The Ultimate Guide to Used Car Loan Length: Finding Your Sweet Spot

The Ultimate Guide to Used Car Loan Length: Finding Your Sweet Spot Carloan.Guidemechanic.com

Buying a used car is an exciting milestone. It offers excellent value, often allowing you to get more car for your money compared to buying new. But once you’ve found that perfect pre-owned vehicle, a crucial decision looms: how long should your used car loan be?

This isn’t just a technical detail; the loan length on a used car can dramatically impact your financial well-being, influencing everything from your monthly payments to the total cost of ownership. Many buyers focus solely on the lowest possible monthly payment, overlooking the deeper implications of a stretched-out loan term.

The Ultimate Guide to Used Car Loan Length: Finding Your Sweet Spot

In this comprehensive guide, we’ll dive deep into the world of used car loan lengths. We’ll explore the pros and cons of various terms, reveal the hidden costs, and equip you with the knowledge to make an informed decision that aligns with your financial goals. By the end, you’ll understand how to choose the best loan length for your used car, ensuring you drive away happy and financially secure.

Understanding Used Car Loans: Beyond the Sticker Price

A used car loan is essentially a secured loan where the car itself acts as collateral. You borrow a specific amount from a lender – be it a bank, credit union, or dealership finance department – and agree to repay it, plus interest, over a set period. This period is what we refer to as the loan length or loan term.

The monthly payment is the sum you pay each month, comprising a portion of the principal (the amount borrowed) and the interest accrued. While that monthly figure is important for budgeting, it’s merely one piece of a much larger financial puzzle. The loan length dictates how many of these payments you’ll make and, critically, how much interest you’ll pay over the life of the loan.

Ignoring the loan length and focusing only on the lowest monthly payment can lead to significant financial disadvantages. It can mean paying substantially more in total for your vehicle, extending your debt burden, and even putting you at risk of owing more than your car is worth. A thoughtful approach to your used car loan terms is paramount.

The Spectrum of Used Car Loan Lengths: Short vs. Long

Used car loan lengths typically range from 24 months to 72 months, with some lenders offering even longer terms like 84 or 96 months. Each category presents a different balance of monthly payment, total interest paid, and financial flexibility. Let’s break down the implications of choosing different loan length on a used car.

Short-Term Loans (e.g., 24-48 Months)

Short-term loans are generally considered anything under five years. These terms often include 24, 36, or 48 months. They are favored by those who want to pay off their car quickly and minimize interest expenses.

Pros of Short-Term Used Car Loans:

- Significantly Lower Total Interest Paid: This is the biggest advantage. Because you’re paying off the principal balance faster, there’s less time for interest to accrue, leading to substantial savings over the life of the loan. Based on my experience, this is where financially savvy buyers see the most direct benefit.

- Quicker Path to Ownership: You achieve full ownership of your vehicle much sooner. This means no more monthly car payments, freeing up your budget for other financial goals or savings.

- Build Equity Faster: Your car’s value typically depreciates over time. With a shorter loan, you pay down the principal faster, meaning you’re less likely to owe more than the car is worth at any given point. You build equity more rapidly.

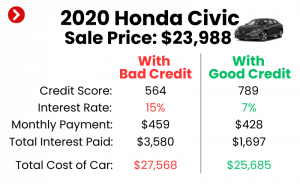

- Often Lower Interest Rates: Lenders perceive shorter terms as less risky. As a result, they may offer slightly lower interest rates for loans with shorter repayment periods, further reducing your overall cost.

Cons of Short-Term Used Car Loans:

- Higher Monthly Payments: The trade-off for lower total interest is a higher monthly payment. You’re condensing the repayment of the principal into fewer installments, which can strain your budget if not carefully planned.

- Less Financial Flexibility: Higher fixed expenses mean less discretionary income each month. This could make it harder to save, invest, or handle unexpected financial emergencies.

Who are Short-Term Loans Best For?

Short-term loans are ideal for buyers with a stable income and sufficient disposable income to comfortably afford higher monthly payments. They are also excellent for those who prioritize minimizing interest costs and becoming debt-free quickly. If you want to avoid the common mistake of paying too much interest, a shorter loan term is often the answer.

Medium-Term Loans (e.g., 48-60 Months)

Medium-term loans, typically ranging from 48 to 60 months, represent a popular middle ground. They strike a balance between manageable monthly payments and reasonable total interest costs. This is often the sweet spot for many buyers, offering a good compromise.

Pros of Medium-Term Used Car Loans:

- Balanced Monthly Payments: Compared to short-term loans, the monthly payments are more affordable, making them accessible to a wider range of budgets without excessively prolonging the debt.

- Manageable Total Interest: While you’ll pay more interest than with a 24 or 36-month loan, it’s significantly less than what you’d accrue over 72 or 84 months. This offers a good balance between cost and affordability.

- Good for Newer Used Cars: If you’re buying a relatively new used car (1-3 years old), a 48 or 60-month loan often aligns well with its remaining reliable lifespan, allowing you to pay it off before major maintenance issues typically arise.

Cons of Medium-Term Used Car Loans:

- More Interest Than Short Terms: You will still pay more in total interest compared to a shorter loan. It’s a trade-off for the lower monthly payment.

- Slower Equity Build-Up: While better than long-term loans, building equity is slower than with short-term options, meaning you might be closer to owing what the car is worth for a longer period.

Who are Medium-Term Loans Best For?

This length is suitable for buyers who need a more comfortable monthly payment but still want to avoid excessive interest. It’s a practical choice for many, especially those purchasing a reliable used vehicle that they plan to keep for several years.

Long-Term Loans (e.g., 72-96 Months)

Long-term loans for used cars, extending to 72, 84, or even 96 months, have become increasingly common, particularly as car prices rise. While they offer the lowest monthly payments, they come with significant financial risks and higher overall costs.

Pros of Long-Term Used Car Loans:

- Lowest Monthly Payments: This is the primary appeal. By spreading the cost over a longer period, the monthly burden becomes very light, making it possible to afford a more expensive vehicle or free up cash flow for other expenses.

- Increased Affordability: For buyers on a tight budget, a long-term loan might be the only way to afford a specific car, making it seem like a helpful option at first glance.

Cons of Long-Term Used Car Loans:

- Significantly Higher Total Interest Paid: This is the biggest drawback. The extended repayment period allows interest to compound for much longer, resulting in a substantially higher total cost for the car. You could end up paying thousands more in interest alone.

- Increased Risk of Negative Equity (Upside Down): This is a critical concern. Cars depreciate rapidly, especially used ones. With a long loan term, the car’s value can decline faster than you pay off the principal, leaving you owing more than the car is worth. We’ll delve deeper into this "upside down" dilemma shortly.

- Higher Interest Rates: Lenders typically charge higher interest rates for longer loan terms due to the increased risk and uncertainty over such an extended period. This further inflates the total cost.

- Longer Debt Burden: You’ll be making car payments for many years, potentially outliving the car’s reliable lifespan or your desire to own it. This can hinder other financial goals.

- Maintenance Issues with Older Cars: By the time you finish paying off an 84-month loan on a used car, the vehicle could be quite old, potentially requiring significant and costly repairs. You could be paying for a car that is no longer reliable or even functional.

Who are Long-Term Loans Best For?

Honestly, long-term loans for used cars are rarely the best choice. They are sometimes a necessity for those who absolutely need a car and cannot afford the monthly payments of shorter terms, but it’s a decision that should be approached with extreme caution and a full understanding of the financial implications. Common mistakes to avoid are stretching a loan too long just for a lower payment, without considering the overall financial burden.

Factors Influencing Your Ideal Loan Length Choice

Choosing the best loan length for your used car isn’t a one-size-fits-all decision. It requires a careful evaluation of several personal and financial factors.

- Your Monthly Budget: This is the most immediate and tangible factor. How much can you comfortably afford to pay each month without stretching your finances thin? Remember, "comfortable" means you still have room for savings, emergencies, and other living expenses. Don’t just look at the payment; consider your entire financial picture.

- Total Cost of Ownership: Beyond the monthly payment, calculate the total amount you will pay over the life of the loan, including all interest. Often, a slightly higher monthly payment on a shorter term leads to significant savings overall. This comprehensive view is crucial.

- Interest Rates: Interest rates vary based on your credit score, the lender, and the loan term itself. Longer terms often come with higher rates. Use online calculators to see how different rates and terms impact your total cost.

- Car’s Age and Condition: Lenders may impose limits on the maximum loan length for very old or high-mileage used cars. A 10-year-old car might not qualify for an 84-month loan. Furthermore, consider the car’s expected reliability. You don’t want to be paying for a car that’s constantly in the repair shop.

- Expected Lifespan of the Car: How long do you realistically plan to keep the car? Ideally, you should aim to pay off the loan before the car starts requiring major, expensive repairs or before you anticipate wanting a new vehicle.

- Down Payment Amount: A larger down payment reduces the amount you need to borrow, which can shorten your loan term, lower your monthly payments, or both. It’s a powerful tool to improve your loan terms and reduce interest.

- Your Credit Score: A strong credit score is your ticket to better interest rates and more favorable used car loan terms. Lenders view borrowers with excellent credit as less risky, offering them the most competitive options across all loan lengths.

- Your Financial Goals: Are you trying to save for a house, pay off other debts, or build an emergency fund? A long car loan can impede these goals. Consider how quickly you want to be debt-free and how a car payment fits into your broader financial strategy.

The "Upside Down" Dilemma: A Critical Consideration

One of the most significant risks associated with long loan lengths on used cars is negative equity, commonly known as being "upside down" or "underwater." This occurs when you owe more on your car loan than the car is actually worth.

Cars depreciate, meaning they lose value over time, often quite rapidly in the initial years. With a long loan term, your principal balance might not decrease as quickly as the car’s market value. Based on my years in the automotive finance world, this is one of the most common pitfalls that catch buyers off guard.

How does it happen? Imagine you take out a 72-month loan for a used car. In the first few years, a large portion of your monthly payment goes towards interest, meaning you’re paying down the principal very slowly. Meanwhile, the car continues to lose value. If you need to sell or trade in the car during this period, you could find yourself in a situation where the sale price doesn’t cover the remaining loan balance.

The implications of negative equity are severe:

- Difficulty Selling or Trading In: If you sell the car, you’ll have to pay the difference out of pocket to clear the loan, even though you no longer own the car. When trading in, the negative equity is often rolled into your new car loan, creating an even larger debt for your next vehicle.

- Financial Loss in Case of Total Loss: If your car is totaled in an accident, your insurance payout might only cover the actual cash value of the car, which could be less than your outstanding loan balance. This leaves you with no car and still owing money to the lender.

Protecting Yourself with GAP Insurance:

This is where Guaranteed Asset Protection (GAP) insurance becomes crucial. GAP insurance covers the "gap" between what your car is worth (and what your standard auto insurance will pay out) and the amount you still owe on your loan if the vehicle is stolen or totaled. For anyone considering a long-term used car loan, or making a small down payment, GAP insurance is a highly recommended safeguard.

Calculating the Real Cost: An Example

To truly understand the impact of loan length on a used car, let’s look at a hypothetical example.

Scenario:

- Used Car Price: $20,000

- Interest Rate: 7.0% (for simplicity, assuming it remains constant for different terms, though in reality, it might vary)

- Down Payment: $0 (to highlight the full cost of the loan)

| Loan Length (Months) | Monthly Payment (Approx.) | Total Interest Paid (Approx.) | Total Cost of Car (Principal + Interest) |

|---|---|---|---|

| 36 Months | $617 | $2,212 | $22,212 |

| 60 Months | $396 | $3,776 | $23,776 |

| 72 Months | $340 | $4,480 | $24,480 |

| 84 Months | $299 | $5,124 | $25,124 |

As you can see, stretching the loan from 36 months to 84 months lowers your monthly payment by over $300, making it seem much more affordable. However, the total cost of the car increases by nearly $3,000 in interest alone! This example clearly demonstrates why prioritizing the total cost of a used car loan over just the monthly payment is essential.

Strategic Steps to Choose Your Best Loan Length

Making the right decision about your used car loan terms requires a methodical approach. Here are the strategic steps you should take:

- Assess Your Financial Health Thoroughly: Before even looking at cars, review your budget. Understand your income, fixed expenses, and discretionary spending. Determine a realistic maximum monthly payment you can comfortably afford, including insurance and potential maintenance costs for a used vehicle. Don’t forget to account for an emergency fund.

- Get Pre-Approved from Multiple Lenders: Pro tips from us: Always get pre-approved from multiple lenders (banks, credit unions, online lenders) before stepping onto a dealership lot. This gives you a clear understanding of the interest rates and loan lengths you qualify for, empowering you to negotiate effectively. Pre-approval separates the financing from the car choice, allowing you to focus on the best deal for each.

- Research Car Depreciation: Understand how quickly the specific make and model of the used car you’re interested in typically depreciates. Resources like Kelley Blue Book or Edmunds can provide insights into resale values. This helps you avoid the "upside down" trap by aligning your loan term with the car’s expected value trajectory.

- Consider the Car’s Reliability and Expected Lifespan: An older, high-mileage used car might not be a good candidate for a very long loan. Research reliability ratings for the specific model and year. You want to pay off the car before it becomes a money pit for repairs. Aligning your loan length on a used car with its projected reliable life is smart financial planning.

- Factor in Future Plans: Do you anticipate a career change, moving, or starting a family in the next few years? These life events can impact your budget and your need for a specific vehicle. Choose a loan term that offers flexibility for your future aspirations.

- Prioritize Total Cost Over Monthly Payment: We can’t stress this enough. While a low monthly payment is appealing, it’s often a mirage that hides a much higher total cost. Always calculate the total amount of interest you’ll pay over different loan terms and make your decision based on the overall financial impact.

Beyond the Loan Term: Other Smart Financing Moves

While loan length on a used car is a major factor, it’s part of a larger financing strategy. Consider these additional moves to secure the best deal:

- Make a Substantial Down Payment: The more you put down upfront, the less you need to borrow. This directly reduces your monthly payment, the total interest paid, and your risk of negative equity. Even a 10-20% down payment can make a significant difference.

- Improve Your Credit Score: A higher credit score translates to lower interest rates, regardless of the loan length. Before applying for a loan, take steps to improve your credit, such as paying bills on time, reducing outstanding debt, and correcting any errors on your credit report. For more detailed tips, you can check out our guide on how to improve your credit score for car loans (Internal Link 1 Placeholder).

- Consider Refinancing: If your financial situation improves after you’ve taken out a loan (e.g., your credit score increases, interest rates drop), you might be able to refinance your used car loan for a lower interest rate or a shorter term, saving you money.

- Don’t Skip GAP Insurance (Especially for Long Terms): As discussed, GAP insurance is a vital protection, particularly if you have a long loan term or a small down payment. It ensures you won’t be stuck with a loan for a car you no longer own.

- Evaluate Extended Warranties Carefully: Extended warranties can offer peace of mind, especially for used cars. However, assess if the cost of the warranty, particularly if rolled into your loan, is truly worth it. Compare it to setting aside money in an emergency fund for potential repairs.

Common Mistakes to Avoid When Choosing Loan Length

Based on my extensive experience helping consumers navigate car financing, certain errors crop up repeatedly. Being aware of these common mistakes can save you a lot of money and stress:

- Only Focusing on the Lowest Monthly Payment: This is the cardinal sin of car financing. While a low payment is attractive, it often comes at the expense of much higher total interest and a prolonged debt burden. Always look at the bigger picture.

- Ignoring the Total Interest Paid: Many buyers fail to calculate or even consider the thousands of dollars in extra interest they’ll pay by extending their used car loan terms. Always do the math.

- Not Considering the Car’s Depreciation: Overlooking how quickly your chosen used car will lose value, especially in relation to your loan balance, is a recipe for negative equity. Understand the depreciation curve for your specific vehicle. You can learn more about this by reading our article on understanding car depreciation and its impact (Internal Link 2 Placeholder).

- Skipping Pre-Approval: Going into a dealership without pre-approval means you don’t know your true borrowing power or best interest rate. This puts you at a disadvantage during negotiations.

- Underestimating Future Maintenance Costs for an Older Used Car: If you’re buying an older used car and stretching the loan out, you could end up with a car that needs significant repairs while you’re still paying off the loan. Factor in potential repair costs when assessing affordability.

- Falling for the "Just a Few Dollars More a Month" Trap: Salespeople might try to upsell you on additional features, warranties, or services by saying it’s "just a few dollars more a month." These small additions can add up to hundreds or thousands over a long loan term.

Conclusion

Choosing the right loan length on a used car is one of the most critical decisions you’ll make in the car-buying process. It’s not just about finding a monthly payment that fits; it’s about making a financially sound choice that protects your long-term well-being. By understanding the trade-offs between shorter and longer used car loan terms, carefully evaluating your personal circumstances, and avoiding common pitfalls, you can navigate the financing landscape with confidence.

Remember to prioritize the total cost of the loan, consider the car’s depreciation, and always aim to be debt-free before your car loses its reliability or you’re ready for an upgrade. With a thoughtful approach, you can secure the best possible financing deal, drive away in your desired used car, and enjoy the journey without financial regrets. For further insights into responsible auto financing, consider exploring resources from trusted financial institutions like NerdWallet’s comprehensive guide on auto loans.

This comprehensive approach to used car loan length ensures you’re not just buying a car, but making a smart financial investment. Happy driving!