Unlock Lower Monthly Car Payments: Your Ultimate Car Loan Quizlet Self-Assessment

Unlock Lower Monthly Car Payments: Your Ultimate Car Loan Quizlet Self-Assessment Carloan.Guidemechanic.com

Are you feeling the squeeze of high monthly car payments? In today’s economic climate, every dollar counts, and optimizing your expenses is more crucial than ever. For many, a car loan represents one of the largest monthly outgoings after housing. But what if you could significantly reduce that burden? What if there was a structured way to assess your current situation and uncover actionable strategies to lower your payments?

That’s precisely what we’re going to explore with our "Car Loan Quizlet." Think of this not as a traditional quiz you take on an app, but rather a powerful, interactive self-assessment. It’s a series of critical questions designed to help you dissect your car loan, understand its mechanics, and identify the most effective levers you can pull to gain financial relief. This isn’t just about cutting costs; it’s about empowering you with knowledge and practical steps to take control of your finances.

Unlock Lower Monthly Car Payments: Your Ultimate Car Loan Quizlet Self-Assessment

We’ve designed this comprehensive guide to be your go-to resource, providing in-depth explanations, expert insights, and actionable advice. By the end of this journey, you’ll have a clear roadmap to potentially lower your monthly car payments, freeing up your budget for other important goals. Let’s dive in and start your self-assessment!

Quizlet Question 1: Do You Truly Understand Your Current Car Loan Terms?

Before you can make any effective changes, you must first understand the foundation of your current commitment. Many people sign loan documents without fully grasping the intricacies of their agreement. This lack of understanding can leave money on the table or lead to missed opportunities for savings.

The Nitty-Gritty of Your Loan Agreement

Your car loan agreement is more than just a piece of paper; it’s the rulebook for your debt. The first step in our "Car Loan Quizlet" is to pull out this document and scrutinize its core components. Don’t be intimidated by the legal jargon; we’ll break down what really matters. Understanding these elements is crucial for identifying areas where you might be able to negotiate or refinance for better terms.

- Interest Rate (APR): This is perhaps the most critical number on your loan. Your Annual Percentage Rate (APR) dictates how much extra you pay each year for borrowing the money. A difference of even one or two percentage points can translate into hundreds, or even thousands, of dollars over the life of the loan. A higher APR means more of your monthly payment goes towards interest, not the principal.

- Loan Term (Duration): This refers to the length of time, usually in months, over which you agree to repay the loan. Common terms range from 36 to 72 months, or even 84 months for new vehicles. While a longer term can result in lower monthly payments, it almost always means you’ll pay significantly more in total interest over the life of the loan. This is a common trade-off that many borrowers make without fully appreciating the long-term cost.

- Principal Amount: This is the original amount of money you borrowed to purchase the vehicle, minus any down payment or trade-in value. Every payment you make chipping away at this principal amount is a step closer to owning your car outright. A larger principal, naturally, means higher payments and more interest accrual.

- Prepayment Penalties/Clauses: Some loan agreements include clauses that penalize you for paying off your loan early. This is less common with standard auto loans but is still important to check. If your goal is to accelerate your payments or refinance, a prepayment penalty could negate some of your savings. Always confirm if your loan has such a clause before making plans to pay it off ahead of schedule.

Based on my experience, many borrowers are surprised when they truly calculate how much interest they’re paying, especially on longer loan terms. They often focus solely on the monthly payment amount during the purchasing process, overlooking the total cost of the loan. Taking the time now to understand these details will empower you to make informed decisions moving forward.

Quizlet Question 2: Have You Explored Car Loan Refinancing Options?

For many, refinancing is the most direct and effective path to lowering monthly car payments. It involves taking out a new loan to pay off your existing car loan, ideally with better terms. This strategy is particularly powerful if your financial situation or credit score has improved since you first took out the original loan.

When is Refinancing Your Best Bet?

Refinancing isn’t a one-size-fits-all solution, but it can be incredibly beneficial in several scenarios:

- Significantly Lower Interest Rates: If interest rates have dropped since you took out your original loan, or if your credit score has improved, you might qualify for a much lower APR. This is the most common and compelling reason to refinance. Even a 1-2% reduction can save you a substantial amount over the loan term.

- Improved Credit Score: When you initially bought your car, perhaps your credit score wasn’t stellar. If you’ve diligently paid your bills and improved your creditworthiness, lenders are likely to offer you more favorable terms now. This is a prime opportunity to capitalize on your good financial habits.

- Original Loan was a Bad Deal: Maybe you felt rushed at the dealership, or you weren’t fully prepared to negotiate. If you suspect you got a high interest rate or unfavorable terms, refinancing allows you a do-over.

- You Need a Lower Monthly Payment (with caution): Refinancing can extend your loan term, thereby reducing your monthly payment. While this offers immediate relief, remember that extending the term often means paying more in total interest over time. Weigh this trade-off carefully against your current financial needs.

The Refinancing Application Process

Applying for a refinance is similar to applying for your original car loan. You’ll typically need:

- Personal Information: Identification, proof of income, residence details.

- Vehicle Information: Make, model, year, VIN, mileage.

- Current Loan Information: Lender, account number, payoff amount.

- Credit Check: Lenders will pull your credit report to assess your risk.

Pro tips from us: Shop around! Don’t just go with the first offer you receive. Contact multiple banks, credit unions, and online lenders. Credit unions often have very competitive rates for car loans. Also, use online refinance calculators to estimate potential savings before you even apply.

Common Mistakes to Avoid are:

- Refinancing for too long: While extending your loan term lowers monthly payments, it increases the total interest paid. If you can afford it, aim for a similar or shorter term than what remains on your current loan.

- Ignoring fees: Some lenders charge application fees or closing costs for refinancing. Make sure these fees don’t outweigh your potential interest savings.

- Refinancing when "upside down": If you owe more on your car than it’s worth, many lenders will be hesitant to refinance, or they might require a substantial down payment to cover the negative equity.

Quizlet Question 3: Can You Consistently Make Extra Principal Payments?

This might seem counterintuitive if you’re trying to lower your monthly payments, but making extra payments directly against your loan’s principal can significantly reduce the total interest you pay and shorten the life of your loan. In the long run, this strategy saves you a substantial amount of money, which indirectly helps your overall financial health and ability to manage expenses.

Understanding the Power of Extra Principal Payments

Every time you make a payment, a portion goes to interest, and a portion goes to the principal. Because interest is calculated on the outstanding principal balance, reducing that principal faster means less interest accrues over time. Even small, consistent extra payments can have a dramatic effect.

- How it Works: When you send an extra payment, clearly specify to your lender that it should be applied directly to the principal. If you don’t, they might just hold it as an advance for your next payment, which doesn’t provide the same interest-saving benefit.

- Bi-weekly vs. Monthly Payments: A popular strategy is to switch from monthly to bi-weekly payments. If your monthly payment is $400, you’d pay $200 every two weeks. This results in 26 bi-weekly payments a year, equivalent to 13 monthly payments instead of 12. That "extra" payment each year goes directly to the principal, effectively shaving months, or even years, off your loan term and saving you a significant amount in interest.

- Small Amounts Add Up: Don’t underestimate the power of small, consistent contributions. Can you throw an extra $25 or $50 at your principal each month? What about applying any unexpected windfalls, like a work bonus or a tax refund, directly to your car loan? These seemingly minor actions compound over time.

Pro tips from us: Automate your extra payments. If you set up an automatic transfer for an additional amount each month, you’re less likely to miss it and more likely to stick to the plan. This consistency is key to seeing real results.

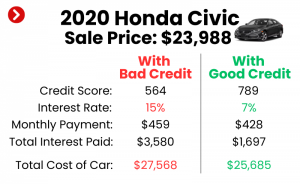

Quizlet Question 4: Is Your Credit Score in Top Shape?

Your credit score is your financial report card, and it plays an enormous role in determining the interest rate you qualify for on any loan, including a car loan refinance. If your score has improved since you initially financed your vehicle, you’re in a much stronger position to negotiate better terms or secure a lower rate through refinancing.

Why Your Credit Score is the Key to Better Rates

Lenders use your credit score to assess your risk. A higher score signals that you are a responsible borrower with a history of repaying debts, making you a less risky proposition. This translates directly into lower interest rates, which, as we’ve discussed, directly impacts your monthly payments and the total cost of your loan.

- How to Improve It:

- Payment History (35% of your score): This is the most crucial factor. Pay all your bills on time, every time. Even one late payment can significantly ding your score.

- Credit Utilization (30% of your score): This is the amount of credit you’re using compared to your total available credit. Keep your credit card balances low, ideally below 30% of your limit.

- Length of Credit History (15% of your score): The longer your accounts have been open and in good standing, the better.

- New Credit (10% of your score): Opening too many new credit accounts in a short period can lower your score.

- Credit Mix (10% of your score): Having a healthy mix of different types of credit (e.g., credit cards, installment loans) can be beneficial.

- Checking Your Score Regularly: You can get free copies of your credit report from AnnualCreditReport.com once a year from each of the three major bureaus (Experian, Equifax, TransUnion). Many credit card companies and banks also offer free credit score monitoring. Reviewing these regularly helps you spot errors and track your progress.

Based on my experience, many people don’t realize the tangible benefits of a few extra points on their credit score. Moving from a "good" score to an "excellent" score can mean saving thousands of dollars in interest on a car loan. It’s an investment in your financial future that pays dividends.

External Link: For a deeper dive into understanding and improving your credit score, you can visit a trusted resource like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov/consumer-tools/credit-reports-and-scores/.

Quizlet Question 5: Have You Considered Selling or Trading Down Your Vehicle?

While this is a more drastic measure, it’s a powerful one to consider if your current car loan payments are truly unsustainable or if you’re "upside down" on your loan (meaning you owe more than the car is worth). Sometimes, the best way to lower your car payments is to change the car itself.

When This Option Makes Sense

- Unsustainable Payments: If your car payment is eating up too much of your budget, especially if your financial situation has changed (job loss, new expenses), selling or trading down might be the most effective solution for immediate relief.

- "Upside Down" on Your Loan: If your car has depreciated significantly, and you owe more than its market value, you’re in a tough spot. Selling or trading it might still be an option, but you’ll need to cover the difference between the sale price and the loan balance.

- High Maintenance Costs: If your car is constantly in the shop, not only are you paying high monthly loan payments, but you’re also sinking money into repairs. A more reliable, less expensive vehicle could save you money on both fronts.

- Lifestyle Change: Perhaps you no longer need a large SUV and a smaller, more fuel-efficient car would better suit your needs and budget.

Pros and Cons

- Pros: Immediate and significant reduction in monthly payments, potential to eliminate negative equity, lower insurance costs, and reduced fuel and maintenance expenses.

- Cons: Can be a hassle to sell, might involve a loss if you’re upside down, and you’ll need to find a new, more affordable vehicle.

Common Mistakes to Avoid are:

- Not knowing your car’s true value: Research its market value using sites like Kelley Blue Book (KBB) or Edmunds before you talk to dealers or potential buyers.

- Ignoring negative equity: If you’re upside down, you’ll need a plan to cover the difference. Rolling negative equity into a new loan is a common mistake that perpetuates the problem and often leads to an even higher overall debt.

Quizlet Question 6: Are You Paying for Unnecessary Add-ons within Your Loan?

When you purchased your car, you were likely presented with a myriad of add-on products and services. While some can offer value, others might be inflating your loan amount and, consequently, your monthly payments, without providing proportionate benefit. It’s time to scrutinize these extras.

Scrutinizing Your Loan for Hidden Costs

Many dealerships include various products in the final loan amount, often bundled into the financing. These can significantly increase the total principal you borrow, leading to higher payments and more interest over the life of the loan.

- Extended Warranties: While some extended warranties can offer peace of mind, many are overpriced or offer coverage that overlaps with the manufacturer’s warranty. Check the terms carefully. Can you cancel it and get a prorated refund?

- GAP Insurance: Guaranteed Asset Protection (GAP) insurance covers the difference between what you owe on your car and its actual cash value if it’s totaled or stolen. This is often a good idea, especially for new cars or if you made a small down payment. However, it’s usually cheaper to buy GAP insurance from your own auto insurer or a credit union rather than the dealership. If you bought it from the dealer, can you cancel it and get a refund?

- Tire and Wheel Protection: Covers damage to tires and wheels.

- Paint and Fabric Protection: Often expensive and provides minimal real benefit.

- Loan Protection Plans: These are designed to cover your payments in case of job loss, disability, or death. While they sound reassuring, they can be very costly and often have restrictive terms.

Can You Cancel and Get a Refund?

For many of these add-ons, especially extended warranties and GAP insurance purchased through the dealership, you can often cancel them and receive a prorated refund. This refund will typically be applied directly to your loan principal, effectively lowering your outstanding balance and, in turn, reducing the total interest you’ll pay.

Pro tips from us: Review your original purchase agreement line by line. Identify any add-ons you purchased. Contact the dealership’s finance department or the warranty provider directly to inquire about cancellation policies and potential refunds. The money might not reduce your monthly payment directly unless you refinance, but it will reduce your total loan amount, which is a huge win.

Quizlet Question 7: Have You Negotiated with Your Current Lender?

Sometimes, the simplest approach is the most overlooked. Many people assume their car loan terms are set in stone once the papers are signed. However, it never hurts to open a dialogue with your current lender, especially if your financial situation has improved or if you’ve received better offers from other institutions.

When to Approach Your Lender

- Improved Credit Score: If your credit score has significantly improved since you took out the loan, you have a strong case for requesting a lower interest rate.

- Competitive Offers: If you’ve received pre-approval for a lower interest rate from another lender (through refinancing inquiries), you can use this as leverage. Your current lender might be willing to match or beat that offer to retain your business.

- Financial Hardship (with caution): If you’re genuinely struggling to make payments due to unforeseen circumstances, your lender might be willing to work with you on a temporary basis, such as payment deferral. However, be extremely cautious with deferrals, as interest usually continues to accrue, potentially increasing your total loan cost in the long run. Only consider this if absolutely necessary and understand all the implications.

What to Ask For

- Lower Interest Rate: This is your primary goal. Present your improved credit score or competing offers.

- Payment Deferral (use sparingly): As mentioned, understand that this usually means extending the loan and paying more interest. It’s a temporary fix, not a long-term solution to lower payments.

- Loan Modification: In rare cases, especially during widespread economic hardship, lenders might offer more significant loan modifications. These are less common for auto loans than for mortgages but are worth asking about if your situation is dire.

Based on my experience, lenders are more likely to work with proactive customers who have a good payment history. They would often prefer to retain you as a customer, even at a slightly lower rate, than to lose you to a competitor through refinancing. Be polite, professional, and well-prepared with your financial information and any competing offers.

Beyond the Quizlet: Sustaining Lower Payments and Smart Car Ownership

Successfully navigating our "Car Loan Quizlet" is a fantastic achievement, but the journey to optimal financial health doesn’t end there. To truly maintain lower payments and ensure smart car ownership in the long term, consider these additional strategies:

- Rigorous Budgeting and Financial Discipline: A lower car payment frees up funds, but where do those funds go? Implement a strict budget that allocates your freed-up cash towards other financial goals, such as building an emergency fund, paying down high-interest debt, or investing. This discipline prevents "lifestyle creep" where new savings are simply absorbed by new expenses.

- Build an Emergency Fund for Car Repairs: Even with lower monthly payments, unexpected car repairs can derail your budget. Having a dedicated emergency fund specifically for vehicle maintenance and unforeseen issues will prevent you from having to take on new debt or defer payments, which can undo all your hard work.

- Future Car Buying Strategies: Learn from your current experience. For your next vehicle, consider:

- Larger Down Payment: The more you put down, the less you borrow, leading to smaller payments and less interest.

- Shorter Loan Term: If you can afford it, opt for a shorter loan term to save significantly on interest.

- Buy Used (Smartly): Letting someone else take the initial depreciation hit by buying a reliable used car can save you thousands.

- Negotiate Like a Pro: Be prepared, research prices, and get pre-approved for financing before stepping into a dealership.

Internal Link: To further enhance your financial management, consider reading our article on "Mastering Your Budget: The Ultimate Guide to Financial Freedom" (replace with a relevant internal link to your blog if you have one). This will provide you with tools to manage your overall finances more effectively, complementing your efforts to lower car payments.

Conclusion: Your Roadmap to Lower Car Payments Starts Now

Congratulations on completing your comprehensive "Car Loan Quizlet" self-assessment! By systematically answering these critical questions, you’ve gained invaluable insights into your current car loan and, more importantly, identified concrete strategies to lower your monthly payments. From the power of refinancing to the subtle art of making extra principal payments, and from optimizing your credit score to scrutinizing unnecessary add-ons, you now possess a powerful toolkit.

Remember, taking control of your car loan isn’t just about saving money; it’s about reducing financial stress, freeing up your budget, and empowering you to make smarter financial decisions in every aspect of your life. Don’t let high car payments dictate your financial future.

Start today. Pull out your loan documents, check your credit score, shop around for better rates, and implement the strategies that best fit your situation. The path to lower monthly payments is clear, and with the knowledge gained from this "Car Loan Quizlet," you are well-equipped to drive towards greater financial freedom.