Unlock Predictability: The Ultimate Guide to Capped Car Loans and How They Protect Your Wallet

Unlock Predictability: The Ultimate Guide to Capped Car Loans and How They Protect Your Wallet Carloan.Guidemechanic.com

Buying a car is a significant financial decision, often involving a loan that will span several years. While the excitement of a new vehicle is undeniable, the financial commitment can be daunting, especially when navigating the complexities of interest rates. In a world where economic shifts can impact your monthly budget, understanding all your financing options is crucial.

This is where a capped car loan emerges as a sophisticated, yet often misunderstood, financing solution. It’s a product designed to offer a unique blend of flexibility and protection, providing a safety net against rising interest rates while potentially allowing you to benefit if rates fall. As an expert blogger and professional SEO content writer, I’ve seen firsthand how clarity on such topics can empower consumers.

Unlock Predictability: The Ultimate Guide to Capped Car Loans and How They Protect Your Wallet

In this comprehensive guide, we will delve deep into the world of capped car loans. We’ll explore what they are, how they work, their distinct advantages and disadvantages, and crucially, whether they are the right choice for your financial situation. Our goal is to equip you with the knowledge to make an informed decision, ensuring your car ownership journey is as smooth and predictable as possible.

What Exactly is a Capped Car Loan?

At its core, a capped car loan is a type of variable-rate auto financing that includes a crucial safety mechanism: an interest rate "cap." Unlike a purely variable loan where your interest rate can fluctuate indefinitely with market changes, a capped loan sets an upper limit on how high your interest rate can go.

Think of it as having a guardian angel for your interest payments. While the rate can move up and down based on a specific financial index, it will never exceed a pre-agreed maximum percentage. This cap provides a vital layer of financial security, shielding you from unexpected payment spikes caused by dramatic market fluctuations.

The Mechanics Behind the Cap: How it Works

To truly understand a capped car loan, we need to peel back the layers and examine its internal workings. It’s more nuanced than a simple fixed or variable rate, offering a strategic middle ground.

Most capped car loans are tied to a benchmark interest rate, often referred to as an "index rate." This index could be the Prime Rate, LIBOR (though less common now), or another widely recognized financial indicator. Your actual loan interest rate is then calculated by adding a predetermined margin to this index rate.

For example, if the index rate is 3% and your margin is 2%, your initial rate would be 5%. If the index rate rises to 4%, your rate would become 6%. However, with a cap, this movement has a ceiling.

Let’s say your loan has a cap of 8%. If the index rate (plus your margin) starts to climb and hits 8%, it stops there. Even if the index continues to rise, your interest rate on the loan will not exceed 8%. This mechanism provides unparalleled peace of mind, knowing your maximum payment is fixed.

Conversely, if the index rate drops, your loan rate will also decrease, potentially leading to lower monthly payments. Some capped loans also feature a "floor," which is a minimum interest rate. This means your rate won’t go below a certain percentage, even if the index plummets. It’s important to clarify whether your specific loan includes both a cap and a floor.

The Distinct Benefits of Opting for a Capped Car Loan

Choosing a capped car loan comes with several compelling advantages, particularly for those who prioritize financial stability and predictability.

1. Protection from Rising Interest Rates

This is arguably the most significant benefit. In an unpredictable economic climate, interest rates can climb, sometimes rapidly. A purely variable loan leaves you exposed to these increases, potentially leading to significantly higher monthly payments than you initially budgeted for.

With a capped car loan, you have a guaranteed ceiling. Your payments will never exceed a certain amount due to interest rate hikes. Based on my experience, this protection is invaluable, especially for long-term loans where market conditions can change dramatically over several years.

2. Enhanced Budgetary Certainty

Knowing the absolute maximum your monthly car payment could be provides immense relief for budget planning. Even though your rate might fluctuate, the cap ensures you can always forecast your worst-case scenario. This clarity allows for more robust financial planning and reduces the stress associated with unexpected expenses.

It helps you avoid the dreaded "payment shock" that can occur with uncapped variable loans. You can set aside funds or adjust other expenses with confidence, knowing your car payment won’t spiral out of control.

3. Potential for Lower Payments if Rates Drop

Unlike a fixed-rate loan, where your interest rate remains constant regardless of market movements, a capped car loan offers the best of both worlds. If the underlying index rate decreases, your interest rate will follow suit (down to a potential floor). This means your monthly payments could actually go down, saving you money over the life of the loan.

This flexibility is a powerful advantage, allowing you to benefit from favorable market conditions without the extreme risk of an uncapped variable loan. It’s a smart strategy for consumers who want some market exposure but with a defined limit on their downside.

4. Peace of Mind

Ultimately, the blend of protection and potential savings translates into significant peace of mind. You can enjoy your new vehicle without constantly worrying about economic forecasts or interest rate announcements. This emotional benefit should not be underestimated, as financial stress can impact many aspects of life.

Pro tips from us: Always prioritize financial products that reduce your stress while aligning with your long-term goals. A capped loan effectively hedges against a major financial unknown.

Potential Downsides and Important Considerations

While capped car loans offer attractive benefits, they aren’t without their considerations. It’s essential to understand the potential drawbacks before committing.

1. Potentially Higher Initial Interest Rate

Lenders take on a certain amount of risk by offering a cap, as they forgo the potential for unlimited earnings if rates skyrocket. To compensate for this, the initial interest rate on a capped car loan might be slightly higher than what you’d find on a purely variable-rate loan.

This slight premium is essentially the cost of the "insurance" against rising rates. You need to weigh whether the security of the cap is worth this potentially higher starting point.

2. Missing Out on Significant Rate Drops (If a Floor Exists)

If your capped loan also includes a floor rate, you won’t benefit from interest rate drops below that specific threshold. While your rate won’t go above the cap, it also won’t go below the floor, even if market rates plummet further.

This is a trade-off for the protection offered by the cap. Understanding both the cap and the floor is critical to assessing the full range of potential payment scenarios.

3. Complexity Compared to Fixed-Rate Loans

A fixed-rate loan is straightforward: your rate and payment never change. Capped car loans, with their variable component, index rates, margins, caps, and potential floors, are inherently more complex.

This complexity requires a more thorough understanding of the loan terms and how market movements could impact your payments. It’s not a set-it-and-forget-it type of loan in the same way a fixed-rate option is.

4. Less Common and Fewer Lenders

Capped car loans are not as widely available as traditional fixed or variable rate options. This means you might need to shop around more extensively to find a lender that offers them, potentially limiting your choices and negotiation power.

Based on my experience, it’s worth the extra effort to seek them out if the benefits align with your financial strategy. Don’t assume every bank or credit union will have this product readily available.

Who Should Consider a Capped Car Loan?

Given its unique characteristics, a capped car loan is best suited for specific financial profiles and risk tolerances.

- The Risk-Averse Borrower: If you’re someone who values predictability and gets anxious about market volatility, a capped loan offers a comforting safety net. It allows you to participate in potential rate drops without the fear of unlimited rate hikes.

- Individuals with Fixed Budgets: For those who need to maintain a strict monthly budget, the cap provides crucial protection. You know your maximum expenditure, making it easier to plan your finances without the stress of potential payment increases.

- Those Anticipating Market Volatility: If economic indicators suggest that interest rates might rise in the near future, but you still want the potential benefit of a rate decrease, a capped loan is a strategic choice. It’s a proactive measure against future uncertainty.

- Borrowers Who Plan to Keep the Car for the Long Term: The longer the loan term, the more exposed you are to interest rate fluctuations. A cap becomes more valuable over extended periods, offering protection over several years.

How to Find the Best Capped Car Loan

Securing the right capped car loan requires diligence and thorough research. It’s not just about finding any capped loan, but finding the one that best fits your specific needs.

1. Research Multiple Lenders

Don’t settle for the first offer you receive. Banks, credit unions, and online lenders all have different products and rates. Cast a wide net to compare terms, initial interest rates, cap percentages, and any potential floor rates.

Pay close attention to how each lender’s capped loan is structured. Some might have a lower cap but a higher initial rate, or vice-versa.

2. Compare the Fine Print Meticulously

The devil is often in the details. Understand every aspect of the loan agreement, including:

- The Index Rate: What financial benchmark is your loan tied to?

- The Margin: How much is added to the index rate to determine your loan rate?

- The Cap Rate: What is the absolute maximum your interest rate can reach?

- The Floor Rate (if any): What is the absolute minimum your interest rate can reach?

- Adjustment Frequency: How often can your interest rate change (e.g., monthly, quarterly, annually)?

- Fees: Are there any origination fees, prepayment penalties, or other charges?

Common mistakes to avoid are focusing solely on the initial interest rate and neglecting to fully understand the cap and floor. Always ask for a detailed breakdown of all potential scenarios.

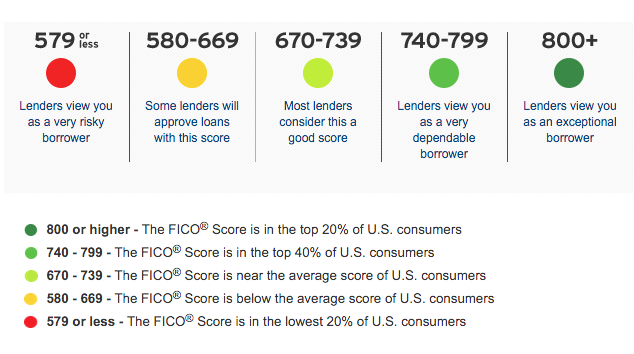

3. Understand Your Credit Score

Your credit score plays a significant role in the interest rate you’ll be offered. Before applying, obtain a copy of your credit report and score. If there are errors, dispute them. If your score is low, consider taking steps to improve it before applying, as a higher score can lead to more favorable terms.

A good credit history demonstrates your reliability as a borrower and can unlock better loan options, including more competitive capped rates.

Key Terms to Understand

Navigating car financing requires a grasp of specific terminology. Here are some essential terms related to capped car loans:

- APR (Annual Percentage Rate): This represents the true annual cost of borrowing, including the interest rate and certain fees. It gives you a more comprehensive picture than just the interest rate alone.

- Principal: The original amount of money you borrow for the car.

- Term: The length of time you have to repay the loan, typically expressed in months (e.g., 60 months, 72 months).

- Cap Rate: The maximum interest rate your loan can reach, regardless of how high the index rate climbs.

- Floor Rate: The minimum interest rate your loan can reach, regardless of how low the index rate drops (not present in all capped loans).

- Index Rate: The external financial benchmark (e.g., Prime Rate) that your loan’s variable interest rate is tied to.

- Margin: The fixed percentage added to the index rate to determine your actual loan interest rate.

Common Mistakes to Avoid When Choosing a Capped Car Loan

As an expert, I’ve seen borrowers make preventable errors. Here are some common mistakes to steer clear of:

- Not Understanding the Cap vs. Floor: Assuming all capped loans are the same. Some only have a cap, others have both. Clarity on this is paramount for managing expectations.

- Focusing Only on the Initial Rate: A low initial rate might seem appealing, but if the cap is very high, you could still face substantial increases. Always look at the cap rate in conjunction with the initial rate.

- Ignoring Fees: Loan origination fees, administrative charges, and other hidden costs can significantly increase the overall cost of your loan. Always ask for a full disclosure of all fees.

- Skipping the Fine Print: As mentioned, the details matter. Don’t rush through the loan agreement. If you don’t understand something, ask for clarification.

- Not Considering Your Future Financial Situation: While the cap offers protection, think about whether your income or expenses might change. Will you still be comfortable with the maximum possible payment if circumstances shift?

Pro Tips for Securing and Managing Your Capped Car Loan

Based on my experience, a little preparation and smart management can go a long way in optimizing your capped car loan experience.

1. Improve Your Credit Score Before Applying

A higher credit score signals less risk to lenders, potentially unlocking lower initial interest rates and more favorable cap terms. Take time to review your credit report, dispute errors, and pay down existing debts before you apply.

Even a small improvement in your score can translate into significant savings over the life of your loan.

2. Shop Around Aggressively

Because capped car loans are less common, it’s even more important to compare offers from multiple lenders. Don’t just check with your primary bank; explore credit unions, online lenders, and even dealerships that partner with various financial institutions.

Each lender might structure their capped loan product differently, so a comprehensive comparison is essential.

3. Understand the Adjustment Period

Know how frequently your interest rate can adjust. Some loans adjust monthly, others quarterly or annually. This impacts how quickly market changes reflect in your payments.

Familiarity with the adjustment period helps you anticipate and plan for potential payment fluctuations.

4. Set Up Automatic Payments

To avoid late fees and maintain a good payment history, set up automatic payments from your bank account. This ensures your payments are always made on time, building positive credit and preventing unnecessary charges.

It also removes the mental burden of remembering due dates.

5. Monitor Market Rates

Even with a cap, it’s wise to keep an eye on general interest rate trends. If rates drop significantly and your loan has no floor (or a very low one), you might see your payments decrease. If rates are consistently high and you’re near your cap, you know you’re protected.

Staying informed empowers you to understand your loan’s performance. For detailed information on current market interest rates, you can consult reliable financial news sources like The Wall Street Journal or the Federal Reserve’s official website.

Capped Car Loans vs. Fixed-Rate vs. Variable-Rate Loans: A Comparison

To truly appreciate the value of a capped car loan, it helps to see it in contrast to its more common counterparts: fixed-rate and purely variable-rate loans.

| Feature | Fixed-Rate Car Loan | Variable-Rate Car Loan | Capped Car Loan |

|---|---|---|---|

| Interest Rate | Stays the same throughout the loan term | Fluctuates with market conditions | Fluctuates with market conditions, but has a maximum |

| Payment Predictability | Highly predictable, always the same | Least predictable, can change frequently | Highly predictable (up to a maximum) |

| Risk of Rate Increases | None | High | Limited (only up to the cap) |

| Benefit from Rate Drops | None | High (payments decrease) | Moderate (payments decrease, possibly to a floor) |

| Initial Interest Rate | Often slightly higher than initial variable rates | Often the lowest initial rates | Typically higher than pure variable, lower than fixed |

| Complexity | Low (very straightforward) | Moderate (requires monitoring market) | Moderate to High (cap, floor, index, margin) |

| Best For | Risk-averse, fixed budget, value simplicity | Risk-tolerant, confident in declining rates | Risk-averse but want potential for savings, balanced approach |

This comparison highlights that a capped car loan is a hybrid solution, aiming to give you the best of both worlds: the potential for lower payments if rates fall, combined with the critical protection against rate surges.

The Application Process: What to Expect

Applying for a capped car loan is similar to applying for any other auto loan, but with a few key differences in what you’ll review.

- Pre-Approval: It’s always a smart move to get pre-approved before you start car shopping. This gives you a clear budget and allows you to negotiate with the dealership as a cash buyer.

- Required Documentation: You’ll typically need:

- Proof of identity (driver’s license, social security number)

- Proof of income (pay stubs, tax returns)

- Proof of residency (utility bill)

- Details about the vehicle (if already chosen)

- Credit Check: The lender will pull your credit report to assess your creditworthiness and determine your interest rate and cap terms.

- Reviewing the Offer: This is where the specific details of the capped loan come into play. Carefully review the initial interest rate, the cap rate, the floor rate (if any), the index used, and the adjustment frequency. Don’t hesitate to ask questions.

- Signing the Agreement: Once you’re satisfied with the terms, you’ll sign the loan agreement. Make sure you receive a copy for your records.

Remember, clarity is key. Ensure you fully understand every clause before you put pen to paper.

Refinancing a Capped Car Loan: Is It Possible?

Yes, refinancing a capped car loan is generally possible, just like refinancing other types of auto loans. You might consider refinancing if:

- Market Rates Have Significantly Dropped: If market rates have fallen well below your current loan’s initial rate, and your capped loan has a high floor (or no floor), you might be able to secure a new, lower fixed or variable rate.

- Your Credit Score Has Improved: A significantly improved credit score can qualify you for better terms than you initially received.

- You Want a Different Loan Type: You might decide a fixed-rate loan is now preferable, or perhaps a purely variable loan if you become more comfortable with risk.

Before refinancing, always calculate the total cost savings versus any new fees associated with the new loan.

Future Outlook: The Evolving Landscape of Car Financing

The auto financing market is continuously evolving, driven by technological advancements, economic shifts, and changing consumer demands. While capped car loans offer a robust solution today, we can expect continued innovation.

- Personalized Lending: More sophisticated algorithms will likely lead to even more tailored loan products, potentially offering highly customized caps and floors based on individual risk profiles.

- Digitalization: The application and approval process will become even more streamlined, with digital platforms making it easier to compare and secure loans from a wider array of lenders.

- Focus on Flexibility: As economic uncertainty persists, loan products that offer a balance of flexibility and protection, like capped loans, are likely to gain more prominence.

Staying informed about these trends will allow consumers to leverage the best financing options available.

Your Journey to Confident Car Ownership Starts Here

A capped car loan is a powerful financial tool, offering a unique blend of protection against rising interest rates and the potential to benefit from rate decreases. It’s an intelligent choice for individuals who value budgetary certainty and peace of mind in their financial planning.

By understanding its mechanics, benefits, and considerations, you can confidently determine if this innovative financing option aligns with your car ownership goals. Don’t let the fear of fluctuating interest rates deter you from your dream car. Empower yourself with knowledge, shop wisely, and drive away with the confidence that your wallet is protected.

Start your research today, compare your options diligently, and embark on a predictable and secure path to owning your next vehicle with a smart capped car loan.