The Ultimate Guide to Your Car Loan Amortization Schedule: Unlock Hidden Savings & Take Control

The Ultimate Guide to Your Car Loan Amortization Schedule: Unlock Hidden Savings & Take Control Carloan.Guidemechanic.com

Buying a car is an exciting milestone, often involving a significant financial commitment: a car loan. While the thrill of a new vehicle can be intoxicating, many drivers overlook one of the most powerful tools in their financial arsenal: the car loan amortization schedule. This isn’t just a dry financial document; it’s a meticulously crafted roadmap that reveals the true cost of your loan and empowers you to save potentially thousands of dollars.

Understanding your car loan amortization schedule is not merely about tracking payments; it’s about gaining complete control over your debt. It demystifies where every dollar of your payment goes, distinguishing between the principal you owe and the interest you pay. This knowledge is crucial for making informed financial decisions and achieving financial freedom faster.

The Ultimate Guide to Your Car Loan Amortization Schedule: Unlock Hidden Savings & Take Control

In this comprehensive guide, we will peel back the layers of car loan amortization. We’ll explain exactly what it is, break down its core components, and show you why mastering this schedule is a non-negotiable step for any car owner. Get ready to transform your understanding of car loans and unlock real savings.

What Exactly is a Car Loan Amortization Schedule? The Foundation

At its heart, an amortization schedule is a detailed table showing every payment you will make over the life of your loan. It meticulously breaks down each payment into two primary components: the principal portion and the interest portion. Think of it as a detailed ledger that tracks your debt’s journey from start to finish.

This schedule provides a transparent view of your loan balance after each payment. It acts as a crystal ball, allowing you to see exactly how your outstanding debt diminishes over time. For anyone looking to manage their finances proactively, this document is an invaluable asset.

Without an amortization schedule, your car loan payments might feel like money disappearing into a black box. With it, you gain clarity, foresight, and the ability to strategize your debt repayment effectively. It transforms a complex financial obligation into an understandable, manageable process.

Deconstructing the Components of Your Amortization Schedule

Every car loan amortization schedule, regardless of its source, will feature several key columns. Understanding each one is fundamental to grasping the full picture of your loan. Let’s break them down.

Scheduled Payment

This is the fixed amount you pay each period, usually monthly, for the entire duration of your loan. While this number remains constant, its internal allocation between principal and interest changes dramatically over time. This consistent payment is what makes budgeting for your car loan straightforward.

It’s the figure you agree upon with your lender, encompassing both the cost of borrowing (interest) and the repayment of the money you borrowed (principal). Knowing this fixed amount helps you plan your monthly budget without surprises.

Interest Paid

This column shows the exact amount of interest you are paying with each scheduled payment. Interest is the cost of borrowing money, calculated on your outstanding principal balance. Early in your loan term, a significant portion of your payment goes towards interest.

As your loan progresses and your principal balance decreases, the interest portion of each payment also gradually reduces. This is a critical concept to grasp, as it highlights the "interest first" phenomenon we’ll discuss shortly.

Principal Paid

This is the portion of your payment that directly reduces your outstanding loan balance. Unlike interest, the principal portion of your payment starts relatively small and progressively increases over the loan term. This gradual shift is key to understanding how you eventually pay off your car.

Each time you make a payment, the principal portion chips away at the original amount you borrowed. The more principal you pay down, the less interest you’ll be charged in subsequent periods, creating a beneficial cycle.

Beginning Loan Balance

This figure represents the total amount you still owe on your car loan before you make the current payment. It’s the starting point for calculating the interest due for that specific payment period. This balance constantly decreases with each payment.

Tracking this balance allows you to see the real-time progress of your debt reduction. It’s a clear indicator of how much closer you are to owning your car outright.

Ending Loan Balance

After your scheduled payment is applied (first to interest, then the remainder to principal), this column shows your new, reduced outstanding loan balance. This becomes the beginning loan balance for your next payment period.

Watching this number shrink is incredibly motivating and provides a tangible measure of your financial discipline. It directly reflects the impact of your payments on your overall debt.

Cumulative Interest and Principal (Optional, but Useful)

Some more detailed amortization schedules include columns for cumulative interest and principal paid. These totals allow you to see, at any point in the loan, exactly how much you’ve paid in total interest and how much you’ve paid towards the original principal amount.

This cumulative view offers a powerful perspective on the overall cost of your loan. It can be a sobering, yet enlightening, reminder of the financial journey you’re undertaking.

Why Understanding Your Amortization Schedule is Non-Negotiable (E-E-A-T)

Based on my experience working with countless individuals on their auto loans, many car buyers sign on the dotted line without truly understanding the mechanics of their payments. This oversight can cost them thousands. Understanding your amortization schedule isn’t just good practice; it’s empowering.

Empowerment Through Knowledge

Knowing precisely how your loan works gives you a powerful sense of control. You’re no longer passively making payments; you’re actively managing your debt. This understanding transforms you from a debtor into a strategic financial planner.

It removes the mystery from your car loan, allowing you to see the direct impact of every payment. This clarity is the first step towards smarter financial decisions.

Unlocking Hidden Savings

Perhaps the most compelling reason to scrutinize your amortization schedule is the potential for significant savings. By understanding how interest accrues, you can identify opportunities to reduce the total interest paid over the life of the loan. This often involves strategic extra payments.

Pro tips from us: Don’t just accept the dealer’s payment amount; understand the total cost. Your amortization schedule is the blueprint for finding those cost-saving opportunities.

Effective Budgeting and Financial Planning

With a clear amortization schedule, you know exactly how much of your monthly payment is going towards interest versus principal. This detailed breakdown allows for more accurate budgeting and financial planning. You can see your debt reduction progress and anticipate when your principal balance will reach certain thresholds.

This insight helps you plan for other financial goals, knowing precisely how your car loan fits into your overall financial picture. It’s about making your money work harder for you.

Informed Debt Reduction Strategies

An amortization schedule is the ultimate tool for debt reduction strategies. Whether you’re considering making extra payments, refinancing, or paying off the loan early, the schedule provides the data you need to assess the impact of these decisions. It allows for "what if" scenarios that reveal potential savings.

It empowers you to make proactive choices that align with your financial goals, rather than simply letting the loan run its course. This proactive approach is key to accelerating your debt-free journey.

The "Interest First" Phenomenon: Why It Matters

One of the most crucial, yet often misunderstood, aspects of car loan amortization is the "interest first" phenomenon. In the early stages of your loan, a disproportionately large percentage of your monthly payment is allocated to interest, with only a small portion going towards reducing your principal.

This isn’t a trick; it’s how loan interest is calculated. Interest is always calculated on the current outstanding principal balance. When your balance is highest at the beginning of the loan, the interest charges are naturally at their peak.

As you continue to make payments, your principal balance slowly decreases. With a lower principal balance, the interest charged for the next period also drops. This means a larger portion of your fixed payment can then be applied to the principal.

Common mistakes to avoid are assuming that your car payment is evenly split between principal and interest from day one. This misconception can lead to frustration if you try to pay off your loan early, only to find the principal balance isn’t shrinking as fast as you expected initially. Understanding this front-loaded interest structure is vital for anyone considering accelerating their loan payoff.

How to Create Your Own Car Loan Amortization Schedule

While your lender might provide a basic schedule, creating your own offers a deeper understanding and allows for scenario planning. Thankfully, you don’t need to be a math wizard to do it.

Online Amortization Calculators

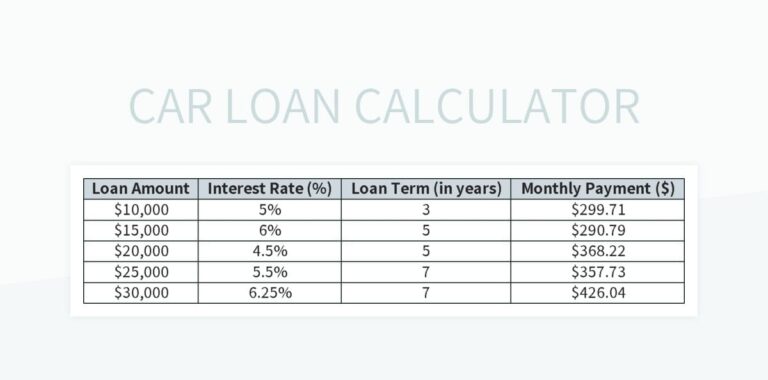

The easiest and most common way to generate an amortization schedule is by using an online calculator. Numerous websites offer free, user-friendly tools where you simply input your loan amount, interest rate, and loan term.

These calculators instantly generate a detailed table, showing every payment’s breakdown. They are excellent for quick insights and for comparing different loan scenarios without any complex calculations.

Spreadsheets (Excel/Google Sheets)

For those who prefer a hands-on approach and want the flexibility to modify variables, a spreadsheet program like Excel or Google Sheets is ideal. You can set up a simple table with columns for payment number, beginning balance, interest, principal, and ending balance.

You’ll need a few basic formulas:

- Monthly Interest Rate: Annual Interest Rate / 12

- Interest Paid: Beginning Balance * Monthly Interest Rate

- Principal Paid: Scheduled Payment – Interest Paid

- Ending Balance: Beginning Balance – Principal Paid

Pro tips from us: Many free templates are available online for amortization schedules, which can save you time in setting up the initial formulas. This method gives you unparalleled control and visibility.

Leveraging Your Amortization Schedule for Financial Advantage

Once you understand your car loan amortization schedule, you’re equipped to make strategic moves that can save you significant money and reduce your debt faster.

Making Extra Payments

This is arguably the most powerful strategy. When you make an extra payment, or even add a small amount to your regular payment, you directly reduce your principal balance. Because interest is calculated on the principal, a lower principal balance immediately translates to less interest charged on future payments.

Your amortization schedule will clearly show how even a small, consistent extra payment can shave months off your loan term and hundreds or thousands of dollars off the total interest paid. It’s a direct attack on the cost of borrowing.

The Power of Bi-Weekly Payments

Instead of making one monthly payment, switching to bi-weekly payments means you make half of your monthly payment every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments, which equates to 13 full monthly payments annually instead of 12.

This "thirteenth payment" directly goes towards principal, significantly accelerating your loan payoff. Your amortization schedule can illustrate the exact impact of this strategy, showing you how much faster you’ll become debt-free.

Strategic Refinancing

Refinancing your car loan involves taking out a new loan, often with a lower interest rate or a shorter term, to pay off your existing loan. Your amortization schedule is critical here. It helps you compare your current loan’s remaining interest with a potential new loan’s total cost.

You can use an online calculator to generate an amortization schedule for the proposed new loan and directly compare it against your current one. This allows you to see if the new loan truly offers a financial advantage after considering any fees.

Avoiding Prepayment Penalties

While paying off your loan early is generally a smart move, some lenders include prepayment penalties in their loan agreements. This fee is designed to compensate the lender for the interest they lose when you pay off your loan ahead of schedule.

Before making any extra payments or considering early payoff, always review your loan agreement carefully for any mention of prepayment penalties. Your amortization schedule helps you calculate the total interest savings, which you can then weigh against any potential penalties.

The Impact of Loan Term and Interest Rate on Your Schedule

The two most significant factors influencing your car loan amortization schedule, and thus the total cost of your loan, are the loan term and the interest rate. Understanding their interplay is crucial for responsible borrowing.

Shorter Loan Term

Opting for a shorter loan term (e.g., 36 or 48 months instead of 60 or 72 months) means you’ll have higher monthly payments. However, because you’re paying off the principal faster, you’ll accumulate significantly less interest over the life of the loan.

Your amortization schedule for a shorter term will show a rapid reduction in your principal balance and a much lower total interest paid. It’s the financially savvy choice if your budget can accommodate the higher monthly payments.

Longer Loan Term

Conversely, a longer loan term offers lower monthly payments, making the car seem more affordable upfront. The trade-off, however, is substantial: you’ll pay considerably more in total interest over the extended period.

The amortization schedule for a longer term will reveal how slowly your principal balance decreases initially and how much more interest accumulates. While it eases the monthly burden, it significantly increases the overall cost of your vehicle.

Higher Interest Rate

The interest rate is the direct cost of borrowing. A higher interest rate means a larger portion of each payment goes towards interest, especially in the early stages of the loan. This directly inflates the total cost of your car.

Even a difference of one or two percentage points can translate to thousands of dollars in extra interest over a typical car loan term. Your amortization schedule will clearly highlight how a higher rate slows down your principal reduction and adds to your financial burden. Always strive for the lowest possible interest rate your credit score allows.

Common Mistakes and Misconceptions About Car Loan Amortization

Despite its importance, many people fall prey to common misunderstandings about their car loan amortization schedules. Recognizing these pitfalls can save you from costly errors.

Ignoring the Schedule Completely

The most prevalent mistake is simply not looking at the amortization schedule at all. Many borrowers only focus on the monthly payment amount, completely overlooking the detailed breakdown of principal and interest. This means missing out on valuable insights and opportunities for savings.

Believing All Payments Go Equally to Principal/Interest

As discussed with the "interest first" phenomenon, payments are not evenly split. Many believe that half of their payment goes to principal and half to interest, which is rarely true, especially at the beginning of the loan. This misconception can lead to inaccurate expectations about how quickly the loan balance is shrinking.

Not Considering Prepayment Options

A common oversight is failing to explore the possibility of making extra payments or paying off the loan early. Many assume they are locked into the original payment schedule, not realizing the significant interest savings that come from accelerating principal reduction. Your amortization schedule is the perfect tool to visualize these savings.

Failing to Account for the Total Cost of the Loan

Focusing solely on the monthly payment can be deceptive. Without reviewing the amortization schedule, it’s easy to overlook the total amount of interest you will pay over the life of the loan. This means you might be underestimating the true cost of your vehicle significantly.

Beyond the Schedule: Holistic Car Loan Management

While the amortization schedule is a powerful tool, it’s part of a larger ecosystem of smart car loan management. To truly master your auto financing, consider these broader strategies.

Pre-purchase planning is paramount. Before you even step into a dealership, knowing your budget, understanding your credit score, and getting pre-approved for a loan can put you in a much stronger negotiating position. This foundational work directly impacts the interest rate and loan term you’ll secure. You might also find our article on Understanding Car Loan Interest Rates helpful in this regard!

Always read the fine print of your loan agreement. This includes checking for any prepayment penalties, understanding late fees, and clarifying the exact interest calculation method. Don’t assume anything; clarify everything before you sign.

Maintaining a good credit score is an ongoing effort that pays dividends. A strong credit history not only helps you secure better rates on car loans but also on mortgages, credit cards, and other financial products. For a deeper dive into improving your credit score, check out Boost Your Credit Score for Better Loan Rates.

Conclusion

The car loan amortization schedule is far more than a dry financial document; it is a blueprint for financial empowerment. By taking the time to understand its components and how they interact, you transform from a passive borrower into an active manager of your debt. This knowledge is your key to unlocking hidden savings and achieving financial freedom faster.

We’ve explored how each payment breaks down into principal and interest, the crucial "interest first" phenomenon, and how to leverage your schedule for strategies like extra payments and refinancing. Armed with this insight, you can make informed decisions that significantly reduce the overall cost of your car loan.

Don’t let your car loan control you; take control of your car loan. Review your own amortization schedule today, or create one using an online calculator. For a reliable online amortization calculator, you can visit a trusted financial resource like Bankrate’s Amortization Calculator. The clarity and potential savings you’ll discover are invaluable. Start your journey towards smarter auto financing now!