The Ultimate Guide to Securing a Navy Fed Car Loan: Drive Your Dreams with Confidence

The Ultimate Guide to Securing a Navy Fed Car Loan: Drive Your Dreams with Confidence Carloan.Guidemechanic.com

Buying a car is a significant milestone for many, representing freedom, convenience, and a crucial tool for daily life. Whether you’re eyeing a brand-new model or a reliable pre-owned vehicle, securing the right financing is just as important as choosing the car itself. For military members, veterans, and their families, one name consistently rises to the top when it comes to auto loans: Navy Federal Credit Union.

A Navy Fed Car Loan isn’t just a financial product; it’s a gateway to exceptional rates, flexible terms, and a member-focused experience that stands apart from traditional lenders. This comprehensive guide will walk you through everything you need to know about navigating the world of Navy Federal auto loans, ensuring you’re well-equipped to make an informed decision and drive off with confidence. We’ll delve deep into eligibility, application tips, rate explanations, and even how to refinance an existing loan.

The Ultimate Guide to Securing a Navy Fed Car Loan: Drive Your Dreams with Confidence

Why Choose a Navy Fed Car Loan? The Unmatched Advantages

When considering financing for your next vehicle, the options can feel overwhelming. However, Navy Federal Credit Union consistently stands out, especially for its dedicated member base. Their Navy Federal Credit Union auto loan offerings are designed with your financial well-being in mind, providing a suite of benefits that are hard to beat.

Based on my extensive experience in consumer finance, Navy Federal’s commitment to its members translates into tangible advantages that simplify the car-buying process and save you money in the long run. They understand the unique financial situations of service members and their families, tailoring products to meet those specific needs.

Here are some of the core reasons why a Navy Fed Car Loan is often the preferred choice:

-

Competitive Interest Rates: One of the most compelling reasons to choose Navy Federal is their consistently low interest rates. These rates are often significantly better than those offered by conventional banks or dealership financing. Lower rates translate directly into lower monthly payments and less interest paid over the life of the loan.

This focus on competitive pricing is a cornerstone of their member-centric philosophy. They aim to put more money back into your pocket, reflecting their credit union status where profits are returned to members, not shareholders. Always compare their offers to ensure you’re getting the best deal.

-

Flexible Loan Terms: Navy Federal understands that not everyone’s financial situation is the same. They offer a wide range of loan terms, allowing you to choose a repayment schedule that comfortably fits your budget. Whether you prefer a shorter term to pay off your car faster or a longer term to reduce your monthly payments, they have options.

These flexible terms empower you to tailor the loan to your specific needs, providing peace of mind knowing your monthly obligations are manageable. It’s about finding the right balance between affordability and the total cost of the loan.

-

Exceptional Member Service: Unlike large commercial banks where you might feel like just another number, Navy Federal prides itself on personalized, supportive member service. Their representatives are known for being knowledgeable, helpful, and genuinely invested in assisting you.

From the initial inquiry to finalizing your loan, you can expect clear communication and assistance every step of the way. This level of service is particularly reassuring when navigating a significant financial decision like a car purchase.

-

Streamlined Pre-Approval Process: Getting pre-approved for a Navy Fed Car Loan is a game-changer in the car-buying journey. It allows you to know exactly how much you can afford before stepping onto a dealership lot. This gives you significant leverage during negotiations, as you walk in with your financing already secured.

The pre-approval process is typically quick and straightforward, providing you with a clear budget and an offer that dealers often struggle to match. It shifts the focus from financing to finding the perfect car, putting you in the driver’s seat.

-

No Hidden Fees or Prepayment Penalties: Transparency is a key benefit of financing with Navy Federal. You won’t encounter unexpected fees or charges that inflate the cost of your loan. Furthermore, they do not impose prepayment penalties, meaning you can pay off your loan early without any extra costs.

This freedom to pay off your loan ahead of schedule offers significant financial flexibility. It allows you to save on interest if your financial situation improves, without being penalized for being fiscally responsible.

Are You Eligible? Understanding Navy Federal Membership

Before you can even consider a Navy Fed Car Loan, you must first be a member of Navy Federal Credit Union. This is a fundamental requirement, and understanding eligibility is the crucial first step. Their membership is exclusive, catering specifically to those who serve or have served our nation, and their families.

Common mistakes to avoid are assuming you’re eligible without verifying, or not understanding the full scope of family connections that qualify. Don’t waste time applying for a loan until your membership is secured.

Here’s a breakdown of who typically qualifies for Navy Federal membership:

- Active Duty Military: This includes all branches of the armed forces: Army, Marine Corps, Navy, Air Force, Coast Guard, and Space Force.

- Veterans: Individuals who have honorably served in any branch of the U.S. armed forces.

- Department of Defense (DoD) Civilians: Employees of the Department of Defense, including contractors working on DoD installations.

- Family Members: This is where eligibility often expands. Spouses, parents, grandparents, children, grandchildren, and even siblings of current members or those eligible for membership can often join.

Pro tips from us: If you’re unsure about your eligibility, the best approach is to visit the Navy Federal website or call their member service line directly. They have a clear "Am I Eligible?" tool that can quickly confirm your status. Securing your membership is a simple online process once your eligibility is confirmed, and it opens the door to all their exceptional financial products, including their attractive NFCU auto loan options.

Types of Navy Fed Car Loans Available

Navy Federal offers a diverse portfolio of loan products designed to meet various vehicle financing needs. Whether you’re buying new or used, or even looking to consolidate an existing loan, they likely have a solution tailored for you. Understanding these options is key to choosing the right Navy Fed Car Loan for your situation.

-

New Car Loans: These loans are designed for brand-new vehicles, typically defined as those that have never been titled. Navy Federal usually offers their most competitive rates for new car loans, reflecting the lower risk associated with financing a new asset.

Terms for new car loans can extend quite long, often up to 84 months, offering flexibility in monthly payments. However, longer terms also mean paying more interest over time, so it’s a balance to consider.

-

Used Car Loans: Financing a pre-owned vehicle with Navy Federal is also a popular option. Their used car loans come with excellent rates, though they might be slightly higher than new car rates due to factors like vehicle age and mileage. Navy Federal typically finances used cars up to a certain age or mileage limit, which is important to verify.

For instance, they might have specific requirements for vehicles older than 5-7 years or with mileage exceeding 100,000 miles. Always check their current guidelines for used vehicles before you start shopping.

-

Motorcycle, RV, and Boat Loans: Beyond standard cars, Navy Federal also provides financing for a range of other recreational vehicles. If you’re dreaming of a motorcycle, an RV for cross-country adventures, or a boat for weekend excursions, they have specialized loan products.

These loans generally follow similar principles to their car loans but may have different terms, rates, and eligibility criteria specific to the vehicle type. It’s worth exploring these options if your vehicle needs extend beyond a typical car.

-

Refinancing Your Existing Auto Loan: One of the most valuable services Navy Federal offers is the ability to refinance an existing auto loan you hold with another lender. This can be a smart financial move if you’ve improved your credit score since your original loan, or if interest rates have dropped.

Refinancing with Navy Federal can potentially lower your interest rate, reduce your monthly payments, or shorten your loan term. We’ll dive deeper into this crucial topic shortly, as it can save members significant money.

Demystifying Navy Federal Car Loan Rates

Understanding how Navy Federal auto loan rates are determined is crucial for securing the best possible deal. While Navy Federal is renowned for its competitive rates, the specific rate you receive will depend on several individual factors. It’s not a one-size-fits-all scenario.

Knowing these factors empowers you to take steps to improve your standing and potentially qualify for a lower rate. This proactive approach can lead to substantial savings over the life of your loan.

Key factors influencing your Navy Fed Car Loan rate include:

-

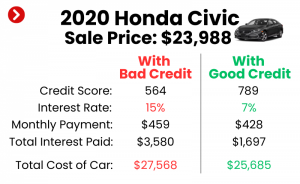

Credit Score: Your credit score is arguably the most significant determinant of your interest rate. Borrowers with excellent credit scores (typically 740+) will qualify for the lowest advertised rates. A strong credit history demonstrates your reliability as a borrower.

Conversely, a lower credit score indicates higher risk to lenders, which translates to a higher interest rate to compensate for that risk. Regularly checking and improving your credit score before applying is a savvy move.

-

Loan Term: The length of your loan repayment period also impacts your rate. Shorter loan terms (e.g., 36 or 48 months) generally come with lower interest rates because the lender’s money is tied up for a shorter period.

Longer terms (e.g., 72 or 84 months) often have slightly higher rates, even though they result in lower monthly payments. This is because the extended repayment period increases the overall risk for the lender.

-

Vehicle Type and Age: The type of vehicle you’re financing plays a role. As mentioned earlier, new cars typically command lower rates than used cars. Older used cars or those with very high mileage may also have slightly higher rates due to perceived higher depreciation or maintenance risks.

Specialty vehicles like RVs or boats might also have different rate structures compared to standard passenger cars. Always confirm the specific rates for the vehicle you intend to purchase.

-

Debt-to-Income Ratio: While not as direct as your credit score, your debt-to-income (DTI) ratio can influence a lender’s perception of your ability to repay a new loan. A lower DTI suggests you have more disposable income to cover your monthly payments.

A high DTI might signal financial strain, potentially leading to a higher rate or even loan denial. Lenders want to ensure you can comfortably manage the new car payment alongside your existing financial obligations.

Pro tips from us: Always look at the "as low as" rates advertised by Navy Federal, but understand that your actual rate will be determined after your application. To get the best possible rate, focus on maintaining a strong credit score and keeping your debt levels manageable. Don’t be afraid to ask your loan officer about ways to potentially reduce your rate during the application process.

The Step-by-Step Application Process for a Navy Fed Car Loan

Applying for a Navy Fed Car Loan is a straightforward process, especially if you’re already a member and have your documents in order. Understanding each step can help you navigate the journey smoothly and efficiently, minimizing stress and accelerating your path to car ownership.

Based on my experience, preparation is key to a seamless application. Gathering necessary information beforehand can significantly speed up the approval process.

Here’s a detailed look at the application journey:

-

Gather Your Information and Documents: Before you even start the application, make sure you have all the necessary personal and financial information readily available. This typically includes:

- Personal Identification: Your Navy Federal membership number, Social Security Number, and a valid government-issued ID (driver’s license, military ID).

- Income Verification: Recent pay stubs, W-2 forms, or tax returns to demonstrate your ability to repay the loan.

- Employment Information: Details about your current employer, including contact information and length of employment.

- Current Debt Information: Details on any existing loans (student, mortgage, other auto loans) and credit card balances.

- Vehicle Information (if applicable): If you already know which car you want, have its VIN, make, model, and mileage ready. For pre-approval, this isn’t strictly necessary but helpful for a more accurate estimate.

-

Choose Your Application Method: Navy Federal offers several convenient ways to apply for a Navy Federal auto loan:

- Online: This is often the quickest and most preferred method. You can complete the application from the comfort of your home, typically in just a few minutes.

- By Phone: Call their dedicated loan specialists. This can be helpful if you have specific questions or prefer to speak with a representative directly.

- In-Branch: Visit a local Navy Federal branch. This is ideal if you prefer face-to-face interaction or need personalized guidance.

-

Consider Pre-Approval – A Strategic Advantage: We highly recommend starting with the pre-approval process. A pre-approval Navy Fed car loan gives you a clear understanding of how much you can borrow and at what interest rate before you even set foot in a dealership.

Having pre-approval transforms you into a cash buyer in the eyes of the dealer, giving you significant negotiation power. You can focus purely on the vehicle price, rather than getting caught up in financing discussions at the dealership.

-

Submit Your Application: Once you’ve chosen your method and gathered your information, submit your application. Be thorough and accurate with all details to avoid delays.

Navy Federal’s system will review your credit history, income, and other factors. For pre-approval, they will typically perform a "soft pull" on your credit, which doesn’t impact your score. If you proceed with a full loan application, a "hard pull" will be initiated.

-

Review the Decision: After submitting, you’ll typically receive a decision fairly quickly, often within minutes for online applications, or within a business day.

- Approval: Congratulations! You’ll receive details on your approved loan amount, interest rate, and terms.

- Conditional Approval: Sometimes, Navy Federal may request additional documents or clarification before giving final approval.

- Denial: If your application is denied, Navy Federal will provide a reason. This allows you to understand what areas to improve for future applications.

-

Finalize the Loan and Purchase Your Vehicle: Once approved, you’ll receive the necessary documents to finalize your loan. If you have pre-approval, you can take this directly to the dealership. They will work with Navy Federal to complete the financing paperwork.

Pro tips from us: Don’t feel pressured by dealership financing. Always compare their offers with your Navy Fed Car Loan pre-approval. In most cases, Navy Federal will offer a superior deal.

Pro Tips for Securing Your Navy Fed Car Loan Approval

While Navy Federal strives to make financing accessible to its members, taking proactive steps can significantly increase your chances of securing the best possible Navy Fed Car Loan terms. It’s about presenting yourself as the most reliable borrower possible.

Common mistakes to avoid are applying with a low credit score, taking on too much new debt right before applying, or not having a clear budget. These can all negatively impact your application.

Here are some expert tips to boost your approval odds and get favorable rates:

-

Boost Your Credit Score: Your credit score is paramount. Before applying for a Navy Federal auto loan, take time to review your credit report for any errors and work to improve your score.

- Pay all bills on time, every time. Payment history is the most important factor.

- Reduce your credit card balances to lower your credit utilization ratio (ideally below 30%).

- Avoid opening new credit accounts in the months leading up to your loan application, as this can temporarily ding your score.

- .

-

Lower Your Debt-to-Income Ratio: Lenders assess your DTI to ensure you can comfortably handle new monthly payments. Calculate your total monthly debt payments (credit cards, student loans, mortgage, etc.) and divide by your gross monthly income.

- Aim for a DTI below 36%, though lower is always better.

- Paying down existing debts before applying for a car loan can significantly improve this ratio.

-

Save for a Down Payment: A substantial down payment not only reduces the amount you need to borrow but also signals to Navy Federal that you’re a serious and responsible borrower. It reduces their risk and can sometimes lead to better rates.

- Even a 10-20% down payment can make a big difference in your monthly payments and overall interest paid.

- It also helps mitigate immediate depreciation of the vehicle.

-

Be Realistic About Your Budget: Don’t overextend yourself. Determine a realistic car budget that aligns with your income and expenses before you start shopping. Navy Federal wants to approve loans that are sustainable for their members.

- Factor in not just the monthly loan payment, but also insurance, fuel, maintenance, and registration costs.

- A good rule of thumb is that your total car expenses (payment, insurance, gas, maintenance) shouldn’t exceed 15-20% of your net monthly income.

-

Maintain Stable Employment: Lenders prefer to see a steady income source. Having consistent employment history demonstrates your ability to make regular payments. If you’ve recently changed jobs, be prepared to explain the transition and demonstrate income stability.

By following these tips, you’ll present a strong financial profile, making your Navy Fed Car Loan application much more appealing and increasing your chances of a favorable outcome.

Refinancing Your Auto Loan with Navy Federal: A Smart Financial Move

Many people secure their initial auto loan at the dealership, often without fully exploring other financing options. If you’re currently paying a high interest rate on your car loan from another lender, or if your financial situation has improved, refinancing with a Navy Fed Car Loan could be a highly beneficial strategy.

Based on my experience, refinancing is one of the most underutilized tools for saving money on car ownership. It’s not just for those struggling with payments; it’s for anyone looking to optimize their finances.

Here’s why and how to consider refinancing your auto loan with Navy Federal:

-

When is Refinancing a Good Idea?

- Lower Interest Rates: If interest rates have dropped since you took out your original loan, or if your credit score has significantly improved, you might qualify for a much lower rate with Navy Federal.

- Reduced Monthly Payments: A lower interest rate or an extended loan term (though be cautious with this, as it increases total interest) can lead to more manageable monthly payments, freeing up cash flow.

- Shorter Loan Term: Conversely, if you want to pay off your car faster and can afford higher monthly payments, you could refinance to a shorter term, saving a substantial amount on interest over time.

- Remove a Co-signer: If your financial standing has improved, you might be able to refinance the loan in your name only, releasing a co-signer from their obligation.

-

Benefits of Refinancing with Navy Federal:

- Competitive Rates: As with their new and used car loans, Navy Federal offers some of the most competitive refinancing rates in the market.

- Seamless Process: The refinancing application is typically quick and easy, similar to their initial loan application process.

- Potential Savings: Even a one or two percentage point reduction in your interest rate can translate into hundreds or even thousands of dollars saved over the life of your loan.

-

The Refinancing Process with Navy Fed:

- Check Your Current Loan: Gather all the details of your existing loan: current interest rate, remaining balance, and payoff amount.

- Apply for a Navy Fed Car Loan Refinance: Use their online application, phone, or visit a branch, specifying that you wish to refinance an existing auto loan.

- Provide Necessary Information: You’ll need personal, income, and employment details, along with information about your current vehicle and the loan you wish to refinance.

- Review the Offer: If approved, Navy Federal will present you with new loan terms, including the interest rate and monthly payment.

- Finalize the Loan: If you accept the offer, Navy Federal will handle the payoff of your old loan, and your new payments will begin with them.

Pro tips from us: Use Navy Federal’s online calculators to estimate your potential savings before applying. Even a small reduction in your interest rate can add up over time. Don’t forget to factor in any potential fees from your current lender for paying off the loan early (though this is rare for auto loans).

Beyond the Loan: Navy Federal’s Car Buying Resources

Navy Federal Credit Union doesn’t just stop at providing excellent Navy Fed Car Loan options; they also offer valuable resources to help you through the entire car-buying journey. These additional tools are designed to empower members and make the process less daunting.

-

Navy Federal Car Buying Service (Powered by TrueCar): This service simplifies finding your next vehicle. It allows you to research cars, compare prices, and even get guaranteed savings from certified dealers in your area.

This partnership can take much of the stress out of negotiating, as you’ll often see what others paid for the same vehicle and receive upfront pricing. It’s a fantastic resource for members to ensure they’re getting a fair deal.

-

Educational Resources and Articles: Navy Federal provides a wealth of information on their website, covering various aspects of car buying and financing. These resources can help you understand topics like:

- How to budget for a car.

- The pros and cons of buying new vs. used.

- Understanding depreciation.

- Tips for negotiating at a dealership.

- .

These resources underscore Navy Federal’s commitment to member education, ensuring you’re well-informed throughout your car ownership experience.

Frequently Asked Questions (FAQs) About Navy Fed Car Loans

To further assist you, here are answers to some common questions about Navy Fed Car Loans:

-

How long does Navy Fed car loan pre-approval last?

Typically, a pre-approval Navy Fed car loan is valid for 30 to 45 days. This gives you ample time to find your desired vehicle without rushing. Always confirm the exact validity period with your loan officer. -

Can I get a Navy Fed Car Loan with bad credit?

While Navy Federal considers a range of credit scores, approval with "bad credit" (typically below 600) can be challenging. However, they are often more flexible and willing to work with members than traditional banks, especially if you have a strong membership history or can provide a co-signer. It’s always worth discussing your options with them. -

Does Navy Federal finance private party car sales?

Yes, Navy Federal does offer financing for vehicles purchased from private sellers. The process is similar to buying from a dealership, but you’ll need to provide them with information about the seller and the vehicle for verification. This flexibility is a significant advantage for members. -

Do they finance older cars or cars with high mileage?

Navy Federal generally has limits on the age and mileage of vehicles they will finance, especially for used car loans. These limits can vary, but typically they might not finance vehicles older than 7-10 years or with mileage exceeding 100,000-125,000 miles. Always check their current guidelines for specific vehicle criteria. -

Is there a prepayment penalty for a Navy Fed Car Loan?

No, Navy Federal Credit Union does not charge prepayment penalties on their auto loans. This means you can pay off your loan early without incurring any additional fees, saving you money on interest. This is a significant benefit for financially savvy borrowers. -

Can I apply for a Navy Federal auto loan before I’m a member?

No, you must be a Navy Federal Credit Union member before you can apply for any of their loan products, including auto loans. The first step is always to verify and secure your membership.

Conclusion: Drive Towards Your Future with a Navy Fed Car Loan

Navigating the world of auto financing can be complex, but with a reliable partner like Navy Federal Credit Union, it becomes a much smoother journey. A Navy Fed Car Loan offers a powerful combination of competitive rates, flexible terms, outstanding member service, and transparent processes, making it an ideal choice for military members, veterans, and their families.

From securing a pre-approval to understanding your rates and even refinancing an existing loan, Navy Federal empowers you with the tools and support needed to make smart financial decisions. By taking the time to understand their offerings, preparing your application, and leveraging their resources, you can confidently drive off in the vehicle of your dreams, knowing you’ve made a financially sound choice.

Don’t let financing stand between you and your next car. Explore your Navy Federal Credit Union auto loan options today and experience the difference of a lender truly dedicated to your success.

External Link: For the most current and official information on Navy Federal Car Loans, please visit the official Navy Federal Credit Union website: https://www.navyfederal.org/