Unlock Savings: Your Ultimate Guide on How to Renegotiate Car Loan Interest Rates

Unlock Savings: Your Ultimate Guide on How to Renegotiate Car Loan Interest Rates Carloan.Guidemechanic.com

Are you feeling the pinch of high monthly car payments? Did you secure a car loan when your credit wasn’t at its best, or perhaps market interest rates have significantly dropped since you first signed on the dotted line? If so, you’re not alone. Many car owners unknowingly pay more than they should for their vehicle financing. The good news? You don’t have to be stuck with a high interest rate forever.

Welcome to the ultimate guide on how to renegotiate your car loan interest rate. As an expert blogger and professional SEO content writer, I’ve seen countless individuals transform their financial situations by understanding and leveraging the power of refinancing. This comprehensive article isn’t just about saving a few dollars; it’s about empowering you with the knowledge and actionable steps to significantly reduce your monthly payments, save thousands over the life of your loan, and take control of your financial future. We’ll delve deep into every aspect, from preparation to negotiation, ensuring you have all the tools to succeed.

Unlock Savings: Your Ultimate Guide on How to Renegotiate Car Loan Interest Rates

Why Should You Consider Renegotiating Your Car Loan? The Power of Refinancing

Before we dive into the "how," let’s explore the compelling reasons why renegotiating or refinancing your car loan could be one of the smartest financial moves you make this year. It’s more than just a quick fix; it’s a strategic decision that can yield substantial long-term benefits.

Lower Your Monthly Payments

This is often the primary motivator for most people. A lower interest rate directly translates to a smaller amount of interest accrued each month, which in turn reduces your total monthly payment. Imagine what you could do with an extra $50, $100, or even more back in your pocket every month! This additional cash flow can be used for savings, other debt reduction, or simply improving your daily budget.

Save Thousands Over the Loan Term

While lower monthly payments are great, the real financial magic happens over the entire life of your loan. Even a seemingly small reduction in your interest rate can shave off hundreds, if not thousands, of dollars from the total amount you pay back. Based on my experience, many people are surprised by the cumulative savings, which can be a game-changer for their financial health.

Shorten Your Loan Term (Or Lengthen It, Strategically)

Refinancing offers flexibility. If your financial situation has improved significantly, you might choose to keep your monthly payments similar but opt for a shorter loan term. This allows you to pay off your car faster, reducing the total interest paid and freeing you from debt sooner. Conversely, if cash flow is extremely tight, you could potentially extend the loan term to further lower monthly payments, though this often means paying more interest over time. It’s crucial to weigh these options carefully.

Improve Your Financial Health and Credit Score

Successfully managing and paying off a refinanced loan can positively impact your credit score over time. Demonstrating responsible borrowing habits, especially at a lower, more manageable rate, contributes to a healthier credit profile. Furthermore, freeing up cash flow can help you tackle other debts, further strengthening your overall financial position.

Key Factors That Influence Your Car Loan Interest Rate

Understanding what lenders look at is the first step toward improving your chances of securing a better rate. These factors are the pillars upon which your loan offer will be built.

Your Credit Score

Undoubtedly, your credit score is the most critical factor. It’s a numerical representation of your creditworthiness, telling lenders how likely you are to repay your debts. A higher credit score (generally above 670) signals lower risk to lenders, making them more willing to offer you their best rates. If your credit score has improved since you first took out your loan, you’re in a prime position to renegotiate.

Your Debt-to-Income Ratio (DTI)

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your ability to handle additional debt. A lower DTI (typically below 36%) indicates that you have more disposable income to cover your loan payments, making you a more attractive borrower. Pro tips from us: Always strive to keep this ratio as low as possible.

Loan-to-Value (LTV) Ratio

The LTV ratio compares the amount you want to borrow (or currently owe) to the current market value of your car. If you owe more than your car is worth (negative equity or being "upside down"), your LTV will be high, making refinancing more challenging. A lower LTV (meaning your car is worth more than you owe) indicates less risk for the lender.

Current Market Interest Rates

The broader economic environment plays a significant role. If overall interest rates have dropped since you financed your car, you’re likely to find better offers today. Lenders adjust their rates based on the federal prime rate and other economic indicators. It’s always a good idea to keep an eye on these trends.

Vehicle Age and Condition

Lenders consider the age and mileage of your vehicle. Older cars with higher mileage are generally seen as higher risk because they are more prone to mechanical issues and depreciate faster. Most lenders prefer to refinance vehicles that are less than 7-10 years old and have reasonable mileage.

Loan Term

The length of your loan also impacts the interest rate. Shorter loan terms typically come with lower interest rates because the lender’s money is tied up for a shorter period. Longer terms, while offering lower monthly payments, usually carry higher interest rates due to the increased risk over time.

Step 1: Assess Your Current Situation – The Crucial Prep Work

Before you even think about contacting a lender, you need to arm yourself with information. This preparatory phase is non-negotiable and will significantly impact your success.

Gather Your Current Loan Documents

Locate your original car loan agreement. You’ll need to know your current interest rate, remaining balance, original loan term, and any prepayment penalties (though these are rare for car loans). Having this information readily available will streamline the comparison process.

Check Your Credit Score and Report

This is paramount. Obtain your credit report from all three major credit bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Review them for any errors that could be negatively impacting your score. Then, get your actual credit scores. Many banks and credit card companies now offer free access to your FICO score. Based on my experience, catching and correcting inaccuracies can sometimes boost your score by enough points to qualify for a much better rate.

Calculate Your Debt-to-Income Ratio

Add up all your monthly debt payments (car loan, mortgage/rent, credit cards, student loans, etc.). Divide that sum by your gross monthly income (before taxes). This ratio gives you a clear picture of your current financial obligations. If it’s high, it might be an area to address before applying.

Determine Your Car’s Current Value

Use reputable sources like Kelley Blue Book (KBB.com) or NADAguides.com to get an estimate of your car’s trade-in and private party value. This will help you understand your LTV ratio. Knowing your car’s worth ensures you’re not trying to refinance a vehicle that’s "underwater" (where you owe more than it’s worth), which can complicate the process.

Step 2: Improve Your Financial Standing (If Needed)

If your initial assessment reveals areas for improvement, taking action now can pay off handsomely in the form of a lower interest rate. Don’t skip this step if your goal is truly to save money.

Boost Your Credit Score

- Pay Bills On Time: Payment history is the biggest factor in your credit score. Make sure all your payments are made punctually.

- Reduce Credit Card Debt: Lowering your credit utilization ratio (the amount of credit you’re using compared to your total available credit) can significantly improve your score. Aim to keep it below 30%.

- Avoid New Credit Applications: Each new application can result in a hard inquiry, which temporarily dings your score. Hold off on opening new credit lines if you’re planning to refinance your car.

Lower Your Debt-to-Income Ratio

If your DTI is high, consider paying down other debts, even small ones, before applying for a refinance. Alternatively, if possible, look for ways to increase your income. Even a temporary boost can help improve this ratio in the short term.

Save for a Lump Sum Payment

If your LTV ratio is high (you owe more than your car is worth), consider making a lump sum payment to reduce your principal balance. This can bring your LTV into a more favorable range, making lenders more comfortable offering you a better rate.

Step 3: Research and Gather Offers – Shop Around Like a Pro

Now that you’re prepared, it’s time to become an educated consumer. This is where you actively seek out the best possible deals.

Contact Your Current Lender First

Sometimes, your existing lender might be willing to offer you a better rate to retain your business. It’s a quick and easy starting point, and you already have an established relationship. However, don’t stop here.

Explore Other Banks, Credit Unions, and Online Lenders

This is where the real savings often lie. Don’t limit yourself to just one type of institution.

- Banks: Traditional banks offer competitive rates, especially if you have an existing relationship with them.

- Credit Unions: Often known for their member-focused approach and potentially lower rates, credit unions are excellent options. Many have open membership requirements.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others specialize in car loan refinancing. They often have streamlined application processes and can offer very competitive rates, especially for those with good credit.

Pro tips from us: Apply to several lenders within a short timeframe (usually 14-45 days, depending on the credit scoring model). This will be treated as a single hard inquiry on your credit report, minimizing the impact while allowing you to compare multiple offers without penalty. Common mistakes to avoid are applying over a long period, which could cause multiple hard inquiries and negatively affect your score.

For a deeper dive into choosing the right lender, see our article on .

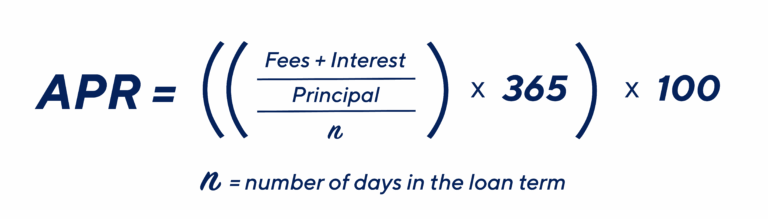

Compare Rates, Terms, and Fees

Don’t just look at the interest rate. Compare the Annual Percentage Rate (APR), which includes the interest rate plus any fees. Also, scrutinize the loan term, monthly payment, and any associated fees (origination fees, prepayment penalties, etc.). Make sure you’re comparing apples to apples.

Step 4: The Application Process – What to Expect

Once you’ve identified a few promising offers, it’s time to formally apply. This step is relatively straightforward if you’ve done your prep work.

Required Documents

Lenders will typically ask for:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs, tax returns, or bank statements.

- Proof of Residence: Utility bill or lease agreement.

- Current Car Loan Information: Your existing loan statement or payoff letter.

- Vehicle Information: Registration, title, and sometimes insurance details.

Understanding the Application Form

Be thorough and accurate when filling out applications. Any discrepancies could delay the process or lead to rejection. Be prepared for a hard credit inquiry once you submit your formal application, which will temporarily lower your score by a few points.

Step 5: Negotiate and Finalize – Don’t Be Afraid to Ask!

You’ve done the hard work; now it’s time to secure the best deal.

Leverage Competing Offers

If you have multiple pre-approvals, use them as leverage. If one lender offered you X% and another offered Y%, go back to your preferred lender and ask if they can beat or match the lower rate. Based on my years in finance, lenders often have a little wiggle room, especially if they know they’re competing for your business.

Understand the New Loan Terms Fully

Before signing anything, meticulously review the new loan agreement. Ensure the interest rate, monthly payment, loan term, and any fees match what you were promised. Pay close attention to the total amount you will pay over the life of the loan.

Read the Fine Print

Don’t rush through the documents. Understand all clauses, including what happens if you miss a payment, late fees, and any other conditions. If something is unclear, ask for clarification. It’s your right as a borrower.

When Might Renegotiating Not Be Right For You?

While refinancing is often beneficial, there are scenarios where it might not be the best move.

- Too Far Into the Loan Term: If you’re nearing the end of your original loan, the amount of interest you’re paying is already minimal, and refinancing might not yield significant savings to justify the new fees.

- Negative Equity (Upside Down): If you owe significantly more than your car is worth, finding a lender willing to refinance might be difficult, or the new terms might not be favorable.

- High Refinancing Fees Outweigh Savings: Always calculate if the money you save in interest truly outweighs any new fees associated with the refinance.

- Credit Score Hasn’t Improved (Or Has Worsened): If your credit profile hasn’t improved since your original loan, you’re unlikely to get a better rate.

Pro Tips for Long-Term Car Loan Management

Securing a better rate is a fantastic achievement, but managing your loan effectively long-term is equally important.

- Set Up Automatic Payments: This ensures you never miss a payment, protecting your credit score and avoiding late fees.

- Consider Extra Payments: If you can afford it, making extra payments towards the principal can further reduce the total interest paid and shorten your loan term. Even rounding up your payment each month can make a difference.

- Maintain Your Vehicle: A well-maintained car retains its value better, which is beneficial if you ever need to refinance again or sell the vehicle.

- Regularly Review Your Financial Health: Periodically check your credit score and review your budget. Staying on top of your finances empowers you to make informed decisions.

For comprehensive financial planning advice, a trusted resource like the Consumer Financial Protection Bureau offers valuable insights: .

Common Mistakes to Avoid When Renegotiating Your Car Loan

- Not Checking Your Credit Score: Going into the process blind can lead to disappointment or missed opportunities.

- Only Contacting One Lender: Failing to shop around means you’re likely leaving money on the table.

- Ignoring Fees: Focus on the total cost of the loan, not just the interest rate.

- Extending the Loan Term Too Much: While it lowers monthly payments, a significantly longer term can lead to paying much more in interest over time.

- Not Understanding the New Terms: Always read and comprehend every detail before signing.

Conclusion: Take Control of Your Car Loan Today!

Renegotiating your car loan interest rate might seem daunting at first, but with the right approach, it’s a powerful tool for financial empowerment. By assessing your situation, improving your financial standing, diligently shopping around, and understanding the fine print, you can significantly reduce your financial burden and free up valuable funds.

Don’t let a high interest rate hold you back. The potential for substantial savings is real, and the process is more accessible than you might think. Start assessing your current loan today, gather your documents, and take the proactive steps outlined in this guide. Your wallet – and your peace of mind – will thank you for it. Empower yourself, save money, and drive confidently knowing you’ve secured the best possible deal.