The Ultimate Guide: What Credit Score Do You Need To Qualify For A Car Loan?

The Ultimate Guide: What Credit Score Do You Need To Qualify For A Car Loan? Carloan.Guidemechanic.com

Buying a car is a significant milestone, a blend of excitement and practical necessity. For many, it represents freedom, convenience, and a step forward in life. Yet, for all the joy a new set of wheels can bring, the journey to financing that vehicle often begins with a single, crucial number: your credit score. Understanding your credit score to qualify for a car loan isn’t just about getting approved; it’s about unlocking the best possible terms, saving thousands over the life of your loan, and making a financially savvy decision.

Based on my experience as an expert in personal finance and auto lending, navigating the world of car loans can feel like deciphering a complex code. Lenders use your credit score as their primary crystal ball, predicting your reliability as a borrower. This comprehensive guide will demystify everything you need to know, from the ideal credit score to the strategies for securing a great auto loan, regardless of your current financial standing. Let’s dive deep into making your car ownership dreams a reality.

The Ultimate Guide: What Credit Score Do You Need To Qualify For A Car Loan?

What Exactly Is a Credit Score and Why Does It Hold Such Weight for Car Loans?

Before we talk numbers, let’s establish a foundational understanding. A credit score is a three-digit number, typically ranging from 300 to 850, that acts as a snapshot of your creditworthiness. It’s a numerical representation of your financial history, reflecting how responsibly you’ve managed debt in the past. The most commonly used models are FICO and VantageScore.

For lenders, this score is an indispensable tool. When you apply for a car loan, they’re essentially taking a calculated risk on you. Your credit score helps them quantify that risk. A higher score signals a lower risk, indicating that you’re likely to make your payments on time and fulfill your financial obligations. Conversely, a lower score suggests a higher risk, raising concerns about potential defaults.

The implications of this score extend far beyond a simple "yes" or "no" on your loan application. It directly influences the interest rate you’ll be offered, the loan term, the amount of your down payment, and even the type of car you can realistically afford. A difference of just a few percentage points in your interest rate can translate into thousands of dollars over a five-year loan period. This is why understanding and improving your credit score to qualify for a car loan is absolutely paramount.

Demystifying Credit Score Ranges for Car Loan Qualification

There isn’t a universal "magic number" that guarantees a car loan, but credit scores are generally categorized into ranges that lenders use as guidelines. Knowing where you stand within these ranges will give you a realistic expectation of what to expect during the application process.

Let’s break down the common credit score tiers and what they typically mean for auto loan applicants:

-

Excellent Credit (780-850): This is the gold standard. Borrowers in this range are seen as extremely low risk. They consistently pay their bills on time, have a long credit history, and manage their debt responsibly. With excellent credit, you’re likely to qualify for the lowest interest rates available, flexible loan terms, and require minimal down payment. You’ll have your pick of lenders vying for your business.

-

Good Credit (670-739): A solid credit score places you firmly in the "good" category. Most Americans fall into this range. Lenders view these applicants as reliable, and while you might not get the absolute lowest rates, you’ll still qualify for very competitive interest rates and favorable loan terms. You should have no trouble securing a car loan.

-

Fair/Average Credit (580-669): This range indicates that you might have some blemishes on your credit history, such as a few late payments or higher debt. While you can certainly get a car loan with a fair credit score, expect higher interest rates than those with good or excellent credit. Lenders might also require a larger down payment or a co-signer to mitigate their risk.

-

Poor Credit (300-579): Borrowers with poor credit scores typically have a history of missed payments, defaults, or even bankruptcies. Qualifying for a traditional car loan in this range can be challenging. If approved, expect significantly higher interest rates, stricter terms, and often a requirement for a substantial down payment or a co-signer. It’s not impossible, but it requires more effort and potentially higher costs.

Understanding these categories is your first step in preparing for a car loan. It helps you set realistic expectations and strategize your approach.

The "Magic Number": What Credit Score Do You Really Need?

Many people wonder, "What’s the absolute minimum credit score to qualify for a car loan?" The truth is, there isn’t a single, definitive "magic number" that applies to everyone. While lenders certainly have thresholds, the actual minimum score for approval is fluid and depends on several factors.

Based on my experience working with countless individuals, most traditional lenders prefer to see a FICO score of at least 620-640 for a standard auto loan. However, it’s entirely possible to get approved with a score lower than that, especially if you explore specific avenues. Conversely, having a score above 700 will almost always put you in a strong position to secure excellent terms.

The "minimum" is less about a fixed digit and more about the lender’s overall risk assessment. Some lenders specialize in subprime loans, catering to individuals with lower credit scores. While they offer approvals, these often come with much higher interest rates to compensate for the increased risk. Therefore, while a car loan might be accessible even with a score in the low 500s, the cost of that loan could be prohibitive. Aiming for at least a "fair" credit score (580+) gives you more options and better rates.

Beyond the Score: Factors Lenders Consider for Your Car Loan

While your credit score is undeniably central, it’s not the only piece of the puzzle. Lenders conduct a holistic review of your financial profile. Pro tips from us suggest understanding these additional factors can significantly bolster your application, even if your credit score isn’t perfect.

Here are other critical elements lenders scrutinize:

-

Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders typically prefer a DTI ratio of 43% or less, though some might go higher for auto loans. A lower DTI indicates that you have ample income to cover your existing obligations plus the new car payment, making you a less risky borrower.

-

Payment History: Even within your credit score, your payment history carries immense weight. A consistent record of on-time payments, especially for other installment loans, demonstrates reliability. Conversely, recent late payments, even if your score is decent, can raise red flags. Lenders look for stability and a pattern of responsible behavior.

-

Down Payment Amount: A substantial down payment is a powerful tool. It reduces the amount you need to borrow, thereby lowering the lender’s risk. It also shows your financial commitment to the vehicle. For those with lower credit scores, a larger down payment can often be the key to approval or to securing a more favorable interest rate.

-

Loan Term: The length of your loan (e.g., 36, 60, 72 months) impacts your monthly payment and the total interest paid. Lenders consider longer terms riskier because there’s more time for things to go wrong. While a longer term means lower monthly payments, it often results in higher overall interest.

-

Vehicle Age and Type: The car you choose also plays a role. Newer, more expensive vehicles might require a higher credit score or more stringent qualifications. Used cars, especially older models, can sometimes be easier to finance, but their interest rates might be higher due to perceived lower collateral value.

-

Employment Stability: Lenders want to see a steady source of income. A long history with the same employer or a stable career path reassures them of your ability to make consistent payments. Frequent job changes or gaps in employment can be a concern.

By presenting a strong profile across these areas, you can significantly improve your chances of approval and secure better terms, even if your credit score to qualify for a car loan isn’t in the "excellent" range.

How Your Credit Score Directly Influences Your Car Loan Terms

The link between your credit score and your car loan terms is direct and profound. It’s the primary determinant of how much you’ll ultimately pay for your vehicle. Let’s break down these critical connections.

-

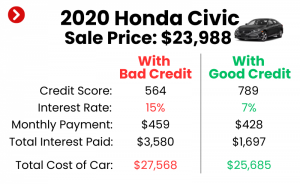

Interest Rates: This is arguably the most significant impact. Borrowers with excellent credit scores (780+) can often qualify for interest rates below 5%, sometimes even as low as 0% during special promotions. Those with good credit (670-739) might see rates in the 5-10% range. However, for individuals with fair credit (580-669), rates can jump to 10-18%, and for poor credit (under 580), it’s not uncommon to see rates exceeding 20% or even 25%. Over a five-year loan, these differences add up to thousands of dollars in extra payments.

-

Monthly Payments: A higher interest rate directly translates to a higher monthly payment for the same loan amount and term. This can strain your budget and impact your overall financial health. Conversely, a lower interest rate makes your car more affordable on a month-to-month basis.

-

Loan Approval Probability: As discussed, your credit score is the primary gatekeeper for loan approval. A higher score significantly increases your chances of getting approved by a wider range of lenders. A lower score narrows your options and may lead to rejections from traditional banks.

-

Down Payment Requirements: Lenders often require a larger down payment from borrowers with lower credit scores. This is a way for them to reduce their risk exposure. If you have excellent credit, you might not need any down payment at all.

-

Loan Term Flexibility: With a strong credit score, you’ll have more flexibility in choosing your loan term. You could opt for a shorter term to pay off the car faster and save on interest, or a slightly longer term for lower monthly payments without a drastic increase in your interest rate. Less-than-perfect credit often limits you to specific, sometimes less desirable, loan terms.

Pro tips from us: Always get pre-qualified with multiple lenders before stepping into a dealership. This allows you to compare offers based on your specific credit score and understand the best rates available to you. Knowledge is power, and comparing offers can save you a substantial amount of money.

Strategies to Improve Your Credit Score Before Applying for a Car Loan

If your current credit score isn’t where you want it to be, don’t despair! You can take proactive steps to improve it, which will directly impact your credit score to qualify for a car loan with better terms. Even a modest improvement can make a big difference.

Here are actionable strategies:

-

Pay All Bills On Time, Every Time: Your payment history accounts for 35% of your FICO score. This is the single most important factor. Set up automatic payments or reminders to ensure you never miss a due date on credit cards, existing loans, utilities, or any other financial obligation. Consistency is key.

-

Reduce Existing Debt: High credit card balances, especially close to your credit limit, negatively impact your credit utilization ratio (how much credit you’re using versus how much you have available). Aim to keep your credit utilization below 30% of your total available credit. Paying down existing debts frees up your credit and shows lenders you’re not overextended.

-

Check Your Credit Report for Errors: Regularly obtain your free credit reports from Equifax, Experian, and TransUnion (via AnnualCreditReport.com). Mistakes can happen, and incorrect information (like accounts you don’t own, incorrect late payments, or identity theft) can unfairly drag down your score. Dispute any inaccuracies immediately.

-

Avoid New Credit Applications: Each time you apply for new credit, a "hard inquiry" appears on your report, which can slightly lower your score for a short period. While shopping for car loans within a specific window (typically 14-45 days) counts as a single inquiry, avoid applying for new credit cards or other loans just before or during your car loan application process.

-

Become an Authorized User: If you have a trusted family member with excellent credit, they might add you as an authorized user on one of their credit card accounts. Their positive payment history can then reflect on your credit report, boosting your score. Ensure they are responsible with their credit, as their mistakes could also affect you.

Common mistakes to avoid are closing old credit card accounts (which can reduce your available credit and shorten your credit history) and making only minimum payments on high-interest debt. Focus on paying down the principal to see real improvement. Improving your credit takes time, but even a few months of diligent effort can yield positive results.

Applying for a Car Loan with Less-Than-Perfect Credit

Having a lower credit score to qualify for a car loan doesn’t mean car ownership is out of reach. It simply means you might need to adjust your expectations and explore different avenues. It’s crucial to be realistic and strategic.

Here are viable options for those with less-than-perfect credit:

-

Subprime Lenders: Many lenders specialize in working with individuals who have lower credit scores (often below 620). These lenders understand that life happens and are willing to take on more risk. Be prepared for higher interest rates, but these loans can be a stepping stone to rebuilding your credit if managed responsibly.

-

Consider a Co-signer: A co-signer, typically a trusted family member or friend with good credit, agrees to be equally responsible for the loan if you default. Their strong credit profile can help you get approved and secure a better interest rate than you’d get on your own. Ensure both parties understand the full implications of co-signing.

-

Secured Loans: Some lenders offer secured auto loans, where the car itself acts as collateral. This can make approval easier for those with lower credit, as the lender has a tangible asset to recover if you fail to pay. However, it also means you risk losing the car if you default.

-

Make a Larger Down Payment: As mentioned earlier, a substantial down payment reduces the loan amount and the lender’s risk. If you can save up 20% or more of the car’s purchase price, you’ll significantly improve your chances of approval and potentially lower your interest rate, even with a challenging credit score.

-

Opt for a Used Car: Financing an older, less expensive used car can be easier than financing a brand-new vehicle. The loan amount will be smaller, reducing the overall risk for the lender. This can be a smart move to get reliable transportation while you work on improving your credit. .

Remember, the goal with a lower credit score is not just to get approved, but to get approved for a loan you can comfortably afford and use to build positive credit history for the future.

The Application Process: What to Expect and How to Navigate It

Once you’ve done your homework on your credit score to qualify for a car loan and explored your options, it’s time to apply. Understanding the process can reduce stress and help you make informed decisions.

-

Pre-qualification vs. Pre-approval:

- Pre-qualification: This is a soft inquiry that doesn’t affect your credit score. It gives you an estimate of what loan amount you might qualify for and at what interest rate. It’s a great starting point for budgeting.

- Pre-approval: This involves a hard inquiry, which will temporarily impact your credit score. However, it provides you with a firm offer for a specific loan amount and interest rate, allowing you to shop for a car with confidence, knowing exactly how much you can spend.

-

"Hard Inquiries" and Their Impact: When you formally apply for a loan, lenders perform a "hard inquiry" on your credit report. This slightly lowers your score for a few months. However, FICO and VantageScore models understand that consumers shop around for the best rates. Multiple auto loan inquiries within a specific timeframe (usually 14-45 days, depending on the scoring model) are typically treated as a single inquiry, minimizing the impact on your score. So, shop around for rates within a concentrated period.

-

Shopping Around for Rates: This is a crucial step that many skip. Don’t just accept the first offer you receive, especially from the dealership. Get quotes from banks, credit unions, and online lenders. Comparing at least three to four offers can reveal significant differences in interest rates and terms, potentially saving you thousands.

-

Documentation Needed: Be prepared to provide various documents, including:

- Proof of identity (driver’s license, passport)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- Social Security Number

- Vehicle information (if you’ve already chosen a car)

Having all your documents ready streamlines the application process and shows lenders you are serious and organized.

Maintaining Good Credit Post-Loan Approval

Getting your car loan approved is a fantastic achievement, but the journey doesn’t end there. The period after approval is just as critical for your financial health and future credit score. Your responsible behavior post-loan will reinforce your creditworthiness and open doors to even better financial opportunities down the line.

-

Making Timely Payments: This is non-negotiable. Your car loan payments will be reported to the credit bureaus. Each on-time payment is a positive mark on your credit history, steadily building your score. Conversely, a single late payment can severely damage the progress you’ve made. Set up automatic payments or calendar reminders to ensure you never miss a due date.

-

Avoiding New Debt: While you’re paying off your car loan, try to avoid taking on significant new debt, especially high-interest credit card debt. Keep your credit utilization low. New debt can increase your debt-to-income ratio and make it harder to manage your current obligations.

-

Monitoring Your Credit: Continue to check your credit reports periodically. Ensure that your car loan payments are being reported accurately and that there are no new errors or fraudulent activities. Monitoring your credit helps you stay on top of your financial health and catch any issues early. .

By consistently demonstrating responsible financial habits throughout the life of your car loan, you’re not just paying for your vehicle; you’re actively building a stronger credit profile that will benefit you for years to come, making future financing, whether for a home or another car, much easier and more affordable.

Conclusion: Your Road to a Great Car Loan Starts Here

Navigating the world of car loans with a clear understanding of your credit score to qualify for a car loan is your most powerful tool. It’s more than just a number; it’s a reflection of your financial reliability and a gateway to better interest rates, lower monthly payments, and overall savings.

We’ve covered everything from understanding what your credit score means to the specific ranges lenders look for, the other factors they consider, and crucial strategies for improving your score or getting approved even with less-than-perfect credit. Remember, knowledge and preparation are your best allies. By taking the time to understand your credit, improve where possible, and strategically approach the application process, you empower yourself to make a smart financial decision that serves your needs now and in the future.

Don’t let the complexity deter you. With this comprehensive guide, you’re now equipped to confidently pursue your car ownership dreams. Drive informed, drive smart!

External Resource: For an in-depth understanding of your FICO Score and how it’s calculated, visit the official FICO website: https://www.fico.com/