Unlock Financial Peace: Your Ultimate Guide to Mastering the Car Loan Payment Calendar

Unlock Financial Peace: Your Ultimate Guide to Mastering the Car Loan Payment Calendar Carloan.Guidemechanic.com

Buying a car is an exciting milestone, often one of the biggest purchases many of us make after a home. While the thrill of a new set of wheels is undeniable, the reality of managing those monthly car loan payments can quickly dampen the excitement if not handled proactively. This is precisely where a robust Car Loan Payment Calendar becomes your most valuable financial tool.

Think of it as your personalized roadmap to debt freedom. It’s more than just knowing your due date; it’s about understanding every facet of your loan, taking control, and ultimately saving money. In this comprehensive guide, we’ll dive deep into why creating and diligently following a car loan payment calendar isn’t just good practice—it’s essential for your financial well-being.

Unlock Financial Peace: Your Ultimate Guide to Mastering the Car Loan Payment Calendar

What Exactly Is a Car Loan Payment Calendar?

At its core, a car loan payment calendar is a detailed schedule that outlines every single payment you need to make on your auto loan, from the first installment to the very last. It’s a proactive financial planning instrument designed to give you a crystal-clear overview of your debt obligations. This isn’t just a simple reminder; it’s a strategic document.

This calendar goes beyond a basic due date notification. It breaks down your loan into manageable segments, showing you not only when to pay but also how each payment contributes to reducing your overall debt. Understanding these nuances is crucial for effective debt management.

Components of an Effective Calendar:

A truly comprehensive payment calendar will include several critical pieces of information. It’s about more than just logging a number.

- Original Loan Amount: This is the principal amount you borrowed to purchase your vehicle. Knowing this baseline helps you track your progress.

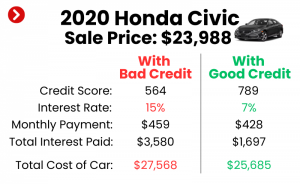

- Interest Rate: Your Annual Percentage Rate (APR) directly impacts how much extra you’ll pay over the life of the loan. A higher rate means more interest.

- Loan Term: This refers to the duration of your loan, typically measured in months (e.g., 36, 48, 60, 72 months). A longer term often means lower monthly payments but more interest paid overall.

- Monthly Payment Amount: The fixed sum you are contractually obligated to pay each month. This is the cornerstone of your budget planning.

- Due Dates: The specific day of the month your payment is expected. Missing this can lead to penalties and credit score damage.

- Principal vs. Interest Breakdown: This is a crucial, often overlooked, component. Early in your loan, a larger portion of your payment goes towards interest. As time progresses, more goes towards reducing the principal balance.

By tracking these elements, you gain a powerful perspective on your financial commitments. It transforms an abstract debt into a concrete, manageable plan.

Why You Absolutely Need a Car Loan Payment Calendar

You might think your lender’s online portal or monthly statement is enough, but based on my experience, relying solely on those can lead to missed opportunities and unnecessary stress. A personalized car loan payment calendar empowers you in ways a generic statement cannot. It’s a proactive approach to financial health.

Having a dedicated calendar for your car loan offers a multitude of benefits, extending far beyond simple payment reminders. It’s a cornerstone of responsible financial management.

1. Master Your Budget and Avoid Surprises:

A car loan payment is a significant fixed expense in most households. Integrating it into your overall budget is non-negotiable for financial stability. Your payment calendar clearly marks when money will leave your account, allowing you to plan other expenditures around it.

This proactive approach eliminates the dreaded "oops, I forgot about that payment" moment. You’ll know exactly how much discretionary income you have available after all your fixed obligations are met, leading to better financial decisions.

2. Say Goodbye to Late Fees and Penalties:

One of the most immediate and tangible benefits of a payment calendar is preventing late fees. These fees are not only an unnecessary drain on your finances but can also snowball into more significant problems if payments are consistently missed. They are a direct hit to your wallet.

Pro tips from us: Even a single late payment can trigger a fee, and multiple late payments can lead to more severe consequences like repossession. Your calendar acts as a critical safeguard against these costly oversights.

3. Protect and Improve Your Credit Score:

Your payment history is the single most important factor influencing your credit score. Consistent, on-time payments demonstrate financial responsibility to credit bureaus. This positive behavior directly contributes to a healthy credit profile.

Conversely, late payments can severely damage your credit score, making it harder and more expensive to secure future loans, mortgages, or even rent an apartment. Your calendar helps ensure a pristine payment record.

4. Understand Your Loan’s Amortization and Progress:

Many people pay their car loan for years without truly understanding how it works. An amortization schedule, which your calendar helps visualize, shows how each payment is split between principal and interest. Early payments primarily cover interest, while later payments reduce the principal more significantly.

Seeing this breakdown helps you understand the true cost of your loan and motivates you to potentially accelerate your payments. It demystifies the loan process, giving you clarity.

5. Peace of Mind and Reduced Financial Stress:

Financial anxiety is a common issue, and debt obligations often contribute significantly to it. Knowing exactly when and how much you need to pay, coupled with a clear understanding of your progress, can dramatically reduce stress levels. This knowledge empowers you.

Having a visual representation of your loan’s trajectory provides a sense of control and accomplishment as you tick off each payment. It turns a daunting obligation into a manageable journey.

6. Strategically Plan Extra Payments to Save Money:

When you have a surplus of funds, your payment calendar becomes a powerful tool for strategic debt reduction. By clearly seeing your principal balance, you can identify opportunities to make extra payments. Even small additional contributions can make a substantial difference.

These extra payments, when applied directly to the principal, reduce the overall interest you pay and shorten your loan term. Your calendar helps you visualize this impact and plan for it effectively.

Creating Your Own Car Loan Payment Calendar: A Step-by-Step Guide

Building your personalized car loan payment calendar isn’t complicated, but it requires a bit of attention to detail upfront. The effort you put in now will pay dividends throughout the life of your loan. It’s about setting yourself up for success.

Step 1: Gather All Your Loan Documents

Before you start, collect all the paperwork related to your car loan. This includes your loan agreement, disclosure statements, and any communication from your lender. These documents contain all the vital information you’ll need.

Look for key details such as the original loan amount, the annual percentage rate (APR), the loan term in months, your monthly payment amount, and the exact due date. Accuracy is paramount here.

Step 2: Identify Key Information for Each Payment

Once you have your documents, extract the core data points for your calendar. This foundational information will populate your schedule.

Ensure you have the precise due date, the exact monthly payment required, and the starting principal balance. If your lender provides an amortization schedule, that will be incredibly helpful for tracking principal and interest.

Step 3: Choose Your Preferred Calendar Tool

You have several options for creating your calendar, each with its own advantages. Select the one that best fits your comfort level and organizational style.

- Spreadsheet (Excel, Google Sheets): This is often the most flexible and powerful option. You can customize columns, use formulas to calculate remaining balances, and easily track principal/interest.

- Digital Calendar (Google Calendar, Outlook Calendar): Great for setting recurring reminders for your due dates. You can also add notes for each payment.

- Budgeting Apps (Mint, YNAB, Personal Capital): Many popular budgeting apps have features to track loans and often integrate with your bank accounts, providing automatic updates.

- Physical Wall Calendar/Planner: For those who prefer a tangible approach, a physical calendar works perfectly for visual tracking and manual entry.

Step 4: Plot All Your Payments

Begin by entering your loan’s starting date and your first payment due date. Then, systematically plot out every single payment for the entire loan term.

If your loan is 60 months, you will have 60 entries. Label each entry clearly with the date and the required payment amount.

Step 5: Track Principal and Interest (If Applicable)

This is where a spreadsheet shines. If you have an amortization schedule, input the principal and interest breakdown for each payment. If not, you can often find amortization calculators online to help estimate these figures.

Seeing how much interest you pay, especially in the early stages, can be a powerful motivator to pay down your principal faster. This transparency provides incredible insight.

Step 6: Set Up Reminders and Automate (Optional but Recommended)

Leverage technology to ensure you never miss a payment. Set up automated payment reminders in your chosen digital calendar or budgeting app.

Consider setting up automatic payments through your lender’s portal or your bank. This eliminates the risk of human error, but always ensure you have sufficient funds in your account before the due date.

Step 7: Regularly Review and Adjust

Your payment calendar isn’t a static document; it’s a living tool. Regularly review your progress, especially after making any extra payments.

Adjust your remaining balance and future payment breakdown accordingly. This keeps your calendar accurate and reinforces your commitment to your financial goals.

Key Elements to Track on Your Calendar

To truly maximize the effectiveness of your car loan payment calendar, you need to track more than just the due date. Each piece of information offers a unique insight into your loan’s progression. This detailed tracking empowers you.

- Payment Due Date: The most obvious, but critical, element. Mark it clearly to ensure timely payments.

- Payment Amount Due: The exact amount your lender expects for that specific month. Double-check this against your statement.

- Actual Payment Made: Record the exact amount you paid, especially if it was more than the minimum. This reflects your true effort.

- Date Paid: Note the day your payment was processed. This helps resolve any discrepancies with your lender.

- Remaining Principal Balance: After each payment, update this figure. Watching the principal shrink is incredibly motivating.

- Amount Paid Towards Principal: How much of your payment went directly to reducing the loan’s core amount.

- Amount Paid Towards Interest: How much of your payment went to the cost of borrowing money.

- Notes/Comments: Use this section for anything unusual. Did you make an extra payment? Was there a late fee? Did you change your payment method? This provides a historical record.

Common mistakes to avoid are neglecting to track the principal and interest breakdown. This information is key to understanding the true cost of your loan and strategizing early repayment.

Maximizing Your Car Loan Payment Calendar for Financial Freedom

A car loan payment calendar isn’t just a tracking tool; it’s a launchpad for strategic debt reduction. By using it wisely, you can significantly reduce the total interest paid and shorten the life of your loan. This proactive approach can save you thousands.

1. Making Strategic Extra Payments:

Based on my experience, even small, consistent extra payments can have a dramatic impact. When you have a little extra cash—from a bonus, tax refund, or simply cutting back on discretionary spending—apply it directly to your principal. Your calendar helps you see the current principal balance, making it easy to calculate the impact.

Always instruct your lender to apply extra payments directly to the principal, not just "pre-pay" future installments. This distinction is crucial for interest savings.

2. Exploring Bi-Weekly Payments:

Instead of making one monthly payment, consider splitting your monthly payment in half and paying it every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments, which equates to 13 full monthly payments annually instead of 12.

This "extra" payment each year goes a long way in reducing your principal faster and saving on interest. Your calendar can easily be adapted to track these bi-weekly installments.

3. Understanding Amortization in Action:

Your calendar, especially if it tracks principal and interest, visually demonstrates the amortization process. You’ll see how more of your early payments go to interest, and as the principal shrinks, more goes to the principal. This insight empowers you to make informed decisions.

This understanding can motivate you to pay extra, knowing that every dollar directed to principal early on has a magnified effect on your overall interest savings.

4. Considering Refinancing Opportunities:

Keep an eye on interest rates and your credit score. If rates drop significantly or your credit score improves, you might qualify for a lower interest rate by refinancing your car loan. This is a powerful way to reduce your total cost.

Your payment calendar will be invaluable for comparing your current loan’s remaining payments and total cost against a potential new, lower-interest loan. For a deeper dive into improving your credit score, check out our guide on .

Common Mistakes to Avoid When Managing Your Car Loan Payments

Even with a well-structured calendar, certain pitfalls can derail your progress. Being aware of these common mistakes can help you navigate your car loan journey more smoothly and cost-effectively. Prevention is always better than cure.

- Ignoring Due Dates: This is the most obvious, yet surprisingly common, mistake. A missed payment can trigger late fees, negatively impact your credit score, and even lead to default. Your calendar is your primary defense.

- Not Checking Statements Regularly: Even if you have a calendar, always cross-reference it with your lender’s monthly statement. Errors can occur, and it’s your responsibility to catch them.

- Paying Only the Minimum for the Entire Term: While meeting the minimum is essential, it’s not optimal. Paying only the minimum ensures you pay the maximum amount of interest over the life of the loan.

- Forgetting About Related Car Expenses: Your car loan payment is just one piece of the puzzle. Remember to budget for insurance, fuel, maintenance, and potential repairs. These often overlooked costs can strain your budget if not planned for.

- Not Understanding Your Interest Rate: Many borrowers don’t fully grasp how their interest rate impacts the total cost of their loan. A higher rate means more money out of your pocket. Your calendar helps visualize this.

- Failing to Update Your Calendar After Changes: If you refinance, make a large lump-sum payment, or have any other loan modification, update your calendar immediately. An outdated calendar is a misleading one.

If you’re exploring options to lower your monthly payments, our article on might be helpful.

Tools and Resources to Help You

You don’t have to manage your car loan payment calendar entirely manually. There’s a wealth of tools and resources available to make the process easier and more efficient. Leveraging technology can simplify your financial life.

- Spreadsheet Software: Excel and Google Sheets are incredibly versatile. You can download free templates for loan amortization or create your own custom spreadsheet to track every detail.

- Budgeting Apps: Apps like Mint, YNAB (You Need A Budget), and Personal Capital can link to your bank accounts and loan providers. They offer automated tracking, budgeting features, and often send payment reminders.

- Lender Portals: Most car loan lenders provide online portals where you can view your payment history, upcoming due dates, and sometimes even your amortization schedule. Use this as your primary source of truth.

- Amortization Calculators: Many financial websites offer free online amortization calculators. Simply input your loan amount, interest rate, and term, and it will generate a detailed payment schedule for you.

- Digital Calendar Reminders: Simple yet effective. Use Google Calendar, Outlook Calendar, or your phone’s native calendar app to set recurring reminders a few days before your payment is due.

For more official guidance on consumer financial products, you can visit the Consumer Financial Protection Bureau’s website.

The Long-Term Impact: Beyond Just Payments

Managing your car loan with a dedicated payment calendar has ripple effects that extend far beyond simply making sure a payment goes out on time. It’s about cultivating robust financial habits that serve you well into the future. This discipline builds lasting financial health.

Enhanced Creditworthiness: A consistent history of on-time payments, meticulously tracked and ensured by your calendar, is a powerful builder of excellent credit. This translates into lower interest rates on future loans, better insurance premiums, and more financial opportunities.

Accelerated Debt Freedom: By understanding your loan’s mechanics and strategically making extra payments, you can pay off your car loan much faster than the original term. This frees up significant cash flow in your monthly budget, which can then be directed towards other financial goals, like saving for a down payment or retirement.

Reduced Financial Stress and Greater Peace of Mind: There’s an immense sense of calm that comes from being in control of your finances. Knowing exactly where you stand with your car loan, and actively working towards its completion, eliminates uncertainty and fosters a sense of accomplishment. This financial peace is invaluable.

Foundation for Future Financial Planning: The discipline and organizational skills you develop by managing your car loan calendar are transferable. These habits lay a strong foundation for managing other debts, investments, and overall financial planning. It’s a stepping stone to a more secure financial future.

Conclusion: Your Roadmap to Car Loan Success

A Car Loan Payment Calendar is not just a fancy organizational tool; it’s a critical component of smart financial management. It empowers you to move beyond simply reacting to monthly statements and instead proactively manage your debt. From avoiding costly late fees and protecting your credit score to strategically accelerating your debt payoff, the benefits are clear and substantial.

By investing a little time upfront to create and consistently use your personalized payment calendar, you’re not just tracking a loan; you’re building a healthier financial future. Take control of your car loan today, and enjoy the journey to financial freedom with confidence and clarity. Your wallet, and your peace of mind, will thank you for it.