The Ultimate Guide to Your Income To Debt Ratio For Car Loan: Drive Away with Confidence

The Ultimate Guide to Your Income To Debt Ratio For Car Loan: Drive Away with Confidence Carloan.Guidemechanic.com

Dreaming of that new car smell, the sleek design, or the reliability of an upgraded ride? Getting a car loan is a significant step, and while the excitement is palpable, understanding the financial mechanics behind it is crucial. One of the most pivotal factors lenders scrutinize is your Income To Debt Ratio For Car Loan approval. This isn’t just a number; it’s a snapshot of your financial health, indicating your ability to comfortably manage new monthly payments alongside your existing obligations.

Navigating the world of auto financing can feel complex, but by demystifying your debt-to-income ratio (DTI), you gain immense power. This comprehensive guide will break down everything you need to know about this critical metric. We’ll explore what it is, why it matters, how to calculate it, and most importantly, how to optimize it to secure the best possible car loan terms. Prepare to embark on a journey towards financial literacy that will empower you to drive away with confidence, not just a car.

The Ultimate Guide to Your Income To Debt Ratio For Car Loan: Drive Away with Confidence

What Exactly Is the Income To Debt Ratio (DTI)?

At its core, your Income To Debt Ratio, often simply called Debt-to-Income (DTI) ratio, is a personal finance metric that compares how much you owe each month to how much you earn. Expressed as a percentage, it reveals the portion of your gross monthly income that goes towards servicing your debts. Lenders use this ratio as a primary indicator of your capacity to take on and manage additional debt, such as a new car loan.

From a lender’s perspective, the DTI ratio serves as a vital risk assessment tool. A high DTI suggests that a significant portion of your income is already committed to existing debts, leaving less disposable income for new financial obligations. Conversely, a lower DTI indicates more financial flexibility and a higher likelihood of making timely payments on a new auto loan. It’s essentially their crystal ball into your repayment reliability.

Many financial experts, based on my experience, consider DTI alongside your credit score as the twin pillars of loan eligibility. While your credit score reflects your past payment behavior, your DTI provides a current snapshot of your financial bandwidth. Understanding this distinction is key to preparing a strong car loan application.

Why Your Income To Debt Ratio Matters for a Car Loan

Your Income To Debt Ratio For Car Loan approval is not merely a formality; it’s a cornerstone of the entire lending decision. Lenders aren’t just looking at whether you can afford the monthly payment in isolation; they’re assessing if you can comfortably integrate that payment into your overall financial picture. A healthy DTI signals financial stability, making you a more attractive borrower.

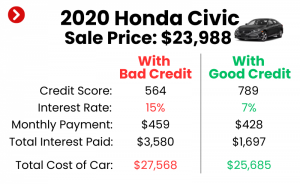

A strong DTI can significantly impact the terms of your auto loan. Borrowers with lower DTIs often qualify for more favorable interest rates, longer repayment periods, or even a higher loan amount. This is because lenders perceive them as lower risk, and they’re willing to offer better conditions to secure their business. A lower interest rate, even by a percentage point, can translate into thousands of dollars saved over the life of the loan.

Conversely, a high DTI can be a major hurdle. It might lead to a denial of your car loan application, or if approved, you might face less attractive terms, such as higher interest rates, shorter repayment periods (leading to higher monthly payments), or a requirement for a larger down payment. Lenders are simply protecting their investment by adjusting terms based on perceived risk.

Pro tips from us: Even before you start test-driving vehicles, calculate your DTI. Knowing this number empowers you to apply for a loan that truly aligns with your financial reality, preventing disappointment and potential credit score dings from multiple hard inquiries if you’re denied. It’s about proactive financial planning for your vehicle financing.

Calculating Your Income To Debt Ratio: A Step-by-Step Guide

Calculating your Income To Debt Ratio for a car loan is a straightforward process, yet it requires careful attention to detail. This simple formula provides a powerful insight into your financial capacity. Let’s break it down into easy steps:

Step 1: Calculate Your Total Monthly Gross Income.

Your gross income is the amount of money you earn before taxes and other deductions are taken out. This includes your salary, wages, commissions, bonuses, and any other regular income streams you receive. If you have multiple jobs or consistent side income, make sure to add all of these figures together to get your total monthly gross income. For self-employed individuals, this might involve averaging your income over a period, usually 12-24 months.

Step 2: List All Your Monthly Debt Payments.

This step requires a comprehensive look at all your recurring debt obligations. Think beyond just minimum payments. Include:

- Mortgage or rent payments

- Student loan payments

- Credit card minimum payments (even if you pay more)

- Personal loan payments

- Alimony or child support payments

- Any existing car loan payments

- Crucially, for a new car loan application, you’ll also need to factor in the estimated monthly payment for the car you intend to purchase. This is where knowing your target car price and potential loan terms becomes vital.

Step 3: Apply the Formula.

Once you have these two figures, simply divide your total monthly debt payments by your total monthly gross income and then multiply by 100 to get a percentage.

Formula: (Total Monthly Debt Payments / Total Monthly Gross Income) x 100 = DTI Percentage

Let’s illustrate with an example:

- Total Monthly Gross Income: $5,000

- Monthly Debt Payments:

- Rent: $1,200

- Student Loan: $250

- Credit Card Minimums: $150

- Estimated New Car Payment: $400

- Total Monthly Debt: $1,200 + $250 + $150 + $400 = $2,000

Calculation: ($2,000 / $5,000) x 100 = 40% DTI

Common mistakes to avoid are forgetting to include all recurring debts, especially smaller ones, or using net income instead of gross income. Lenders always use gross income for DTI calculations. Be thorough and honest with your figures for an accurate assessment of your personal finance.

The Ideal Income To Debt Ratio for Car Loan Approval

While there isn’t a single, universally "perfect" Income To Debt Ratio that guarantees car loan approval, there are general benchmarks that lenders prefer. Most financial institutions and experts suggest that an overall DTI of 36% or lower is considered excellent. This 36% often includes your housing costs (mortgage or rent).

For many auto lenders, they typically look for a DTI that does not exceed 43%. This 43% threshold is often cited as the maximum acceptable DTI for many types of loans, including mortgages and auto loans. If your DTI is above this, you might find it challenging to secure favorable loan terms, or even get approved at all, especially if other factors like your credit score aren’t exceptionally strong.

It’s important to understand that your DTI is one piece of a larger puzzle. A lower DTI indicates less risk, potentially leading to better interest rates and more flexible loan terms. From a professional standpoint, aiming for a DTI as low as possible is always beneficial. It not only increases your chances of approval but also ensures that your new car payment won’t strain your budget, contributing to better financial health.

Lenders might also consider a "front-end" DTI, which focuses solely on housing costs relative to gross income, and a "back-end" DTI, which includes all other debts. For car loans, the back-end DTI is usually the more significant figure. Keep in mind that every lender has its own specific criteria and risk appetite, so what one lender accepts, another might decline.

Strategies to Improve Your Income To Debt Ratio Before Applying

Improving your Income To Debt Ratio For Car Loan approval isn’t about magic; it’s about strategic financial planning and discipline. By proactively managing your income and debt, you can significantly enhance your borrowing capacity and secure better auto loan terms. Here are effective strategies:

1. Increase Your Income:

This is often the most direct way to lower your DTI. More income means the same amount of debt takes up a smaller percentage. Consider avenues like:

- Asking for a Raise: If you’ve been excelling at your job, now might be the time to discuss a salary increase.

- Taking on a Side Hustle: Freelancing, consulting, or part-time work can provide a valuable boost to your monthly earnings.

- Selling Unused Items: A one-time influx of cash from selling belongings can help pay down a lump sum of debt, indirectly improving your DTI over time.

2. Reduce Your Debt:

This strategy focuses on decreasing the numerator in your DTI calculation. Every dollar you pay off reduces your monthly debt obligations.

- Pay Down High-Interest Debt First: Focus on credit card balances with the highest interest rates. This minimizes the total interest you pay and frees up more of your income.

- Consolidate Debt: Consider consolidating multiple high-interest debts into a single loan with a lower interest rate. This can reduce your overall monthly debt payment, making your DTI more favorable.

- Avoid New Debt: During the period leading up to your car loan application, refrain from opening new credit cards or taking on additional loans. Every new debt commitment impacts your DTI negatively.

3. Lower Your Proposed Car Payment:

If you’ve already calculated your DTI and it’s on the higher side, adjusting your car loan expectations can make a difference.

- Consider a Less Expensive Vehicle: A lower purchase price means a smaller loan amount and, consequently, a smaller monthly payment.

- Make a Larger Down Payment: A substantial down payment reduces the principal amount you need to borrow, which directly lowers your monthly payment and improves your loan-to-value (LTV) ratio.

- Explore Longer Loan Terms (with caution): While a longer term can reduce monthly payments, be aware that it often means paying more in interest over the life of the loan. Weigh the pros and cons carefully.

4. Budgeting and Financial Planning:

A robust budget is your roadmap to financial control. Create a realistic monthly budget that tracks all your income and expenses. This will help you identify areas where you can cut back spending to free up funds for debt repayment or savings. For more detailed budgeting strategies, check out our guide on . Consistent financial planning demonstrates responsibility and improves your overall financial standing, which lenders appreciate. Pro tip: Stick to your budget for at least 3-6 months before applying for a major loan to show a consistent financial habit.

Beyond DTI: Other Factors Lenders Consider for Your Auto Loan

While your Income To Debt Ratio For Car Loan is a major player, it’s certainly not the only factor lenders weigh. A comprehensive assessment of your creditworthiness involves several other crucial elements. Understanding these can further enhance your chances of securing the best possible auto loan.

1. Credit Score and History:

Your credit score is a numerical representation of your creditworthiness, reflecting your payment history, amounts owed, length of credit history, new credit, and credit mix. A strong credit score (typically 670 and above) demonstrates a history of responsible borrowing and repayment. Lenders often use this score to determine your interest rate, with higher scores usually leading to lower rates.

External Link: To understand more about what makes up your credit score and how to improve it, visit a trusted source like Experian: https://www.experian.com/

2. Down Payment Amount:

Making a significant down payment on your vehicle can dramatically improve your loan application. A larger down payment reduces the amount you need to borrow, thereby decreasing the lender’s risk. It also signals your financial commitment to the purchase and can lead to a lower monthly payment and better loan terms. Aim for at least 10-20% of the car’s value if possible.

3. Job Stability and Employment History:

Lenders want assurance that you have a consistent and reliable source of income to make your monthly payments. A stable employment history, typically two years or more with the same employer or in the same industry, is highly favorable. Frequent job changes or gaps in employment can raise red flags for lenders.

4. Loan-to-Value (LTV) Ratio:

The LTV ratio compares the amount you are borrowing to the actual value of the car. If you’re borrowing more than the car is worth (e.g., rolling negative equity from a trade-in into a new loan), your LTV will be high. Lenders prefer a lower LTV because it means they have less risk if the car needs to be repossessed. A high LTV can make loan approval more difficult or result in higher interest rates.

5. Savings and Assets:

Having a healthy savings account or other liquid assets can also bolster your application. This demonstrates financial prudence and provides an additional layer of security for lenders, suggesting you have a buffer in case of unexpected financial challenges. An emergency fund, for instance, shows you’re prepared for unforeseen circumstances.

Common Mistakes to Avoid When Applying for a Car Loan

Navigating the car loan process can be tricky, and even well-intentioned applicants can make mistakes that hinder their chances of approval or lead to less favorable terms. Being aware of these common pitfalls can save you time, money, and frustration.

1. Not Knowing Your Income To Debt Ratio:

Perhaps the most significant oversight is going into the application process without understanding your DTI. This leaves you guessing about your financial standing and vulnerable to unfavorable offers. Always calculate your DTI beforehand.

2. Applying for Too Much Loan:

It’s easy to get carried away by the allure of a luxury vehicle. However, applying for a loan that stretches your budget, and consequently your DTI, beyond reasonable limits is a common error. This often leads to denial or a loan with unmanageable monthly payments.

3. Ignoring Your Credit Score:

Your credit score is your financial report card. Neglecting to check it before applying means you might miss errors or opportunities to improve it. A low credit score, combined with a high DTI, is a recipe for loan denial.

4. Skipping the Pre-Approval Process:

Many buyers go straight to the dealership without getting pre-approved for a loan. Pre-approval gives you a clear understanding of what you can afford, what interest rates you qualify for, and empowers you to negotiate effectively, essentially turning you into a cash buyer at the dealership.

5. Not Budgeting for All Car Expenses:

A car loan payment is just one piece of the puzzle. Many applicants forget to factor in other essential costs like insurance, fuel, maintenance, registration, and potential repairs. These expenses can quickly add up and strain your budget, even if your DTI seems healthy initially. Learn more about securing the best auto loan rates in our article: .

6. Applying to Too Many Lenders Simultaneously:

While it’s wise to shop around for the best rates, applying to numerous lenders within a short period can negatively impact your credit score due to multiple hard inquiries. Group your applications within a 14-45 day window to have them count as a single inquiry.

Conclusion: Drive Away with Financial Confidence

Understanding and optimizing your Income To Debt Ratio For Car Loan approval is not just about getting the keys to your dream car; it’s about making a financially sound decision that supports your long-term well-being. This critical metric serves as a powerful indicator of your financial health, directly influencing a lender’s willingness to extend credit and the terms they offer.

By proactively calculating your DTI, implementing strategies to improve it, and being mindful of other factors lenders consider, you position yourself as a responsible and attractive borrower. Remember, a car loan is a significant financial commitment, and approaching it with knowledge and preparation will save you stress and money in the long run.

Don’t let the excitement of a new vehicle overshadow the importance of financial preparedness. Take control of your debt-to-income ratio, refine your financial habits, and empower yourself to secure an auto loan that fits comfortably within your budget. Drive away not just with a new car, but with the confidence of knowing you’ve made a smart financial choice.