Unlock Luxury for Less: Your Ultimate Guide to Leasing a BMW Loaner Car

Unlock Luxury for Less: Your Ultimate Guide to Leasing a BMW Loaner Car Carloan.Guidemechanic.com

Dreaming of driving a BMW but find the price tag of a brand-new model a little steep? You’re not alone. Many luxury car enthusiasts seek savvy ways to get behind the wheel of their desired vehicle without breaking the bank. This is where the often-overlooked, yet incredibly smart, option of a BMW loaner car lease comes into play. It’s a sweet spot that offers significant savings, premium features, and the undeniable prestige of a BMW, all wrapped up in a flexible lease agreement.

In this super comprehensive guide, we’ll dive deep into everything you need to know about leasing a BMW loaner car. From understanding what these vehicles are to navigating the negotiation process and unlocking exceptional value, we’ll provide you with the expert insights needed to make an informed decision. Our goal is to equip you with the knowledge to drive away in your dream BMW, confidently and affordably.

Unlock Luxury for Less: Your Ultimate Guide to Leasing a BMW Loaner Car

What Exactly is a BMW Loaner Car? A Closer Look

Before we delve into the specifics of leasing, it’s crucial to understand what a "loaner car" truly is within the BMW ecosystem. These aren’t just any used cars; they serve a very specific and important purpose for dealerships.

The Purpose of Service Loaner Vehicles

BMW loaner cars, also known as "service loaners" or "courtesy vehicles," are brand-new BMW models provided by dealerships to customers whose personal BMWs are in for service or repair. This ensures that BMW owners maintain their mobility and continue to experience the brand’s luxury, even when their own vehicle is temporarily unavailable. These cars are meticulously maintained by the dealership’s service department, ensuring they remain in excellent condition.

Demonstrator Vehicles: A Similar Concept

Alongside service loaners, you might also encounter "demonstrator vehicles" or "demo cars." These are new BMWs that dealership staff, such as sales managers, use for a short period. Their primary purpose is to showcase the latest models and features to potential buyers, allowing for more in-depth explanations and hands-on demonstrations. Both service loaners and demonstrators fall under the umbrella of low-mileage, pre-driven vehicles available for lease.

Typical Mileage and Condition

A key characteristic of BMW loaner cars is their relatively low mileage. Most loaner vehicles accumulate between 2,000 to 10,000 miles before they are retired from the loaner fleet and made available for sale or lease. This mileage is typically logged under careful supervision and regular maintenance, meaning these cars are far from "worn out." They are kept in pristine condition, regularly detailed, and serviced according to BMW’s strict schedules.

Why Consider a BMW Loaner Car for Lease? Unbeatable Advantages

The appeal of a BMW loaner car lease stems from a compelling array of benefits that make it an incredibly smart financial move for luxury car seekers. Based on my experience in the automotive finance industry, these advantages often outweigh the minor considerations.

Significant Savings on the Purchase Price

One of the most attractive aspects of leasing a BMW loaner car is the substantial discount on its initial price. Since these vehicles are no longer technically "brand new" (due to their prior use as loaners), dealerships are motivated to move them off their lot. This translates to a significantly reduced selling price, often thousands of dollars below the MSRP of an identical new model. This lower capitalized cost directly leads to lower monthly lease payments.

Access to Premium Features for Less

BMW loaner cars are frequently well-equipped with desirable packages and options. Dealerships tend to stock their loaner fleets with popular configurations, ensuring customers enjoy a premium experience even when driving a courtesy vehicle. This means you can often lease a loaner with features like a panoramic sunroof, advanced driver-assistance systems, or a premium sound system, all for a lease payment that might otherwise only get you a base model new BMW.

Meticulously Maintained and Dealer-Serviced

You might wonder about the care these vehicles receive. Rest assured, BMW loaner cars are meticulously maintained by the dealership’s certified technicians. They adhere strictly to BMW’s service schedules, ensuring optimal performance and longevity. This diligent maintenance means you’re leasing a vehicle that has been cared for by experts, minimizing potential mechanical issues during your lease term.

Less Initial Depreciation Hit Absorbed

New cars suffer their steepest depreciation in the first year. When you lease a BMW loaner, the dealership has already absorbed a significant portion of this initial depreciation. This means the residual value, which is crucial for lease calculations, is set against an already discounted price, making your lease payments more favorable. It’s like getting a head start on savings.

Still a Recent Model Year

While not brand-new, BMW loaner cars are typically only one or two model years old, if not the current model year. This means you’re still driving a very modern vehicle with the latest technology, safety features, and design aesthetics. You won’t feel like you’re driving an outdated car; in many cases, it will be indistinguishable from a brand-new model to the casual observer.

Potential Pitfalls: Disadvantages of Leasing a BMW Loaner

While the benefits are compelling, it’s equally important to understand the potential drawbacks of a BMW loaner car lease. Being aware of these points will help you make a truly informed decision and avoid any surprises down the road.

Not "Brand New" – Minor Wear and Tear

The most obvious disadvantage is that the vehicle isn’t factory-fresh. While dealerships maintain their loaners meticulously, these cars have been driven by various individuals. This means there might be minor cosmetic imperfections, such as a tiny scratch, a slight ding, or some wear on the interior surfaces. It’s crucial to inspect the car thoroughly, as you would any used vehicle, before committing to a lease.

Limited Customization Options

When you lease a new BMW, you have the freedom to configure it exactly to your specifications – from exterior color and interior trim to specific option packages. With a loaner car, you’re limited to the vehicles currently available in the dealer’s fleet. You won’t be able to choose specific colors or obscure options, so flexibility is key. What you see is essentially what you get.

Variable Warranty Start Date

The manufacturer’s warranty for a loaner car begins when the dealership first puts the vehicle into service, not when you sign your lease agreement. This means that a portion of the original 4-year/50,000-mile warranty might have already been used up. While many loaners are still well within their warranty period, it’s essential to confirm the exact remaining warranty coverage to ensure it aligns with your lease term.

Mileage Accumulation Can Affect Residual Value

While the mileage on loaner cars is generally low, it’s still mileage. The more miles a loaner car has accumulated, the more it will affect the vehicle’s residual value calculation. A higher starting mileage might lead to a slightly lower residual value, potentially offsetting some of the initial discount on the capitalized cost. Always clarify how the starting mileage impacts the lease’s residual value with the dealer.

Potentially Higher Money Factor

In some instances, the money factor (which is essentially the interest rate on your lease) for a loaner vehicle might be slightly higher than for a brand-new model. This isn’t always the case, and it largely depends on the dealership’s current incentives and financing partners. It’s an important detail to inquire about and compare against new car lease rates to ensure you’re getting the best overall deal.

The Leasing Process: How to Lease a BMW Loaner Car

Navigating the process of a BMW loaner car lease isn’t drastically different from leasing a new vehicle, but there are specific steps and considerations to keep in mind. Based on my experience, a structured approach leads to the best outcomes.

Finding a Dealer and Identifying Loaner Inventory

Your first step is to contact local BMW dealerships. Many dealerships list their "demonstrator," "courtesy vehicle," or "service loaner" inventory on their websites. However, it’s always a good idea to call and speak with a sales representative directly. Ask specifically about their available loaner vehicles for lease, their mileage, and their current pricing. Don’t be shy about asking for specific models or feature sets you’re interested in.

Thorough Vehicle Inspection

Once you’ve identified a potential vehicle, a comprehensive inspection is paramount. Remember, these cars have been driven by others. Scrutinize the exterior for any dings, scratches, or paint imperfections. Check the interior for wear and tear on seats, carpets, and controls. Ensure all electronics and features are fully functional. This is your opportunity to document any existing damage before you take possession, preventing future disputes.

Understanding and Negotiating the Lease Terms

This is where the real work, and potential savings, come in. A lease agreement is made up of several key components that you need to understand and negotiate.

Negotiating the Capitalized Cost (Selling Price)

The capitalized cost is the vehicle’s agreed-upon selling price, which forms the basis of your lease payment. Since loaners are pre-driven, there’s often more room for negotiation on this figure compared to a brand-new car. Aim for a significant discount off the original MSRP. Every dollar you shave off the cap cost will reduce your monthly payment.

Residual Value: How Pre-Driven Mileage Affects It

The residual value is the estimated value of the car at the end of the lease term. For loaner cars, the residual value is typically calculated based on the original MSRP but then adjusted downwards to account for the starting mileage. For example, BMW Financial Services might deduct a certain amount (e.g., $0.25 per mile) from the residual for every mile over a very low threshold (e.g., 500 miles). Understand this calculation thoroughly. A lower starting mileage generally leads to a higher residual, which is favorable for leasing.

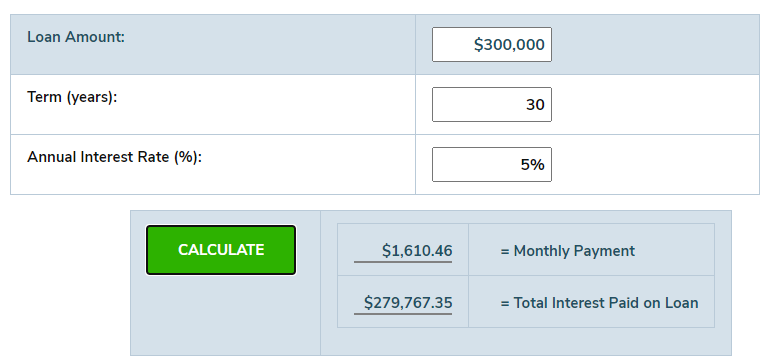

The Money Factor (Lease Interest Rate)

The money factor is essentially the interest rate charged on your lease. It’s expressed as a very small decimal (e.g., 0.00150). You can convert this to an approximate annual interest rate by multiplying by 2400. While some loaners might have a slightly higher money factor than new cars, this is negotiable. Your credit score will significantly influence the money factor you qualify for. For a deeper dive into understanding lease money factors, check out our comprehensive guide on .

Mileage Allowance and Lease Term

Standard lease terms are typically 36 months, with mileage allowances of 10,000, 12,000, or 15,000 miles per year. Choose an allowance that accurately reflects your driving habits to avoid costly overage fees at the end of the lease. Discuss if there’s any flexibility in adjusting the mileage allowance for a loaner car.

Warranty Specifics

Reconfirm the exact start date and remaining duration of the manufacturer’s warranty. Ensure it will cover the majority, if not all, of your lease term. If the remaining warranty is short, discuss options for extended warranty coverage with the dealer.

The All-Important Test Drive

Even though it’s a "used" car, a test drive is non-negotiable. Pay close attention to how the car drives, any unusual noises, and the feel of the steering and brakes. Test all features, from the infotainment system to the climate control. This is your final check to ensure the car meets your expectations and there are no hidden issues.

Key Factors Affecting Your BMW Loaner Lease Deal

Several critical elements intertwine to determine the final cost of your BMW loaner car lease. Understanding these will empower you to negotiate effectively and ensure you’re getting the best possible value.

Original MSRP vs. Negotiated Selling Price

The starting point for any lease calculation is the capitalized cost, which is the negotiated selling price of the vehicle. For a loaner, this price is typically significantly lower than the original Manufacturer’s Suggested Retail Price (MSRP). The larger the discount you can secure off the MSRP, the lower your monthly payments will be. Pro tips from us: always focus your negotiation on this ‘cap cost’ first.

Residual Value: The Cornerstone of Your Lease

The residual value is arguably the most crucial factor in a lease. It’s the predicted value of the car at the end of your lease term. For loaner cars, the residual value is often calculated based on the original MSRP of the car, but then adjusted downwards to account for the miles already on the odometer when you lease it. For example, if a new car has a 60% residual after 36 months, a loaner with 5,000 miles might have its residual reduced by a few percentage points or by a fixed amount per mile. A higher residual value (as a percentage of the cap cost) translates directly to lower monthly payments.

The Money Factor: Your Lease’s Interest Rate

The money factor represents the interest rate you pay on the amount of money you’re financing (the depreciation portion of the lease). It’s typically presented as a small decimal (e.g., 0.00125). Your credit score plays a significant role in determining the money factor you qualify for. While BMW Financial Services offers competitive rates, it’s always wise to compare them and negotiate if you believe there’s room.

Current Incentives and Rebates

Even for loaner vehicles, BMW may offer specific lease incentives or rebates that can further reduce your monthly payments or lower your drive-off costs. These incentives can change monthly, so inquire about all applicable programs. Sometimes, a loyalty rebate or a conquest rebate (for switching from a competitor) might still apply, even to an ex-loaner.

Your Credit Score: The Gateway to Better Terms

A strong credit score is paramount for securing the most favorable lease terms. Lenders, including BMW Financial Services, offer their best money factors to applicants with excellent credit. If your credit score is lower, you might face a higher money factor, which will increase your monthly payment. It’s always a good idea to know your credit score before stepping into the dealership.

Comparing BMW Loaner Lease to New Car Lease and CPO Lease

Understanding where a BMW loaner car lease fits in comparison to other leasing options is key to making the best choice for your needs and budget. Each option has its distinct advantages and disadvantages.

New Car Lease: The Premium Experience

Leasing a brand-new BMW offers the ultimate in customization and the assurance of being the first owner. You get to choose every detail, from color to options, and the full manufacturer’s warranty starts on day one of your lease. However, this premium experience comes at a higher cost. Monthly payments for a new car lease are typically higher due to the higher capitalized cost and the initial depreciation hit. If you prioritize absolute newness and customization above all else, a new car lease is the way to go, but be prepared for the higher financial commitment.

Certified Pre-Owned (CPO) Lease: A Different Path

Leasing a BMW Certified Pre-Owned (CPO) vehicle is another alternative that offers value. CPO BMWs undergo a rigorous inspection process and come with an extended warranty from BMW, providing significant peace of mind. However, CPO vehicles generally have higher mileage and are older than loaner cars. While they offer a good balance of value and warranty coverage, their capitalized cost might be higher than a low-mileage loaner, and the residual value might not be as favorable as an ex-loaner, depending on the specific vehicle. Loaners often represent a unique sweet spot – nearly new, low mileage, with a substantial discount. For official details on BMW’s Certified Pre-Owned program and warranty specifics, you can always refer to the .

The Loaner Lease Advantage: A Unique Middle Ground

A BMW loaner car lease effectively bridges the gap between a brand-new lease and a traditional used car purchase or CPO lease. You get a vehicle that is almost new, often with very low mileage, and frequently equipped with desirable features, but at a significantly reduced price. This reduction in the capitalized cost leads directly to lower monthly payments compared to leasing an identical new model. It’s an excellent option for those who want the luxury and technology of a recent BMW model without paying the premium for a car with zero miles on the odometer. If you’re still weighing your options between leasing and buying, our article provides valuable insights.

Pro Tips for Securing the Best BMW Loaner Lease Deal

Based on years of analyzing lease contracts and assisting numerous clients, I’ve distilled the most effective strategies for securing an exceptional BMW loaner car lease. These insights can save you thousands over your lease term.

Be Flexible on Color and Options

One of the biggest advantages of a loaner car deal is the significant discount. To maximize this, embrace flexibility. If you’re open to different exterior colors or interior trims, or if you don’t require a very specific, rare option, your chances of finding an outstanding deal increase dramatically. Dealerships want to move their loaner inventory, so being less rigid can open doors to better negotiation leverage.

Shop Around Multiple Dealerships

Never settle for the first offer. BMW dealerships operate independently, and their inventory of loaner cars, as well as their pricing strategies, can vary widely. Contact several dealerships within a reasonable driving distance. Get quotes for comparable loaner vehicles and use them to leverage a better deal. This competitive environment works in your favor.

Negotiate Aggressively on the Selling Price (Capitalized Cost)

This is the most critical negotiation point. Remember, the loaner vehicle is no longer "new," so it commands a lower price. Aim for a substantial discount off the original MSRP – often 15-20% or even more, depending on the model, mileage, and how long it’s been in the loaner fleet. A lower capitalized cost directly translates to lower monthly payments. Don’t be afraid to walk away if the initial offers aren’t compelling.

Understand All the Numbers – Beyond Just the Monthly Payment

While the monthly payment is important, it’s a result of several factors. Focus on negotiating the capitalized cost, the money factor, and understanding how the residual value is calculated for that specific loaner car’s mileage. A common mistake many prospective lessees make is only focusing on the monthly payment, which can hide unfavorable terms elsewhere in the contract. Ensure you understand every line item.

Time Your Purchase Strategically

Just like new cars, loaner cars often see better deals towards the end of the month, quarter, or year. Dealerships have sales quotas to meet, and a loaner vehicle can be a great way for them to hit their targets. If you can be patient, waiting for these periods might yield more aggressive pricing and incentives.

Thoroughly Review the Warranty Coverage

Before signing, confirm the exact remaining manufacturer’s warranty. Ensure it will cover the majority, if not all, of your lease term. If the remaining warranty is short, discuss options for purchasing an extended warranty through BMW. This protects you from unexpected repair costs during your lease. You want peace of mind knowing your luxury vehicle is covered.

Common Myths and Misconceptions about BMW Loaner Cars

Misinformation can often deter potential buyers or lessees from exploring excellent opportunities. Let’s debunk some common myths surrounding BMW loaner cars.

Myth 1: "Loaner Cars are Abused and Driven Recklessly."

Reality: This is a pervasive misconception. While it’s true that various people drive loaner cars, dealerships have a vested interest in keeping them in excellent condition. These vehicles are future inventory for sale or lease. Dealerships closely monitor their loaner fleet, often restricting their use to local areas and ensuring they are serviced regularly. Any significant damage would reduce their resale/lease value, which is not in the dealership’s interest. Most drivers treat them with reasonable care, knowing they are temporary.

Myth 2: "The Warranty is Completely Gone or Severely Limited."

Reality: The manufacturer’s warranty does start when the car is put into service as a loaner. However, it’s rarely "completely gone." Most loaner cars are retired from the fleet with 5,000 to 10,000 miles, meaning a significant portion of the original 4-year/50,000-mile warranty still remains. You’ll typically have 3+ years and 40,000+ miles of warranty coverage. Always verify the exact in-service date and remaining coverage, but don’t assume the warranty is a non-factor.

Myth 3: "You Can’t Lease a Loaner Car."

Reality: This is absolutely false, and the very premise of this article! Leasing a BMW loaner car is a very common and financially savvy practice. Dealerships actively market these vehicles for lease because it allows them to recoup their investment and cycle through their inventory efficiently. In many cases, the lease programs for loaners are designed to be highly attractive to facilitate their quick movement off the lot.

Myth 4: "Loaner Cars are Only Base Models with No Features."

Reality: While some base models are used as loaners, many dealerships equip their courtesy fleet with popular options and packages. This ensures that customers receiving a loaner still experience the luxury and technology BMW is known for, and it also makes the cars more appealing when they are eventually offered for sale or lease. You can often find loaners with desirable upgrades like premium sound systems, navigation, driver-assistance features, and upgraded interiors.

Conclusion: Drive Your Dream BMW for Less

Leasing a BMW loaner car presents an exceptional opportunity to experience the luxury, performance, and advanced technology of a BMW at a significantly reduced cost. It’s a strategic move for the savvy consumer who values both prestige and practicality. By understanding what these vehicles are, recognizing their unique benefits and potential drawbacks, and mastering the negotiation process, you can unlock incredible value.

Remember, the key to a successful BMW loaner car lease lies in thorough research, meticulous inspection, and confident negotiation. Don’t let common misconceptions deter you from exploring this fantastic option. With the insights provided in this comprehensive guide, you are now well-equipped to approach BMW dealerships, identify the best deals, and confidently drive away in your dream BMW, all while keeping more money in your pocket. Happy leasing!