Unlock the Road Ahead: A Comprehensive Guide to TIAA Car Loans

Unlock the Road Ahead: A Comprehensive Guide to TIAA Car Loans Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect, but navigating the complexities of auto financing can often feel daunting. For millions of dedicated professionals in the academic, research, medical, and cultural fields, TIAA stands as a beacon of financial security, primarily known for its retirement planning expertise. However, TIAA’s commitment to its members extends far beyond pensions, offering a suite of banking services, including highly competitive TIAA car loans.

This comprehensive guide is designed to illuminate every facet of securing a TIAA auto loan, ensuring you are equipped with the knowledge to make an informed decision. We’ll delve deep into the unique advantages, eligibility criteria, application process, and expert tips to help you drive away with confidence. Our ultimate goal is to provide you with pillar content that demystifies TIAA vehicle financing, making it accessible and understandable for every reader.

Unlock the Road Ahead: A Comprehensive Guide to TIAA Car Loans

Understanding TIAA: More Than Just Retirement Planning

Before diving into the specifics of car loans, it’s essential to appreciate TIAA’s foundational mission. Established over a century ago, TIAA (Teachers Insurance and Annuity Association of America) was created to provide financial services specifically for those working in the academic, research, medical, and cultural fields. This includes teachers, professors, researchers, public service employees, and many more who dedicate their lives to serving others.

Unlike many traditional banks, TIAA operates with a member-centric philosophy. This unique structure often translates into more advantageous financial products and services for its eligible members. Their focus is not solely on profit maximization, but on the long-term financial well-being of the individuals they serve. This ethos is particularly evident in their banking offerings, including their auto loan products.

Why Consider a TIAA Car Loan? Unpacking the Benefits

When it comes to financing a vehicle, you have a plethora of options. So, what makes a TIAA car loan a standout choice, especially for its eligible members? The advantages are often significant and can lead to substantial savings and a smoother borrowing experience.

1. Competitive Interest Rates

One of the most compelling reasons to explore TIAA auto loan rates is their potential for competitiveness. Based on my experience in the financial sector, institutions that cater to a specific, often financially responsible, member base can frequently offer lower interest rates than broad-market lenders. TIAA leverages its unique structure and understanding of its members’ financial stability to provide attractive rates.

These competitive rates can translate into lower monthly payments and reduced overall interest paid over the life of the loan. Even a seemingly small difference in APR (Annual Percentage Rate) can save you hundreds or even thousands of dollars over a typical five-year car loan term. It’s always wise to compare TIAA’s offerings against other lenders to fully appreciate this benefit.

2. Member-Centric Service and Support

TIAA prides itself on understanding the financial lives of its members. This deep understanding extends to their customer service approach for TIAA vehicle financing. You’re not just another loan applicant; you’re a valued member of a community.

Pro tips from us: This personalized approach often means clearer communication, more flexible problem-solving, and a dedicated team ready to guide you through the process. They are attuned to the specific needs and financial cycles of academic and public service professionals, which can make a significant difference during your car buying journey.

3. Flexible Loan Terms and Options

A one-size-fits-all approach rarely works for financial products. TIAA understands this, offering a range of flexible loan terms designed to fit various budgets and financial goals. Whether you’re looking for a shorter term to pay off your vehicle faster or a longer term to reduce monthly payments, options are typically available.

This flexibility extends to the types of vehicles you can finance, covering new cars, used cars, and even the option to refinance an existing auto loan. Having these choices empowers you to tailor the financing to your personal circumstances, ensuring it aligns with your long-term financial plan.

4. Streamlined Application Process

In today’s fast-paced world, convenience is paramount. TIAA has invested in making the application for a TIAA car loan as straightforward and efficient as possible. Many aspects of the application can be completed online, from initial inquiry to final submission.

This streamlined process minimizes paperwork and reduces the time spent waiting for approval. Based on my years of observing financial applications, a simple, clear process significantly reduces stress for borrowers and accelerates the path to vehicle ownership.

5. Refinancing Opportunities

For those who already have a car loan but are looking for better terms, TIAA also offers refinancing options. This can be a game-changer if interest rates have dropped since you took out your original loan, or if your credit score has significantly improved. Refinancing with TIAA could lead to a lower interest rate, a reduced monthly payment, or even a shorter loan term.

We will explore refinancing in more detail later, but it’s a crucial benefit for existing car owners within the TIAA community. It demonstrates TIAA’s commitment to supporting your financial well-being throughout your entire car ownership experience.

Who is Eligible for a TIAA Car Loan? Navigating Membership

The primary criterion for accessing a TIAA car loan is eligibility for TIAA products and services. TIAA was founded to serve specific sectors, and their banking services, including auto loans, typically follow these guidelines.

Eligibility generally extends to:

- Employees of educational institutions: This includes colleges, universities, K-12 schools, and related educational organizations.

- Employees of research organizations: Individuals working for research institutes and scientific bodies.

- Employees of medical institutions: Healthcare professionals and staff at hospitals and medical centers.

- Employees of cultural institutions: Staff at museums, libraries, foundations, and other non-profit cultural organizations.

- Public service employees: Depending on specific affiliations, certain public sector employees may also qualify.

Pro tip from us: It’s crucial to verify your eligibility early in the process to avoid any delays. The easiest way to confirm if you qualify is to visit the TIAA Bank website or contact their customer service directly. They can quickly ascertain your eligibility based on your employer or professional affiliation. While the focus is on direct employees, sometimes family members or retirees from these institutions might also have access to certain benefits, so it’s always worth checking.

The Application Process: A Step-by-Step Guide

Securing a TIAA auto loan doesn’t have to be complicated. By understanding the process and preparing adequately, you can ensure a smooth and successful application.

Step 1: Pre-Approval – Your Strategic First Move

One of the smartest steps you can take is to get pre-approved for a car loan before you even step foot in a dealership. Pre-approval gives you a clear understanding of how much you can borrow and at what interest rate. This financial clarity empowers you to negotiate confidently, knowing your budget and financing terms upfront.

To get pre-approved, TIAA will typically conduct a soft credit inquiry, which doesn’t impact your credit score. They’ll ask for basic financial information to give you an estimate. Once you’re ready for a firm offer, a hard inquiry will be made.

Step 2: Gathering Your Essential Documents

Preparation is key to a swift application. Common mistakes to avoid include not having all your documents ready, which can significantly delay the approval process. Based on my experience, having these documents organized beforehand makes a huge difference.

You’ll generally need:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs, W-2s, or tax returns (if self-employed).

- Proof of Employment: Verification of your current employer and position, aligning with TIAA’s eligibility.

- Credit History: While TIAA will pull your credit report, it’s good to know your score beforehand.

- Vehicle Information: Once you’ve chosen a car, you’ll need details like the VIN, make, model, year, and selling price.

Step 3: Submitting Your TIAA Car Loan Application

With your documents in hand and a car in mind, you can proceed with the formal application. TIAA typically offers multiple ways to apply:

- Online: This is often the quickest and most convenient method, allowing you to upload documents digitally.

- By Phone: You can speak with a TIAA loan specialist who will guide you through the application over the phone.

- In-Person: If TIAA has a local branch, you might be able to apply in person, though this is less common for auto loans specifically.

Ensure all information provided is accurate and complete to avoid any discrepancies that could hold up your application.

Step 4: Review and Approval Process

Once your application is submitted, TIAA’s underwriting team will review your financial information, credit history, and eligibility. They will assess your ability to repay the loan based on your income, debt-to-income ratio, and creditworthiness.

The approval timeline can vary, but TIAA generally strives for efficiency. You might receive a decision within a few business days, or sometimes even sooner. If additional information is needed, they will contact you directly.

Step 5: Funding and Finalization

Upon approval, you will receive your final loan offer, detailing the interest rate, term, and monthly payment. Once you accept these terms, TIAA will work with you to finalize the necessary paperwork.

The funds for your TIAA car loan are typically disbursed directly to the dealership or, in the case of a private sale or refinance, to you or the previous lender. You’ll then be ready to drive off in your new vehicle, confident in your financing choice.

TIAA Car Loan Rates and Terms: What to Expect

The interest rate and terms you receive on your TIAA auto loan are influenced by several factors. Understanding these elements can help you prepare and potentially secure the most favorable deal.

Factors Influencing Your Rate:

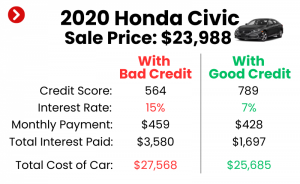

- Credit Score: Your credit score is perhaps the most significant factor. A higher credit score (generally 700+) indicates a lower risk to lenders, often resulting in lower interest rates.

- Loan Term: Shorter loan terms (e.g., 36 or 48 months) typically come with lower interest rates because the lender’s risk is spread over a shorter period. Longer terms (e.g., 60 or 72 months) often have higher rates but lower monthly payments.

- Down Payment: A larger down payment reduces the amount you need to borrow, which can lower your monthly payments and sometimes lead to a better interest rate. It also signals your financial commitment to the vehicle.

- Vehicle Type: New car loans often have slightly lower rates than used car loans, as new vehicles typically hold their value better initially.

- Debt-to-Income Ratio: TIAA will assess your current debt obligations relative to your income. A lower ratio indicates greater capacity to handle new debt.

It’s important to understand the difference between an interest rate and APR. The interest rate is the cost of borrowing money, while the APR includes the interest rate plus any additional fees associated with the loan. Always focus on the APR for the most accurate comparison of total borrowing costs. For more detailed information on auto loan financing, you can refer to trusted external sources like the Consumer Financial Protection Bureau .

Comparing TIAA Car Loans: How Do They Stack Up?

In the competitive landscape of auto financing, it’s natural to wonder how a TIAA car loan compares to other options. Let’s briefly examine the key distinctions.

- Traditional Banks: Large commercial banks offer a wide range of auto loans, but their rates might not always be as competitive as TIAA’s for eligible members. Their service can sometimes feel less personalized.

- Credit Unions: Credit unions are often compared to TIAA due to their member-owned structure. They frequently offer excellent rates and personalized service. If you’re eligible for both, it’s worth comparing TIAA’s specific offers against your local credit union.

- Dealership Financing: While convenient, dealership financing sometimes includes markups or less transparent terms. It’s often beneficial to arrive at the dealership with pre-approved financing from TIAA, giving you leverage in negotiations.

The unique selling proposition of TIAA for its members lies in its specialized focus. They understand the financial nuances of academics and public servants, potentially leading to tailored products and a more empathetic lending approach that might not be found at larger, more generalized institutions.

Refinancing Your Car Loan with TIAA: A Smart Move?

If you already have a car loan, but your financial situation has improved, or interest rates have dropped since you originally financed, refinancing with a TIAA car loan could be a very smart financial decision.

When is Refinancing Beneficial?

- Lower Interest Rates: If TIAA can offer you a significantly lower interest rate than your current loan, you’ll save money on interest over time.

- Lower Monthly Payments: By extending your loan term (though this might mean paying more interest overall) or securing a lower rate, you can reduce your monthly outflow, freeing up cash for other priorities.

- Shorter Loan Term: If your financial situation has improved, you might be able to afford higher monthly payments to pay off your car faster, saving you substantial interest.

- Remove a Co-signer: If your credit has improved, you might be able to refinance in your name only, releasing a co-signer from their obligation.

The process for refinancing with TIAA is similar to applying for a new loan. You’ll need to provide personal and financial information, and details about your current loan and vehicle. TIAA will then assess your eligibility and offer new terms. Pro tips from us: Always calculate the total cost of the new loan, including any fees, against the remaining cost of your old loan to ensure it’s truly a beneficial move.

Pro Tips for Securing the Best TIAA Car Loan

Based on my years of helping individuals navigate vehicle financing, these strategies consistently lead to better outcomes. Applying for a TIAA car loan is an excellent start, but these tips can help you optimize your experience even further.

- Boost Your Credit Score: Before applying, take steps to improve your credit score. Pay down existing debts, dispute any errors on your credit report, and avoid opening new credit accounts. A higher score directly translates to lower interest rates.

- Save for a Down Payment: A larger down payment reduces the loan amount, lowers your monthly payments, and can secure a better interest rate. It also provides equity in your vehicle from day one.

- Shop Around (Even with TIAA): While TIAA offers competitive rates, it’s always wise to compare their final offer with other lenders (especially credit unions) if you are eligible. This ensures you’re getting the absolute best deal available to you.

- Negotiate the Car Price, Not Just the Loan: Remember, your loan is tied to the price of the car. Focus on negotiating the vehicle’s purchase price first. A lower purchase price means you need to borrow less, resulting in a smaller loan amount and lower overall costs.

- Understand the Fine Print: Always read all loan documents thoroughly before signing. Understand the interest rate, APR, loan term, monthly payment, and any fees or penalties for early repayment. Don’t hesitate to ask questions if anything is unclear.

Common Misconceptions About TIAA Car Loans

Many people hold common misconceptions about specialized lenders like TIAA. Let’s address a few:

- Myth: TIAA only offers retirement products.

- Reality: While retirement is a core focus, TIAA also provides a full suite of banking services, including checking, savings, mortgages, and TIAA car loans.

- Myth: Their loans are only for the highest-paid academics.

- Reality: Eligibility is based on employment within specific sectors, not necessarily income level. TIAA aims to serve a broad spectrum of eligible professionals.

- Myth: Applying is complicated due to their specialized nature.

- Reality: TIAA has worked to streamline its application processes, making them as user-friendly as any other modern financial institution.

Conclusion: Drive Your Dream Car with TIAA Confidence

For eligible members, a TIAA car loan represents a compelling option for financing your next vehicle. With its commitment to competitive rates, member-centric service, flexible terms, and streamlined processes, TIAA offers a distinct advantage over many traditional lenders. By leveraging your eligibility and following our expert tips, you can secure favorable financing that aligns with your financial goals.

Don’t let the process of buying a car overshadow the joy of owning one. Explore the unique benefits that TIAA offers to its dedicated community. Take the first step today by visiting the TIAA Bank website to check your eligibility and discover how a TIAA auto loan can put you in the driver’s seat with confidence and peace of mind. Your journey to a new car, backed by a trusted partner, starts here.