The Ultimate Guide to Securing a Used Car Loan: Why a Good Credit Score is Your Golden Ticket

The Ultimate Guide to Securing a Used Car Loan: Why a Good Credit Score is Your Golden Ticket Carloan.Guidemechanic.com

Buying a used car is a significant financial decision, offering a practical and often more affordable alternative to a brand-new vehicle. However, for many, the journey to ownership involves securing a loan. This is where your credit score steps into the spotlight, playing a pivotal role that can either pave a smooth road to approval or present a challenging uphill battle. Understanding the profound impact of a good credit score for a used car loan isn’t just about getting approved; it’s about unlocking the best possible terms, saving thousands of dollars, and enjoying a stress-free purchase experience.

In this comprehensive guide, we’ll dive deep into why your credit score is the most powerful tool in your car-buying arsenal. We’ll explore what constitutes a "good" score, the tangible benefits it brings, actionable strategies to improve your credit, and how to navigate the used car loan process like a seasoned pro. Our goal is to equip you with the knowledge and confidence to not only secure your dream used car but to do so on the most favorable terms imaginable, ensuring you get real value for your money.

The Ultimate Guide to Securing a Used Car Loan: Why a Good Credit Score is Your Golden Ticket

The Undeniable Link: Why Your Credit Score Matters for a Used Car Loan

Your credit score is essentially a three-digit numerical representation of your creditworthiness. It’s a quick snapshot that lenders use to assess the risk involved in lending you money. A higher score indicates a lower risk, suggesting you’re reliable in repaying your debts, while a lower score signals a higher risk. This simple number has a monumental impact, particularly when you’re seeking a used car loan.

Lenders, whether they are banks, credit unions, or dealership financing departments, rely heavily on this score to make their lending decisions. They aren’t just looking at your income; they want to know if you’ve managed credit responsibly in the past. Your credit history, summarized by your score, tells them a story about your financial habits.

For used car loans, this assessment is especially critical. Used cars can sometimes be perceived as having a slightly higher risk for lenders due to factors like varying conditions, mileage, and depreciation compared to new vehicles. A strong credit score helps mitigate these perceived risks, making you a much more attractive borrower. It directly influences everything from whether your loan application is approved to the interest rate you’ll pay over the life of the loan. Based on my experience in the automotive and finance sectors, a robust credit score is often the single biggest differentiator between an affordable loan and one that burdens your budget.

What Constitutes a "Good" Credit Score for a Used Car Loan?

While the term "good" can be subjective, in the world of credit scores, there are generally accepted ranges that lenders use. Most commonly, the FICO Score model is used, which ranges from 300 to 850. Understanding these tiers is crucial for setting expectations when applying for a used car loan.

Here’s a general breakdown of FICO Score ranges:

- Exceptional: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

For a used car loan, a score in the "Good" range (typically 670-739) is generally considered a strong position. If your score falls within this bracket, you’re likely to qualify for competitive interest rates and favorable loan terms. Moving into the "Very Good" or "Exceptional" categories significantly enhances your leverage, often securing the absolute lowest rates available.

However, even a score in the mid-600s, while technically "Fair," can still secure a loan, albeit often with slightly higher interest rates. The sweet spot, where lenders are eager to offer their best deals for a good credit score for a used car loan, really starts at 670 and goes upwards. Pro tips from us: aiming for at least a 700+ score should be your goal if you want to access premium financing options and maximize your savings. Don’t settle for just "approved" when "approved with excellent terms" is within reach.

The Tangible Benefits: How a Good Credit Score Saves You Money

The impact of a good credit score for a used car loan extends far beyond mere approval; it translates directly into significant financial savings and a smoother overall experience. These benefits are not abstract; they are tangible and can save you thousands of dollars over the life of your loan.

Lower Interest Rates

This is arguably the most substantial benefit. With a good credit score, lenders view you as a low-risk borrower, making them more willing to offer you lower Annual Percentage Rates (APRs). Even a difference of a few percentage points can lead to substantial savings. For instance, on a $20,000 used car loan over five years, reducing your interest rate from 8% to 5% could save you well over $1,500 in total interest paid. This money stays in your pocket, rather than going to the lender.

Better Loan Terms and Flexibility

Beyond interest rates, a strong credit score opens the door to more favorable loan terms. This could mean a longer repayment period without a significant jump in interest, making your monthly payments more manageable. Alternatively, it might give you more flexibility with down payment requirements, allowing you to keep more cash on hand if needed. Lenders are more accommodating to borrowers they trust.

Higher Approval Chances

A good credit score significantly increases your likelihood of loan approval. You won’t have to worry about being turned down or facing endless rejections. This reduces stress and saves valuable time, allowing you to focus on finding the right car rather than constantly searching for a lender willing to take a chance on you. It also means you’ll have more options, as multiple lenders will be eager to work with you.

Enhanced Negotiating Power

When you walk into a dealership with a pre-approval in hand, secured thanks to your excellent credit, you gain immense negotiating power. You’re not reliant on their in-house financing, which might be less competitive. You can confidently compare offers and push for better prices on the car itself, knowing your financing is already solid. Common mistakes to avoid are accepting the first financing offer without shopping around, even with good credit.

Lower Monthly Payments

Ultimately, lower interest rates and better loan terms combine to result in lower monthly payments. This improves your cash flow, freeing up money for other expenses, savings, or investments. A more affordable monthly payment contributes to your overall financial stability and peace of mind, making your used car ownership experience far more enjoyable.

Strategies to Cultivate and Maintain a Good Credit Score

Cultivating and maintaining a good credit score for a used car loan is an ongoing process, but the effort pays immense dividends. It involves understanding the key factors that influence your score and consistently practicing responsible financial habits.

1. Payment History: Be On Time, Every Time

This is the most critical factor, accounting for about 35% of your FICO score. Late payments, even by a few days, can severely damage your credit. Make it a priority to pay all your bills—credit cards, loans, utilities—on or before their due dates. Setting up automatic payments or payment reminders can be incredibly helpful.

2. Credit Utilization: Keep It Low

Your credit utilization ratio is the amount of credit you’re using compared to your total available credit. It makes up about 30% of your score. Lenders prefer to see this ratio below 30%, ideally even lower (10-20%). For example, if you have a credit card with a $10,000 limit, try to keep your balance below $3,000. Paying down credit card balances is one of the quickest ways to see an improvement in this area.

3. Length of Credit History: Time is Your Ally

The longer your credit accounts have been open and in good standing, the better. This factor accounts for about 15% of your score. Avoid closing old credit accounts, even if you don’t use them frequently, as this can shorten your average credit age. Patience and consistent good behavior are key here.

4. Credit Mix: A Healthy Blend

Having a variety of credit accounts, such as credit cards, installment loans (like student loans or previous car loans), and a mortgage, can positively impact your score. This demonstrates your ability to manage different types of credit responsibly. This factor contributes around 10% to your score. However, don’t open new accounts just for the sake of diversity; only take on credit you genuinely need and can manage.

5. New Credit: Be Mindful of Applications

Each time you apply for new credit, a hard inquiry is placed on your credit report, which can slightly lower your score for a short period. While necessary when applying for a used car loan, avoid opening multiple new credit lines in a short timeframe. This signals higher risk to lenders and accounts for about 10% of your score.

6. Check Your Credit Report Regularly

It’s vital to review your credit reports from all three major bureaus (Equifax, Experian, TransUnion) at least once a year. You can get free copies at AnnualCreditReport.com. Look for any errors or fraudulent activity, which can unfairly drag down your score. If you find discrepancies, dispute them immediately. For a deeper dive into improving your financial standing, you might find our article on How to Effectively Boost Your Credit Score for Major Purchases particularly helpful.

7. Pay Down Existing Debt

Focus on reducing high-interest debt, especially on credit cards. This not only lowers your credit utilization but also frees up more income, making you a more attractive borrower for a used car loan.

Navigating the Used Car Loan Process with a Good Credit Score

Having a good credit score for a used car loan gives you a distinct advantage, but knowing how to leverage it effectively during the car-buying process is equally important. Strategic planning can further enhance your position and secure the best deal.

1. Get Pre-approved First

This is perhaps the most powerful step you can take. Before you even set foot on a dealership lot, apply for pre-approval from multiple lenders – banks, credit unions, and online lenders. Pre-approval gives you a clear understanding of the loan amount you qualify for, the interest rate you can expect, and the terms. It transforms you into a cash buyer in the eyes of the dealership, shifting the focus from your creditworthiness to the price of the car itself. This separates the financing negotiation from the car price negotiation, giving you immense leverage.

2. Shop Around for Lenders

Don’t just take the first offer you receive, even if it seems good. Different lenders have varying criteria and offer different rates. Compare interest rates, fees, and terms from at least three to five different sources. Credit unions, in particular, often offer very competitive rates to their members. Because multiple hard inquiries for the same type of loan (like an auto loan) within a short period (typically 14-45 days, depending on the scoring model) are usually treated as a single inquiry, your score won’t be overly penalized for rate shopping.

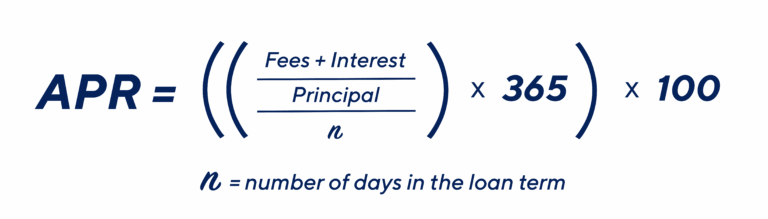

3. Understand All Loan Terms, Not Just the Interest Rate

While the interest rate is crucial, also pay close attention to the Annual Percentage Rate (APR), which includes the interest rate plus any fees. Understand the loan duration (e.g., 36, 48, 60 months), any prepayment penalties, and late payment fees. A longer loan term might mean lower monthly payments but will almost always result in paying more interest over time.

4. Consider a Down Payment (Even with Good Credit)

Even with a fantastic credit score, making a down payment on a used car can be highly beneficial. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay. It also creates immediate equity in the vehicle, protecting you from becoming "upside down" on your loan (owing more than the car is worth).

5. Be Prepared for Dealer Financing, But Don’t Rely On It

Dealerships often have relationships with various lenders and can sometimes offer competitive rates. However, it’s crucial to compare their offers with your pre-approval. Having your own financing ready gives you a strong baseline and prevents you from being pressured into less favorable terms. Your good credit score for a used car loan empowers you to say no if the dealer’s offer isn’t the best. For more insights into responsible borrowing, you can always refer to trusted resources like the Consumer Financial Protection Bureau (CFPB) on understanding auto loans.

What If Your Credit Isn’t "Good" Yet? Alternatives and Next Steps

While this article emphasizes the benefits of a good credit score for a used car loan, it’s important to acknowledge that not everyone is there yet. If your credit score is currently in the "fair" or "poor" range, securing a loan might be more challenging, but it’s not impossible.

One common option is to consider a co-signer. A co-signer with excellent credit can help you get approved and potentially secure better terms, as their creditworthiness acts as a guarantee for the loan. However, this is a significant responsibility for the co-signer, as they become equally responsible for the debt. Another path could be a secured loan, where you use the car itself as collateral. These often have higher interest rates but can be an option for building credit.

Ultimately, the best long-term strategy is to focus on improving your credit score. Even if you need a car now, commit to the credit-building strategies we discussed earlier. Making on-time payments, reducing debt, and monitoring your reports will gradually elevate your score. Every step you take towards a healthier credit profile will pay off not just for future car loans, but for all your financial endeavors. For those navigating the complexities of securing financing with less-than-perfect credit, our guide on Navigating Used Car Loans with Challenging Credit offers practical advice and strategies.

Conclusion: Your Good Credit Score – The Key to Your Dream Used Car

In the journey to purchasing a used car, your credit score stands as a fundamental pillar of your financial success. It’s more than just a number; it’s a reflection of your financial reliability and a direct determinant of the terms and affordability of your used car loan. As we’ve explored, a good credit score for a used car loan isn’t merely a gateway to approval; it’s your golden ticket to unlocking lower interest rates, more flexible terms, reduced monthly payments, and substantial savings over the lifetime of your loan.

By understanding what constitutes a good score, diligently applying strategies to improve and maintain your credit, and navigating the loan application process with foresight and knowledge, you empower yourself. You transform from a passive applicant into an informed, confident buyer, ready to negotiate the best possible deal. Don’t underestimate the power of your credit. Start today by checking your score, identifying areas for improvement, and building the financial foundation that will not only secure your next used car but also pave the way for a healthier financial future. Your dream used car, with the best financing terms, is within reach when you prioritize your credit health.