Unlock the Best Pffcu Used Car Loan Rates: A Comprehensive Guide to Smart Financing

Unlock the Best Pffcu Used Car Loan Rates: A Comprehensive Guide to Smart Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car can be both exciting and daunting. While the thrill of finding the perfect vehicle is undeniable, navigating the world of financing often brings a wave of questions: Where can I find the best rates? What factors influence my loan terms? And how can I ensure I’m making a truly smart financial decision? For many, especially those in the police and fire communities and their families, Police and Fire Federal Credit Union (Pffcu) emerges as a beacon of trust and competitive rates.

This comprehensive guide is designed to demystify Pffcu used car loan rates, walk you through the entire application process, and equip you with the knowledge to secure the most favorable terms possible. Our goal is to transform your car buying experience from a source of stress into an empowering journey, ensuring you drive away not just with a great car, but also with a loan that truly fits your budget. Let’s dive deep into how Pffcu can be your ultimate partner in financing your next used vehicle.

Unlock the Best Pffcu Used Car Loan Rates: A Comprehensive Guide to Smart Financing

Understanding Pffcu: Your Trusted Financial Partner

Before we delve into the specifics of used car loan rates, it’s crucial to understand what Pffcu stands for and why it’s a preferred choice for many. Pffcu, or Police and Fire Federal Credit Union, is not just another financial institution; it’s a member-owned cooperative dedicated to serving its community. This fundamental difference sets credit unions apart from traditional banks.

As a credit union, Pffcu’s primary focus is on its members, not external shareholders. This member-centric approach often translates into more competitive loan rates, lower fees, and a more personalized banking experience. When you apply for a loan with Pffcu, you’re not just a customer; you’re a part-owner, and your financial well-being is their priority. This cooperative model frequently allows them to offer rates that are significantly more attractive than those found at many commercial banks.

Who Can Join Pffcu?

A common question is about eligibility. Pffcu primarily serves active and retired police and fire personnel, their families, and certain related employee groups within specific geographic areas. However, their field of membership has expanded over time. If you’re unsure about your eligibility, it’s always best to check their official website or contact them directly. Joining a credit union like Pffcu means gaining access to a wide array of financial products and services tailored to benefit its members.

Demystifying Pffcu Used Car Loan Rates

The interest rate you secure on a used car loan can significantly impact your monthly payments and the total cost of your vehicle over time. Pffcu, like other lenders, determines its used car loan rates based on a combination of factors. Understanding these elements is key to preparing yourself and securing the best possible offer.

What Influences Your Pffcu Used Car Loan Rate?

Several critical factors come into play when Pffcu calculates your personalized loan rate. Being aware of these can help you strategize and potentially improve your financial standing before applying.

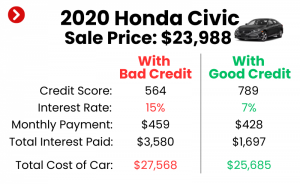

- Your Credit Score: This is arguably the most significant factor. Your credit score, often a FICO or VantageScore, is a numerical representation of your creditworthiness. It tells lenders how responsibly you’ve managed debt in the past. A higher credit score (generally 700+) indicates a lower risk to the lender, typically resulting in lower interest rates. Conversely, a lower score might lead to higher rates to offset the perceived risk.

- Loan Term: The loan term refers to the length of time you have to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72 months). Shorter loan terms often come with lower interest rates because the lender’s risk exposure is reduced. While shorter terms mean higher monthly payments, they also mean less total interest paid over the life of the loan. Longer terms, while reducing monthly payments, typically carry higher interest rates and accumulate more interest over time.

- Loan Amount: The total amount you wish to borrow for the used car also plays a role. Pffcu will assess this in relation to the vehicle’s market value and your ability to repay. Borrowing an amount that is disproportionately high compared to your income or the car’s worth might affect the rate.

- Down Payment: Making a substantial down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. A larger down payment can often lead to a more favorable interest rate. It also shows the lender your commitment to the purchase and your financial stability.

- Vehicle Age and Mileage: For used car loans, the age and mileage of the vehicle are important considerations. Older vehicles with higher mileage are generally considered a higher risk by lenders, as they may be more prone to mechanical issues and depreciation. This can sometimes result in slightly higher interest rates compared to financing a newer used car.

- Interest Rate Type: Pffcu primarily offers fixed-rate auto loans. This means your interest rate, and consequently your monthly payment (excluding any insurance or taxes rolled into the loan), will remain constant throughout the loan term. This provides predictability and makes budgeting easier, which is a significant advantage for borrowers.

How Pffcu’s Rates Compare: The Credit Union Advantage

Based on my experience in the financial sector, credit unions like Pffcu are renowned for their competitive interest rates. Because they operate as non-profits for the benefit of their members, they often have lower operating costs and can pass those savings on in the form of lower loan rates. This is a significant advantage when financing a used car, as even a small difference in the interest rate can save you hundreds, if not thousands, of dollars over the loan term.

Pro Tip: Always check Pffcu’s official website for their most current used car loan rates. These rates can fluctuate based on market conditions, and their site will always have the up-to-date information. While I cannot provide live rates here, you can find them directly at their auto loan section: Pffcu Auto Loans (Please replace this with the actual, current Pffcu auto loan page URL when publishing). Remember that the rates advertised are usually for applicants with excellent credit; your specific rate will depend on your individual credit profile and the factors mentioned above.

The Pffcu Used Car Loan Application Process: A Step-by-Step Guide

Navigating the application process for a used car loan with Pffcu is designed to be straightforward and supportive. Understanding each step can help you prepare thoroughly and ensure a smooth experience.

1. Pre-Approval: Your Strategic Advantage

Getting pre-approved for a used car loan is one of the smartest moves you can make before even stepping foot on a dealership lot. Pre-approval gives you a clear understanding of how much you can borrow, what your interest rate will likely be, and what your estimated monthly payments will look like. This knowledge empowers you.

With a pre-approval in hand, you become a cash buyer in the eyes of the dealership. This means you can focus solely on negotiating the car’s price, rather than getting entangled in financing discussions that might distract from securing the best deal on the vehicle itself. It also provides a valuable benchmark, allowing you to compare any financing offers from the dealership against your Pffcu pre-approval.

2. Gathering Your Documents

To ensure a swift application process, it’s wise to have all necessary documents ready. While the exact requirements might vary slightly, here’s a general list of what Pffcu will likely request:

- Proof of Identity: A valid government-issued photo ID (e.g., driver’s license, state ID, passport).

- Proof of Income: Recent pay stubs (typically the last 2-3 months), W-2 forms, tax returns (especially if self-employed), or other documentation verifying your stable income.

- Proof of Residency: Utility bills, lease agreements, or mortgage statements that confirm your current address.

- Vehicle Information (for final approval): Once you’ve chosen your used car, you’ll need details such as the VIN (Vehicle Identification Number), make, model, year, mileage, and purchase price. Pffcu may also require a bill of sale or buyer’s order from the dealership.

Having these documents organized and readily available will prevent delays and streamline your application.

3. Submitting Your Application

Pffcu offers convenient options for submitting your used car loan application:

- Online: Their website typically features a secure online application portal, allowing you to apply from the comfort of your home.

- In-Person: Visiting a Pffcu branch allows you to speak directly with a loan officer who can guide you through the process and answer any questions.

- By Phone: You might also have the option to apply over the phone with a Pffcu representative.

After submission, Pffcu’s lending team will review your information, conduct a credit check, and assess your financial standing. They might contact you for additional information or clarification if needed.

4. Loan Approval & Funding

Once your application is approved, Pffcu will provide you with the final loan terms, including your approved interest rate, monthly payment, and total loan amount. It’s crucial to carefully read and understand all aspects of the loan agreement before signing. Don’t hesitate to ask questions if anything is unclear.

Upon your acceptance of the terms, Pffcu will arrange for the disbursement of funds. If you’re purchasing from a dealership, the funds are often sent directly to the dealer. If it’s a private party sale, the funds might be issued to you to complete the purchase. The entire process, from application to funding, can often be completed efficiently, especially with all your documents in order.

Maximizing Your Chances for the Best Pffcu Used Car Loan Rates

Securing a low interest rate on your used car loan can save you a substantial amount of money over the life of the loan. Here are some actionable strategies to help you maximize your chances of getting the best Pffcu used car loan rates.

1. Improve Your Credit Score

Your credit score is paramount. Taking steps to boost it before applying for a loan can significantly impact the rate you receive.

- Pay Bills On Time: Payment history is the biggest factor in your credit score. Make sure all your credit card bills, utility payments, and other loan payments are made punctually.

- Reduce Existing Debt: Lowering your credit utilization (the amount of credit you’re using compared to your total available credit) can improve your score. Aim to keep credit card balances below 30% of your credit limit.

- Check Your Credit Report for Errors: Obtain free copies of your credit report from Equifax, Experian, and TransUnion annually. Dispute any inaccuracies, as these can negatively affect your score. Even small errors can make a difference.

2. Save for a Down Payment

A larger down payment is a powerful tool. It reduces the amount you need to borrow, which lowers the lender’s risk.

- Benefits: A significant down payment can lead to a lower interest rate, smaller monthly payments, and less interest paid over the loan term. It also provides you with immediate equity in the vehicle, which is a great financial position.

- Recommendation: Aim for at least 10-20% of the car’s purchase price as a down payment if possible.

3. Choose the Right Loan Term

While longer loan terms mean lower monthly payments, they often come with higher interest rates and more total interest paid.

- Based on my experience, many borrowers are tempted by the lowest monthly payment, but this can be a false economy. A shorter loan term (e.g., 36 or 48 months) might have a higher monthly payment, but it will almost certainly result in less overall interest paid.

- Balance: Find a balance between a monthly payment you can comfortably afford and a loan term that minimizes the total cost of the loan. Pffcu’s loan officers can help you explore different scenarios.

4. Consider a Co-Signer (If Necessary)

If your credit score is fair or you have limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a better rate.

- When to Consider: This is particularly useful for young borrowers or those rebuilding credit.

- Risks: Be aware that a co-signer is equally responsible for the loan. If you miss payments, it negatively impacts both your credit scores. Ensure open communication and a clear understanding of responsibilities.

5. Negotiate Wisely at the Dealership

Armed with your Pffcu pre-approval, you have a strong negotiating position.

- Separate Negotiations: Always negotiate the price of the car first, independently of the financing. Once you agree on a price, then you can discuss financing.

- Common Mistakes to Avoid Are: letting the dealership roll negative equity from your trade-in into a new loan, or focusing solely on the monthly payment without understanding the total cost of the loan. Always look at the full purchase price and the APR (Annual Percentage Rate) offered.

- Compare Offers: Use your Pffcu pre-approval as leverage. If the dealership can beat Pffcu’s rate, ensure it’s a genuine offer with no hidden fees or extended loan terms.

Beyond the Rates: Additional Benefits of Pffcu Used Car Loans

While competitive rates are a major draw, Pffcu offers several other advantages that make them an excellent choice for financing a used car. These benefits contribute to a more positive and secure borrowing experience.

- Personalized Service: As a member-owned institution, Pffcu prides itself on offering personalized service. You’re not just a number; loan officers are often more accessible and willing to work with you to find solutions tailored to your unique financial situation.

- No Hidden Fees: Credit unions are generally known for their transparency. Unlike some traditional lenders, Pffcu is less likely to surprise you with unexpected fees or complex charges, making your loan terms clearer and more straightforward.

- Convenient Payment Options: Pffcu typically offers a range of convenient ways to make your loan payments, including online banking, automatic transfers, phone payments, and in-person options. This flexibility ensures you can manage your loan efficiently.

- Potential for Member Discounts/Rewards: Being a Pffcu member can unlock access to other benefits, such as lower rates on other loan products, higher savings yields, or even exclusive member discounts on various services, further enhancing the value of your membership.

- Refinancing Options: If you already have a car loan with another institution and your credit score has improved, or if market rates have dropped, Pffcu often provides competitive refinancing options. Refinancing with Pffcu could potentially lower your interest rate and monthly payments, saving you money over the remaining loan term. (For more details on this, you might find our article on Refinancing Your Car Loan Effectively helpful.)

Real-World Scenarios and Case Studies

Let’s illustrate how different factors can impact Pffcu used car loan rates with a couple of hypothetical scenarios:

Scenario 1: Sarah, Excellent Credit

Sarah has a credit score of 780, a stable job, and is making a 20% down payment on a $20,000 used car. She applies for a 48-month loan with Pffcu. Due to her excellent credit and substantial down payment, Pffcu offers her their lowest advertised rate, perhaps 4.99% APR. Her monthly payments are manageable, and she pays minimal interest over the loan term.

Scenario 2: Mark, Good Credit with Lower Down Payment

Mark has a credit score of 680, a steady income, but can only afford a 5% down payment on the same $20,000 used car. He also applies for a 48-month loan. Because his credit score is good but not excellent, and his down payment is smaller, Pffcu might offer him a slightly higher rate, perhaps 6.79% APR. His monthly payment will be higher than Sarah’s, and he will pay more in total interest.

These examples highlight how your individual financial profile directly influences the rates you receive. Preparing thoroughly can make a significant difference.

Frequently Asked Questions (FAQs) About Pffcu Used Car Loans

To further clarify common queries, here are some frequently asked questions about Pffcu used car loans:

Q1: What is the minimum credit score required for a Pffcu used car loan?

A1: Pffcu, like most lenders, does not publicly state a strict minimum credit score. Loan approval depends on a holistic review of your financial profile, including income, debt-to-income ratio, and credit history. While a higher score (e.g., 700+) will generally secure the best rates, Pffcu may approve loans for members with good to fair credit, albeit potentially at a slightly higher interest rate. It’s always best to apply and let them assess your specific situation.

Q2: Can I refinance an existing car loan with Pffcu?

A2: Yes, Pffcu often offers competitive options for refinancing existing auto loans from other financial institutions. If you’ve improved your credit score since you took out your original loan, or if Pffcu’s current rates are lower, refinancing could save you money. It’s a great way to potentially lower your monthly payments or reduce the total interest you’ll pay. (For more on this, check out our guide on Maximizing Your Auto Loan Refinancing Potential).

Q3: What types of used cars does Pffcu finance?

A3: Pffcu typically finances a wide range of used cars, including sedans, SUVs, trucks, and even some recreational vehicles. Generally, they will have specific criteria regarding the vehicle’s age and mileage (e.g., usually less than 7-10 years old and under 100,000-125,000 miles), as well as its overall condition and market value. It’s always best to confirm these specifics with a Pffcu loan officer or check their official loan policies.

Q4: How long does the Pffcu used car loan approval process take?

A4: The approval process for a Pffcu used car loan can be remarkably quick, especially if you have all your documents ready. Many members report receiving pre-approval decisions within hours, or at most, a couple of business days. Final approval and funding typically follow soon after, once all necessary paperwork is completed and the vehicle details are finalized.

Conclusion: Your Path to Smart Used Car Financing with Pffcu

Navigating the landscape of used car financing doesn’t have to be overwhelming. By understanding the factors that influence Pffcu used car loan rates, meticulously preparing your application, and implementing smart financial strategies, you can position yourself to secure the most advantageous terms possible. Pffcu, with its member-focused approach and competitive offerings, stands as an excellent choice for those seeking a reliable and beneficial financing partner.

Remember, an informed decision is a powerful one. Take the time to review your credit, save for a down payment, and get pre-approved before you start shopping. By doing so, you’ll not only unlock the best Pffcu used car loan rates but also empower yourself to make a truly smart and satisfying vehicle purchase. Drive confidently, knowing you’ve made a financially sound choice with a trusted partner like Pffcu. Your journey to owning the perfect used car, with the best possible financing, starts now.