Trapped in Your Car Loan? A Comprehensive Guide to "Buy Me Out Of My Car Loan"

Trapped in Your Car Loan? A Comprehensive Guide to "Buy Me Out Of My Car Loan" Carloan.Guidemechanic.com

Many car owners eventually find themselves in a challenging position: they want to get rid of their current vehicle, but they still owe money on the loan. The phrase "Buy me out of my car loan" perfectly encapsulates this desire, often indicating a struggle with payments, a need for a different vehicle, or simply being "upside down" – owing more than the car is worth.

If you’re feeling stuck, you’re not alone. This is a common scenario, and thankfully, there are viable strategies to navigate it. This comprehensive guide will delve deep into understanding your situation, exploring your options, and empowering you with the knowledge to make the best financial decision. Our ultimate goal is to provide real value, helping you escape a burdensome car loan with minimal financial impact.

Trapped in Your Car Loan? A Comprehensive Guide to "Buy Me Out Of My Car Loan"

Understanding Your "Upside Down" Car Loan Situation

Before exploring solutions, it’s crucial to understand precisely what "Buy me out of my car loan" often implies. For many, it means they are experiencing negative equity, also known as being "upside down" on their car loan. This happens when the outstanding balance of your loan is higher than the current market value of your vehicle.

Imagine you bought a car for $30,000, and after two years, you still owe $25,000, but the car is only worth $20,000. That $5,000 difference is your negative equity. This situation can feel like being financially trapped, making it difficult to sell or trade in your car without incurring a significant loss.

Why Do People End Up Upside Down?

Several factors contribute to negative equity, and understanding them can help prevent future occurrences. The primary culprit is often rapid depreciation, especially during the initial years of ownership. New cars can lose 20-30% of their value in the first year alone.

Longer loan terms, such as 72 or 84 months, also play a role. While they offer lower monthly payments, they extend the period over which you pay interest, and your car’s value depreciates faster than you pay down the principal. Additionally, rolling negative equity from a previous car into a new loan is a common trap that perpetuates the cycle.

Determining Your Car’s True Value and Loan Payoff

The first step in any strategy is to gather accurate information. You need to know exactly how much you owe and how much your car is currently worth. This will reveal the extent of your negative equity, if any.

Start by contacting your lender to request a payoff quote. This isn’t just your current balance; it’s the exact amount required to fully satisfy the loan on a specific date, often including any per diem interest. Make sure to get this in writing, as it’s a critical figure for any transaction.

Next, research your car’s market value. Utilize reputable online resources like Kelley Blue Book (KBB.com), Edmunds, and NADAguides. These sites allow you to input your car’s make, model, year, mileage, and condition to get estimated trade-in and private party sale values. Be honest about your car’s condition for the most accurate appraisal.

Strategies to Get Out of Your Car Loan

Once you understand your financial position, you can explore the various avenues available to you. Each option comes with its own set of advantages and disadvantages, and the best choice will depend on your specific circumstances, including your financial health and the amount of negative equity you’re facing.

1. Selling Your Car Privately

Selling your car to a private buyer often yields the highest selling price compared to a dealership trade-in. This is because dealerships need to buy low to resell at a profit, whereas a private buyer is typically looking for a fair market price. If you have significant negative equity, a private sale might be your best bet to minimize your out-of-pocket expenses.

Pros:

- Potentially higher selling price.

- More control over the sale process and negotiation.

- Ability to recoup more of your car’s value.

Cons:

- Requires more time and effort (marketing, showing the car, handling paperwork).

- Dealing with potential buyers can be frustrating.

- Managing the loan payoff and title transfer can be complex with negative equity.

Based on my experience: Private sales, while demanding, consistently offer the best return, especially for cars in good condition. You’re essentially cutting out the middleman and keeping their profit margin for yourself. However, it requires patience and a proactive approach to marketing and negotiation.

How to Handle a Private Sale with a Loan:

The process is slightly more involved when you have an outstanding loan. You cannot simply hand over the title, as your lender holds it.

- Get a Payoff Quote: Obtain a precise payoff amount from your lender.

- Find a Buyer: Market your car effectively. Use online marketplaces, social media, and local classifieds. Be transparent about the car’s condition and history.

- Negotiate the Price: Aim for a price that covers your loan payoff and ideally leaves you with some cash or at least minimizes your negative equity.

- Managing the Negative Equity: If your selling price is less than your payoff amount, you’ll need to cover the difference out of pocket. This is crucial. For example, if you sell for $18,000 but owe $20,000, you’ll need to pay the lender $2,000 to release the title.

- Facilitate the Transaction: Once you have a buyer and agreed-upon price, arrange to meet at your bank or a neutral location. The buyer typically pays you, and you then immediately pay off your loan. Your lender will then send the title to you, which you can then sign over to the buyer. Some lenders can work directly with the buyer’s bank for a smoother transfer.

Pro tips from us: Always insist on secure payment methods like a cashier’s check or bank transfer. Never accept personal checks or large amounts of cash unless you can verify them instantly. Draw up a bill of sale that details the transaction, protecting both parties.

2. Trading In Your Car at a Dealership

Trading in your car at a dealership is the most convenient option, as they handle all the paperwork and the loan payoff. This is often the path people take when they want to "buy me out of my car loan" and immediately get into a new vehicle. However, convenience often comes at a cost.

Pros:

- Extremely convenient; one-stop shop for selling and buying.

- Dealership handles loan payoff and title transfer.

- Potential tax savings in some states (you only pay sales tax on the difference between the new car’s price and your trade-in value).

Cons:

- Generally lower offer price than a private sale.

- Negative equity can be rolled into your new loan, increasing your overall debt.

- Less control over the negotiation process.

Common mistakes to avoid are: Focusing solely on the monthly payment of the new car without understanding how your trade-in’s negative equity is affecting the total loan amount. Dealerships are masters at "payment packing," making a bad deal look good by spreading it over a longer term.

How Negative Equity is Rolled Over:

If you owe $20,000 on your old car and the dealership offers $18,000 for it, you have $2,000 in negative equity. If you then buy a new car for $25,000, the dealership will add that $2,000 to your new car loan, making your new loan amount $27,000 (plus taxes and fees). This increases your new monthly payments and the total interest paid over the life of the loan.

Strategies for a Better Trade-In:

- Know Your Car’s Value: Go in armed with KBB and Edmunds estimates.

- Separate Negotiations: Try to negotiate the trade-in value and the new car purchase price as separate transactions. Don’t let them combine them initially.

- Shop Around: Get trade-in offers from multiple dealerships.

- Pay Down the Difference: If you have some savings, paying off the negative equity upfront is always the smartest move to avoid rolling it into your new loan.

3. Refinancing Your Car Loan

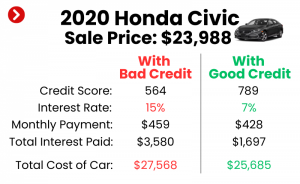

Refinancing means taking out a new loan to pay off your existing car loan, often with different terms. This strategy is less about "getting out" entirely and more about making your current loan more manageable or reducing its cost. It’s particularly effective if your credit score has improved since you first took out the loan, or if interest rates have dropped.

Pros:

- Potentially lower interest rate, saving you money over time.

- Lower monthly payments if you extend the loan term (though this increases total interest).

- Ability to shorten the loan term to pay it off faster (if your payments increase but are affordable).

Cons:

- Not always possible with significant negative equity. Lenders are hesitant to finance more than a car is worth.

- Extending the loan term increases the total interest paid.

- May not significantly reduce payments if your current rate is already low.

When it’s a good option: If you have positive equity or only slight negative equity, a good credit score, and current interest rates are favorable. If you’ve made a lot of extra payments, your loan-to-value ratio might be good enough for a refinance.

When it’s not a good option: If you have substantial negative equity (e.g., you owe 130% or more of your car’s value), most lenders won’t approve a refinance. It also won’t help if your primary goal is to completely get rid of the car.

Steps to Refinancing:

- Check Your Credit Score: A higher score will get you better rates.

- Shop Around: Compare offers from multiple banks, credit unions, and online lenders. Don’t just stick with your current lender.

- Review Loan Terms: Pay close attention to the interest rate, loan term, and any fees.

- Submit Application: Provide necessary documents like pay stubs, loan statements, and vehicle information.

4. Paying Off the Difference Out of Pocket

If you have some savings, this is often the most financially sound approach when you’re upside down. By paying the difference between your car’s value and your loan balance, you can eliminate the negative equity. This then allows you to sell the car outright, trade it in without rolling over debt, or simply own it free and clear.

Pros:

- Eliminates negative equity immediately.

- Gives you more flexibility in selling or trading.

- Reduces overall debt and financial burden.

Cons:

- Requires available cash.

- May deplete emergency savings if not carefully considered.

Pro tips from us: Even if you can’t pay the entire difference, paying down a portion can significantly improve your loan-to-value ratio, making refinancing or a trade-in more viable. Every dollar you put towards the principal reduces future interest payments.

5. Voluntary Repossession / Surrender (Avoid at All Costs)

This is a last resort and should be avoided whenever possible due to severe long-term consequences. Voluntary repossession means you return the car to the lender because you can no longer afford the payments. While it might seem like an easy way out, it’s far from it.

Consequences:

- Credit Score Devastation: A repossession will severely damage your credit score, making it difficult to get loans, credit cards, or even rent an apartment for years.

- Deficiency Balance: The lender will sell the car at auction, usually for much less than its market value. You will still be responsible for paying the "deficiency balance" – the difference between what you owed and what the car sold for, plus repossession and auction fees. This can be thousands of dollars.

- Collection Efforts: Lenders will pursue you for the deficiency balance, potentially leading to wage garnishment or lawsuits.

Based on my experience: There are almost always better options than voluntary repossession. Explore every other strategy, including negotiating with your lender for forbearance or a modified payment plan, before considering this destructive path.

Addressing Negative Equity Head-On

Negative equity is the core problem for many who want to "buy me out of my car loan." Actively working to reduce it can provide significant financial relief and open up more options.

What is it, and Why Does it Matter?

As discussed, negative equity is owing more than your car is worth. It matters because it traps you. You can’t sell the car without paying money out of pocket, and rolling it into a new loan simply digs you deeper into debt. It’s a significant barrier to financial flexibility.

Strategies to Reduce Negative Equity

- Make Extra Payments Towards Principal: Even an extra $50 or $100 a month specifically directed towards your loan’s principal can accelerate payoff and reduce the amount of interest you pay over time. Confirm with your lender that extra payments go directly to principal, not just towards future interest.

- Lump-Sum Payments: If you receive a bonus, tax refund, or any unexpected windfall, consider using a portion of it to make a significant dent in your loan balance. This is one of the fastest ways to build equity.

- Temporary Side Hustle: Consider taking on a temporary side job or selling unused items around your house to generate extra income solely for paying down your car loan.

- Cut Expenses: Review your budget and identify areas where you can temporarily cut back on discretionary spending. Every dollar saved can be redirected to your car loan.

Preparing for the Process: Essential Steps

Regardless of which strategy you choose, thorough preparation is key to a smooth and successful outcome.

- Gather All Documents: Have your loan statements, original loan agreement, vehicle title (if you have it, though usually the lender holds it), and maintenance records ready.

- Get a Fresh Payoff Quote: As mentioned, this is critical. Payoff quotes are time-sensitive, so get one that’s current for when you plan to complete the transaction.

- Research Car Value: Use multiple sources (KBB, Edmunds, NADA) to get a realistic range for both private sale and trade-in values.

- Understand Your Credit Score: Your credit score will influence refinancing options and potentially new car loan terms. Access your credit report for free annually from AnnualCreditReport.com.

- Set a Realistic Budget: If you’re planning to buy another car, know exactly what you can afford for monthly payments, insurance, and maintenance.

Financial Considerations & Long-Term Planning

Getting out of a car loan, especially when upside down, is an opportunity to re-evaluate your financial habits and plan for a more secure future.

- Budgeting and Debt Management: Create a detailed budget to understand your income and expenses. Prioritize debt repayment and avoid accumulating new unnecessary debt.

- Building an Emergency Fund: A robust emergency fund (3-6 months of living expenses) is crucial. It provides a buffer against unexpected financial setbacks, preventing you from falling behind on payments again.

- Avoiding Future Negative Equity:

- Make a Significant Down Payment: Aim for at least 20% to immediately build equity.

- Choose a Shorter Loan Term: A 36 or 48-month loan ensures you build equity faster than depreciation occurs.

- Buy Used: Used cars have already taken their biggest depreciation hit, offering better value retention.

- Don’t Roll Over Debt: Never agree to roll negative equity from an old car into a new loan. Pay it off first.

Common mistakes to avoid are: Buying more car than you need or can truly afford. The allure of a fancy new vehicle can often lead to financial strain down the road. Stick to your budget and needs.

When to Seek Professional Help

Sometimes, the financial situation is too complex or overwhelming to handle alone. Don’t hesitate to seek professional guidance.

- Financial Advisors: A certified financial planner can help you assess your overall financial picture, create a budget, and develop a long-term strategy for debt management and wealth building.

- Credit Counseling Agencies: Non-profit credit counseling agencies offer free or low-cost advice on budgeting, debt management plans, and negotiating with creditors. Look for agencies accredited by the National Foundation for Credit Counseling (NFCC).

- Your Lender: If you’re struggling to make payments, proactively contact your lender. They may be willing to offer temporary forbearance, a modified payment plan, or other solutions to avoid default and repossession. Open communication is always better than ignoring the problem.

For more information on managing debt and financial wellness, you can consult trusted external resources like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov. They offer unbiased information and tools to help consumers make informed financial decisions.

Conclusion: Taking Control of Your Car Loan Situation

The feeling of being trapped by a car loan, especially when you’re upside down, can be incredibly stressful. However, as an Expert Blogger and Professional SEO Content Writer, I want to assure you that you have options. The phrase "Buy me out of my car loan" is not a cry for help without solutions; it’s a starting point for proactive financial management.

By understanding your current standing, exploring strategies like private sales, dealership trade-ins, refinancing, or making extra payments, and committing to long-term financial planning, you can regain control. Remember, knowledge is power. Arm yourself with information, be patient, and make choices that align with your financial goals. You can get out from under that burdensome car loan and drive towards a more secure financial future.