The Ultimate Roadmap to Financial Freedom: Decoding Your Car Loan Amortization Chart

The Ultimate Roadmap to Financial Freedom: Decoding Your Car Loan Amortization Chart Carloan.Guidemechanic.com

Buying a new car is often an exhilarating experience. The scent of a fresh interior, the hum of a new engine, and the promise of new adventures are intoxicating. Yet, beneath the shiny exterior lies a financial commitment that many drivers don’t fully understand: their car loan. While you know your monthly payment, do you truly grasp how that money is distributed between principal and interest over the loan’s lifetime?

This is where the Car Loan Amortization Chart becomes your most powerful tool. Far more than just a table of numbers, it’s a financial roadmap that reveals the true cost of your auto loan and empowers you to make smarter decisions. As an expert in personal finance and auto lending, I’ve seen countless individuals benefit from this critical insight. Understanding this chart can save you thousands of dollars and shave months off your loan term.

The Ultimate Roadmap to Financial Freedom: Decoding Your Car Loan Amortization Chart

In this comprehensive guide, we will dive deep into what a car loan amortization chart is, how it works, why it’s indispensable for every car owner, and how you can leverage it for significant financial advantage. Prepare to transform your approach to car ownership and take control of your financial future.

What Exactly is a Car Loan Amortization Chart?

At its core, a car loan amortization chart (often called an amortization schedule) is a detailed breakdown of every single payment you’ll make on your auto loan. It illustrates how each payment is split between reducing the principal balance and covering the interest charged. Think of it as a transparent ledger for your debt.

Most people only focus on the total monthly payment. However, this chart reveals the underlying mechanics. It shows you exactly how much of your hard-earned money goes towards paying down the actual debt (principal) and how much goes to the lender as a fee for borrowing (interest).

This isn’t just a theoretical concept; it’s a practical document that sheds light on your financial commitment. It transforms a single, seemingly opaque monthly payment into a clear, predictable sequence of events, empowering you with knowledge.

The Core Mechanics: How Car Loan Amortization Works

Understanding how amortization functions is key to unlocking its power. The process of amortization involves gradually paying off a debt over time through a series of regular, equal payments. While the payment amount remains constant (for fixed-rate loans), the composition of that payment changes significantly over the life of the loan.

Initial Payments: Interest-Heavy

In the early stages of your car loan, a disproportionately large portion of your monthly payment goes towards interest. This is because your outstanding principal balance is at its highest. Lenders calculate interest based on the remaining principal amount. Therefore, with a larger principal, more interest accrues.

Later Payments: Principal-Heavy

As you continue to make payments, your principal balance slowly decreases. With a smaller principal, less interest is charged each month. Consequently, a larger percentage of your fixed monthly payment can then be applied to the principal. This accelerates the rate at which you pay down the actual debt, snowballing your progress towards ownership.

This shift is crucial. It’s why making even small extra payments early in the loan term can have a dramatic impact. Based on my experience, many car owners are surprised to learn how little principal they pay off in the first year of a five or six-year loan. This insight alone is often enough to motivate them to pay down their loan faster.

Decoding Your Car Loan Amortization Chart: A Line-by-Line Guide

A typical car loan amortization chart will feature several key columns, each providing a vital piece of information. Let’s break them down:

- Payment Number: This column simply indicates which payment you are making in the sequence (e.g., 1 of 60, 2 of 60, etc.). It helps you track your progress.

- Payment Date: This column specifies the exact date each payment is due. It’s essential for budgeting and ensuring timely payments.

- Beginning Balance (or Starting Principal): This is the outstanding amount of your loan before the current payment is applied. It represents how much you still owe the lender.

- Scheduled Payment: This is the fixed amount you are required to pay each month. For a fixed-rate loan, this figure remains constant throughout the loan term.

- Interest Paid: This column shows the exact dollar amount of your monthly payment that goes towards interest. As discussed, this amount is higher at the beginning of the loan and decreases over time.

- Principal Paid: This column reveals how much of your monthly payment is directly applied to reducing your outstanding loan balance. This amount starts small and gradually increases with each payment.

- Ending Balance (or Remaining Principal): This is the amount of your loan remaining after the current payment has been applied. It’s your new outstanding balance, ready for the next month’s calculation.

Pro Tip from Us: Don’t just glance at the "Scheduled Payment" column. Take the time to examine the "Interest Paid" and "Principal Paid" columns for the first 12-24 months. You’ll likely be surprised by the interest-heavy nature of those initial payments. This visual cue often motivates people to make extra principal payments if they can.

Why Every Car Buyer Needs This Chart: The Value Proposition

The car loan amortization chart is more than just a document; it’s a powerful financial planning tool. Its value extends far beyond simply knowing your monthly payment.

- Unmatched Budgeting and Financial Planning: The chart provides a clear, month-by-month forecast of your financial obligations. You can see exactly how much cash flow is committed to your car loan at any given point. This helps you plan for other expenses, savings, and investments with greater accuracy. Knowing your exact principal reduction schedule is a huge advantage for future financial decisions.

- Revealing the True Cost of Interest: Many car buyers focus solely on the vehicle’s price and monthly payment. The amortization chart starkly reveals the total amount of interest you will pay over the loan’s lifetime. Seeing this figure laid out can be a powerful motivator to pay off your loan faster or negotiate a better interest rate upfront.

- Strategically Accelerating Debt Repayment: This is where the chart truly shines. By understanding the principal and interest breakdown, you can strategically apply extra payments directly to the principal. The chart allows you to visualize how even a small additional payment can dramatically reduce the total interest paid and shorten your loan term. We’ll delve deeper into this strategy soon.

- Empowered Negotiation During Car Purchase: Before you even step into the dealership, creating a few amortization charts with different loan terms and interest rates gives you immense power. You can clearly see how a slight difference in interest rate or an extra year on the loan term impacts your total cost. This knowledge enables you to negotiate more effectively and avoid being pressured into unfavorable terms.

- Verifying Lender Calculations: Mistakes can happen. Having your own amortization chart allows you to cross-reference your lender’s statements. You can ensure that your payments are being applied correctly and that the interest calculations align with your loan agreement. This provides an important layer of financial security and trust.

Common mistakes to avoid are signing loan documents without reviewing them thoroughly and not understanding the total cost of borrowing. The amortization chart provides the clarity needed to avoid these pitfalls.

Creating Your Own Car Loan Amortization Chart

You don’t need to be a financial wizard to create your own amortization chart. Several accessible tools can help you generate this invaluable document.

- Online Amortization Calculators: This is by far the easiest and most popular method. Many reputable financial websites and lender sites offer free, user-friendly calculators. You simply input your loan amount, interest rate, and loan term, and the calculator instantly generates a detailed schedule.

- Pro Tip: Look for calculators that allow you to input extra payments to see their impact. This feature is incredibly useful for planning debt acceleration.

- Spreadsheet Software (Excel, Google Sheets): For those comfortable with spreadsheets, creating your own chart offers maximum flexibility. You can use built-in functions like

PMT(Payment) to calculate your monthly payment and then manually create the columns for beginning balance, interest, principal, and ending balance for each payment period.- Basic Formula Logic:

- Interest Paid = Beginning Balance * (Annual Interest Rate / 12)

- Principal Paid = Scheduled Payment – Interest Paid

- Ending Balance = Beginning Balance – Principal Paid

- This method allows for custom scenarios and detailed analysis, especially if you want to model various extra payment strategies.

- Basic Formula Logic:

- Manual Calculation (for the mathematically inclined): While less practical for generating a full chart, understanding the underlying formula for a fixed-payment loan can be enlightening:

M = P /

Where:- M = Monthly Payment

- P = Principal Loan Amount

- i = Monthly Interest Rate (Annual Rate / 12)

- n = Total Number of Payments (Loan Term in Years * 12)

This formula gives you the fixed monthly payment. From there, you can iteratively calculate interest and principal for each month.

Based on my experience, starting with an online calculator is the best approach for most people. It’s quick, accurate, and provides a clear visual representation without the need for complex calculations.

Strategic Insights: Using Your Chart for Smart Financial Decisions

The true power of the car loan amortization chart lies in its ability to inform strategic financial decisions. It’s not just a passive report; it’s an active tool for debt management.

- Making Extra Payments: The Interest-Saving Superpower: Your amortization chart clearly shows how much interest you pay each month. By making even small extra payments and instructing your lender to apply them directly to the principal, you bypass a significant amount of future interest. The chart allows you to see how each extra dollar reduces your ending balance, leading to less interest calculated on the next payment. This can shave months or even years off your loan term and save you hundreds, if not thousands, of dollars.

- Example: If your chart shows you pay $150 in interest and $250 in principal on an early payment, an extra $50 on principal means you’ve effectively paid $300 towards the actual debt that month.

- Refinancing Considerations: Is It Worth It? If interest rates drop or your credit score improves, refinancing your car loan might be a good option. Use your current amortization chart to compare it against a new chart generated with the proposed refinance terms. This side-by-side comparison will show you the exact impact on your monthly payment, total interest paid, and the new loan term. It helps you determine if the savings outweigh any potential fees associated with refinancing.

- Pro Tip: Don’t just look at the monthly payment reduction. Focus on the total interest savings over the remaining life of the loan.

- Shortening Your Loan Term: While a longer loan term means lower monthly payments, it almost always results in paying significantly more interest over time. Your amortization chart will vividly illustrate this. By opting for a shorter loan term (if affordable), you accelerate the principal repayment process and dramatically reduce the total interest burden. The chart allows you to compare different term lengths and see the financial implications clearly.

- Understanding Balloon Payments or Residual Values: Some car loans, particularly leases or certain financing arrangements, involve a large "balloon payment" at the end of the term. The amortization chart for these loans will look different, showing a substantial remaining balance at the end. Understanding this distinction from the outset prevents unwelcome surprises and helps you plan for that final large payment or decide whether to return/purchase the vehicle.

Common pitfalls include making extra payments without specifying they should go to principal (lenders might apply it to the next month’s payment instead) and not revisiting your chart after life changes like a pay raise, which could enable you to accelerate payments.

Beyond the Chart: Other Factors Influencing Your Car Loan

While the car loan amortization chart is a powerful tool, it’s important to remember that several factors influence the numbers you see on that chart. Understanding these can help you secure better terms initially and manage your loan effectively.

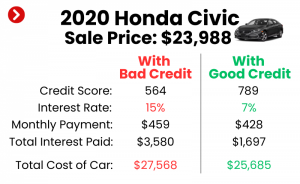

- Your Credit Score: This is perhaps the most significant factor. A higher credit score signals lower risk to lenders, resulting in lower interest rates. Even a difference of 1-2% in your interest rate can translate into hundreds or thousands of dollars saved on total interest over the life of your loan, as clearly shown on your amortization chart.

- Down Payment: Making a larger down payment reduces the total amount you need to borrow. A smaller principal loan amount means less interest will accrue over the loan term, leading to lower monthly payments and significant overall savings. This positive impact will be immediately visible on your amortization schedule.

- Trade-in Value: Similar to a down payment, a good trade-in value for your old car effectively reduces the principal of your new car loan. The less you borrow, the less interest you pay, improving your amortization outlook.

- Loan Term (Length of the Loan): As mentioned, a shorter loan term (e.g., 36 or 48 months) generally means higher monthly payments but substantially less total interest paid. A longer term (e.g., 72 or 84 months) offers lower monthly payments but significantly increases the total interest. Your chart will lay out these trade-offs clearly.

- Fees and Charges: Be aware of any origination fees, documentation fees, or other charges that might be rolled into your loan. These increase your principal loan amount, meaning you’ll pay interest on these fees as well. Always scrutinize the full loan disclosure before signing.

Understanding these variables before applying for an auto loan empowers you to secure the most favorable terms possible. A well-informed decision at the outset will make your amortization journey much smoother and more affordable. For more in-depth guidance on improving your credit score before buying a car, you might want to explore articles like .

Conclusion: Take Control of Your Car Loan Journey

The car loan amortization chart is more than just a financial document; it’s a declaration of financial empowerment. It transforms a complex financial obligation into a transparent, manageable journey. By understanding how your payments are distributed between principal and interest, you gain the knowledge to make informed decisions, accelerate your debt repayment, and ultimately achieve financial freedom faster.

Don’t let your car loan be a mystery. Arm yourself with this powerful tool, create your own amortization chart, and actively use it to manage your debt. Whether you’re planning to buy your first car, looking to refinance, or simply want to understand your current auto loan better, this chart is your indispensable guide. Take control, understand your numbers, and drive towards a smarter financial future. For further reading on smart auto financing, consider resources from reputable organizations like the Consumer Financial Protection Bureau (CFPB) which offers excellent guides on understanding auto loans. .