The Ultimate Guide to Securing Your "1 Finance Car Loan": Drive Away with Confidence

The Ultimate Guide to Securing Your "1 Finance Car Loan": Drive Away with Confidence Carloan.Guidemechanic.com

Getting behind the wheel of your dream car is an exhilarating experience, but for most of us, it starts with a crucial step: securing a car loan. This isn’t just about borrowing money; it’s about making a significant financial decision that impacts your budget for years to come. Understanding the ins and outs of vehicle financing is paramount to ensuring you get a deal that works for you, not against you.

This comprehensive guide is designed to empower you with the knowledge needed to navigate the complex world of auto loans. We’ll break down every aspect, from understanding the basics to advanced strategies for securing what we call your "1 Finance Car Loan" – your optimal, well-informed, and highly advantageous vehicle financing solution. Prepare to become an expert and drive away with confidence!

The Ultimate Guide to Securing Your "1 Finance Car Loan": Drive Away with Confidence

Understanding Car Loans: The Essential Foundation

Before you even start browsing vehicles, it’s vital to grasp the core concepts of car loans. This foundational knowledge will serve as your compass throughout the financing journey, helping you make smarter decisions.

What Exactly is a Car Loan?

At its heart, a car loan, or auto loan, is a sum of money borrowed from a financial institution or lender to purchase a vehicle. You agree to repay this amount, known as the principal, over a set period, typically with added interest. The car itself often serves as collateral for the loan, meaning the lender can repossess it if you fail to make payments.

This financial agreement allows individuals to acquire a vehicle without needing to pay the full purchase price upfront. It’s a common and accessible way to finance transportation, but the terms and conditions can vary widely based on numerous factors. Understanding these variables is your first step towards securing an ideal car loan.

Types of Car Loans: Knowing Your Options

Not all car loans are created equal. Different types cater to various situations and preferences, each with its own set of advantages and considerations. Exploring these options can significantly influence the best path for your "1 Finance Car Loan."

New Car Loans vs. Used Car Loans

Financing a brand-new vehicle often comes with lower interest rates and longer loan terms due to the car’s higher value and perceived reliability. Lenders view new cars as less risky collateral. However, new cars depreciate rapidly the moment they leave the dealership lot.

Used car loans, conversely, might have slightly higher interest rates and shorter terms because of the increased risk associated with an older vehicle’s unknown history and potential maintenance issues. Despite this, the overall cost of a used car, even with a higher interest rate, is often less than a new car due to lower purchase prices and slower depreciation. It’s a trade-off that requires careful consideration of your budget and priorities.

Secured vs. Unsecured Loans

The vast majority of car loans are secured loans. This means the car itself acts as collateral. If you default on your payments, the lender has the legal right to repossess the vehicle to recoup their losses. This collateral reduces the risk for the lender, often leading to more favorable interest rates for the borrower.

Unsecured personal loans can be used to purchase a car, but they are far less common for this purpose. These loans are not backed by collateral, making them riskier for lenders. Consequently, unsecured loans typically come with much higher interest rates and stricter eligibility requirements. For most car buyers, a secured auto loan is the practical and more affordable choice.

Dealer Financing vs. Bank/Credit Union vs. Online Lenders

Where you get your loan can also make a big difference. Dealerships often offer convenient financing options, sometimes with promotional rates. However, these rates might not always be the best available, and the dealer may mark up the interest rate to earn a profit.

Banks and credit unions are traditional sources for auto loans. Credit unions, being non-profit organizations, often provide some of the most competitive interest rates and personalized service. Online lenders have emerged as a popular option, offering quick applications and competitive rates, often without the overhead of physical branches. Based on my experience, it’s always wise to compare offers from at least three different types of lenders before making a decision.

Key Terms You Need to Know

Navigating loan agreements requires understanding the jargon. Familiarizing yourself with these terms is crucial for deciphering offers and ensuring you truly understand your "1 Finance Car Loan."

- APR (Annual Percentage Rate): This is the total cost of borrowing money over a year, expressed as a percentage. It includes not just the interest rate but also any additional fees or charges associated with the loan. Always compare APRs, not just interest rates, for an accurate comparison of loan costs.

- Loan Term: This refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A longer loan term means lower monthly payments but results in paying more interest over the life of the loan. Shorter terms mean higher monthly payments but less total interest paid.

- Down Payment: This is the initial amount of money you pay towards the purchase of the car, reducing the amount you need to borrow. A larger down payment can lead to lower monthly payments, less interest paid overall, and a better loan-to-value ratio.

- Principal: This is the original amount of money borrowed, excluding interest and fees. As you make payments, a portion goes towards reducing the principal, and another portion covers the interest.

- Interest: This is the cost of borrowing money, calculated as a percentage of the principal balance. It’s the profit lenders make on the loan.

- Equity: This is the difference between your car’s market value and the amount you still owe on your loan. Positive equity means your car is worth more than you owe, while negative equity (being "upside down") means you owe more than the car is worth.

Preparing for Your "1 Finance Car Loan": The Foundation for Success

The groundwork you lay before even applying for a loan can significantly impact the terms you receive. This preparation phase is where you build the strongest possible case for your "1 Finance Car Loan."

Credit Score Matters: Your Financial Passport

Your credit score is arguably the most influential factor in determining your car loan’s interest rate and approval chances. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt.

Why Your Credit Score is Crucial

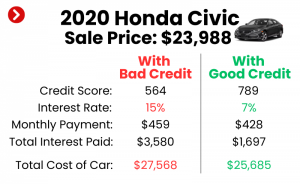

Lenders use your credit score to assess the risk of lending money to you. A high credit score (generally 700+) indicates a responsible borrower who is likely to repay their debts on time. This translates into lower interest rates, better loan terms, and a higher chance of approval. Conversely, a low credit score signals higher risk, leading to higher interest rates or even loan denial.

Based on my experience, even a difference of 50-100 points in your credit score can translate into thousands of dollars saved or spent over the life of a car loan. It’s truly your financial passport to favorable terms.

How to Check and Improve Your Credit Score

You’re entitled to a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year via AnnualCreditReport.com. Review these reports for accuracy and dispute any errors. Knowing your score before you apply helps you set realistic expectations.

To improve your credit score, focus on these key areas: pay all your bills on time, reduce outstanding debt (especially on credit cards), avoid opening too many new credit accounts at once, and keep old, positive accounts open. It takes time, but these steps can significantly boost your credit profile, paving the way for a better "1 Finance Car Loan."

Budgeting & Affordability: Knowing Your Limits

Falling in love with a car that’s outside your budget is a common mistake. A crucial step for your "1 Finance Car Loan" is establishing what you can genuinely afford, not just for the monthly payment, but for all associated costs.

Determining What You Can Truly Afford

Start by analyzing your monthly income and expenses. Create a detailed budget that includes all fixed costs (rent/mortgage, utilities, existing loans) and variable costs (groceries, entertainment). From your remaining disposable income, determine a realistic monthly car payment that won’t strain your finances.

Pro tips from us: Remember to factor in other car-related expenses beyond the loan payment. This includes car insurance, fuel, maintenance, registration fees, and potential repair costs. A good rule of thumb is to allocate no more than 10-15% of your net monthly income to your total car expenses. Don’t forget that a higher down payment can significantly reduce your monthly loan obligation.

Down Payment Power: The Benefits of Investing Upfront

A down payment is your initial cash contribution towards the purchase price of the car. While it’s not always mandatory, making a substantial down payment offers numerous advantages for your "1 Finance Car Loan."

A larger down payment directly reduces the amount you need to borrow, which means lower monthly payments and less interest paid over the life of the loan. It also helps you build equity in your vehicle faster, reducing the risk of being "upside down" on your loan (owing more than the car is worth). Lenders also view borrowers with significant down payments as less risky, potentially leading to better interest rates. Aim for at least 10-20% of the car’s purchase price, if possible.

Pre-Approval Advantage: Your Negotiating Powerhouse

Getting pre-approved for a car loan before you step foot in a dealership is one of the smartest moves you can make. It transforms your car-buying experience from a negotiation into a simple transaction.

When you’re pre-approved, a lender reviews your creditworthiness and provides you with a conditional loan offer, including a maximum loan amount, interest rate, and terms. This gives you a clear budget and an actual interest rate to compare against any financing offers from the dealership. It essentially gives you the power of a cash buyer.

Common mistakes to avoid are waiting until you’re at the dealership to think about financing. Dealers often prioritize selling the car and may try to roll less favorable financing into the deal. With a pre-approval in hand, you can confidently negotiate the car’s price separately, knowing you already have a solid financing option. It puts you in control of your "1 Finance Car Loan."

Navigating the Application Process: Securing Your Loan

With your preparations complete, it’s time to officially apply for your car loan. This stage involves gathering documents, comparing offers, and understanding the fine print to ensure you secure the best possible terms.

Gathering Your Documents: Be Prepared

Lenders require specific documentation to verify your identity, income, and creditworthiness. Having these ready in advance streamlines the application process and avoids delays.

Typically, you’ll need proof of identity (driver’s license, passport), proof of income (pay stubs, tax returns, bank statements), proof of residence (utility bill, lease agreement), and potentially your social security number. For some loans, you might also need vehicle information if you’ve already chosen a car. Being organized saves time and shows the lender you are a serious and prepared applicant.

Shopping for Lenders: The Power of Comparison

This is where your pre-approval really shines, but even without one, comparing offers is crucial. Don’t settle for the first loan offer you receive.

Explore options from various sources: traditional banks, local credit unions, and reputable online lenders. Apply for pre-approval with a few different institutions within a short period (typically 14-45 days, depending on the credit scoring model). This is because multiple credit inquiries for the same type of loan within a condensed timeframe are usually counted as a single inquiry, minimizing the impact on your credit score.

Pro tips from us: Credit unions often have some of the most competitive interest rates because they are member-owned and non-profit. Always check with your local credit union, even if you’re not a member yet, as joining is often straightforward. This comparison shopping is key to finding the most competitive "1 Finance Car Loan" rate.

Understanding Loan Offers: Deciphering the Fine Print

Once you receive loan offers, it’s critical to review them meticulously. Don’t just look at the monthly payment; dive deeper into the details.

Compare the APR (not just the interest rate), the loan term, and any associated fees (origination fees, documentation fees, prepayment penalties). A lower interest rate might seem appealing, but a longer loan term could mean paying significantly more interest overall. Ensure there are no hidden clauses or unexpected charges.

Common mistakes to avoid are signing without reading every word or feeling pressured to make a quick decision. Ask questions if anything is unclear. A transparent lender will be happy to explain all aspects of your "1 Finance Car Loan."

Negotiating Your Deal: Beyond the Car Price

Many people think negotiation ends with the car’s purchase price. However, you can also negotiate aspects of your loan, especially if you have a strong credit profile or multiple pre-approval offers.

You can try to negotiate the interest rate, especially if the dealer’s financing offer is higher than your pre-approval. You might also negotiate the loan term or ask about different payment schedules. Remember, the dealership makes money on both the car sale and the financing, so they have flexibility. Leverage your pre-approval to get the best possible rate, even if you ultimately choose to finance through the dealership. This strategic approach ensures you get a "1 Finance Car Loan" that truly benefits you.

Beyond the Loan: Responsible Car Ownership

Securing your "1 Finance Car Loan" is a significant achievement, but the journey doesn’t end there. Responsible car ownership extends beyond the initial purchase, encompassing timely payments, understanding your agreement, and managing ongoing costs.

Making Payments On Time: The Cornerstone of Good Credit

Consistency in your monthly payments is non-negotiable. Missing or making late payments can have severe negative consequences for your credit score, making it harder and more expensive to borrow money in the future.

Set up automatic payments if possible to ensure you never miss a due date. If you anticipate difficulty making a payment, contact your lender immediately. They may offer options like deferment or a modified payment plan, which is always better than defaulting. Maintaining a perfect payment history is crucial for maintaining your financial health and future credit opportunities.

Refinancing Options: When and Why to Consider It

Your "1 Finance Car Loan" might be great today, but circumstances can change. Refinancing means replacing your current car loan with a new one, often with more favorable terms.

You might consider refinancing if interest rates have dropped since you took out your original loan, if your credit score has significantly improved, or if you want to lower your monthly payments by extending the loan term (though this will mean paying more interest overall). Refinancing can also be a way to remove a co-signer or get out of an unfavorable loan. Always calculate how much you’d save before committing to a new loan.

Understanding Your Loan Agreement: What Happens if You Can’t Pay

It’s vital to fully understand the terms of your loan agreement, especially what happens in the event of default. While no one plans to miss payments, unforeseen circumstances can arise.

Your loan agreement will detail the consequences of non-payment, which typically include late fees, negative impacts on your credit score, and eventually, repossession of the vehicle. Know your rights and the lender’s procedures. Pro tips from us: Don’t wait until you’re in trouble; be proactive and communicate with your lender if you foresee payment issues. Open communication can often lead to a solution.

Insurance & Maintenance: The Hidden Costs of Car Ownership

Your "1 Finance Car Loan" covers the car itself, but it’s just one part of the total cost of ownership. Car insurance is legally required in most places and is a significant ongoing expense.

The type of car, your driving history, and even your location affect insurance premiums. Similarly, all cars require regular maintenance (oil changes, tire rotations) and occasional repairs. These costs can add up quickly. Always budget for these essential expenses to avoid financial surprises and keep your vehicle running smoothly and safely. For more detailed insights on managing car expenses, you might find our article on "Budgeting for Car Ownership" helpful .

Special Considerations & Pro Tips

Beyond the standard advice, there are specific situations and expert insights that can further refine your approach to securing and managing your car loan.

Used Car Loans vs. New Car Loans: A Deeper Dive

While we touched on this earlier, understanding the nuances is key. Used car loans can be a fantastic value proposition. The major depreciation hit on a car occurs in its first few years. Buying a used car means someone else has absorbed that initial loss.

However, used car loans might come with slightly higher interest rates and potentially shorter loan terms, as lenders perceive a greater risk with older vehicles. Always get a vehicle history report (like Carfax or AutoCheck) and a pre-purchase inspection by an independent mechanic when buying a used car. This diligence helps you avoid costly surprises and ensures your "1 Finance Car Loan" for a used vehicle is a sound investment.

Co-signers: When They Help, When They Hurt

A co-signer is someone who agrees to be equally responsible for your loan if you fail to make payments. This can be beneficial if you have limited credit history or a low credit score, as it leverages the co-signer’s good credit to help you qualify for a loan or secure a better interest rate.

However, a co-signer’s credit is also on the line. If you miss payments, their credit score will be negatively impacted, and they will be legally obligated to repay the loan. This can strain relationships. Common mistakes to avoid are not fully understanding the co-signer’s responsibility. Both parties should be fully aware of the implications before agreeing to a co-signing arrangement.

Gap Insurance: Is It Necessary for Your "1 Finance Car Loan"?

Gap insurance (Guaranteed Asset Protection) covers the "gap" between what you owe on your car loan and what your car is worth if it’s totaled or stolen. Because cars depreciate quickly, especially new ones, you could easily owe more on your loan than your insurance payout would cover.

Gap insurance is often recommended for new cars, cars with small down payments, or loans with long terms. It provides peace of mind, preventing you from being "upside down" on a car you no longer possess. However, it’s an additional cost. Evaluate your situation carefully. For a deeper look into insurance options, consider reading our article on "Choosing the Right Auto Insurance" .

Red Flags to Watch Out For: Protecting Yourself

The auto loan market can sometimes be tricky. Be vigilant for red flags that indicate potentially predatory lending or unfavorable terms.

- "Guaranteed Approval" claims: Legitimate lenders always review credit. Be wary of anyone promising a loan without checking your financial history.

- Pressure tactics: Don’t let a salesperson rush you into signing. Take your time, read documents thoroughly, and ask questions.

- Excessive fees: Understand every fee. If a fee seems unusually high or is vaguely described, question it.

- "Yo-Yo" financing: This occurs when a dealer lets you drive off with a car, only to call you back days later claiming the financing fell through and demanding a higher interest rate or more money down. Always ensure your financing is fully approved before taking possession of the vehicle.

- Add-ons you don’t need: Dealers may try to bundle expensive extended warranties, paint protection, or other add-ons into your loan. Evaluate these critically and decline if unnecessary.

For reliable external information on consumer protection in lending, you can always consult resources like the Consumer Financial Protection Bureau (CFPB) website .

Conclusion: Driving Forward with Your "1 Finance Car Loan"

Securing a car loan is a significant financial commitment, but it doesn’t have to be a daunting one. By understanding the basics, preparing diligently, shopping wisely, and managing your loan responsibly, you can transform a complex process into a rewarding experience. Your "1 Finance Car Loan" isn’t about finding the cheapest rate at all costs; it’s about finding the right loan for your financial situation, one that supports your budget and your aspirations.

Armed with the knowledge from this comprehensive guide, you are now well-equipped to navigate the auto loan landscape with confidence and intelligence. Remember to prioritize your credit score, budget realistically, compare offers, and read every document thoroughly. Drive away not just with a new car, but with the peace of mind that comes from making an informed and empowered financial decision. Happy driving!