choose a shorter loan term of 48 months, meaning he’ll be debt-free much faster and pay less overall interest. These scenarios highlight the tangible benefits of a strong credit score.

Conclusion

A 700 credit score for a car loan is a remarkable asset that places you in a prime position to secure excellent financing terms. It’s a testament to your financial responsibility and opens the door to lower interest rates, better loan flexibility, and a smoother application process. By understanding the advantages and following a strategic approach, you can significantly reduce the overall cost of your car and enjoy a stress-free buying experience.

Remember to get your credit report in order, establish a clear budget, and always get pre-approved from multiple lenders. Avoid common pitfalls like focusing solely on monthly payments or neglecting the fine print. With your strong credit score and these expert tips, you’re well-equipped to drive away with the best possible car loan. Your journey to a new vehicle doesn’t have to be complicated; let your 700 credit score pave the way for a successful car purchase.