The Ultimate Guide: What Credit Score Do You Really Need for a Car Loan Without a Cosigner?

The Ultimate Guide: What Credit Score Do You Really Need for a Car Loan Without a Cosigner? Carloan.Guidemechanic.com

The open road, the fresh scent of a new (or new-to-you) car, and the independence of owning your own vehicle – it’s a dream many of us share. However, for many, the path to car ownership hits a roadblock: securing a car loan, especially when you’re flying solo without a cosigner. The question that often looms largest is: "What credit score do I really need for a car loan without a cosigner?"

Navigating the world of auto financing can feel like a complex maze, particularly when your credit history isn’t perfect. Lenders scrutinize your financial past to assess risk, and your credit score is their primary report card. This comprehensive guide will demystify the credit score requirements, explore what else lenders consider, and arm you with strategies to secure that car loan approval without needing a cosigner. We’re here to transform confusion into confidence, providing you with actionable insights to drive off the lot with keys in hand.

The Ultimate Guide: What Credit Score Do You Really Need for a Car Loan Without a Cosigner?

Understanding Your Credit Score: The Foundation of Auto Financing

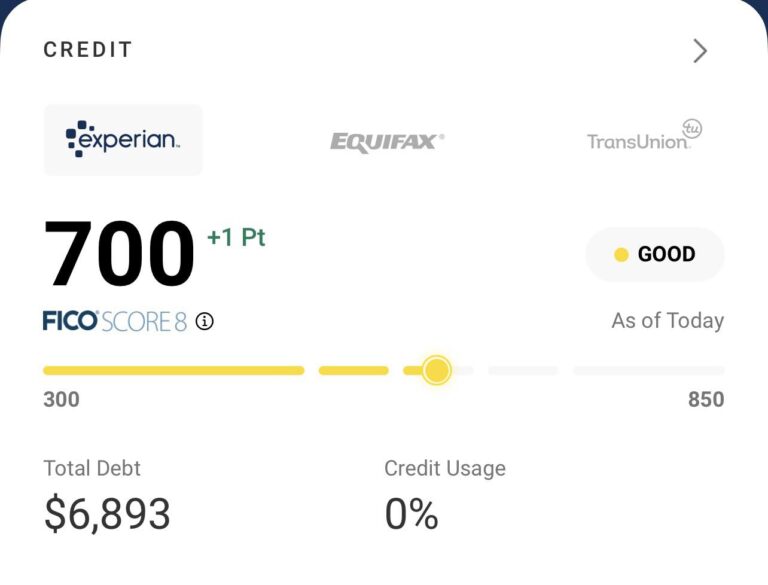

Before we dive into specific numbers, it’s crucial to grasp what a credit score is and why it holds so much weight in the lending world. Essentially, your credit score is a three-digit number that represents your creditworthiness – your ability to repay borrowed money. It’s a snapshot of your financial responsibility, compiled from your credit reports by agencies like Experian, Equifax, and TransUnion.

The most widely used scoring models are FICO and VantageScore, both ranging from 300 to 850. A higher score indicates lower risk to lenders, making you a more attractive borrower. Lenders use this score to determine not only if they’ll approve your loan but also the interest rate they’ll offer you.

Based on my experience helping countless individuals navigate auto financing, understanding your credit score is the absolute first step. It’s like checking the weather before planning an outdoor event; you need to know what you’re up against. Lenders want to see a history of responsible borrowing, and your credit score condenses that history into an easily digestible number for them.

The General Credit Score Ranges:

- Excellent: 780-850

- Very Good: 740-779

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

Knowing where you stand in these ranges will give you a realistic expectation of your loan prospects. The goal, naturally, is to aim for the "good" or "excellent" categories for the most favorable terms.

The Magic Number: What Credit Score Do You Really Need for a Car Loan Without a Cosigner?

Let’s cut to the chase: there isn’t one single "magic number" that guarantees a car loan without a cosigner. However, there are general thresholds and expectations that significantly impact your chances and the terms you’ll receive. Lenders typically prefer borrowers with a good to excellent credit score because it signifies a lower risk of default.

For a standalone car loan approval, most conventional lenders look for a credit score of 670 or higher. This range is generally considered "Good" and puts you in a strong position to secure competitive interest rates and favorable loan terms. With a score in this bracket, lenders view you as a reliable borrower.

However, it’s entirely possible to get a car loan without a cosigner with a credit score in the "Fair" range, typically between 580 and 669. While approval is still achievable, you should prepare for higher interest rates. Lenders will perceive you as a moderate risk, and they’ll compensate for that risk by charging more for the loan.

If your credit score falls into the "Poor" category, below 580, securing a car loan without a cosigner becomes significantly more challenging. It’s not impossible, but it often requires specific strategies, a larger down payment, or exploring subprime lenders who specialize in higher-risk loans. These loans typically come with very high interest rates and stricter terms.

Pro tips from us at emphasize that even if your score is on the lower end, showing stability in other areas of your financial life can tip the scales in your favor. Never assume you won’t be approved; always explore your options.

Beyond the Score: Other Factors Lenders Consider for Your Car Loan

While your credit score is a major player, it’s by no means the only factor lenders evaluate when you apply for a car loan without a cosigner. They perform a holistic assessment to get a complete picture of your financial health and repayment capability. Ignoring these additional elements would be a common mistake.

Understanding these factors allows you to strengthen your application even if your credit score isn’t perfect. It demonstrates to lenders that you are a responsible borrower in other aspects of your life.

Here are the critical elements lenders scrutinize:

1. Your Income and Debt-to-Income (DTI) Ratio

Lenders want to ensure you have a stable and sufficient income to comfortably make your monthly car payments. They’ll look at your gross monthly income and compare it to your existing monthly debt obligations (mortgage/rent, credit card payments, student loans, etc.). This calculation is known as your Debt-to-Income (DTI) ratio.

A lower DTI ratio indicates you have more disposable income to cover new debt, making you a less risky borrower. Generally, lenders prefer a DTI ratio below 43%, though some may accept slightly higher depending on other factors. A high DTI can be a red flag, regardless of your credit score.

2. Employment History

Stability in employment signals financial reliability. Lenders prefer to see a consistent work history, ideally with the same employer for at least one to two years. Frequent job changes, especially within a short period, might raise concerns about your income stability and ability to repay the loan consistently.

If you’re self-employed, be prepared to provide more extensive documentation, such as tax returns and bank statements, to prove your income.

3. Payment History

This is perhaps the most influential component of your credit score, and lenders review it directly from your credit report. They want to see a consistent track record of on-time payments across all your credit accounts. A history of missed or late payments, bankruptcies, or foreclosures will significantly hurt your chances of approval and lead to higher interest rates.

Demonstrating a solid payment history, even for small bills, builds trust with potential lenders.

4. Length of Credit History

The longer your credit history, the better. Lenders appreciate seeing how you’ve managed credit over an extended period. A long history with responsible behavior provides more data points for them to assess your risk.

If you’re new to credit, securing a car loan without a cosigner can be more challenging, as lenders have less information to base their decision on. However, this doesn’t mean it’s impossible; other factors like income and down payment become even more crucial.

5. Credit Mix and Utilization

A healthy credit mix (a combination of revolving credit like credit cards and installment loans like student loans or mortgages) shows you can manage different types of debt responsibly. Lenders also pay close attention to your credit utilization ratio – how much of your available credit you’re using.

Keeping your credit utilization low (ideally below 30%) indicates you’re not over-reliant on credit and manage your finances well. High utilization can suggest financial strain, even if you make payments on time.

6. Down Payment Amount

A significant down payment is one of your strongest allies when applying for a car loan without a cosigner, especially if your credit score is less than ideal. A larger down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. It also demonstrates your financial commitment and ability to save.

From a lender’s perspective, a substantial down payment means less money they have to potentially lose if you default on the loan. It can often be the deciding factor in approval.

7. Vehicle Age and Value

The type of car you choose can also influence your loan approval and interest rate. Lenders often view newer, more valuable cars as less risky because they hold their value better as collateral. Older, high-mileage vehicles might be harder to finance, as their depreciation rate is higher, and their resale value is lower.

Common mistakes to avoid are applying for a loan for a car that is significantly older or has very high mileage if your credit profile isn’t strong. This adds another layer of risk for the lender.

Strategies for Securing a Car Loan Without a Cosigner (Even with Less-Than-Perfect Credit)

Don’t despair if your credit score isn’t in the "excellent" range. There are several proactive steps you can take to significantly improve your chances of securing a car loan without a cosigner. These strategies focus on presenting yourself as the most reliable borrower possible.

1. Improve Your Credit Score (If Time Allows)

This is the most direct route to better loan terms. If you’re not in a rush, dedicating a few months to boosting your score can save you thousands in interest.

- Pay All Bills On Time: Payment history is paramount. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Credit Card Balances: Lowering your credit utilization ratio can provide a quick boost. Pay down high-interest credit card debt.

- Dispute Errors on Your Credit Report: Obtain your free credit reports from AnnualCreditReport.com and meticulously check for inaccuracies. Disputing and correcting errors can instantly improve your score.

- Avoid New Credit Applications: Each hard inquiry can temporarily ding your score. Refrain from opening new credit accounts in the months leading up to your car loan application.

2. Save for a Larger Down Payment

As mentioned, a substantial down payment is a powerful tool. Aim for at least 10-20% of the vehicle’s price, if not more. Not only does it reduce the amount you need to borrow, but it also signals financial prudence to lenders. This can be especially impactful if your credit history is a bit shaky.

A larger down payment also means lower monthly payments and less interest paid over the life of the loan. It’s a win-win situation.

3. Consider a Used Car or a Less Expensive Model

While the allure of a brand-new car is strong, opting for a reliable used vehicle or a more budget-friendly new model can make a significant difference. A lower total loan amount means less risk for the lender, making them more likely to approve your application.

Additionally, interest rates might be slightly higher for used cars, but the overall principal amount is less, potentially making the monthly payments more manageable.

4. Shop Around Aggressively for Loan Offers

Never take the first loan offer you receive, especially from a dealership. Competition among lenders is fierce, and different institutions have varying lending criteria and interest rates.

- Banks: Traditional banks often offer competitive rates to their existing customers.

- Credit Unions: These member-owned institutions are known for offering lower interest rates and more flexible terms, especially for those with less-than-perfect credit.

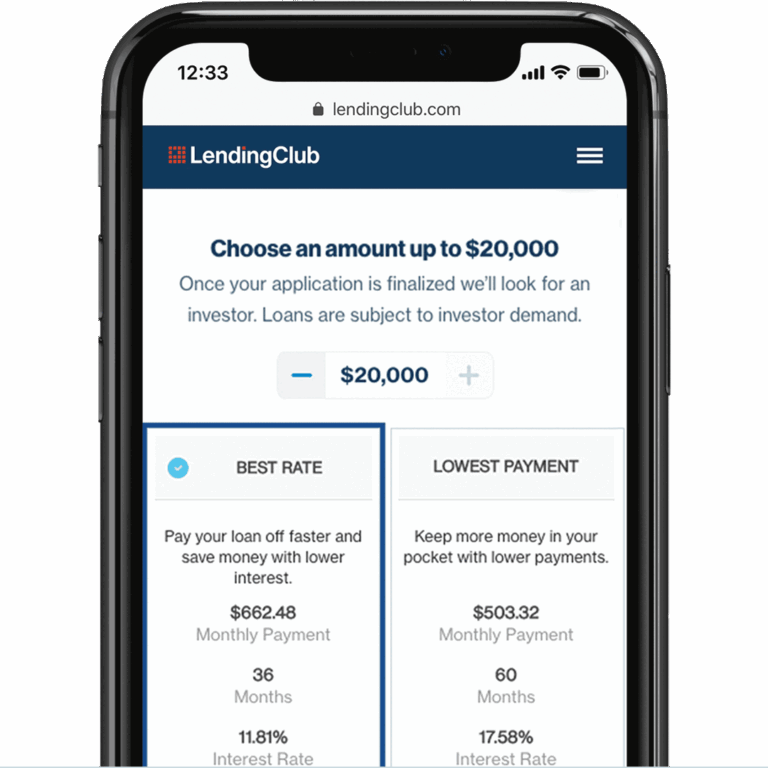

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others offer convenient online applications and competitive rates.

- Dealership Financing: While convenient, dealership financing (often through captive finance companies like Ford Credit or GM Financial) may not always offer the best rates, especially for those without excellent credit. However, they sometimes have special programs for specific credit tiers.

Get pre-approved from at least 2-3 different lenders before you even step foot on a dealership lot. This gives you leverage and a clear understanding of what you can afford.

5. Get Pre-Approved Before You Shop

Pre-approval is a game-changer. It means a lender has reviewed your credit and financial information and is willing to lend you a specific amount at a particular interest rate, usually valid for 30-60 days. This transforms you into a cash buyer at the dealership, allowing you to focus solely on negotiating the car’s price, not the financing terms.

It eliminates the pressure of in-the-moment financing decisions and helps you stick to your budget.

6. Understand Your Budget and Stick To It

It’s tempting to stretch your budget for a car you truly desire, but overextending yourself is a common pitfall. Beyond the monthly loan payment, remember to factor in insurance, fuel, maintenance, and registration fees. A car payment should ideally not exceed 10-15% of your net monthly income.

Use online calculators to estimate total costs and ensure the car fits comfortably within your overall financial plan.

7. Consider a Shorter Loan Term

While a longer loan term (e.g., 72 or 84 months) offers lower monthly payments, it also means you’ll pay significantly more in interest over the life of the loan. If you can afford it, opt for a shorter term, such as 36 or 48 months. This reduces the total interest paid and gets you out of debt faster.

8. Build a Relationship with a Local Credit Union

For individuals with fair or even somewhat poor credit, credit unions can be a godsend. They often take a more personalized approach to lending, looking beyond just the credit score. If you have an existing relationship, or are willing to open an account, they might be more flexible.

The Application Process: What to Expect

Once you’ve done your homework and chosen a lender, the application process for a car loan without a cosigner involves a few key steps:

- Gather Your Documents: You’ll typically need proof of identity (driver’s license), proof of income (pay stubs, tax returns), proof of residence (utility bill), and potentially bank statements. Having these ready will streamline the process.

- Submit Your Application: This can be done online, in person, or over the phone. You’ll provide personal, employment, and financial information.

- Credit Check: The lender will perform a hard inquiry on your credit report. This will temporarily lower your score by a few points, but multiple inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are usually grouped as one for scoring purposes.

- Review the Offer: If approved, carefully review the loan offer. Pay close attention to the Annual Percentage Rate (APR), the loan term, and the total monthly payment. Don’t hesitate to ask questions if anything is unclear.

- Negotiate (if possible): Sometimes, there’s room for negotiation on the interest rate or loan terms, especially if you have multiple pre-approvals. Use any other offers as leverage.

Remember, transparency is key. Be honest about your financial situation, and don’t try to hide any issues.

When a Cosigner Might Be Your Best Option (Even if You Don’t Want One)

Despite all the strategies, there might be situations where securing a car loan without a cosigner is simply not feasible. This is often the case for individuals with very low credit scores (below 550), extremely limited credit history, or a high debt-to-income ratio. In these instances, a cosigner can be the bridge to approval.

A cosigner is someone with excellent credit who agrees to take on the legal responsibility for the loan if you fail to make payments. This significantly reduces the lender’s risk. While it grants you access to financing and potentially better terms, it’s a serious commitment for the cosigner, as their credit will also be impacted if you miss payments.

Using a cosigner can be a strategic move to get your first car loan and start building your own credit history. Once you’ve made consistent, on-time payments for a year or two, you might be able to refinance the loan in your name alone, effectively removing the cosigner and further boosting your independent credit profile.

Conclusion: Drive Towards Your Dream Car with Confidence

Securing a car loan without a cosigner is a very achievable goal, even if your credit history isn’t perfect. While a good credit score (670+) undoubtedly opens the door to the best rates, it’s crucial to remember that lenders consider a comprehensive range of factors, from your income stability to the size of your down payment. You are more than just a three-digit number.

By understanding how lenders evaluate your application and by proactively implementing the strategies we’ve outlined, you can significantly improve your chances of approval. Focus on building strong financial habits, saving for a down payment, and meticulously shopping for the best loan terms. Don’t be afraid to explore all your options, from credit unions to online lenders, and always get pre-approved to empower your car-buying journey.

The road to car ownership might have a few turns, but with the right knowledge and preparation, you can confidently navigate it solo. Start your journey today by checking your credit score, assessing your financial situation, and preparing to present your best self to lenders. Your dream car awaits!