Unlock Savings: Your Ultimate Guide on How to Get Your Car Loan Lowered

Unlock Savings: Your Ultimate Guide on How to Get Your Car Loan Lowered Carloan.Guidemechanic.com

Are you feeling the pinch of high monthly car payments? You’re not alone. Many car owners find themselves in a situation where their current auto loan no longer aligns with their financial reality or could simply be improved. The good news is, you don’t have to passively accept your current terms. There are effective strategies you can employ to significantly lower your car loan, reduce your interest rate, and free up valuable cash each month.

As an expert blogger and professional SEO content writer, I’ve spent years analyzing financial strategies that genuinely benefit consumers. Based on my experience, navigating the world of auto financing can seem daunting, but with the right knowledge and approach, you can take control. This comprehensive guide will walk you through every step, from understanding your current loan to exploring powerful options like refinancing and negotiation, ensuring you have all the tools to make an informed decision. Our ultimate goal is to provide you with actionable insights that put more money back in your pocket.

Unlock Savings: Your Ultimate Guide on How to Get Your Car Loan Lowered

Why Consider Lowering Your Car Loan? More Than Just Monthly Savings

Before we dive into the "how," let’s briefly touch on the "why." Lowering your car loan payment or interest rate offers a multitude of benefits that extend beyond just a smaller monthly bill.

Firstly, it provides crucial financial relief. If your financial situation has changed – perhaps you’ve taken on new responsibilities, faced unexpected expenses, or simply want to optimize your budget – reducing a major fixed cost like a car payment can make a significant difference. It frees up cash flow, which can then be allocated to other essential needs, savings goals, or even debt reduction.

Secondly, a lower interest rate means you pay less over the life of the loan. Even a small percentage point reduction can translate into hundreds, or even thousands, of dollars saved over several years. This is essentially keeping more of your hard-earned money in your own account, rather than paying it to the lender. Ultimately, taking proactive steps to lower your car loan is a smart financial move that contributes to your overall economic well-being and stability.

The Foundation: What You Need Before You Start

Before you pick up the phone or fill out an application, laying the groundwork is essential. Understanding your current standing and gathering the necessary information will significantly strengthen your position and streamline the process.

1. Understand Your Current Car Loan

The first step is to become intimately familiar with the details of your existing auto loan. Pull out your loan documents or log into your lender’s online portal.

Focus on key metrics like your current interest rate, the remaining balance on the loan, and the exact number of months left on your loan term. You should also check for any prepayment penalties. Some older or subprime loans might include clauses that charge you a fee for paying off your loan early, which is something you need to factor into your decision-making. Knowing these specifics will give you a clear baseline from which to compare new offers.

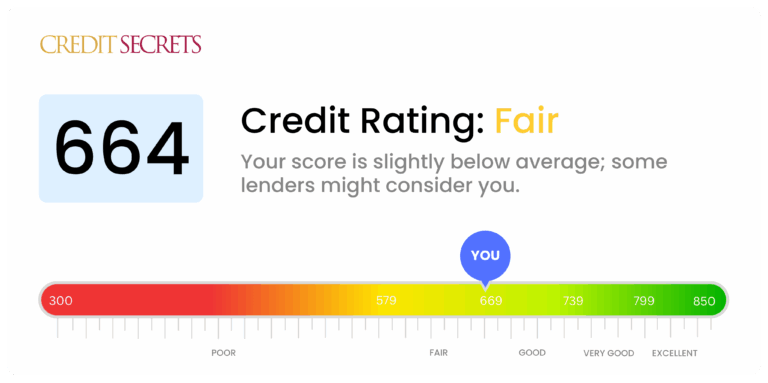

2. Check Your Credit Score

Your credit score is perhaps the single most important factor that lenders consider when evaluating a loan application. A higher credit score signals less risk to lenders, which typically translates to lower interest rates.

Take the time to obtain your latest credit score and a full credit report. You can often get a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once a year through AnnualCreditReport.com. Review your report for any inaccuracies and dispute them immediately, as errors can negatively impact your score. If your credit score has improved since you first took out your loan, you’re in an excellent position to secure a better rate. can provide more detailed information on this crucial step.

3. Gather Necessary Documents

Being prepared with all the required paperwork will make any application process much smoother and faster.

Typically, you’ll need proof of identity (like a driver’s license), proof of income (recent pay stubs or tax returns), and documentation related to your current car loan (account statements, original loan agreement). You’ll also need details about your vehicle, such as its Vehicle Identification Number (VIN), make, model, and mileage. Having these documents organized and ready will demonstrate your seriousness and readiness to lenders, helping to expedite their review.

Primary Strategies to Lower Your Car Loan

Now that you’re well-prepared, let’s explore the most effective strategies for how to get your car loan lowered. Each approach has its nuances and benefits, so consider which one best fits your personal circumstances.

Strategy 1: Refinancing Your Car Loan

Refinancing is often the most straightforward and effective way to lower your car loan. It essentially involves taking out a new loan to pay off your existing one, ideally with better terms.

What is Refinancing and When is it a Good Idea?

Refinancing works by replacing your old loan with a brand-new one, usually from a different lender. The goal is to secure a lower interest rate, a shorter loan term, or a combination of both, leading to lower monthly payments or significant savings over time. It’s an excellent option if your credit score has improved since you first took out the loan, if current interest rates have dropped, or if you initially took out a loan with a high rate due to a less-than-perfect credit history. Based on my experience, many people who bought a car at a dealership and accepted the dealer’s financing without shopping around could benefit significantly from refinancing.

Step-by-Step Guide to Refinancing

- Shop Around for Lenders: Don’t just go with the first offer. Check rates from various banks, credit unions, and online lenders. Each institution has different criteria and rates. Credit unions, in particular, often offer competitive rates to their members.

- Get Pre-approved: Many lenders offer pre-approval processes that involve a soft credit inquiry, which won’t hurt your credit score. This allows you to see potential rates and terms without committing.

- Compare Offers Carefully: Look beyond just the monthly payment. Compare the Annual Percentage Rate (APR), which includes the interest rate and any fees, and the total cost of the loan over its new term. Be wary of offers that significantly extend your loan term, as this could mean paying more interest overall, even with a lower monthly payment.

- Complete the Application: Once you choose a lender, you’ll complete a full application, which will involve a hard credit inquiry. This will temporarily ding your credit score by a few points, but the long-term benefits of a lower rate usually outweigh this minor drawback.

- Finalize the Loan: If approved, the new lender will pay off your old loan, and you’ll start making payments to them under the new, improved terms.

Common Mistakes to Avoid When Refinancing

One of the most common mistakes is extending the loan term too much just to achieve a lower monthly payment. While it might seem appealing to drastically reduce your monthly outflow, stretching a 3-year loan into a 6-year one, even at a lower interest rate, could mean paying more in total interest over the life of the loan. Another error is failing to check for prepayment penalties on your current loan. If your existing lender charges a fee for early payoff, factor that into your calculation to ensure refinancing is still worthwhile.

Pro tips from us: Always use an online car loan refinance calculator to compare different scenarios. This tool can quickly show you the total cost of various loan options, making it easier to see the true savings. Also, consider setting up automatic payments for your new loan; some lenders offer a small interest rate discount for doing so.

Strategy 2: Negotiating with Your Current Lender

While refinancing with a new lender is often the most effective route, sometimes it’s worth trying to negotiate directly with your existing lender. This strategy is particularly relevant if you’ve had a recent, significant improvement in your credit score or if you’re facing a temporary financial hardship.

When to Consider This Approach

Negotiating with your current lender might be a viable option if you have a strong payment history with them and your credit score has significantly improved. They might be willing to adjust your interest rate or extend your loan term slightly to retain your business, especially if they see you as a low-risk customer who could easily refinance elsewhere. Additionally, if you’re experiencing a short-term financial difficulty, your lender might be open to discussing payment deferrals or forbearance options, though these typically don’t lower your overall loan cost and should be used with caution.

How to Approach Your Lender

Preparation is key when approaching your lender. Gather evidence of your improved financial standing, such as a higher credit score, increased income, or a consistent payment history. Clearly articulate your request: do you want a lower interest rate, a reduced monthly payment, or a temporary pause in payments? Be polite, professional, and firm. Explain why you deserve better terms – perhaps you’ve been a loyal customer, or you’re simply exploring more competitive offers from other institutions.

Present them with any better offers you’ve received from other lenders, using them as leverage. For example, you could say, "I’ve been offered a 4% APR from Bank X. Would you be able to match or beat that rate to keep my business?" This approach shows you’ve done your homework and are serious about finding better terms.

Potential Outcomes

While it’s less common for lenders to dramatically reduce your interest rate simply through negotiation, it’s not impossible. More often, they might offer a slight reduction, especially if you have a compelling reason and good alternatives. They might also be willing to extend your loan term, which would lower your monthly payment but could increase the total interest paid over time. In cases of financial hardship, they might offer a payment deferral, allowing you to skip a payment or two, but remember that interest usually accrues during this period, and the skipped payments are added to the end of your loan. Always get any agreed-upon changes in writing.

Strategy 3: Debt Consolidation (for Broader Financial Improvement)

While not a direct method to lower just your car loan, debt consolidation can be a powerful strategy for improving your overall financial picture, which in turn can make your car loan feel less burdensome.

How it Works

Debt consolidation involves combining multiple debts, often high-interest ones like credit card balances, into a single, new loan with a lower interest rate. This could be a personal loan or even a home equity loan if you own property. By reducing your total monthly debt obligations and interest payments, you free up more cash flow. This extra cash can then indirectly make your car loan payment more manageable, or even allow you to put extra money towards your car loan principal, paying it off faster. This strategy is most effective for those struggling with several different types of debt, not just their car loan.

Strategy 4: Selling Your Car and Buying a Cheaper One

This is a more drastic but potentially very effective solution if your car loan is truly unmanageable or if you are significantly upside down (owe more than the car is worth).

When This Makes Sense

Selling your current car and purchasing a less expensive one makes sense if your financial situation has drastically changed, or if you simply bought more car than you could comfortably afford. It’s a way to hit the reset button on your auto debt. If your car is worth more than you owe, you can use the surplus to put a down payment on a cheaper vehicle, potentially eliminating a loan altogether or securing a much smaller one. Even if you’re slightly upside down, selling and making up the difference with savings might still be better than continuing to pay on an unsustainable loan.

The Process and Implications

The process involves determining your car’s market value (using resources like Kelley Blue Book or Edmunds), finding a buyer (private sale or trade-in), and then shopping for a more affordable vehicle. Be prepared to cover the difference if you owe more than your car is worth. While this might involve an initial outlay, the long-term benefit of significantly lower or no car payments can be life-changing. It’s a big decision, but for some, it’s the most impactful way to get out from under a burdensome car loan.

Alternative Approaches & Considerations

Beyond the main strategies, there are other tactics and important points to keep in mind when aiming to lower your car loan.

Paying More Than the Minimum (to Reduce Total Interest)

While this doesn’t directly lower your monthly payment, paying even a small amount extra each month can significantly reduce the total interest you pay over the life of the loan. Any extra payment typically goes directly towards the principal balance. By reducing the principal, you reduce the amount on which interest is calculated, leading to a faster payoff and substantial savings. For example, if you add just $50 to a $300 payment, you could shave months off your loan term and save hundreds in interest.

Temporarily Reducing Payments (Deferral/Forbearance)

In genuine hardship situations, such as job loss, illness, or a natural disaster, your lender might offer options like payment deferral or forbearance. This allows you to temporarily pause or reduce your payments for a specified period.

While this can provide immediate relief, it’s crucial to understand the terms. Interest usually continues to accrue during this period, and the skipped payments are often added to the end of your loan term, potentially increasing your total cost. Pro tips from us: Only use these options as a last resort for short-term crises, and always clarify how the missed payments and interest will be handled before agreeing. This is a temporary band-aid, not a long-term solution for lowering your car loan.

Common Mistakes to Avoid When Trying to Lower Your Car Loan

Successfully lowering your car loan requires careful planning and avoiding common pitfalls that can undermine your efforts or even put you in a worse financial position.

- Extending the Loan Term Too Much: This is perhaps the most frequent mistake. While a longer term means lower monthly payments, it almost always results in paying significantly more interest over the life of the loan. Always calculate the total cost, not just the monthly payment.

- Not Checking Your Credit Score: Your credit score is your leverage. Without knowing it, you can’t accurately assess your chances of getting a better rate or identify errors that might be holding you back.

- Ignoring Prepayment Penalties: Some loans, especially older ones or those from subprime lenders, include clauses that penalize you for paying off the loan early. Always verify this on your current loan agreement before refinancing.

- Only Checking One Lender: This is a crucial mistake. Different lenders have different rates and criteria. Shopping around aggressively is the only way to ensure you’re getting the best possible deal. Don’t settle for the first offer.

- Falling for Predatory Loans: Be wary of offers that seem too good to be true, especially those with extremely low monthly payments but hidden fees, very high interest rates, or complex terms. Always read the fine print and ensure the lender is reputable. Check reviews and look for transparency.

Proactive Steps for Future Car Loan Management

Once you’ve successfully lowered your car loan, or even if you’re just planning for future vehicle purchases, there are proactive steps you can take to ensure you always secure the best possible financing.

- Maintain a Good Credit Score: Consistently paying bills on time, keeping credit utilization low, and regularly checking your credit report are fundamental. A strong credit score is your most powerful tool for securing favorable interest rates on any loan.

for more insights. - Save for a Larger Down Payment: A substantial down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay. It also helps avoid being "upside down" on your loan early on.

- Shop Around for Loans Before You Shop for a Car: Get pre-approved for an auto loan from a bank or credit union before you even step foot in a dealership. This gives you negotiating power, as you’ll know exactly what rate you qualify for and won’t be reliant solely on dealer financing.

- Understand the Full Cost of Ownership: Beyond the loan payment, consider insurance, maintenance, fuel efficiency, and depreciation. A cheaper car with high insurance or frequent repairs might not be a true saving.

Conclusion: Take Control of Your Car Loan Today

Lowering your car loan is a tangible goal that can significantly improve your financial health and peace of mind. Whether through strategic refinancing, direct negotiation, or a more significant change like selling your vehicle, the power to reduce your burden is within your grasp.

Remember, preparation is key: understand your current loan, check your credit score, and gather your documents. Then, explore your options, compare offers meticulously, and avoid common pitfalls. The journey to a lower car payment begins with taking that first informed step. Don’t let high payments hold you back any longer. Start exploring your options today and unlock the savings you deserve! For more comprehensive financial advice and tools, we recommend visiting a trusted resource like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.