Unlock Financial Freedom: Your Ultimate Guide to the Car Loan Early Payment Calculator

Unlock Financial Freedom: Your Ultimate Guide to the Car Loan Early Payment Calculator Carloan.Guidemechanic.com

Imagine a world where you’re debt-free sooner, paying significantly less for your car than you originally agreed, and freeing up monthly cash flow for other financial goals. This isn’t a pipe dream; it’s a tangible reality for those who strategically tackle their car loans. One of the most powerful tools in this journey is the Car Loan Early Payment Calculator.

This comprehensive guide will demystify the process, showing you exactly how this calculator works, why it’s a game-changer, and how to leverage it for maximum financial benefit. Whether you’re just starting your car loan journey or looking to accelerate your payoff, understanding and utilizing an early payment calculator is your first crucial step towards financial liberation.

Unlock Financial Freedom: Your Ultimate Guide to the Car Loan Early Payment Calculator

What Exactly is a Car Loan Early Payment Calculator?

At its core, a car loan early payment calculator is a sophisticated online tool designed to reveal the impact of making extra payments on your automotive loan. It goes beyond a simple balance check, providing a clear projection of how additional contributions can shorten your loan term and drastically reduce the total interest you pay over the life of the loan.

Think of it as your personal financial crystal ball for your car loan. By inputting a few key pieces of information, the calculator performs complex amortization calculations instantly. It then presents you with a side-by-side comparison of your original loan schedule versus a revised schedule with your proposed extra payments.

Why Should You Even Consider Early Car Loan Payments?

The idea of paying off debt sooner often comes with a natural appeal, but with car loans, the benefits are particularly compelling. Based on my experience, many people underestimate the true cost of interest over a typical 5-7 year car loan term. An early payment strategy directly addresses this.

The primary motivation is saving money. Every extra dollar you pay towards your principal balance directly reduces the amount of interest the lender can charge you. Over time, these savings can accumulate into hundreds, or even thousands, of dollars.

Beyond financial savings, there’s the invaluable benefit of achieving debt freedom faster. Imagine the peace of mind that comes from knowing your car is truly yours, without the burden of monthly payments. This freed-up cash flow can then be redirected towards other financial priorities, such as building an emergency fund, investing, or tackling higher-interest debts like credit cards.

How Does a Car Loan Early Payment Calculator Work? A Deep Dive

Understanding the mechanics of the calculator is crucial for interpreting its results effectively. It operates by taking your current loan details and then simulating different payment scenarios. Let’s break down the essential inputs and outputs.

Key Inputs You’ll Need

To get accurate results from any car loan early payment calculator, you’ll need to gather specific information about your existing loan. Don’t worry, all of this can typically be found on your original loan agreement or your most recent loan statement.

- Original Loan Amount: This is the initial principal you borrowed when you financed your vehicle. It’s the starting point for all calculations.

- Original Interest Rate (APR): The annual percentage rate is the cost of borrowing money, expressed as a percentage. This rate significantly influences how much interest you’ll pay over the loan’s life.

- Original Loan Term: This refers to the number of months or years you initially agreed to pay back the loan. Common terms are 36, 48, 60, or 72 months.

- Current Outstanding Balance: This is the remaining principal balance on your loan today. It’s vital because the calculator needs to know where you currently stand in your repayment journey.

- Desired Extra Payment Amount: This is where you experiment. You’ll input how much extra you plan to pay each month, or how often you plan to make additional payments (e.g., bi-weekly).

- Date of Next Payment: Some advanced calculators might ask for this to accurately project future payments, especially if you’re making a lump sum.

Understanding the Outputs

Once you’ve plugged in your numbers, the early car loan payoff calculator will quickly process them and present you with powerful insights. These outputs are the core value of the tool.

- New Payoff Date: This is arguably the most exciting output. It shows you exactly how much sooner you can become debt-free by implementing your extra payment strategy.

- Total Interest Saved: This figure quantifies the financial benefit. It’s the difference between the total interest you would have paid on your original schedule and the reduced interest under your new payment plan.

- New Total Cost of the Loan: This shows the overall amount you’ll pay for your vehicle, including principal and interest, with your accelerated payments. It will be lower than the original total cost.

- Comparison to Original Schedule: Many calculators will display a side-by-side comparison, highlighting the difference in payoff date and total interest paid. This visual comparison makes the benefits crystal clear.

A Step-by-Step Guide to Using Your Car Loan Early Payment Calculator

Using this powerful tool is straightforward once you have your information ready. Follow these steps to unlock its potential.

- Gather Your Loan Details: As mentioned, collect your original loan amount, interest rate, term, and current outstanding balance. Having these readily available will make the process quick and accurate.

- Find a Reliable Calculator: Many financial websites, banks, and credit unions offer free car loan early payment calculators. Ensure the one you choose is reputable and easy to use.

- Input Your Data: Carefully enter each piece of information into the corresponding fields. Double-check your entries to avoid errors that could skew the results.

- Experiment with Extra Payments: This is the fun part! Start by adding a small extra amount, say $25 or $50, to your monthly payment. See the impact. Then try a larger amount.

- Interpret the Results: Look closely at the new payoff date and the total interest saved. These numbers provide the clearest picture of your potential benefits.

- Adjust and Re-calculate: Don’t stop at one calculation. Try different scenarios:

- What if you make a one-time lump sum payment?

- What if you switch to bi-weekly payments instead of monthly?

- How does even a small, consistent extra payment add up over time?

By playing with different scenarios, you can find a strategy that fits your budget and accelerates your path to debt freedom.

Beyond the Calculator: Effective Strategies for Early Payoff

While the car loan early payment calculator helps you visualize the benefits, implementing an effective strategy is where the real magic happens. Based on my experience helping clients achieve their financial goals, these methods are highly effective.

Making Extra Principal Payments

This is the most direct and impactful strategy. Every dollar you pay above your minimum monthly payment should be directed specifically towards the principal balance. This immediately reduces the amount on which interest is calculated, leading to faster payoff and greater savings.

Pro tip from us: Always confirm with your lender that extra payments are applied directly to the principal and not just advanced to the next month’s payment. Some lenders require specific instructions.

The Bi-Weekly Payment Approach

Instead of making one monthly payment, you split your regular monthly payment in half and pay that amount every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments, which equates to 13 full monthly payments annually instead of 12. This subtle shift effectively adds one extra full payment per year without feeling like a huge financial strain.

Strategic Refinancing

Refinancing your car loan means taking out a new loan to pay off your existing one, ideally with a lower interest rate or a shorter term. If your credit score has improved since you first took out the loan, or if interest rates have dropped, refinancing can significantly reduce your total interest cost and accelerate your payoff.

However, be cautious. Ensure that the new loan doesn’t come with excessive fees that negate the interest savings. For a deeper dive into managing your overall debt, check out our guide on .

Lump Sum Payments

Did you receive a tax refund, a work bonus, or an unexpected inheritance? A portion or all of this money can be strategically used to make a significant lump sum payment on your car loan. Even a few hundred dollars can shave months off your loan term and save substantial interest.

Round-Up Payments

This is a simpler, less aggressive strategy but still effective. If your monthly payment is $347, round it up to $350 or $375. These small, consistent extra amounts accumulate over time and contribute to early principal reduction. It’s often so minor that you won’t feel the pinch in your budget.

The Financial Benefits of Early Payoff: A Deeper Look

Beyond the immediate satisfaction, paying off your car loan early offers several profound financial advantages that contribute to your overall financial well-being.

Quantifying Interest Savings

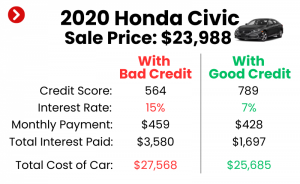

This is the most tangible benefit. A car loan early payment calculator clearly shows you the exact dollar amount you’ll save. For instance, on a $25,000 loan at 6% over 60 months, paying just an extra $50 a month could save you hundreds of dollars in interest and shave several months off your loan term. These savings are real money that stays in your pocket.

Impact on Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is a key metric lenders use to assess your ability to manage monthly payments and repay debts. By eliminating your car loan, you significantly reduce your monthly debt obligations, thereby improving your DTI. A lower DTI can make it easier to qualify for other loans (like a mortgage) in the future, often with more favorable terms.

Boosting Your Credit Score

While paying off a loan early doesn’t directly boost your score in the same way making on-time payments does, it contributes positively. Reducing your overall debt load improves your credit utilization ratio (how much credit you’re using versus how much is available). This, coupled with a history of responsible payments, helps build a strong credit profile, making you a more attractive borrower.

Psychological Benefits: Freedom and Peace of Mind

This benefit, though not quantifiable, is incredibly valuable. The feeling of owning your vehicle outright, without the looming burden of monthly payments, brings immense peace of mind. This psychological freedom can reduce stress and empower you to pursue other financial goals with greater confidence.

Common Mistakes to Avoid When Paying Off Your Car Loan Early

While accelerating your car loan payoff is generally a smart move, there are pitfalls to avoid. Common mistakes can negate your efforts or even put you in a worse financial position.

- Ignoring Prepayment Penalties: Some loan agreements, though less common with car loans than mortgages, include prepayment penalties. These are fees charged by the lender if you pay off your loan ahead of schedule. Always review your loan documents or contact your lender to confirm if such penalties apply.

- Depleting Your Emergency Fund: Prioritizing early debt payoff over a robust emergency fund is a common mistake. Your emergency fund should always be your top financial priority. It acts as a safety net for unexpected expenses like job loss or medical emergencies. Without it, you might be forced back into debt.

- Prioritizing Car Loan Over Higher-Interest Debt: If you have credit card debt or personal loans with significantly higher interest rates than your car loan, it almost always makes more financial sense to tackle those first. The interest savings on high-interest debt will be much greater.

- Not Verifying How Extra Payments Are Applied: As mentioned earlier, always confirm that your extra payments are being applied directly to the principal balance. Some lenders might automatically advance your due date if you don’t specify. This won’t accelerate your payoff or save you interest.

Is Early Payoff Always the Best Option? Important Considerations

While the benefits are clear, paying off your car loan early isn’t a one-size-fits-all solution. There are specific situations where it might not be the optimal financial move for you.

- Prepayment Penalties: If your loan agreement includes a significant prepayment penalty, the cost of paying off early might outweigh the interest savings. Always check your loan terms first.

- Opportunity Cost: Consider what else you could do with that extra money. If you have opportunities to invest that money and earn a return significantly higher than your car loan’s interest rate, then investing might be a better choice. This is especially true for those with low-interest car loans.

- Other Higher-Interest Debts: As noted, if you’re carrying balances on credit cards or other high-interest loans, channeling your extra funds towards those debts first will typically yield greater financial benefits due to the higher interest rates.

- Emergency Fund Adequacy: Before dedicating extra funds to your car loan, ensure you have a fully funded emergency savings account (typically 3-6 months of living expenses). This provides crucial financial security against unexpected life events.

If you’re considering refinancing as an option, our article on offers valuable insights.

Pro Tips for Maximizing Your Early Payoff Strategy

To truly make the most of your car loan early payment calculator and accelerate your debt-free journey, implement these professional tips.

- Automate Extra Payments: Set up an automatic transfer from your checking account to your loan account for the extra amount you plan to pay. Automation ensures consistency and removes the temptation to skip a payment.

- Review Your Budget Regularly: Periodically review your budget to identify areas where you can cut back or find additional funds to put towards your car loan. Even small, consistent sacrifices can make a big difference over time.

- Monitor Your Loan Statements: Regularly check your loan statements to ensure your extra payments are being applied correctly to the principal balance. This vigilance prevents potential issues and keeps you on track.

- Consider Your Financial Goals Holistically: Don’t view your car loan in isolation. Integrate your early payoff strategy into your broader financial plan, considering how it aligns with your emergency fund, retirement savings, and other debt reduction efforts. A balanced approach is key to long-term financial success.

- Use the Calculator as a Motivator: Revisit the car loan early payment calculator periodically. Seeing the revised payoff date and interest savings can be incredibly motivating, encouraging you to stick to your plan or even find ways to accelerate it further.

For general financial literacy resources and budgeting tools, you might find the Consumer Financial Protection Bureau (CFPB) website helpful, offering unbiased advice to consumers.

Conclusion: Your Road to a Debt-Free Car

The Car Loan Early Payment Calculator is more than just a tool; it’s a powerful ally in your quest for financial freedom. It transforms complex financial projections into clear, actionable insights, showing you precisely how to save money and become debt-free faster. By understanding its mechanics, strategically implementing extra payments, and avoiding common pitfalls, you can take control of your car loan and unlock significant financial benefits.

Don’t let interest payments erode your hard-earned money any longer. Take the first step today: gather your loan details, use a reliable early payment calculator, and visualize your debt-free future. The road to owning your car outright, with thousands saved in interest, is within your reach. Start planning your early payoff strategy now and experience the liberating power of smart financial decisions.