Unlock Financial Freedom: Your Ultimate Guide to Refinance Your Car Loan Online

Unlock Financial Freedom: Your Ultimate Guide to Refinance Your Car Loan Online Carloan.Guidemechanic.com

Are you feeling the pinch of high monthly car payments? Perhaps your financial situation has improved, or interest rates have taken a dip since you first bought your vehicle. If so, you’re not alone. Many car owners are discovering the significant benefits of refinancing their car loan, and doing it online has made the process more accessible and convenient than ever before.

In today’s fast-paced digital world, the ability to refinance my car loan online is a game-changer. It empowers you to take control of your finances from the comfort of your home, potentially saving you thousands of dollars over the life of your loan. This comprehensive guide will walk you through every step, shedding light on the "why," "when," and "how" of online auto loan refinancing, ensuring you have all the knowledge to make an informed decision and achieve greater financial flexibility.

Unlock Financial Freedom: Your Ultimate Guide to Refinance Your Car Loan Online

Why Should You Even Consider Refinancing Your Car Loan? The Compelling Benefits

Refinancing a car loan isn’t just about getting a new loan; it’s about optimizing your financial landscape. Based on my experience in the financial industry, the reasons people choose to refinance are often deeply rooted in a desire for better financial health. Let’s explore the primary benefits:

Lower Interest Rates and Reduced Monthly Payments

This is often the most appealing benefit. If interest rates have dropped since you financed your car, or if your credit score has significantly improved, you’re likely eligible for a much better Annual Percentage Rate (APR). A lower APR directly translates to less interest paid over time and, crucially, a reduced monthly payment. This can free up significant cash flow in your budget.

For instance, imagine saving $50 or even $100 per month. Over a year, that’s $600 to $1200 back in your pocket, which can be used for savings, other debt reduction, or simply improving your quality of life. This immediate relief is a powerful motivator for many seeking to refinance my car loan online.

Decrease the Total Cost of Your Loan

While a lower monthly payment is great, the long-term savings are equally important. A lower interest rate means you’ll pay less interest overall throughout the life of the loan. Even if your monthly payment doesn’t drastically change, reducing the total amount you pay back to the lender is a smart financial move.

This benefit is especially pronounced for those who secured their initial loan with a higher interest rate due to a less-than-perfect credit score at the time. As your financial standing improves, refinancing allows you to correct past financial challenges.

Adjust Your Loan Term for Better Fit

Refinancing offers flexibility regarding the loan term. You have two main options, each with distinct advantages:

- Shorter Loan Term: If you’re looking to pay off your car faster and can afford a slightly higher monthly payment, a shorter term will reduce the total interest paid. This strategy accelerates your path to debt freedom and gets you out from under car payments sooner.

- Longer Loan Term: Conversely, if your budget is tight and you need more breathing room, extending the loan term can significantly lower your monthly payments. While this means you’ll pay more interest over the life of the loan, it can provide immediate financial relief and prevent you from missing payments, which could harm your credit score.

The ability to tailor your loan term to your current financial goals is a key advantage of pursuing an online auto loan refinance.

Remove a Co-signer from Your Loan

Sometimes, when you initially purchase a car, you might need a co-signer to qualify for better rates or even get approved. If your credit score has since improved, refinancing allows you to remove that co-signer from the obligation. This provides financial freedom for both you and your co-signer, as their credit will no longer be tied to your vehicle.

This is a common scenario, and many individuals use refinancing as a strategic step to take full ownership of their financial responsibilities.

Improve Your Overall Financial Flexibility

Ultimately, refinancing provides greater control over your finances. Whether it’s freeing up cash flow, reducing total debt, or simply aligning your car loan with your current budget, it offers a pathway to better financial health. This added flexibility can be invaluable, allowing you to reallocate funds to savings, investments, or other essential expenses.

When Is the Absolute Right Time to Refinance Your Car Loan? Key Triggers and Considerations

Deciding when to refinance my car loan online is as crucial as understanding why. Certain circumstances make refinancing particularly advantageous. Recognizing these triggers can save you a substantial amount of money.

Interest Rates Have Dropped

The broader economic environment plays a significant role. If general interest rates have declined since you took out your original loan, there’s a good chance you can secure a lower rate through refinancing. Keep an eye on market trends and compare them to your existing APR.

Even a percentage point or two can lead to significant savings over several years, making it well worth the effort of an online car loan refinance.

Your Credit Score Has Significantly Improved

This is one of the most common and powerful reasons to refinance. If you’ve been diligently paying bills on time, reducing other debts, and your credit score has jumped from "fair" to "good" or "good" to "excellent," lenders will view you as a much lower risk. This improved creditworthiness translates directly into eligibility for lower interest rates.

Pro tip from us: Regularly check your credit score and report. If you see a substantial improvement, it’s an excellent indicator that it’s time to explore refinancing options.

You’ve Paid Down a Good Portion of Your Original Loan

As you make payments, the principal balance of your loan decreases, and your equity in the car increases. This makes you a more attractive borrower to new lenders. They see less risk involved when the loan amount is smaller and the car’s value is closer to or exceeds the outstanding balance.

However, be mindful of being "upside down" on your loan, where you owe more than the car is worth. Refinancing in this situation can be challenging, though not impossible.

Your Financial Situation Has Changed for the Better

Perhaps you’ve received a promotion, landed a higher-paying job, or eliminated other significant debts. An improved financial standing means you might now comfortably afford a shorter loan term, allowing you to pay off the vehicle faster and save on interest.

Conversely, if your financial situation has tightened, refinancing for a longer term and lower monthly payment can provide much-needed breathing room.

Your Original Loan Terms Were Unfavorable

Sometimes, you might have taken out your initial car loan under less-than-ideal circumstances – perhaps you needed a car quickly, had limited options, or didn’t fully understand the terms. If you’re stuck with a high APR, a long term you regret, or predatory fees, refinancing offers a chance to rectify these past decisions.

Common mistakes to avoid are: Rushing into the first loan offer without understanding all the terms. Refinancing gives you a second chance to get it right.

You Want to Remove a Co-signer

As mentioned, if a co-signer helped you secure your initial loan, and your financial standing has improved, refinancing allows you to release them from the obligation. This is a considerate and responsible move that benefits both parties.

When NOT to Refinance (Prepayment Penalties & Upside-Down Loans)

Before you jump into an online auto loan refinance, check your current loan agreement for any prepayment penalties. Some lenders charge a fee if you pay off your loan early. Also, if you are significantly "upside down" on your loan (you owe far more than the car is worth), it might be difficult to find a lender willing to refinance, or the terms might not be favorable enough to make it worthwhile. In such cases, focusing on increasing your equity first might be a better strategy.

The "Online" Advantage: Why Refinance Your Car Loan Digitally?

The internet has revolutionized how we manage our finances, and auto loan refinancing is no exception. The "online" aspect of refinance my car loan online offers distinct advantages that traditional methods simply can’t match.

Unparalleled Convenience and Speed

Forget about making appointments, driving to banks, or waiting in long lines. Online refinancing allows you to complete the entire process from anywhere, at any time. You can research lenders, compare offers, and submit applications from your couch, during your lunch break, or even late at night.

The digital nature of the process often means faster approvals and quicker funding, getting you to your new, lower payment sooner.

Access to a Wider Range of Lenders and Competitive Offers

Traditional banks are just one piece of the puzzle. Online refinancing opens the door to a vast marketplace of lenders, including credit unions, online-only lenders, and financial technology companies. This increased competition works in your favor, as lenders are eager to offer competitive rates and terms to attract your business.

This broader access significantly increases your chances of finding the absolute best deal tailored to your financial situation.

Enhanced Transparency and Easy Comparison

Online platforms are designed for comparison. They often present loan offers side-by-side, making it easy to compare APRs, loan terms, monthly payments, and fees. Many websites even offer calculators to help you visualize potential savings.

This level of transparency empowers you to make a truly informed decision, rather than relying on a single offer from one institution.

Streamlined Application Process and Digital Documentation

Online applications are typically intuitive and user-friendly. You can upload necessary documents digitally, eliminating the need for printing, scanning, or faxing. This not only saves time but also reduces the chances of errors and speeds up the verification process.

From initial pre-qualification to final signing, the entire journey is designed to be as smooth and paperless as possible.

Key Factors Lenders Consider for Your Online Auto Loan Refinance

When you apply to refinance my car loan online, lenders will evaluate several aspects of your financial profile and the vehicle itself. Understanding these factors will help you prepare and increase your chances of approval for the best possible terms.

Your Credit Score: The Ultimate Indicator

Your credit score is arguably the most critical factor. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt.

- Excellent Credit (720+): You’ll qualify for the lowest interest rates and most favorable terms.

- Good Credit (660-719): Still eligible for competitive rates, though perhaps not the absolute lowest.

- Fair Credit (600-659): Refinancing is possible, but rates will be higher. Focus on improving your score for future opportunities.

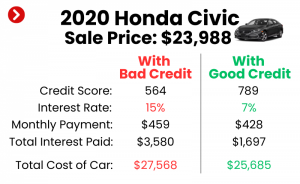

- Bad Credit (Below 600): Refinancing with bad credit is challenging but not impossible. You’ll likely face very high interest rates. In such cases, securing a co-signer or focusing on credit repair might be beneficial before applying.

Lenders use your credit score to gauge the risk of lending to you. A higher score means lower risk, which translates to a lower interest rate for you.

Debt-to-Income (DTI) Ratio

Your DTI ratio is the percentage of your gross monthly income that goes towards paying your monthly debt payments. Lenders want to ensure you have enough disposable income to comfortably afford your new car payment. A lower DTI ratio indicates less financial strain and a greater ability to manage additional debt.

Typically, lenders prefer a DTI ratio below 43%, but this can vary. A high DTI might signal to lenders that you are overextended, even with a good credit score.

Loan-to-Value (LTV) Ratio of Your Vehicle

The LTV ratio compares the amount you owe on your car loan to the car’s current market value. Lenders generally prefer an LTV of 100% or less, meaning you don’t owe more than the car is worth. If your LTV is too high (e.g., 120% or more, indicating you are "upside down"), it poses a higher risk for the lender, as the car itself isn’t sufficient collateral for the loan amount.

You can determine your car’s value using resources like Kelley Blue Book (KBB) or Edmunds. This is a crucial step before seeking an online auto loan refinance.

Vehicle Age and Mileage

Lenders typically prefer to refinance newer vehicles with lower mileage. Older cars with high mileage depreciate faster and are considered higher risk because their resale value is lower, and mechanical issues are more likely. Many lenders have limits, such as not refinancing vehicles older than 8-10 years or with more than 100,000-120,000 miles.

This is because the car acts as collateral for the loan, and its value directly impacts the lender’s risk assessment.

Current Loan Balance

Lenders often have minimum and maximum loan balance requirements for refinancing. If your outstanding loan balance is too small (e.g., under $5,000), some lenders might not find it worthwhile to process the refinance. Conversely, if it’s very high, it might require a stronger credit profile.

Employment Stability and Income Verification

Lenders want to see a stable employment history and a consistent income source. This assures them that you have the financial means to make your monthly payments reliably. You’ll typically need to provide proof of income, such as pay stubs, tax returns, or bank statements.

The Step-by-Step Guide to Refinance Your Car Loan Online

Ready to dive in? Refinancing your car loan online is a straightforward process when you know the steps. Follow this guide to navigate your online auto loan refinance successfully.

Step 1: Gather All Necessary Documents and Information

Preparation is key. Having everything organized beforehand will streamline your application process. You’ll generally need:

- Your Current Loan Information: Account number, lender name, current payoff amount, original loan date, and current interest rate.

- Vehicle Information: Make, model, year, Vehicle Identification Number (VIN), mileage, and current registration.

- Personal Identification: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (1-2 months), tax returns (if self-employed), or bank statements.

- Proof of Residence: Utility bill or lease agreement.

- Insurance Information: Current auto insurance policy details.

Having these documents ready will save you time and prevent delays.

Step 2: Check Your Credit Score and Review Your Credit Report

Before applying, get a clear picture of your credit health. You can get a free copy of your credit report from each of the three major bureaus (Experian, EquiFax, TransUnion) once a year at AnnualCreditReport.com. Review it for any errors or inaccuracies that could negatively impact your score.

Understanding your credit score helps you gauge what kind of rates you might qualify for and identify areas for improvement. This knowledge empowers you when you compare offers.

Step 3: Research and Compare Online Lenders

This is where the "online" advantage truly shines. Don’t settle for the first offer you find. Explore various lenders, including:

- Traditional Banks: Many large banks offer online refinancing.

- Credit Unions: Often known for competitive rates and personalized service (may require membership).

- Online-Only Lenders: Companies specializing in digital lending often have streamlined processes and competitive offers.

Look for lenders that specialize in auto loan refinancing and have positive customer reviews.

Step 4: Get Pre-qualified (Soft Credit Check)

Most online lenders offer a pre-qualification process. This involves a "soft credit inquiry," which doesn’t impact your credit score. You’ll provide some basic information, and the lender will give you an estimated interest rate and terms you might qualify for.

Pro tips from us: Get pre-qualified with several lenders. This allows you to compare actual offers without harming your credit score and helps you identify the most competitive options.

Step 5: Compare Offers and Choose the Best One

Once you have a few pre-qualification offers, carefully compare them. Don’t just look at the monthly payment; consider the entire picture:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and some fees. Aim for the lowest APR.

- Loan Term: Does it fit your financial goals (shorter for faster payoff, longer for lower payments)?

- Fees: Are there any origination fees, application fees, or prepayment penalties?

- Total Cost of Loan: Calculate the total amount you’d pay over the life of each loan.

Choose the offer that best aligns with your financial objectives and provides the most significant savings.

Step 6: Complete the Full Application (Hard Credit Check)

Once you’ve selected a lender, you’ll proceed with the full application. This step typically involves a "hard credit inquiry," which will temporarily (and usually minimally) impact your credit score. This is a normal part of the process.

You’ll submit all the documents you gathered in Step 1. The lender will verify your information and make a final decision.

Step 7: Finalize and Sign the New Loan Documents

If approved, the lender will send you the final loan documents. Read every single word carefully. Understand the APR, the loan term, the monthly payment, and any clauses or conditions. Don’t hesitate to ask your lender questions if anything is unclear.

Once you’re satisfied, sign the documents electronically or physically, as instructed.

Step 8: Your New Lender Pays Off Your Old Loan

After you’ve signed, your new lender will pay off your existing car loan. You’ll then begin making payments to your new lender under the new, more favorable terms. Confirm with your previous lender that the old loan has been closed and your account balance is zero.

It’s a seamless transition designed to ensure you don’t have to manage two payments during the changeover.

Common Mistakes to Avoid When Refinancing Your Car Loan

While refinancing can be highly beneficial, there are pitfalls to avoid. Being aware of these common mistakes can save you from costly errors and ensure your online auto loan refinance is truly advantageous.

Not Shopping Around for Multiple Offers

One of the biggest mistakes is accepting the first offer you receive without comparing it to others. As an Expert Blogger and Professional SEO Content Writer, I’ve seen too many people miss out on substantial savings by not leveraging the competitive online lending market. Always get at least 3-5 pre-qualification offers.

Extending the Loan Term Unnecessarily

While a longer term means lower monthly payments, it almost always means paying more interest over the life of the loan. Only extend the term if absolutely necessary for budget relief. If your goal is to save money, a shorter term is usually better, provided you can afford the payments.

Focusing Only on the Monthly Payment, Not the Total Cost

It’s easy to get fixated on the lower monthly payment. However, always calculate the total cost of the loan (principal + total interest paid) over the entire term. A slightly higher monthly payment over a shorter term can often result in significant overall savings.

Ignoring Fees and Hidden Charges

Some lenders might charge origination fees, application fees, or other administrative costs. While these are often rolled into the loan, they still add to the total cost. Always ask about all associated fees and factor them into your comparison.

Refinancing When You’re Significantly Upside Down on Your Loan

If you owe much more than your car is worth (high LTV), refinancing might not be possible or beneficial. Lenders are reluctant to take on this risk, and any offers you receive might still have high interest rates. In such cases, it might be better to pay down the principal first.

Not Checking Your Credit Report Beforehand

Errors on your credit report can unjustly lower your score, leading to higher interest rates. Always review your credit report for accuracy before applying. Disputes can take time, so do this well in advance.

Pro Tips for a Successful Online Car Loan Refinance

To maximize your chances of securing the best terms and having a smooth experience, consider these expert tips. Based on my experience, these insights can make a significant difference in your refinancing journey.

Know Your Current Loan Details Inside and Out

Before you even start, have a crystal-clear understanding of your current loan’s APR, remaining balance, payoff amount, and any prepayment penalties. This information is your baseline for comparison and will be requested by new lenders.

Understand the Impact of Different Loan Terms

Play with online refinance calculators. See how changing the loan term affects both your monthly payment and the total interest paid. This visual understanding will help you choose the term that best fits your short-term budget needs and long-term financial goals.

Consider a Co-signer If Your Credit Is Weak

If your credit score isn’t ideal, adding a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. Ensure both parties understand the responsibilities involved.

Read the Fine Print Carefully

This cannot be stressed enough. Loan documents are legally binding. Don’t skim through them. Understand every clause, especially concerning fees, payment schedules, and what happens if you miss a payment.

Don’t Be Afraid to Ask Questions

If anything in the application process or loan documents is unclear, contact the lender’s customer service. A reputable lender will be happy to clarify any points. It’s your money and your loan – ensure you’re fully informed.

Automate Your Payments

Once your new loan is set up, consider automating your monthly payments. This ensures you never miss a payment, which protects your credit score and helps you avoid late fees. Many lenders offer incentives for setting up autopay.

Refinancing with Less-Than-Perfect Credit: Is It Possible?

The short answer is yes, it is often possible to refinance my car loan online even with a less-than-perfect credit score. However, it comes with certain considerations and expectations.

You might not qualify for the absolute lowest interest rates, but if your credit has improved at all since your original loan, or if market rates have dropped, you could still secure a better deal. Lenders specializing in "subprime" auto loans exist, and online platforms make it easier to find them.

Focus on demonstrating stability in other areas: steady employment, a low debt-to-income ratio, and a vehicle with good equity. Consider taking steps to improve your credit score before applying, even small improvements can make a difference. If available, a co-signer with good credit can also significantly enhance your chances. Remember, even a small reduction in your interest rate can save you money over time.

Conclusion: Take Control of Your Car Loan Today

Refinancing your car loan online is a powerful financial tool that can provide significant relief and flexibility. From securing a lower interest rate and reducing your monthly payments to adjusting your loan term or removing a co-signer, the benefits are clear and tangible. The convenience, speed, and competitive nature of online lending make it an ideal choice for today’s savvy consumer.

By understanding the factors lenders consider, following our step-by-step guide, and avoiding common pitfalls, you are well-equipped to navigate the process successfully. Don’t let high interest rates or unfavorable loan terms hold you back. Take the initiative, leverage the power of online auto loan refinance, and unlock greater financial freedom. Your journey to a more manageable car payment starts now.